Inflation

Our US bond team’s thoughts on this afternoon’s FOMC meeting and yesterday’s CPI release.

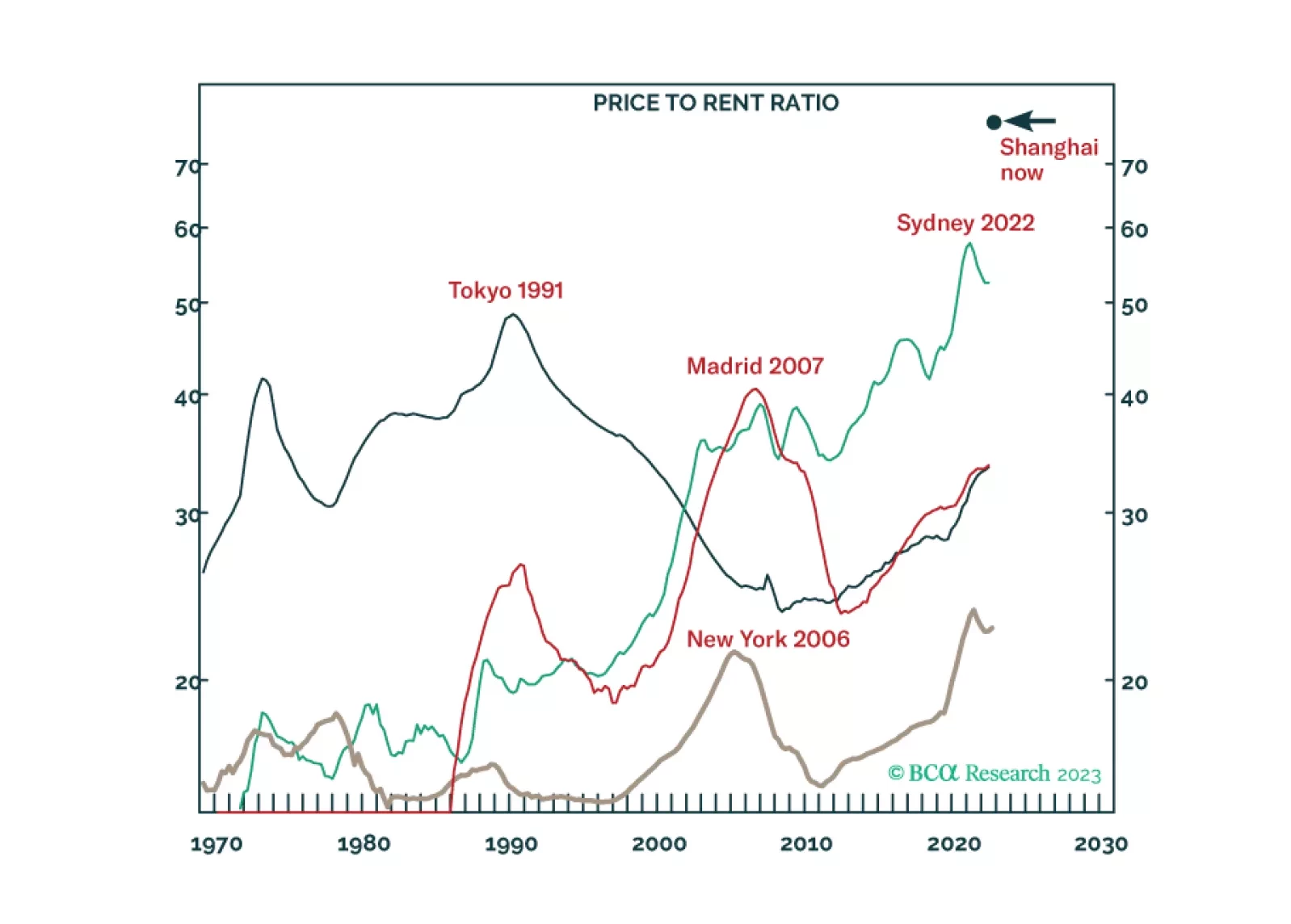

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.

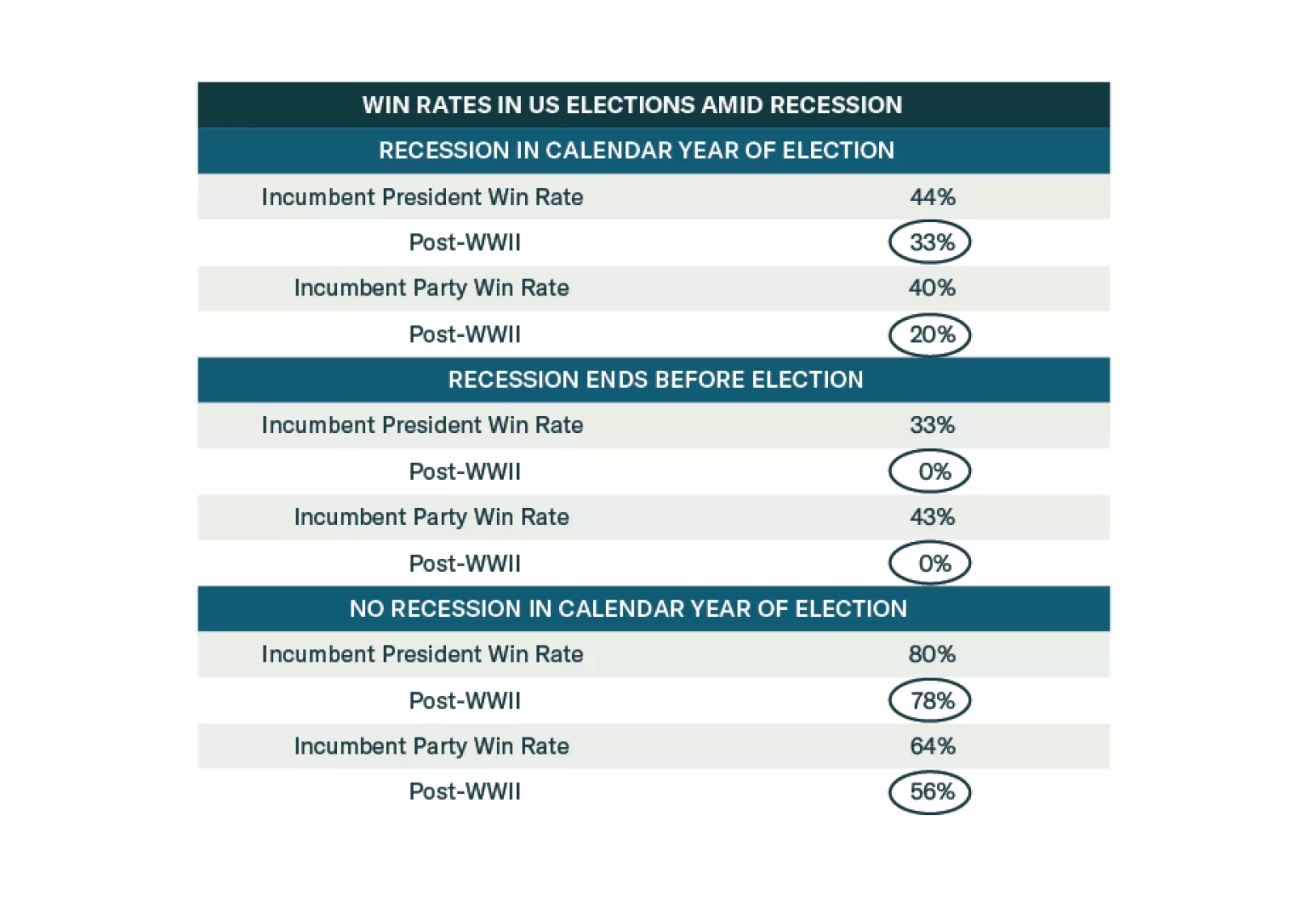

Democrats are favored to win the election until recession materializes. But recession risks are high. Investors should adopt a defensive and conservative strategy in 2024 amid extreme US policy uncertainty.

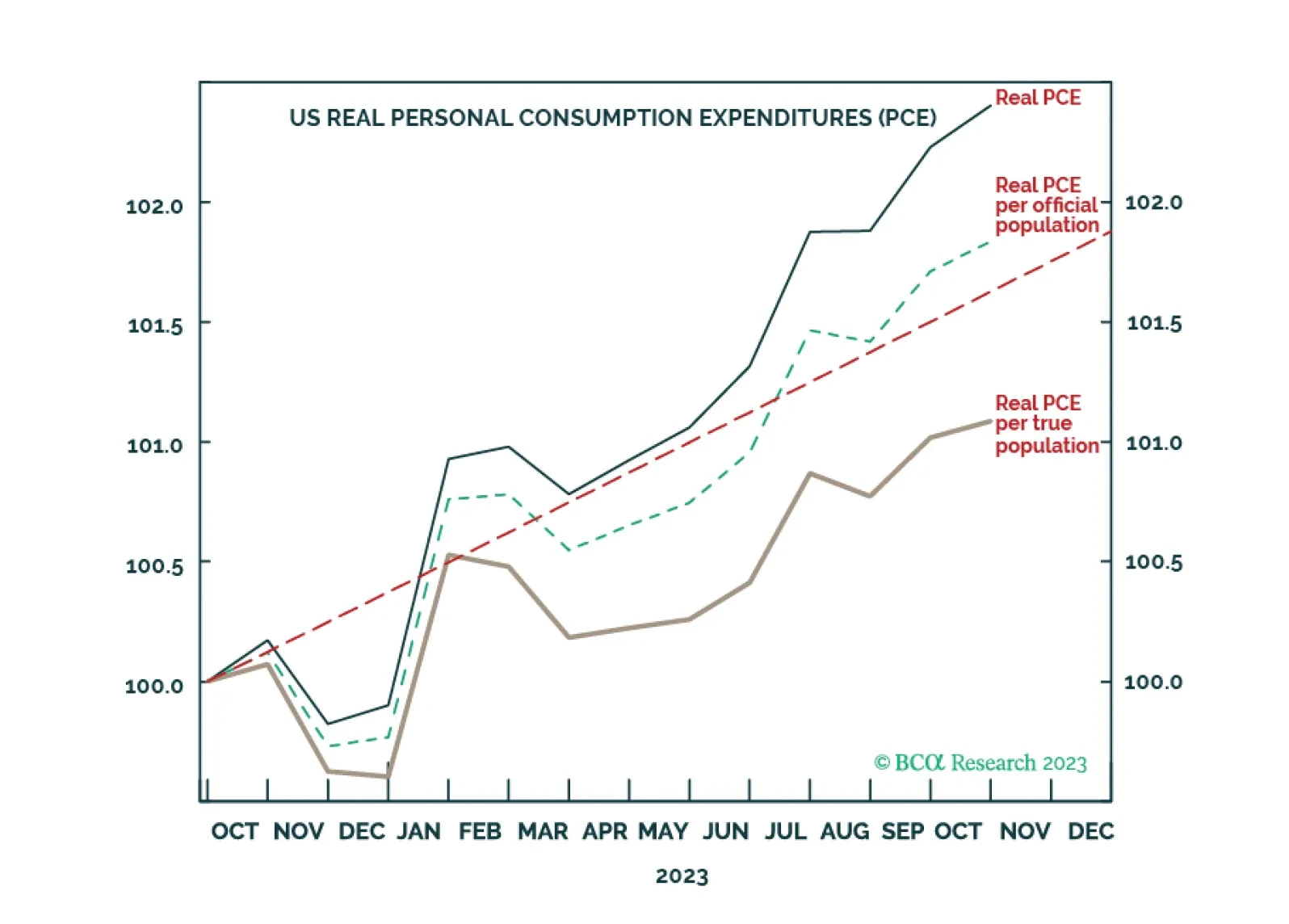

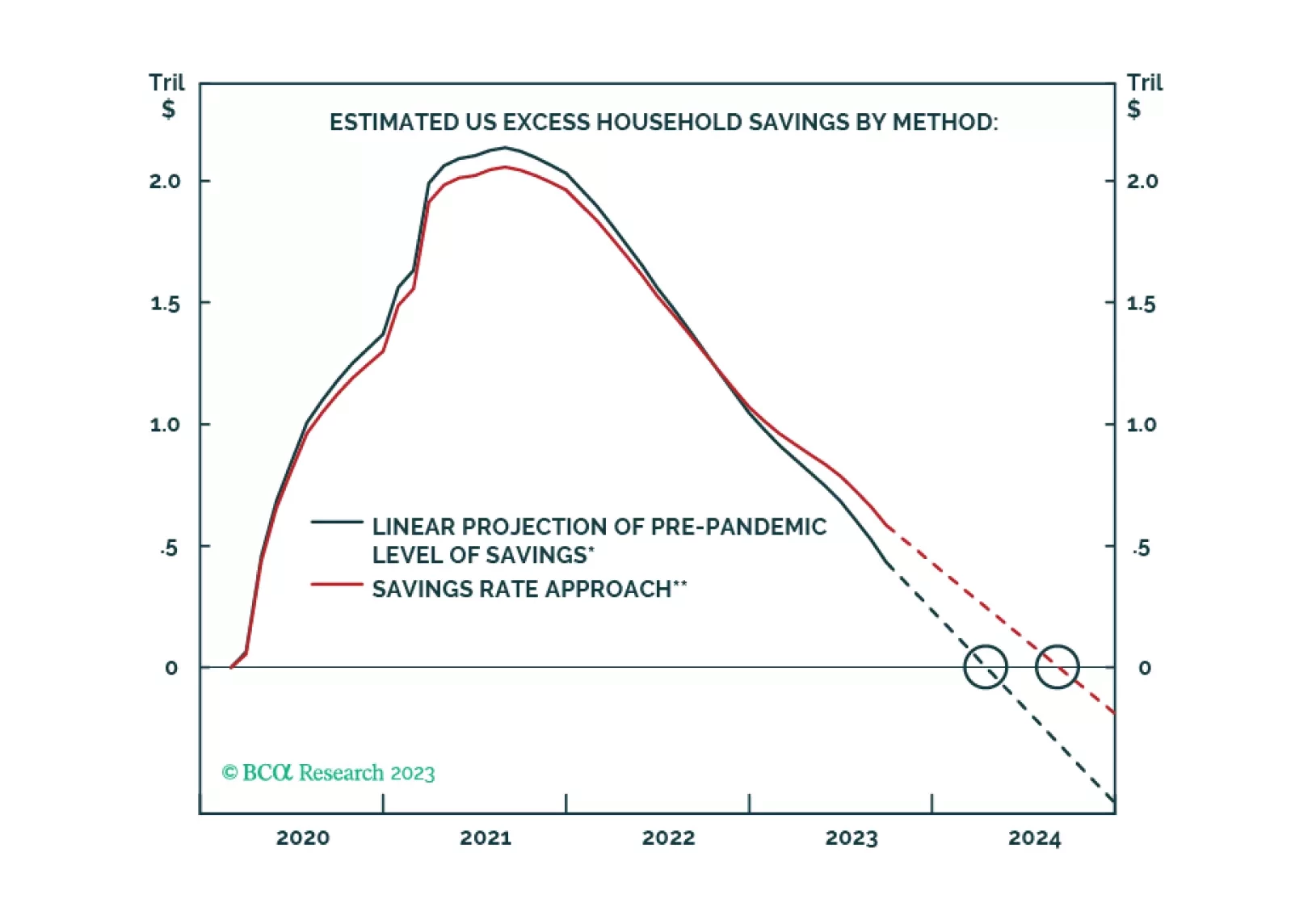

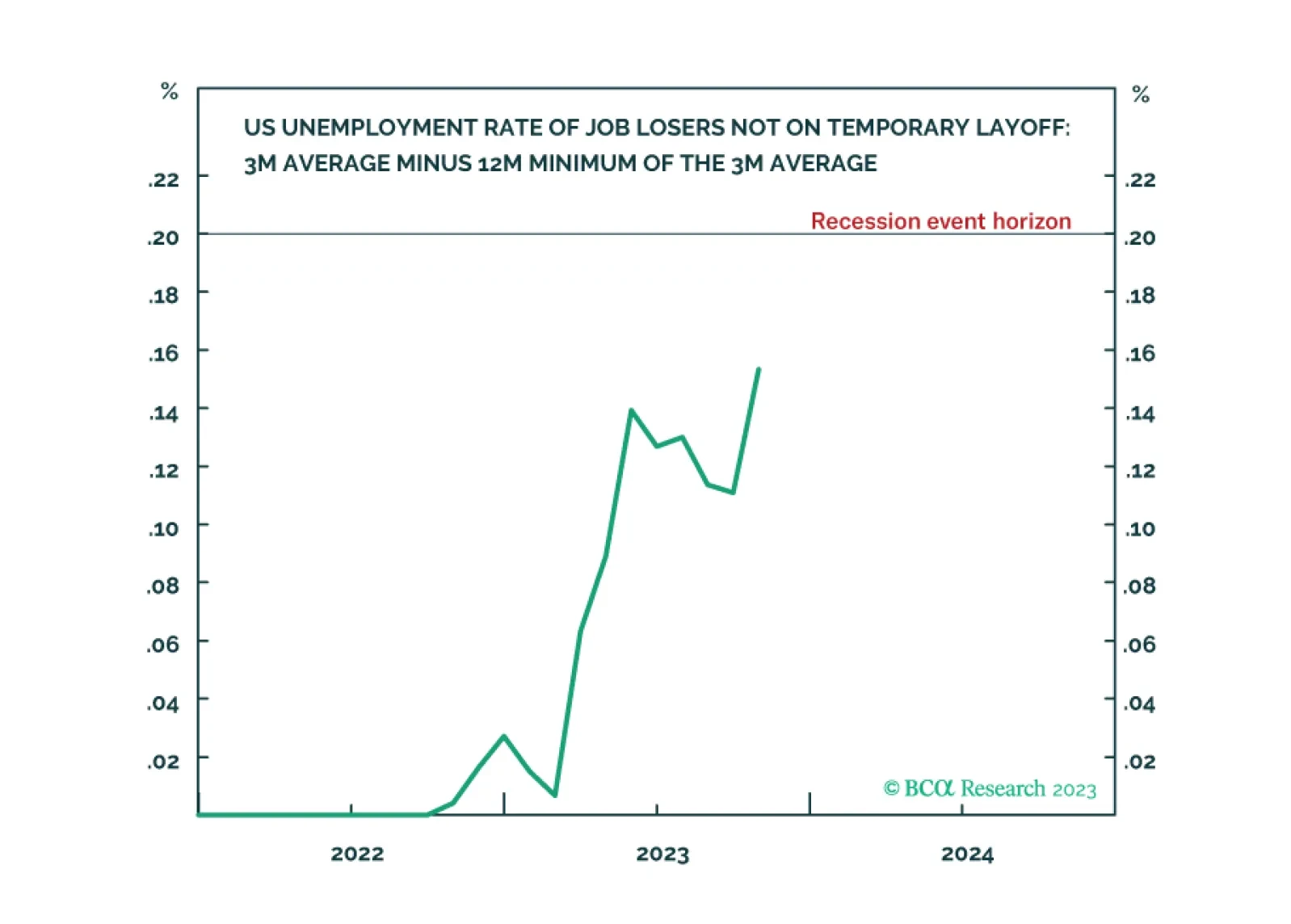

Illegal immigration into the US has skyrocketed to record levels. Correctly accounting for this, US real consumption growth on a per head basis is already fragile. Meanwhile, the real bond yield is only now approaching the pain point that typically triggers a recession. Ahead of the upcoming US jobs report, we point out what it would take for the Joshi rule real-time US recession indicator to breach its event horizon. And how to position in stocks and bonds, both tactically and cyclically. Plus: potential turning points in Biotech and Genome, ADBE, and Taiwan versus China.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

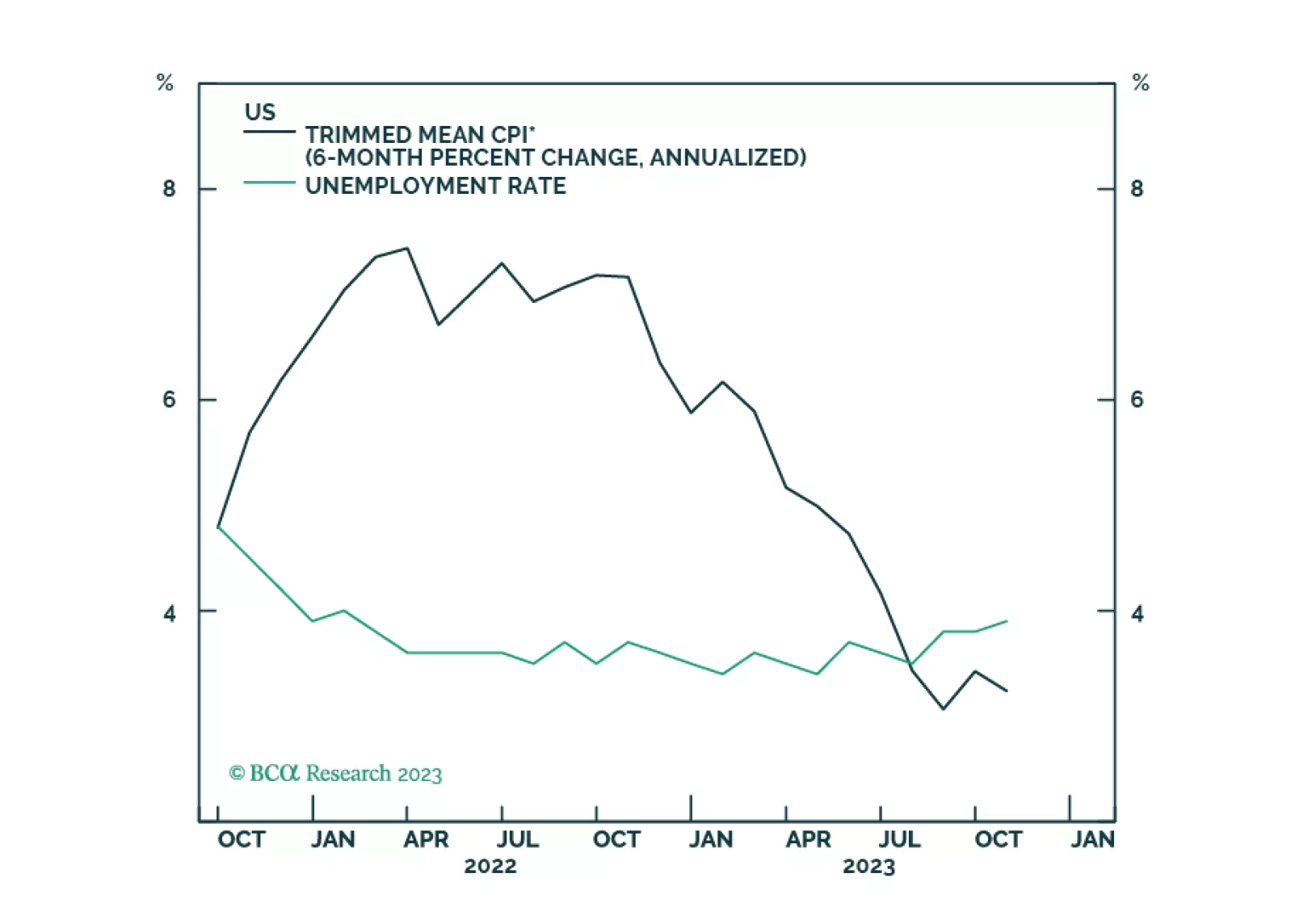

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

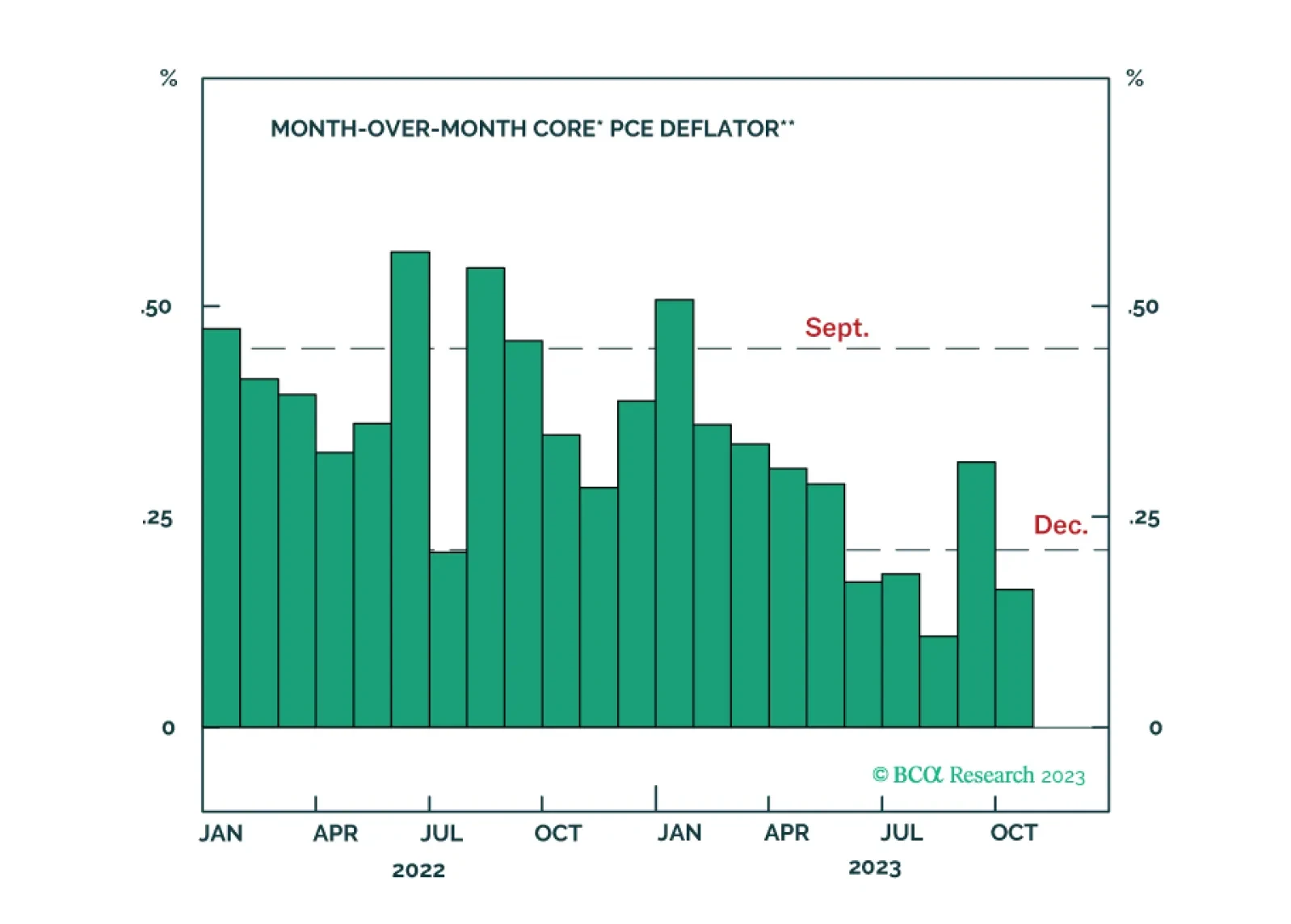

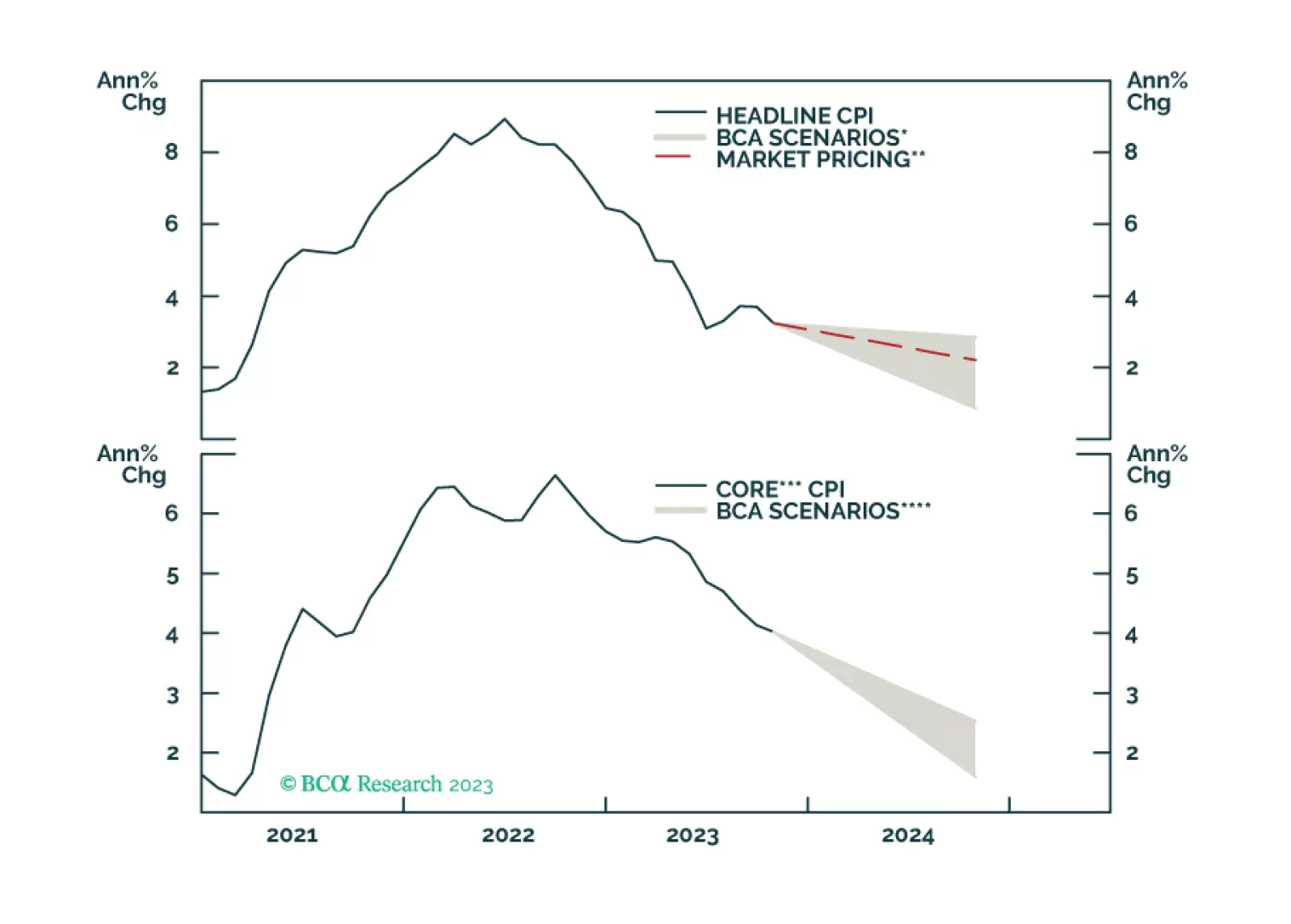

This week’s Special report revisits our TIPS Golden Rule. We provide a 12-month inflation forecast and discuss how it impacts our TIPS view.

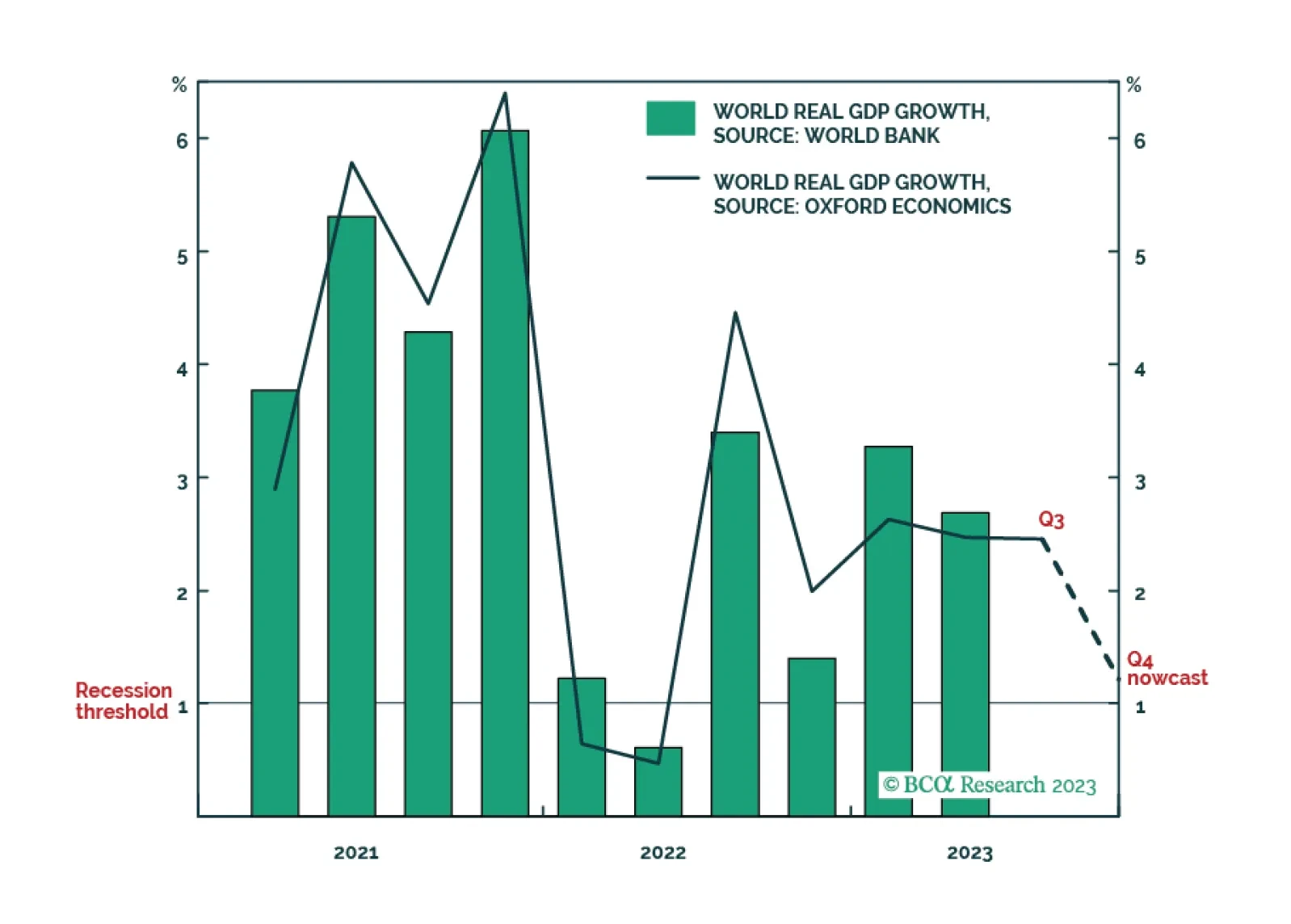

The latest ‘nowcast’ for world economic growth in the fourth quarter has plunged to just 1.2 percent, marking the cusp of another world recession. One important implication is that expectations for oil demand growth and industrial metal demand growth are way too optimistic.

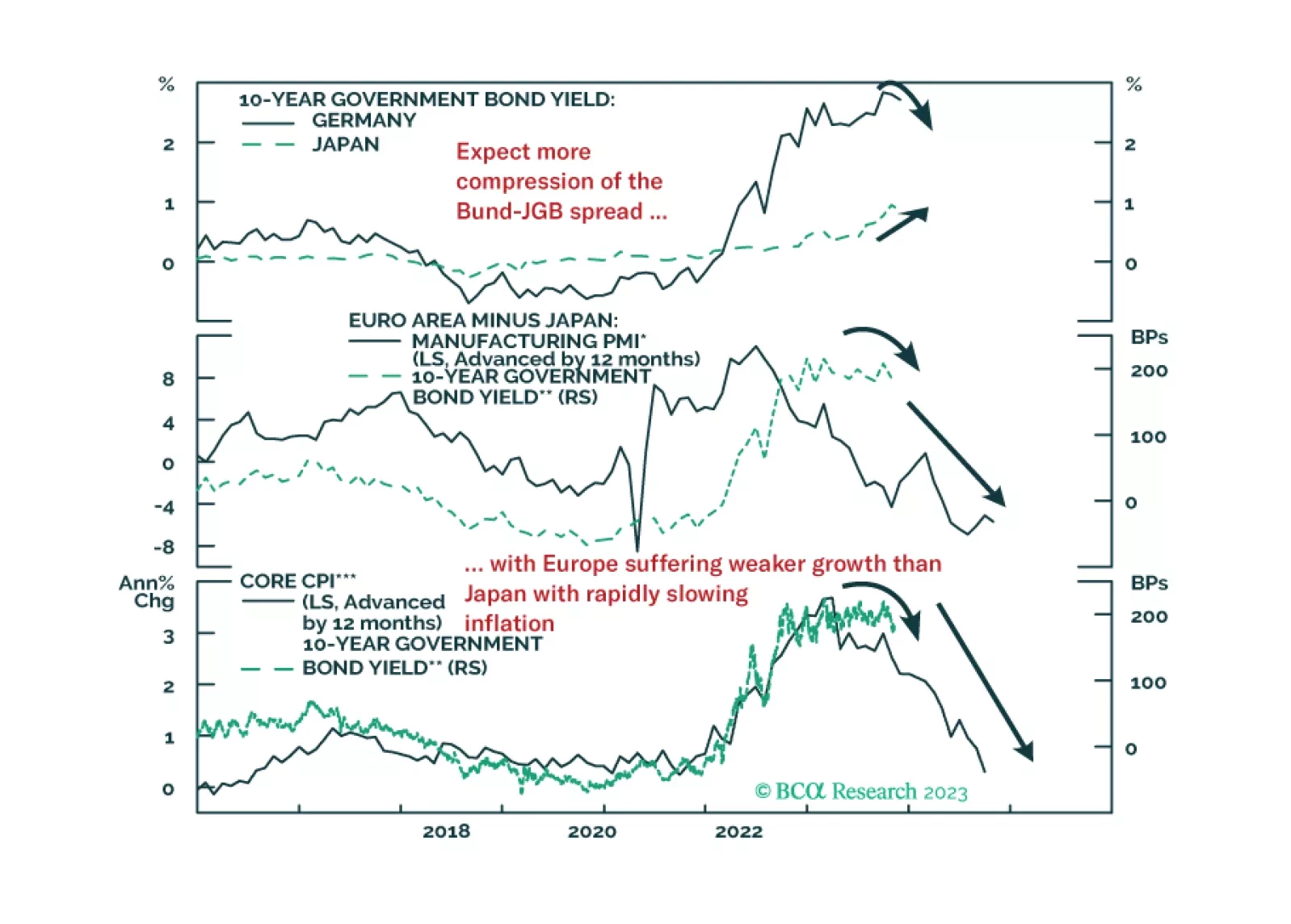

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.

Following the October US jobs data, the ‘Joshi rule’ real-time US recession indicator increased from 0.11 to 0.15, meaning that it is fast approaching its event horizon of 0.20. We go through the investment implications. We also highlight a new long-term recommendation. Plus, the Norwegian krone is close to a potential rebound.