Inflation/Deflation

In lieu of next week’s report, I will be presenting the quarterly Counterpoint webcast titled ‘Where Is The Groupthink Wrong? And How To Profit From It.’ I do hope you can join. We will then take a summer break, so our next report will come out on August 5. Highlights The quantum theory of finance describes the strange quantum effects of ultra-low inflation, of ultra-low interest rates, and of ultra-low probabilities. The key finding of the quantum theory of finance is that when inflation and interest rates get ultra-low, inflation becomes completely insensitive to monetary policy, while risk-asset valuations become hyper-sensitive to monetary policy. The hyper-sensitivity of $500 trillion of global risk-assets to bond yields means that the ultimate low in the US T-bond yield is still to come. Given the hyper-sensitivity of equity valuations to bond yields and the demand for US assets during bond market rallies, it also means that the structural bull market in equities and the structural bull market in the US dollar are both still intact. Feature Feature ChartNear The Lower Bound In Bond Yields, Potential Losses Are Greater Than Potential Gains

Near The Lower Bound In Bond Yields, Potential Losses Are Greater Than Potential Gains

Near The Lower Bound In Bond Yields, Potential Losses Are Greater Than Potential Gains

When things get ultra-small, the laws of physics undergo a radical shift. Classical physics breaks down, and we must to turn to an alternative theory to explain and predict the physical world. That theory is the quantum theory of physics. In this updated Special Report we propose that, just as there is the quantum theory of physics, there is The Quantum Theory Of Finance. When inflation and interest rates get ultra-low, the laws of economics and finance undergo a radical shift. And we must turn to the alternative theory to explain and predict the economic and financial world. In the physical world, the allowable values of a physical system appear to be continuous, with all values permitted. In fact, the permitted values occur in discrete ‘quanta’. At ultra-small scales, these quantum effects become the dominant driver of physical systems and form the foundation of the quantum theory of physics. Likewise, in the economic and financial world of ultra-low inflation and interest rates, quantum effects become the dominant drivers of the system. These quantum effects take three forms: The quantum effects of ultra-low inflation. The quantum effects of ultra-low interest rates. The quantum effects of ultra-low probabilities. The Quantum Effects Of Ultra-Low Inflation Even though inflation is continuous mathematically, we do not perceive it as such psychologically. Instead we perceive inflation as ‘quantum states’ of either price stability or price instability. A recent IFO paper points out that households’ inflation perceptions are “more in line with the imperfect information view prevailing in social psychology than with the rational actor view assumed in mainstream economics.”1 And in Real-Feel Inflation: Quantitative Estimation of Inflation Perceptions, Michael Ashton confirms that “it would be challenging for a consumer to distinguish 1 percent inflation from 2 percent inflation – that fine of a gradation in perception would be extremely unusual to find.”2 There are several reasons why we perceive inflation imprecisely: We do not recognise quality change and substitution adjustments. We tend to feel inflation asymmetrically, noticing goods whose prices are rising, but noticing less goods whose prices are falling. This is the classic attribution bias: higher prices are inflation, lower prices are “good shopping.” Items whose prices are volatile tend to draw more attention, and give more opportunities for these asymmetries to compound. We notice the price changes of small, frequently purchased items more than the price changes of large infrequently purchased items. We perceive the cost of homeownership as the monthly mortgage payment, and not the imputed cost of owners’ equivalent rent (OER). Yet OER is the largest single item in the US core CPI basket, weighted at 30 percent. The result of these biases is that we perceive inflation intuitively, as a quantum state rather than as a precise number within a continuum. The quantum effects of ultra-low inflation mean that policymakers can take an economy from the state of price instability to the state of price stability, and vice-versa, but they cannot sustainably hit an arbitrary inflation target within the quantum state, such as 2 percent (Chart I-2). Chart I-2Mission Impossible: 2 Percent Inflation

Mission Impossible: 2 Percent Inflation

Mission Impossible: 2 Percent Inflation

The Quantum Effects Of Ultra-Low Interest Rates Policymakers accept that there exists an interest rate, at around -1 percent, below which there would be an exodus of bank deposits. Hence, this marks the lower bound of policy interest rates. When policy interest rates are at, or near, this lower bound, central banks can turn to a second strategy: they can promise to keep the policy rate ultra-low for an extended period. Thereby they can pull down the long bond yield towards the lower bound too. To do this, they must convince the market that their promise is genuine. Enter quantitative easing (QE) which, in the words of the ECB’s former Chief Economist Peter Praet, is nothing more than “a signalling channel which reinforces the credibility of forward guidance on (ultra-low) policy rates.” Once forward guidance plus QE has taken bond yields close to their lower bound, we start to see the quantum effects of ultra-low interest rates. Specifically, the bond investor is left with a highly asymmetric payoff – the bond price can fall much more than it can rise. Witness the performance of Swiss bonds through the past three years. The worst drawdowns have far exceeded the best gains (Feature Chart, Chart I-3 and Chart I-4). Chart I-3Swiss Bonds Offer Small Potential Gains...

Swiss Bonds Offer Small Potential Gains...

Swiss Bonds Offer Small Potential Gains...

Chart I-4...But Big Potential Losses

...But Big Potential Losses

...But Big Potential Losses

This asymmetric payoff is technically known as negative skew and it starts to take effect when bond yields decline to around 2 percent above their lower bound. So, if the lower bound for the 10-year T-bond yield is -0.5 percent, the negative skew in its payoffs would start to take effect at around 1.5 percent. One important implication of the quantum effect of ultra-low interest rates is that the asymmetry of bond payoffs becomes very similar to the asymmetry of equity and other risk-asset payoffs (Chart I-5). This is important because, as we describe in the next section, it is the skew of an asset’s payoff that establishes its absolute and relative riskiness. Chart I-5Equities Can Suffer Bigger Short-Term Losses Than Short-Term Gains (Negative Skew)

Equities Can Suffer Bigger Short-Term Losses Than Short-Term Gains (Negative Skew)

Equities Can Suffer Bigger Short-Term Losses Than Short-Term Gains (Negative Skew)

The Quantum Effects Of Ultra-Low Probabilities We are very bad at comprehending low probabilities. For example, we cannot distinguish a 1 in a 1000 risk from a 1 in a 100 risk, even though the second risk is ten times greater than the first. This is what Daniel Kahneman’s and Amos Tversky’s Nobel prize winning Prospect Theory called the ‘quantal effect’ of ultra-low probabilities. Kahneman and Tversky discovered that our fears and hopes come in quanta rather than in a continuum, with the result that we overweight the tail-events in a payoff distribution. “Because people are limited in their ability to comprehend and evaluate extreme probabilities, highly unlikely events are either ignored or over-weighted.” If the payoff distribution is symmetric, then our overweighting of the positive and negative tails cancels out, meaning there is no impact on the value of the payoff (Figure I-1). However, if the payoff distribution is skewed, then the longer tail dominates our perceived value of the payoff. Figure I-1In A Symmetric Payoff, We Overestimate The Big Gain And the Big Loss Equally, So It Cancels Out

The Quantum Theory Of Finance (Part 2)

The Quantum Theory Of Finance (Part 2)

A lottery payoff has an extreme positive skew. There exists a miniscule chance of winning a fortune. As we overweight this highly unlikely event, we overvalue the lottery ticket relative to its expected payoff (Figure I-2). And this explains the existence of the multi-billion dollar lottery industry. Figure I-2In A Positively-Skewed Payoff (Lottery), We Overestimate The Big Gain, So We Overpay

The Quantum Theory Of Finance (Part 2)

The Quantum Theory Of Finance (Part 2)

Conversely, the payoff from equities has a negative skew. As we overweight the tail-event of losing a lot of money, we undervalue this negatively skewed payoff (Figure I-3). In other words, we demand a higher return from a negatively skewed payoff relative to a symmetrical payoff, such as the payoff from bonds when yields are not ultra-low. And this explains the existence of the so-called ‘equity risk premium.’ Figure I-3In A Negatively-Skewed Payoff (Risk-Assets), We Overestimate The Big Loss, So We Demand A ‘Risk Premium’

The Quantum Theory Of Finance (Part 2)

The Quantum Theory Of Finance (Part 2)

Crucially though, at ultra-low bond yields – when both equity and bond payoffs carry the same negative skew – we no longer demand a higher return from equities versus bonds. As the equity risk premium compresses, the return demanded from equities and other risk-assets collapses to the ultra-low bond yield. Put another way, the valuation of risk-assets soars. The Quantum Theory Of Finance, The Past And The Future The key finding of the quantum theory of finance is this. When inflation and interest rates get ultra-low, inflation becomes completely insensitive to monetary policy, while risk-asset valuations become hyper-sensitive to monetary policy. This is the story of the past decade, and most likely the story of the coming years. For over a decade now, central banks have fixated on hitting their 2 percent inflation targets when the quantum effects of ultra-low inflation make such a target unachievable. In their misguided fixation, the unleashing of trillions of dollars of QE has taken bond yields to unprecedented lows which has driven risk-asset valuations to unprecedented highs, and made them hyper-sensitive to the slightest move in bond yields (Chart I-6 and Chart I-7). Chart I-6Real Estate Prices Have Massively Outperformed Rents

Real Estate Prices Have Massively Outperformed Rents

Real Estate Prices Have Massively Outperformed Rents

Chart I-7Equity Prices Have Massively Outperformed Profits

Equity Prices Have Massively Outperformed Profits

Equity Prices Have Massively Outperformed Profits

Yet to be clear, though policymakers cannot consistently hit the 2 percent inflation target, they could certainly take the economy back to price instability – if they pursued ultra-loose monetary policy combined with ultra-loose fiscal policy aggressively enough for long enough. But if a major economy were to take this road – intentionally or accidentally – the $500 trillion valuation of global risk-assets that is premised on ultra-low inflation and ultra-low interest rates would collapse. As we have previously written, this means that The Road To Inflation Ends At Deflation and the ultimate low in the T-bond yield is still to come. Alternatively, another deflationary shock could take us to this ultimate low in the T-bond yield more directly. Given the hyper-sensitivity of equity valuations to bond yields and the massive portfolio inflows into US assets during shocks, this also means that the structural bull markets in equities and the structural bull market in the US dollar are both still intact. Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 Please see Households’ Inflation Perceptions and Expectations: Survey Evidence from New Zealand, IFO Working Paper, February 2018 available at https://www.ifo.de/DocDL/wp-2018-255-hayo-neumeier-inflation-perceptions-expectations.pdf 2 Please see Real-Feel Inflation: Quantitative Estimation of Inflation Perceptions by Michael Ashton, National Association for Business Economics available at https://link.springer.com/content/pdf/10.1057/be.2011.35.pdf Fractal Trade Update We are pleased to report that long USD/CAD achieved its 3.7 percent profit target, and short building materials (PKB) versus healthcare (XLV) achieved its 15 percent profit target. Combined with other successes, this lifts the 6-month win ratio to an all-time high of 76 percent, comprising 12.3 winners versus just 3.9 losers. This week, we present two new candidates for countertrend reversal. First, the strong recent rally in Australian 30-year bonds has reached fragility on its 65-day fractal structure. The recommended trade is to short Australian versus Canadian 30-year bonds, setting the profit-target and symmetrical stop-loss at 3.9 percent. Second, the strong recent rally in lead versus platinum has also reached fragility on its 65-day fractal structure. The recommended trade is to short lead versus platinum, setting the profit-target and symmetrical stop-loss at 6.4 percent. Chart I-8Short Australian Vs, Canadian 30-Year Bonds

Short Australian Vs, Canadian 30-Year Bonds

Short Australian Vs, Canadian 30-Year Bonds

Chart I-9Short Lead Vs. Platinum

Short Lead Vs. Platinum

Short Lead Vs. Platinum

Fractal Trading System Fractal Trades 6-Month Recommendations Structural Recommendations Closed Fractal Trades Closed Trades Asset Performance Equity Market Performance Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Home prices have risen at a rapid rate over the last year, stirring some fears that a new bust could be in store: The housing market is strong, but price appreciation has not been that significant relative to history and popular concerns appear to be misplaced. Banks and households are on much sounder financial footing than they were before the housing bust: Banks’ exposure to residential mortgages has shrunk and stiffer regulatory requirements have made them more resilient to shocks. Households have been de-levering since the crisis and have accumulated massive excess savings since the pandemic began. The housing market is not oversupplied in the aggregate and does not appear as if it will become oversupplied soon: High prices are a reliable cure for high prices, but the housing supply response has been muted and looks as if it will remain so for the immediate future. The Global Financial Crisis had its roots in debauched underwriting standards that bear no resemblance to today’s mortgage lending environment: Before it spread around the world, the GFC was known as the subprime crisis, but subprime borrowers are almost entirely shut out of today’s residential mortgage market. Feature The state of the housing market was a central concern for investors in the wake of the global financial crisis. That incident was initially known as the subprime crisis, as a new class of loans – subprime mortgages – set a self-reinforcing debt-deflation dynamic into motion. When the music stopped, dedicated mortgage originators and securitizers were out of business, a sizable share of borrowers faced foreclosure and a lot of homes, from freshly built subdivisions to tattered urban blocks, stood empty. Many of the people who were a part of the pipeline – making loans, appraising properties, wholesaling loans, packaging loans into securities, trading securities, and building and selling houses – were thrown out of work. As if the consequences in the real economy weren’t bad enough, the convulsions in the financial markets imperiled the banking system. Record mortgage default rates and plunging collateral values left commercial banks gasping, and highly leveraged investment banks holding unsold securities, as-yet-unpackaged whole loans or other property investments found their capital levels whittled nearly to zero. A high-profile insurer was undone by guaranteeing against the securities’ defaults, but several life insurers were squeezed by the losses they sustained on highly rated securities that turned out to harbor a lot of poorly underwritten loans. The net result of the financial distress was a paucity of investment capital to help the real economy get back on its feet. Elected officials, central bankers, regulators and investors are all understandably wary of a repeat of the crisis and its wide-ranging effects. In his press conference after the FOMC’s April meeting, Chair Powell acknowledged the risks before going on to say that they don’t appear particularly strong right now. “So many of the financial crack-ups … that have happened in the last 30 years have been around housing. We … really don’t see that [financial stability concerns] here. We don’t see bad loans and unsustainable prices and that kind of thing.” This Special Report examines why we concur with the Fed’s view. Investors May Be Jittery, But The Banks Are Steady Chart 1Once Bitten, Twice Shy

Once Bitten, Twice Shy

Once Bitten, Twice Shy

This evening in the States we will get on the phone with an Asia-Pacific client who wants to discuss the following topic: “One of the issues that we are currently exploring is the US housing market. It is exceptionally strong and may create an important medium-term risk for the US and global markets.” Internet users closer to home have also taken note of the housing market’s strength and have their own concerns about it. Google searches for “housing crash” by US users are making new highs, dwarfing the interest the phrase drew ahead of the GFC (Chart 1). While potential homebuyers are understandably wary of getting in at the top, and households who already have mortgages are averse to price declines that would erode the value of their equity, it is the overall financial system’s exposure to US home prices that draws global investors’ attention. Such an overwhelming majority of households borrow to buy their home that single-family homes have traditionally comprised the largest component of banking system collateral (Chart 2). Although US banks have less exposure to residential mortgages than their peers in other major developed economies (Table 1), the housing market poses an outsize risk to financial stability by virtue of the amount of debt financing it. Chart 2Moving Beyond Mortgages

Moving Beyond Mortgages

Moving Beyond Mortgages

Table 1Don't Look At Us

The US Housing Market: Déjà Vu All Over Again?

The US Housing Market: Déjà Vu All Over Again?

Since the GFC, however, the largest banks have sharply reduced their exposure to lending (Chart 3, top panel). They have a disproportionate influence on the state of the overall banking system and their offloading of qualifying loans to Fannie Mae and Freddie Mac have helped the system pare residential real estate loans’ share of total assets to 10%, or half of their pre-GFC weight (Chart 3, bottom panel). The wave of post-GFC regulation has forced systemically important banks to hold more capital against their assets, making them more resilient to shocks and the ordinary vagaries of asset markets and the business cycle. Loans account for less than half of all bank assets, with nearly all the rest going to Treasury and agency securities, cash, property and goodwill and fully collateralized short-term loans (Chart 4). Chart 3Big Banks Have Become Much More Judicious Lenders

Big Banks Have Become Much More Judicious Lenders

Big Banks Have Become Much More Judicious Lenders

Chart 4Risk Off

Risk Off

Risk Off

Bottom Line: The banking system is better capitalized than it was in 2007 and has considerably less exposure to residential real estate loans. The financial system is much less vulnerable to a rupture in the housing market than it was 15 years ago. Better Borrowers, Better Loans Household balance sheets are not a source of vulnerability, either, as they are in far better shape than they were before the GFC. Employment gains, increased savings, lender write-offs and lower debt-service costs helped shore up household finances after the crisis, and the pandemic yielded explosive wealth gains via whopping fiscal transfers, reduced spending options and surging stock and home prices. No previous four-quarter stretch has been better for household net worth gains, nominal (Chart 5, top panel) or real (Chart 5, bottom panel), than the one ended March 31st, and even the five-quarter stretch including last year’s disastrous first quarter was quite strong relative to history, especially in real terms. Households have paid down their outstanding credit card balances, and with interest rates at rock-bottom levels, servicing the debt they have has never been easier (Chart 6). Chart 5The Pandemic Has Been Great For Household Net Worth

The Pandemic Has Been Great For Household Net Worth

The Pandemic Has Been Great For Household Net Worth

Chart 6A Light Yoke

A Light Yoke

A Light Yoke

Chart 7Only Qualified Borrowers Need Apply

The US Housing Market: Déjà Vu All Over Again?

The US Housing Market: Déjà Vu All Over Again?

The improvement in aggregate household financial positions would be of little import if lenders repeated their pre-GFC practices of lending to the weakest candidates in the pool of potential borrowers. Fortunately for financial stability and the health of the housing market, the highest-quality borrowers have been capturing an increasing share of new mortgage loans. In a reversal of the underwriting follies of a decade-and-a-half ago, lenders are shunning subprime and near-prime borrowers in favor of the best credits (Chart 7). The current housing boom has been built on a solid credit foundation. Supplies Are Tight As measured by the Case-Shiller 20-City Index, home prices are appreciating at a double-digit clip on a year-over-year basis. The rapid appreciation has helped fuel fears of a housing bubble, but it pales beside the 46-month stretch of double-digit percentage gains from August 2002 through May 2006 (Chart 8). Our Bank Credit Analyst and Global Fixed Income Strategy colleagues have made the case that the current burst of home price appreciation across the developed world has largely derived from generous fiscal transfers and extremely accommodative monetary policy.1 That implies that home prices will not be able to maintain their current pace once the policy support fades, but it does not necessarily foreshadow a looming crash. In our view, policy has contributed to a sugar rush that has briefly quickened price gains, a much less destabilizing condition than the multi-year course of steroid injections provided by the willful abandonment of prudent lending standards that triggered the GFC. Chart 8Nothing Like The Last Boom Yet

Nothing Like The Last Boom Yet

Nothing Like The Last Boom Yet

Despite the run-up in prices, homes remain much more affordable today than they were at the peak of the pre-GFC boom (Chart 9, top panel), thanks to mortgage rates that are about half their 2004-7 level (Chart 9, middle panel). Homebuilders have maintained their discipline this time around, holding new home construction at or below the rate of household formation (Chart 10, top panel) and there is none of the overtrading associated with bubbles, like the flipping at the top of the last cycle. As a share of the total housing stock, inventories of new and existing homes for sale are more than two standard deviations below their four-decade mean (Chart 10, middle panel) and the share of vacant homes, at 0.9%, is sitting at its 65-year series low (Chart 10, bottom panel). Unusually high prices will eventually inspire new sources of supply and push price gains down to levels consistent with their long-run mean; in the meantime, low mortgage rates will likely summon enough demand to prevent the disruption that Google searchers and cranky Austrians fear. Chart 9Affordability Is Still Quite High ...

Affordability Is Still Quite High ...

Affordability Is Still Quite High ...

Chart 10... Even Though Supply Is Tight

... Even Though Supply Is Tight

... Even Though Supply Is Tight

Haven’t We Left Something Out? Now wait a minute; you’re trying to have it both ways. You’ve been citing rising wealth for a while, suggesting that it will help foster a virtuous growth cycle that will last through next year, six or seven quarters after the final stimulus checks were cut. Home prices have been a part of that wealth surge but you’re ignoring what will happen once they stop defying gravity. We have been tracking aggregate household income, spending and savings for over a year and the growing pile of savings has been a key pillar of our argument that the economy will grow way above trend. Our running estimate of excess pandemic savings is now up to $2.4 trillion through May. That’s quite a lot even in a $21 trillion economy, and if it were all spent over a two-year period, GDP would grow by 10% more than it otherwise would. There is no close precedent for the income windfall that up to three-fourths of households have received since the pandemic began, so we cannot turn to regression models for an estimate of the savings’ near-term impact. However, it's important to recognize the money was directed at households below the top rungs of the income scale with a higher marginal propensity to consume, especially the federal unemployment insurance benefit supplements, which wound up going largely to the lowest-paid workers who bore the brunt of pandemic layoffs. Our working assumption is that around half of the savings will be spent across 2021 and 2022, which would push output over the period higher by more than 5%. We don’t care about GDP growth per se, but it does impact the outlook for corporate earnings, household income and credit performance. We have viewed the savings developments as making an important contribution to the positive macro backdrop for investments in equities and credit and expect they will continue to do so well into next year. Although we expect the returns on risk assets to slow, we anticipate that they will continue to exceed returns from Treasuries and cash and therefore maintain our overweight recommendations on equities and spread product. The household net worth gains from financial asset and home price appreciation haven’t factored much into our view. Though their advances have far outpaced the increase in savings, mainstream economic models consider their effects on consumption to be modest. Most of the gains are captured by wealthier households, who are more apt to save wealth increases than spend them, and our rule of thumb is that five cents and three cents of every dollar of stock and home price gains are spent, respectively. By that measure, the $7.4 and $3.2 trillion advances in the value of directly held stocks and home equity are less impactful than the savings gains and do not figure meaningfully into our view. We disagree with the widespread assumption that the increase in home prices is particularly notable. Per the Fed’s quarterly report on US financial accounts, the first quarter’s year-over-year increase in the value of real estate owned by households was 10.3%, a little more than half a standard deviation above the 275-quarter mean (Chart 11). It’s a nice gain, especially against a backdrop of low inflation, but it’s hardly a game changer. We agree that what goes up must come down, but in this case, reverting to the mean would only involve a three-percentage-point decline. Chart 11Housing Wealth Is Rising, But Not At An Outsized Rate

Housing Wealth Is Rising, But Not At An Outsized Rate

Housing Wealth Is Rising, But Not At An Outsized Rate

It should also be noted that outright national declines in nominal home values are rare – the only incidence in the postwar era occurred amidst the subprime crisis/GFC. It appears that the trauma of that event has global investors and Google-searching US citizens overestimating the probability that it might occur again. We have exhumed the term “subprime crisis” because that housing bust was caused by a near-total abandonment of established lending standards by virtually everyone involved in mortgage origination and securitization, including the agencies that rated the securities, the middlemen who warehoused them, the end-investors who bought them and the insurer who blithely wrote credit protection on them. Nothing even remotely similar from a credit perspective is going on today. Chart 12 shows the aggregate loan-to-value (LTV) on residential mortgages since 1971, when the first baby boomers began to turn 25, derived from the Fed’s financial accounts data. Aggregate household LTV is back to the 33% level it hugged throughout the seventies and eighties. It exploded higher from 2006 to 2009 as new mortgage debt galloped ahead of stagnating home values during the lending crescendo of 2006 and 2007 and then continued on in 2008 and 2009 as mortgage balances fell more slowly than home values (Chart 13). Chart 12High LTVs Amplify Shocks, Low LTVs Absorb Them

High LTVs Amplify Shocks, Low LTVs Absorb Them

High LTVs Amplify Shocks, Low LTVs Absorb Them

Chart 13Six Years That Crippled The Housing Market

The US Housing Market: Déjà Vu All Over Again?

The US Housing Market: Déjà Vu All Over Again?

Appalling underwriting provided the kindling for the crisis and the unprecedented plunge in US home prices that was a feature of it. A similar plunge will not recur this cycle when there are almost no borrowers with little to no skin in the game who would walk away from their nonrecourse loans at the first sign of trouble. Psychology also matters; given our deep-seated aversion to recognizing losses, homeowners who do not have to sell often hold on until prices climb back above their basis. Home values will surely encounter some headwinds once mortgage rates rise from rock-bottom levels, but an outright decline remains unlikely when increases in longer-dated Treasury yields will almost certainly be accompanied by an increase in inflation and/or real growth expectations, both of which would be associated with higher home prices. We hold our conclusion with high conviction: the US housing market does not look vulnerable and it is not likely to be a source of distress for the financial system here or abroad. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see the May 28, 2021 Global Fixed Income Strategy/Bank Credit Analyst Special Report, “Global House Prices: A New Threat For Policymakers.”

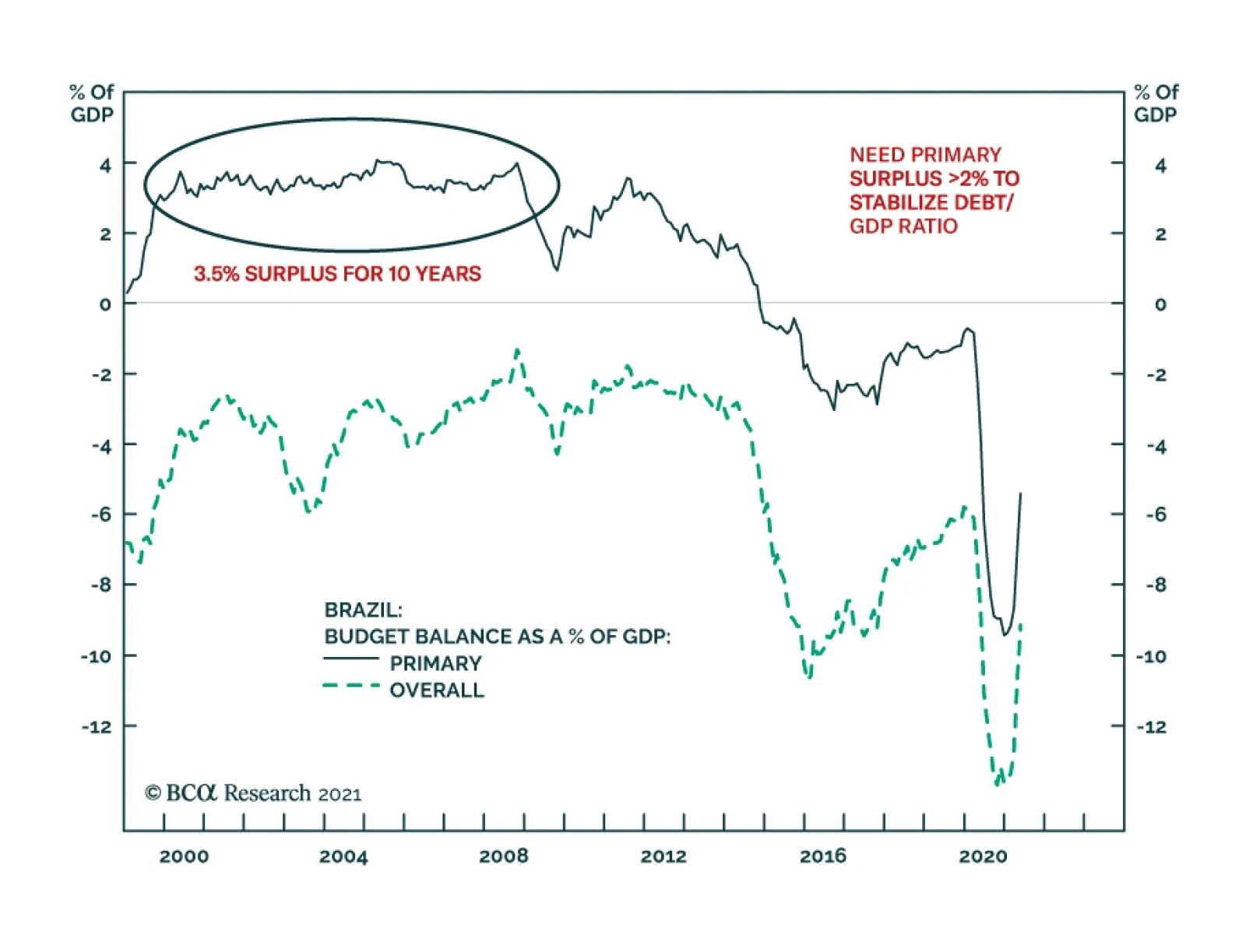

One of the structural challenges Brazil faces is its public debt overhang. The authorities have responded by periodically embarking on fiscal and monetary austerity. Yet, such austerity depresses nominal growth and has in fact worsened public debt dynamics. …

Highlights Our sense remains that the dollar is undergoing a countertrend bounce, rather than entering a new bull market. The litmus test for this view is if the DXY fails to break above the 93-94 level that marked the March highs. Stay short USD/JPY. The drop in global bond yields should give this trade a welcome fillip. Short GBP/JPY positions also make sense. We are long CHF/NZD as a play on a potential increase in currency volatility. Look to rebuy a basket of Scandinavian currencies versus the USD and EUR at a trigger point of -2% from today’s levels. Remain long silver both in absolute terms and relative to gold. Our limit buy on EUR/USD was triggered at 1.18. Place tight stops given the potential for the dollar rally to continue for the next few weeks. We also believe the change in the ECB’s framework portends another bullish tailwind for the euro beyond the near term. Feature In our webcast last week, we made the case that the recent FOMC meeting (perceived as hawkish by market participants) has not altered the longer-term downtrend in the US dollar. This week, we are revisiting some of the sentiment and technical indicators that could help gauge how high the dollar can rise in the interim. Our view remains that three fundamental forces will continue to dictate currency market trends into the year end and beyond. First, the Federal Reserve will lag other central banks in raising rates amidst a shift in economic momentum from the US towards the rest of the world. This will boost short-term interest rates outside the US and provide a floor for procyclical currencies. Second, US inflation will prove stickier compared to other countries such as the eurozone or Japan. This will depress real interest rates in the US relative to the rest of the world, and curb bond inflows. And finally, an equity market rotation towards non-US stocks will improve flows into cyclical currencies. The transition could prove volatile in the coming month or so. Equity markets remain overbought, bond yields are falling, PMIs have stopped rising, and cyclical stocks are lagging growth stocks. More widespread infection from the Delta variant of Covid-19 will continue to reprice risk to the downside. As a countercyclical currency, the dollar will be a critical variable to watch. Sentiment and technical indicators make up an important component of our currency framework and are usually good at gauging significant shifts in financial markets. Our sense remains that the dollar is undergoing a countertrend bounce, rather than entering a new bull market. The litmus test for this view is if the DXY fails to break above the 93-94 level that marked the March highs. Momentum Indicators Our momentum indicators suggest that while the dollar is very oversold, the bear market remains very much intact. The dollar advance/decline line is sitting below its 200-day moving average (Chart I-1). Historically, bull markets in the dollar have been characterized by our advance/decline line breaking both above its 200-day and 400-day moving averages. This suggests a rally towards these critical resistance levels is in play but will constitute more of a countertrend bounce. Speculators are only neutral the dollar while, admittedly, leveraged funds are very short (Chart I-2). Historically, whenever the percentage of leveraged funds that are short the dollar has dipped near 40%, a meaningful rally has ensued. There are two important offsets to this. First, as Chart I-1 suggests, the dollar is a momentum currency. As such, during the bull market of the last decade, speculators were either neutral or long the dollar. If indeed the paradigm has shifted to a decade-long bear market, we expect speculators to be either short or neutral. Meanwhile, leveraged funds are a small subset of overall open interest, suggesting they are not the elephant in the room when it comes to dictating dollar movements. Leveraged funds were short the dollar during most of the bull market run last decade. Chart I-1The US Dollar Downtrend Is Intact

The US Dollar Downtrend Is Intact

The US Dollar Downtrend Is Intact

Chart I-2Leveraged Funds Are Short The Dollar

Leveraged Funds Are Short The Dollar

Leveraged Funds Are Short The Dollar

Carry trades are relapsing anew, suggesting the environment may be becoming unfavorable for high-yielding developed and emerging market currencies. The dollar has been negatively correlated with the Deutsche Bank carry ETF, DBV, since investors ultimately dump carry trades and fly to the safety of Treasurys on any market turbulence (Chart I-3). High-beta carry currencies such as the RUB, ZAR, MXN, and BRL have been consolidating recent gains. These currencies are usually good at sniffing out a change in the investment landscape, specifically one becoming precarious for carry trades. Our carry index tends to do well when the yield spread between US Treasuries and the indexes’ constituents’ is low. As such, there is some more adjustment underway, but one of limited amplitude (Chart I-4). Chart I-3The Carry Trade Rally Is Relapsing

The Carry Trade Rally Is Relapsing

The Carry Trade Rally Is Relapsing

Chart I-4Carry Trades Have Hit An Air Pocket

Carry Trades Have Hit An Air Pocket

Carry Trades Have Hit An Air Pocket

Chart I-5Currency Volatility Is Very Low

Currency Volatility Is Very Low

Currency Volatility Is Very Low

Both expected and actual currency volatility are extremely depressed. Whenever currency volatility has been this low, the dollar has staged a meaningful rally. For example, the most significant episodes were the lows of 1996-1997, 2007-2008, and 2014-2015, and early 2020 (Chart I-5). Usually, low currency volatility is a sign of complacency, while higher volatility allows for a more balanced and healthy market rotation. The nature in which currency volatility adjusts higher this time around might be the same playbook as in previous episodes. The Asian crisis of the late 90s set the stage for the dollar bear market of the 2000s. The adjustment higher in the dollar during the Global Financial crisis jumpstarted the bull market the following decade. This time around, the Covid-19 crisis might have commenced a renewed dollar bear market. If this analogy is correct, then we should be selling the dollar on strength rather than buying on weakness. It is important to remember that the policy environment remains bearish for the dollar. These include deeply negative real rates, quantitative easing (which, admittedly, will soon end), generous liquidity swap lines to assuage any dollar funding pressures abroad (Chart I-6), and a global economy on the cusp of a renewed cycle. In our portfolio, we are long CHF/NZD since this cross has historically been a good hedge against rising currency volatility (Chart I-7). So is being short AUD/JPY. Being short the GBP/JPY cross might prove even more profitable, given that the UK has been a pandemic winner this year. Chart I-6The Fed Extended Its Swap Lines

The Fed Extended Its Swap Lines

The Fed Extended Its Swap Lines

Chart I-7Buy CHF/NZD As Insurance

Buy CHF/NZD As Insurance

Buy CHF/NZD As Insurance

Bottom Line: The message from our momentum indicators is that the bounce in the dollar was to be expected. We remain in the camp that believes the rally will be short-lived but are opportunistically playing what could be a more volatile environment. Equity Markets Signals A potential catalyst that could trigger further upside in the dollar is an equity market correction. Both the dollar and equities tend to be inversely correlated (Chart I-8). On this front, a few equity market indicators continue to flag that the rally in the dollar has a bit further to go. Chart I-8The Dollar And Equities Move Opposite Ways

The Dollar And Equities Move Opposite Ways

The Dollar And Equities Move Opposite Ways

Chart I-9Global Industrials Are Relapsing Anew

Global Industrials Are Relapsing Anew

Global Industrials Are Relapsing Anew

The underperformance of cyclical stocks, especially global industrials, suggests equity markets could be entering a more volatile phase (Chart I-9). The dollar tends to strengthen when cyclical stocks are underperforming defensive ones. This is because non-US equity markets have a much higher concentration of cyclical stocks in their bourses. In more general terms, non-US markets are underperforming the US, a clear sign that the marginal dollar is rotating back towards the US (Chart I-10A and I-10B). Technology stocks have also been well bid in recent weeks, on the back of lower bond yields. These are all temporary headwinds for dollar weakness. Chart I-10ANon-US Stock Markets Are Underperforming

Non-US Stock Markets Are Underperforming

Non-US Stock Markets Are Underperforming

Chart I-10BNon-US Stock Markets Are Underperforming

Non-US Stock Markets Are Underperforming

Non-US Stock Markets Are Underperforming

Chart I-11US Relative Earnings Revisions Are High, But Rolling Over

US Relative Earnings Revisions Are High, But Rolling Over

US Relative Earnings Revisions Are High, But Rolling Over

Earnings revisions continue to head higher across most markets, but US profit expectations are still higher compared to other countries (Chart I-11). Non-US bourses will need much higher earnings revisions to stimulate portfolio inflows, and for the dollar bear market to resume. On this front, both the euro area and emerging markets are showing only tentative improvement. The character of any selloff in equity markets will be worth monitoring. Cyclicals and value stocks are at historically bombed-out levels and could start to outperform high-flying stocks on any market reset. Bottom Line: Whether a correction ensues, or the bull market continues, requires a change in equity market leadership from defensives to cyclicals. This is a necessary condition for the dollar bear market to resume. Commodities, Bonds, And The Dollar Commodity and bond prices give important cues about the health of the global economy. For example, rising copper prices and rising yields are a sign that industrial activity is humming, which in turn points to accelerating global growth. As a counter-cyclical currency, the dollar usually weakens in this scenario. Rising gold prices are generally a sign that policy settings remain ultra-accommodative, which also points to a weaker dollar. At the FX strategy service, we tend to focus more on the internal dynamics of commodity and bond markets, which can provide early warning signs. Chart I-12The Copper-To-Gold Ratio Is Consolidating Gains

The Copper-To-Gold Ratio Is Consolidating Gains

The Copper-To-Gold Ratio Is Consolidating Gains

The copper-to-gold ratio is important since it indicates whether the liquidity-to-growth transmission mechanism is working. A rising ratio suggests policy settings are stimulating growth, while a falling ratio is a warning shot that the environment might be becoming deflationary. Correspondingly, this ratio has tended to track the dollar closely (Chart I-12). The copper-to-gold ratio is consolidating at very high levels. This is consistent with a healthy reset, rather than a reversal in the dollar bear market. The gold/silver ratio (GSR) tends to track the US dollar, and its recent price action also appears to be a welcome reset (Chart I-13). Like copper, silver benefits from rising industrial demand, especially in the electronics and renewable energy space. A falling GSR will be a sign that the manufacturing cycle is still humming. We are short the GSR with a target of 50, and a stop-loss at 71. The bond-to-gold ratio has bounced from very oversold levels. Both US Treasurys and gold are safe-haven assets and thus are competing assets. Remarkably, the ratio of the total return in US government bonds-to-gold prices has tracked the dollar pretty well since the end of the Bretton Woods system in the early ‘70s (Chart I-14). Gold has always been considered the perfect anti-fiat asset vis-à-vis the dollar, making the bond-to-gold ratio both a good short-term and long-term sentiment indicator. For now, the bounce in the ratio is not yet worrisome. We have noticed that inflows into US government bonds have risen sharply, while those into gold are falling. This should soon reverse with the fall in US rates, and the correction in gold prices. Chart I-13The Gold-To-Silver Ratio Is Consolidating Losses

The Gold-To-Silver Ratio Is Consolidating Losses

The Gold-To-Silver Ratio Is Consolidating Losses

Chart I-14Competing Assets And The Dollar

Competing Assets And The Dollar

Competing Assets And The Dollar

Bottom Line: The US is ultimately generating the most inflation in the G10, which is dampening real rates, and should curtail investor enthusiasm for gold relative to US Treasurys. The underperformance of Treasurys relative to gold will be a bearish development for the dollar. A Final Word On The Euro The strategic review from the European Central Bank had three key changes. The ECB now has a symmetric 2% inflation target. This is not a game changer, since it brings it in line with other global central banks, including the Bank of Japan. House prices will meaningfully begin to impact monetary policy, as the committee eventually includes owner’s equivalent rent (OER) in the HICP index (the ECB’s preferred inflation measure) for the euro area. This could be a game changer for the ECB’s price objective. Climate change was reiterated as important for price stability. Financial stability was also repeated as an important objective. As FX strategists, the second change was the most important. Shelter constitutes 17.7% of the euro area CPI basket, but it is 32.9% of the US CPI basket (Table I-1). Meanwhile, the shelter component of both the CPI basket in the US and euro area have tracked each other (Chart I-15). Table I-1Euro Area CPI Weights

An Update On Dollar Sentiment And Technical Indicators

An Update On Dollar Sentiment And Technical Indicators

Chart I-15What Will Happen To Eurozone Inflation?

What Will Happen To Eurozone Inflation?

What Will Happen To Eurozone Inflation?

An adjustment in the weight of the shelter component in the euro area will boost the European CPI relative to the US and could trigger a major policy shift from the ECB in the coming years. This will especially be the in case if the current environment generates an inflationary shock. Bottom Line: The ECB will stay very accommodative in the next 1-2 years, but the change in its mandate could portend a bullish tailwind for the euro beyond the near term. Investment Implications We expect the current dollar rebound to be short-lived. As such, our strategy is as follows: Stay long other safe-haven currencies. Our preferred vehicle is the Japanese yen, which sports an attractive real rate relative to the US. Investors can also short GBP/JPY from current levels. Chart I-16The Euro, Yen And Real Rates

The Euro, Yen And Real Rates

The Euro, Yen And Real Rates

Our limit-buy on EUR/USD was triggered at 1.18. Given our expectation that the dollar could rally in the near term, we are setting the stop-loss at the same level. However, the improvement in real rates in the euro area relative to the US could cushion any downside (Chart I-16). We are also long CHF/NZD, as a bet on rising currency volatility. Correspondingly, we are setting a limit buy on Scandinavian currencies relative to the euro and USD at a trigger level of -2%. Both gold and silver benefit from the current environment, but we prefer silver to gold, due to the former’s call option on continued improvement in global growth. We are short the gold/silver ratio from the 68 level. Overall, we expect the dollar to weaken towards the end of the year, as has been the case since the 1970s (Chart I-17). Chart I-17The Yen And Swiss Franc Are Usually Winners In H2

An Update On Dollar Sentiment And Technical Indicators

An Update On Dollar Sentiment And Technical Indicators

Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Currencies US Dollar USD Technicals 1

USD Technicals 1

USD Technicals 1

USD Technicals 2

USD Technicals 2

USD Technicals 2

The recent data out of the US have been robust: June non-farm payrolls showed an increase of 850K jobs, versus expectations of a 700K increase. The unemployment rate was relatively flat at 5.9% in June. Factory orders came in at 1.7% year-on-year in May, in line with expectations. The US dollar DXY index is relatively flat this week, but with tremendous volatility. It was a relatively quiet week in the US, due to Independence Day, but the key theme remained a drop in US yields, with the 10-year yield moving from a high of near 1.8% this year to 1.3% currently. This move has catalyzed rallies in lower beta currencies, such as the yen and Swiss franc. The FOMC minutes released this week continue to suggest a Fed that will remain very patient in both tapering asset purchases and lifting interest rates. Report Links: Arbitrating Between Dollar Bulls And Bears - March 19, 2021 The Dollar Bull Case Will Soon Fade - March 5, 2021 Are Rising Bond Yields Bullish For The Dollar? - February 19, 2021 The Euro EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data from the euro area were mixed: The PPI print for May came in at 9.6%, in line with expectations. Both the services and composite PMI were revised higher by 0.3 in June. At 59.2, the composite PMI is the highest in over a decade. ZEW expectations for the euro area fell sharply from 81.3 to 61.2. In Germany, there was a big decline in automotive surveys. The euro was flat this week against the dollar, despite gains overnight. The big news was the change in the ECB’s monetary policy objectives, which we discussed briefly in the front section of this report. The euro rallied on the news of three fundamental drivers in our view – real rate differentials are improving in favor of Europe, the ECB’s consideration for house price inflation could allow its price stability objective to be achieved sooner, and consideration for financial stability will be less favorable for negative interest rates. Report Links: Relative Growth, The Euro, And The Loonie - April 16, 2021 The Euro Dance: One Step Back, Two Steps Forward - April 2, 2021 On Japanese Inflation And The Yen - January 29, 2021 The Yen JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data from Japan remains subpar, but is improving: Labor cash earnings rose 1.9% in May, in line with expectations. Household spending rose 11.6% in May, in line with expectations. The Eco Watchers Survey for June came in at 47.6 from a May reading of 38.1. The outlook component rose from 47.6 to 52.4. The yen was up by 1.6% against the USD this week, the best performer. We argued a month ago that the yen is the most underappreciated G10 currency today. The catalyst that triggered yen gains were a drop in US real rates, that favored other safe-haven currencies. Going forward, further yen gains should materialize on the back of Japan successfully overcoming the pandemic like its Western counterparts. Report Links: The Case For Japan - June 11, 2021 The Dollar Bull Case Will Soon Fade - March 5, 2021 On Japanese Inflation And The Yen - January 29, 2021 British Pound GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

There was scant data out of the UK this week: The construction PMI rose from 64.2 to 66.3 in June. House prices remain robust, with the RICS house price balance printing an elevated 83% in June. The pound was flat this week against the USD. The new delta variant of the COVID-19 virus is gaining momentum in the UK and will likely erode some of the dividends GBP had priced in from a fast vaccine rollout. As such, short GBP positions may pay off in the near term. Shorting GBP/CHF could be an attractive near-term hedge. Report Links: Why Are UK Interest Rates Still So Low? - March 10, 2021 Portfolio And Model Review - February 5, 2021 Thoughts On The British Pound - December 18, 2020 Australian Dollar AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

There was scant data out of Australia this week: The Melbourne Institute of Inflation survey came it at 3% year on year in June, from 3.3%. The RBA kept interest rates unchanged at 0.1%, reiterating its commitment to stay accommodative until inflation and wages pick up meaningfully. The AUD was down by 0.4% this week against the USD. The RBA is decisively lagging other central banks in communicating less monetary accommodation in the coming years. This will create a coiled spring response for the AUD, because the RBA will have to eventually play catchup as the global economic cycle gains momentum. Report Links: The Dollar Bull Case Will Soon Fade - March 5, 2021 Portfolio And Model Review - February 5, 2021 Australia: Regime Change For Bond Yields & The Currency? - January 20, 2021 New Zealand Dollar NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

The was scant data out of New Zealand this week: ANZ commodity price index rose by 0.8% in June. The NZD was down 0.3% against the dollar this week. Our long CHF/NZD position paid off handsomely in this environment. We recommend holding onto this trade, as a reset in global rates hurts the hawkish pricing in the NZD forward curve. Report Links: How High Can The Kiwi Rise? - April 30, 2021 Portfolio And Model Review - February 5, 2021 Currencies And The Value-Versus-Growth Debate - July 10, 2020 Canadian Dollar CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Canadian data softened but remained robust: Building permits fell by 14.8% month on month in May. The Markit manufacturing PMI fell from 57 to 56.5 in June. The Canadian trade balance deteriorated from C$0.6bn to a deficit of -C$1.4bn in May. Business Outlook Survey indicator hit the highest level on record. As the Bank of Canada put it, improving business sentiment is broadening. The CAD fell by 0.8% against USD this week. The results of the BoC survey highlight that a reopening phase is categorically bullish for economic activity in general and financial prices. Until recently, the CAD was one of the best performing currencies in the G10. This is a sea change from a country that was previously a laggard in vaccination efforts. CAD should hold up well once the dollar rally fades, but other currency laggards such as SEK and JPY could do even better. Report Links: Relative Growth, The Euro, And The Loonie - April 16, 2021 Will The Canadian Recovery Lead Or Lag The Global Cycle? - February 12, 2021 The Outlook For The Canadian Dollar - October 9, 2020 Swiss Franc CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

The was scant data out of Switzerland this week: The unemployment rate was near unchanged at 3.1% in June, from 3.0%. Total sight deposits were unchanged at CHF 712 bn on the week of July 2. The Swiss franc was up by 1.1% this week against the USD. Falling yields improved the relative appeal of the franc that has bombed out interest rates. The franc is also benefiting from the rising bout of volatility as a safe-haven currency. On this basis, we are long CHF/NZD cross, which performed well this week. Report Links: An Update On The Swiss Franc - April 9, 2021 Portfolio And Model Review - February 5, 2021 The Dollar Conundrum And Protection - November 6, 2020 Norwegian Krone NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Data out of Norway is improving: The unemployment rate fell from 3.3% to 2.9% in July. Industrial production growth came in at 2.1% year-on-year in May. Mainland GDP rose by 1.8% month on month in May. The NOK was down by 1.8% this week against the dollar, the worst performing G10 currency. The NOK is bearing the brunt of a reset in the US dollar, but our bias is that we are nearing a buy zone. NOK is cheap, would benefit from high oil prices and the economy is on the mend. We are looking to sell EUR/NOK and USD/NOK on further strength. Report Links: The Norwegian Method - June 4, 2021 Portfolio And Model Review - February 5, 2021 Revisiting Our High-Conviction Trades - September 11, 2020 Swedish Krona SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data from Sweden have been mildly positive: The Swedbank/Silf composite PMI fell from 70.2 to 66.9 in June. Industrial production came in at 24.4% year on year in May, after a rise of 26.4% in April. Household consumption jumped 8.8% year on year in April. The SEK was also up this week against the USD. Bombed-out interest rates in Sweden have also improved the appeal of the franc, given falling global bond yields. Meanwhile, the SEK remains one of the cheapest currencies in our models. Report Links: Revisiting Our High-Conviction Trades - September 11, 2020 More On Competitive Devaluations, The CAD And The SEK - May 1, 2020 Sweden Beyond The Pandemic: Poised To Re-leverage - March 19, 2020 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

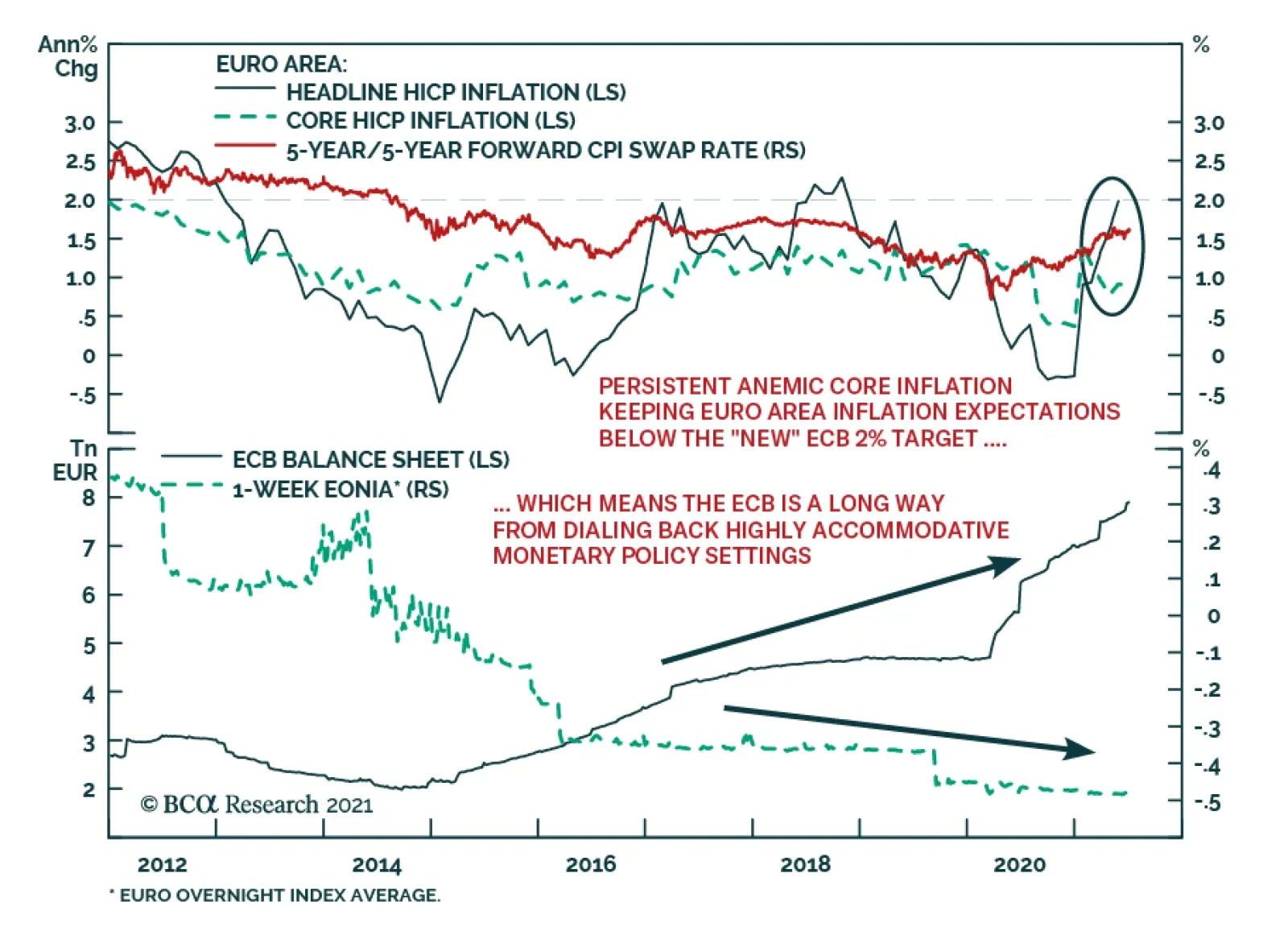

The ECB unveiled the results of its strategic review yesterday, with some noteworthy tweaks to the policy framework. The central bank shifted to a symmetric inflation target of 2%, a change from the prior goal of aiming for inflation “just below” 2%.…

In their Q2/2021 model bond portfolio performance review, BCA Research’s Global Fixed Income Strategy team updated their recommended positioning for the next six months. Firstly, the team changed its US Treasury curve exposure to have more of a flattening…

Highlights Economy – The endpoint of easier-for-longer monetary policy may be coming into view: Elevated inflation readings and discomfort among more hawkish FOMC members may signal that a monetary policy inflection is on the way. Markets – Volatility should pick up as investors reprice financial assets to reflect the end of emergency accommodation: The rumblings in bond, currency and precious metals markets that followed the June FOMC meeting are likely to spread as investors pull their liftoff date expectations forward. Strategy – Maintain below-benchmark duration positioning and ensure that portfolios can withstand increased volatility: Don’t be lulled to sleep by the 10-year Treasury yield’s backing and filling or by the VIX’s foray into the low teens. It is a more auspicious time to be buying insurance than selling it. Feature After fourteen years, investors may be weary of focusing so much attention on the Fed, but there’s been no avoiding its impact since the global financial crisis (GFC) emerged. Zero interest rate policy (ZIRP), large-scale asset purchases and other emergency measures have exerted a strong pull on financial markets as they have been switched on and off. The extended turn of rushing to the rescue appears to be weighing on the Fed as well. Last August’s revisions to its Statement on Longer-Run Goals and Monetary Policy Strategy explicitly acknowledged the challenges of operating in a ZIRP world in which its ability to deploy its primary tool for countering economic weakness – cutting the fed funds rate – is constrained by the zero lower bound. The Fed responded by adjusting its approach to each element of its dual mandate. It adopted an average-inflation-targeting framework that seeks to remediate past inflation shortfalls and indicated that it would only intervene to mitigate shortfalls from its maximum employment estimate. The latter move marked a break with the previous four decades, when the Fed, unwilling to give inflation pressures a chance to take root, proactively tightened policy when it judged that the labor market might be getting too strong. Taken together, the changes amounted to a significant break from doing whatever it took to keep inflation from gaining a foothold to making sure it didn’t completely vanish from households’, businesses’ and investors’ consciousness. If the changes were implemented as outlined, the effects could be wide-ranging. Inflation would be able to gain more traction, all else equal, leading to higher bond yields as markets anticipated that a higher terminal fed funds rate would be required to bring it to heel. A higher terminal fed funds rate might lead to a deeper economic slowdown, ushering in lower bond yields than otherwise would have prevailed. By inducing higher highs and lower lows in Treasury yields, the revisions to the Fed’s framework could promote increased financial market volatility, depending on FOMC members’ ongoing commitment to them and the way that commitment interacted with investors’ expectations. Although the revised framework is eleven months old, it is freshly relevant as the interaction between its implementation and investors’ expectations may be approaching an inflection point. When the FOMC announced the framework revisions last August, it didn’t have any immediate monetary policy implications and investors and committee members could reasonably have figured they would cross the new-framework bridge when they came to it. Elevated inflation readings and some differences in views within the FOMC suggest the bridge might now have to be crossed soon enough to fit within most institutional investors’ time horizons. Volatility may well rise as markets attempt to reprice assets against the backdrop of a novel monetary policy approach. End Of An Era The aforementioned changes that the FOMC made to its monetary policy strategy represented a watershed moment for US monetary policy. Beginning with Paul Volcker’s tenure as Fed chair near the end of the high-inflation ‘70s, the Fed has kept a sharp lookout for inflation pressures (Chart 1). Though it only introduced an annual inflation target in the aftermath of the GFC, its one-way view of inflation was well established. Signs that it might be emerging could be grounds for tighter monetary conditions while dormant readings were nothing to worry about. Chart 1Upholding Volcker's Mantle

Upholding Volcker's Mantle

Upholding Volcker's Mantle

The average inflation target indicates that inflation shortfalls will henceforth be as much of a concern as inflation overshoots and the Fed will attempt to remediate them with an eye towards keeping inflation expectations from slipping below 2%. On the other hand, the new framework shifts from a two-way to a one-way perspective on employment. Where the committee had previously attempted to conduct policy in a way that mitigated any deviations from its maximum-employment assessment, the new framework seeks only to mitigate shortfalls. Citing the post-crisis experience, when inflation remained in check despite a half-century low in the unemployment rate, and a desire to see expansion gains spread more widely across households, Chair Powell has repeatedly emphasized that too much employment is not a concern. Easier Said Than Done When the Fed announced the changes to its approach, we noted that they would be significant for investors provided it were to follow through on them. It is one thing to promise wide-reaching changes in the indefinite future but quite another to execute them in real time under duress. Financial markets seemed to be aware that turning on a dime would be easier said than done and did not bother to adjust their fed funds rate expectations (Chart 2) or reprice assets that might be most affected by the new policy framework. Among investors with a time frame of a year or less, the talk was all theoretical, anyway – of course policy was going to remain extremely easy when the US and the rest of the world were still knee-deep in a once-in-a-century pandemic and the development of an effective vaccine was a ways off. Chart 2Until Recently, Markets Saw Little Chance Of Rate Hikes On A Two-Year Horizon

Until Recently, Markets Saw Little Chance Of Rate Hikes On A Two-Year Horizon

Until Recently, Markets Saw Little Chance Of Rate Hikes On A Two-Year Horizon

In other words, talk was cheap when the FOMC unveiled its new framework. Its plans would only matter once the pandemic’s grip eased and central banks regained some discretion. The committee’s resolve to adhere to the new framework would only be tested in the face of uncomfortably high inflation prints and/or inflation expectations that threatened to anchor at levels above its target range. Investors wouldn’t bother to reprice financial assets in line with the new framework until they were certain it would apply. Inoculating Against Deflation As it turned out, effective vaccines appeared on the horizon sooner than anticipated. Pfizer and BioNTech announced the enormously encouraging results from their vaccine’s Phase III trials before the New York open on November 9th, and the Moderna vaccine’s similar clinical successes followed shortly thereafter. Vaccine distribution would begin in January, and the long end of the Treasury curve would begin to reprice, nudged along by rising inflation expectations. Agita sparked by March CPI data caused expectations to peak ahead of the April release, and 10-year breakevens briefly edged above the levels consistent with the Fed’s goals (Chart 3, top panel). Chart 3Coloring Within The Lines

Coloring Within The Lines

Coloring Within The Lines

Chart 4Unsustainable Outliers

Unsustainable Outliers

Unsustainable Outliers

We share the view of most mainstream economists that the upside surprises in the March and April inflation prints resulted from transitory reopening factors and do not mark an inflection point. Increases in used car prices will slow once rental car companies rebuild their fleets to match burgeoning demand and new car production can resume at its intended pace, lumber prices will continue to ease as sawmills ramp up operations to capture outsized profits, and the pace of increases in airfares will settle down once staffing bottlenecks can be resolved and more flights can be added to meet resurgent demand (Chart 4). Easier For How Much Longer? Markets’ collective shrug upon the release of the revisions to the Fed’s monetary policy framework reflected the view that they did not amount to a meaningful change over most investors’ time horizons. The second wave of COVID-19 infections had peaked a month before, but at least one other was likely in store as students returned to college campuses, and a vaccine was not yet on the horizon. According to Good Judgment’s professional superforecasters, there was roughly an equal 40% probability that 25 million vaccine doses would be available for distribution in the US between October 1st, 2020 and March 31st, 2021 or between April 1st and September 30th, 2021 (Chart 5). The more optimistic estimate turned out to be right, albeit not quite optimistic enough: nearly 25 million doses were administered by the end of February and nearly 50 million by the March 31/April 1 midpoint of the two periods (Chart 6). Chart 5Vaccine Development And Distribution Wound Up Beating August's Expectations ...

Transitioning Away From Auto-Pilot

Transitioning Away From Auto-Pilot

Chart 6... By A Considerable Margin

... By A Considerable Margin

... By A Considerable Margin

The vaccine outlook was relevant because it was hard to envision any incremental tightening of monetary policy while the country was still in the throes of the pandemic. Treasury yields at the longer end of the curve weren’t likely to go anywhere in the absence of increases in the fed funds rate (Chart 7) or increases in inflation or real growth expectations. Just as a still-raging virus was likely to keep the FOMC from hiking rates, it would also put a lid on inflation pressures and economic growth. With economic activity sharply limited by social distancing mandates and individuals’ innate reluctance to risk exposure, it was certain that capacity would continue to surpass aggregate demand. Chart 7Treasury Yields Move With Fed Funds Expectations

Treasury Yields Move With Fed Funds Expectations

Treasury Yields Move With Fed Funds Expectations

To the extent investors thought about the FOMC’s new framework when it was unveiled, they seem to have taken it as confirmation that monetary policy would remain easier for longer, consistent with the theme that has prevailed since the Bernanke Fed led the charge to counter the GFC. Treasury yields were subdued even after the vaccine news broke in November (Chart 8, top panel), and with the interest rate structure remaining quiet, there was no major repricing in other rate-sensitive markets. Gold, which might have been expected to benefit from more accommodative policy, slipped nearly 15%, from the mid-$1,900s to the high $1,600s, between the release of the new framework and its March trough. After retracing half of its post-August decline, it shed a fresh 5% following the FOMC’s June meeting (Chart 8, second panel). Chart 8Growth Prospects, Not Fed Prospects

Growth Prospects, Not Fed Prospects

Growth Prospects, Not Fed Prospects

Commodity currencies had added 10% versus the US dollar before ceding half of those gains in the wake of the June FOMC meeting, but their rally appears to have been driven by the increased global growth expectations that followed the positive vaccine news as they went nowhere in September and October (Chart 8, third panel). Similarly, the DXY Index had taken its post-revision cue from global growth prospects, moving inversely with pandemic news (rising when bad, falling when good), before rallying after the June meeting (Chart 8, bottom panel). The rise in measured inflation has encouraged some committee members to bring forward their anticipated liftoff dates and accelerate their individual dot plots, as disclosed last month. Now that the Fed no longer seems to be of one mind on the easier-for-longer path, investors have begun to reassess the scene. Prices are moving as capital reportedly exits pro-inflation positions and the money markets now call for two-and-a-half rate hikes by mid-2023 (Chart 2). More volatility could be in store amidst a shift in the Fed consensus as markets pull forward or push back their expected liftoff date and the expected pace of hikes speeds up or slows down. Investment Implications With the moves in measured inflation and inflation expectations seeming to have met the FOMC’s first two criteria for hiking rates (Table 1), a return to full employment looms as the final hurdle to liftoff. We reiterate our view that hiring progress is the swing factor that investors should be watching to anticipate the coming shift in monetary policy settings. Net payrolls expanded by 850,000 in June, topping estimates and putting the three-month moving average, 567,000, ahead of the 375-485,000 pace required to return the economy to full employment by the second half of 2022.1 That may sound like an overly ambitious target on its face, but we contend that annualized monthly payroll expansion of 4% for fourteen months or 3.1% for eighteen months is attainable given the magnitude of the pandemic job losses (Chart 9). Table 1A Checklist For Liftoff

Transitioning Away From Auto-Pilot

Transitioning Away From Auto-Pilot

Chart 9A 2H22 Return To Full Employment Is Entirely Possible

A 2H22 Return To Full Employment Is Entirely Possible

A 2H22 Return To Full Employment Is Entirely Possible

Our outlook for sustained net payroll expansion remains near the optimistic end of the expectations continuum, though the money market consensus has lately caught up with our sometime-before-the-end-of-2022 liftoff date view (Chart 10). Given that we expect that the yield curve will steepen as the hiring strength shows itself, we advise maintaining below-benchmark duration in Treasury portfolios. The optimism embedded in our hiring view implies robust growth over the next twelve months and we therefore recommend overweighting spread product within fixed income portfolios via a high-yield overweight, and overweighting equities within multi-asset portfolios. Hot growth will eventually induce the Fed to start pumping the monetary brakes, slowing the economy and investment returns, but the twelve-month outlook remains favorable for risk assets. Chart 10Looking For At Least One Hike By The End Of 2022

Looking For At Least One Hike By The End Of 2022

Looking For At Least One Hike By The End Of 2022

Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Making the simplifying (and overly conservative) assumption that returning to full employment will require recovering February 2020’s level of nonfarm payrolls, the US is currently short 6.8 million jobs. Regaining those jobs by August 2022 (14 months from now) will require a monthly average of 485,000 net job gains; regaining them by December 2022 (18 months hence) will require a 375,000 monthly average.

Dear Client, We are sending you our Strategy Outlook today, where we outline our thoughts on the macro landscape and the direction of financial markets for the rest of 2021 and beyond. Next week, please join me for a webcast on Thursday, July 8 at 10:00 AM EDT (3:00 PM BST, 4:00 PM CEST, 10:00 PM HKT) where I will discuss the outlook. Best regards, Peter Berezin, Chief Global Strategist Highlights Macroeconomic Outlook: Global growth is peaking but will remain solidly above trend. While the proliferation of the Delta strain is likely to trigger another wave of Covid cases this summer, the economic impact will be far smaller than during past waves. Global Asset Allocation: The risk-reward profile for stocks has deteriorated since the start of the year. Nevertheless, with few signs that the global economy is heading towards another major downturn, investors should maintain a modest equity overweight on a 12-month horizon. Equities: Favor cyclicals, value-oriented, and non-US equities. Emerging markets should spring back to life in the autumn once vaccine supplies increase and Chinese fiscal policy turns more stimulative. Fixed Income: Maintain below average interest-rate duration exposure. The 10-year US Treasury yield will finish the year at 1.9%. Spread product will continue to outperform high quality government bonds. Currencies: The US dollar will resume its weakening trend as growth momentum rotates from the US to the rest of the world. EUR/USD will finish the year at 1.25. Commodities: Brent will rise to $79/bbl by end-2021, 9% above current market expectations. While the lagged effects from the slowdown in Chinese credit growth earlier this year will weigh on base metals during the summer months, the long-term outlook for metals is positive. Favor gold over cryptos as an inflation hedge. I. Macroeconomic Outlook Global Vaccination Campaign Kicks Into High Gear Nearly 18 months after the pandemic began, the global economy is on the mend. In its latest round of forecasts released on May 31st, the OECD projects that the global economy will expand by 5.8% this year, up from its March projection of 5.6%. The OECD also bumped up its growth forecast for 2022 from 4% to 4.4%. After a rough start, the vaccination campaign is progressing well in most advanced economies (Chart 1). The US and the UK were the first major developed economies to roll out the vaccines, followed by Canada and the EU. While Japan has lagged behind, the pace of vaccinations has picked up lately. Twenty percent of the Japanese population has now received at least one dose. Developing economies are still struggling to secure enough vaccines. Fortunately, this problem should abate over the next six months. The Global Health Innovation Center at Duke University estimates that pharmaceutical companies are on track to produce more than 10 billion vaccine doses this year (Chart 2). While perhaps not enough to inoculate everyone who wants a jab, it will suffice in providing protection to the most vulnerable members of society – the elderly and those with pre-existing medical conditions. Chart 1The Vaccination Campaign Is Progressing Well In Most Developed Economies

The Vaccination Campaign Is Progressing Well In Most Developed Economies

The Vaccination Campaign Is Progressing Well In Most Developed Economies

Chart 2Vaccine Makers Are On Track To Produce Over 10 Billion Doses In 2021

2021 Third Quarter Strategy Outlook: The Path To Normal

2021 Third Quarter Strategy Outlook: The Path To Normal

New Variants And Vaccine Hesitancy Are Risks Novel strains of the virus remain a concern. First identified in India, the so-called “Delta variant” is spreading around the world. The number of new cases in the UK, where the Delta variant accounts for over 90% of all new infections, is rising again (Chart 3). The latest outbreak has forced the government to postpone “Freedom Day” from June 21st to July 19th (Chart 4). Chart 3The Number Of New Cases In The UK Is Rising Anew

2021 Third Quarter Strategy Outlook: The Path To Normal

2021 Third Quarter Strategy Outlook: The Path To Normal

Chart 4Dismantling Of Lockdown Measures Occurring At Varying Pace

2021 Third Quarter Strategy Outlook: The Path To Normal

2021 Third Quarter Strategy Outlook: The Path To Normal

It is highly likely that the Delta variant will produce another wave of cases in the US this summer. Despite ample availability, one-third of Americans over the age of 18 have yet to receive a single dose of a vaccine. As is the case with most everything in the United States, the question of whether to be inoculated has become politicized. In many Republican-leaning states, more than half the population remains unvaccinated (Chart 5). Chart 5The US Politicization Of Vaccines Raises The Risk From COVID-19 Variants

2021 Third Quarter Strategy Outlook: The Path To Normal

2021 Third Quarter Strategy Outlook: The Path To Normal