Inflation

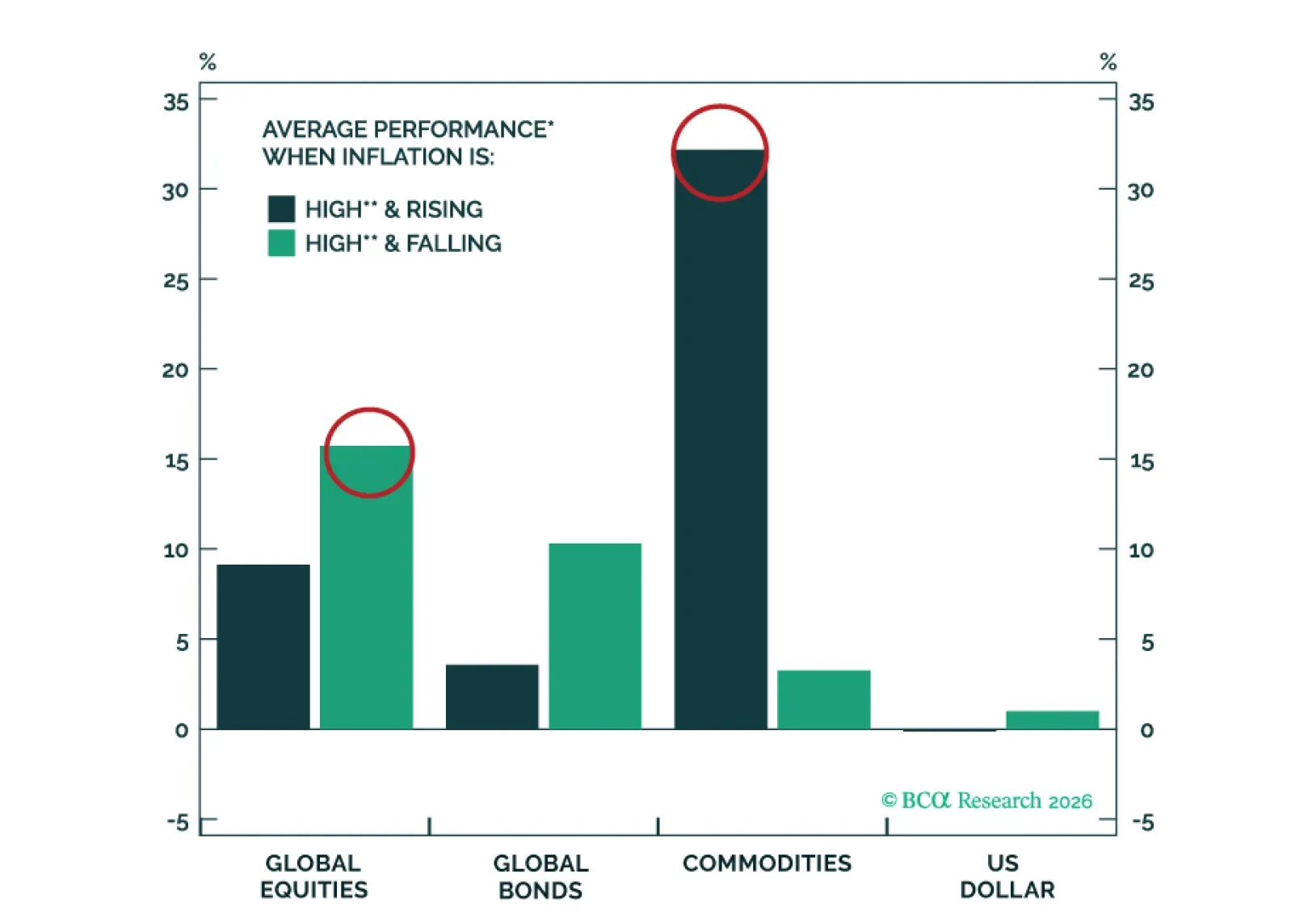

The Iran war provides a timely motivation for examining how the main financial asset classes and commodity sectors perform across different inflation regimes and during periods of elevated geopolitical risk.

We are pleased to introduce our new Quarterly Investment Outlook, a joint publication bringing together the European Investment Strategy (EIS), Global Fixed Income Strategy (GFIS), and Foreign Exchange Strategy teams.

The main takeaway of the current edition is that investors should not add risk. Markets are still focused on inflation, but the binding constraint is growth: if the energy shock persists into mid-April, a rapid shift toward recession pricing will follow.

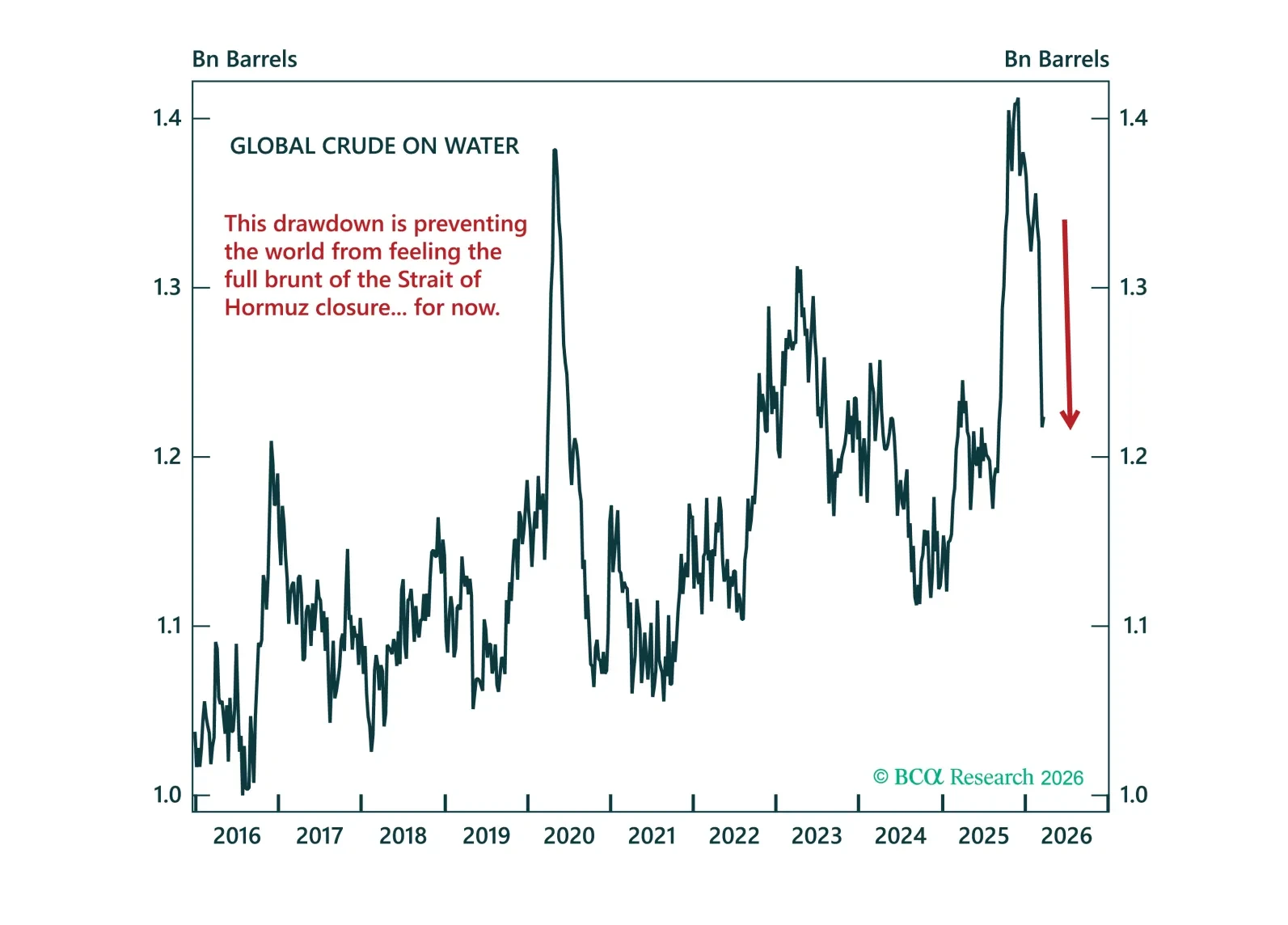

One month into the Iranian conflict, we take stock of how markets have moved so far and how some of the big open questions might influence them going forward. A long opportunity may be developing at the long end of the Treasury curve.

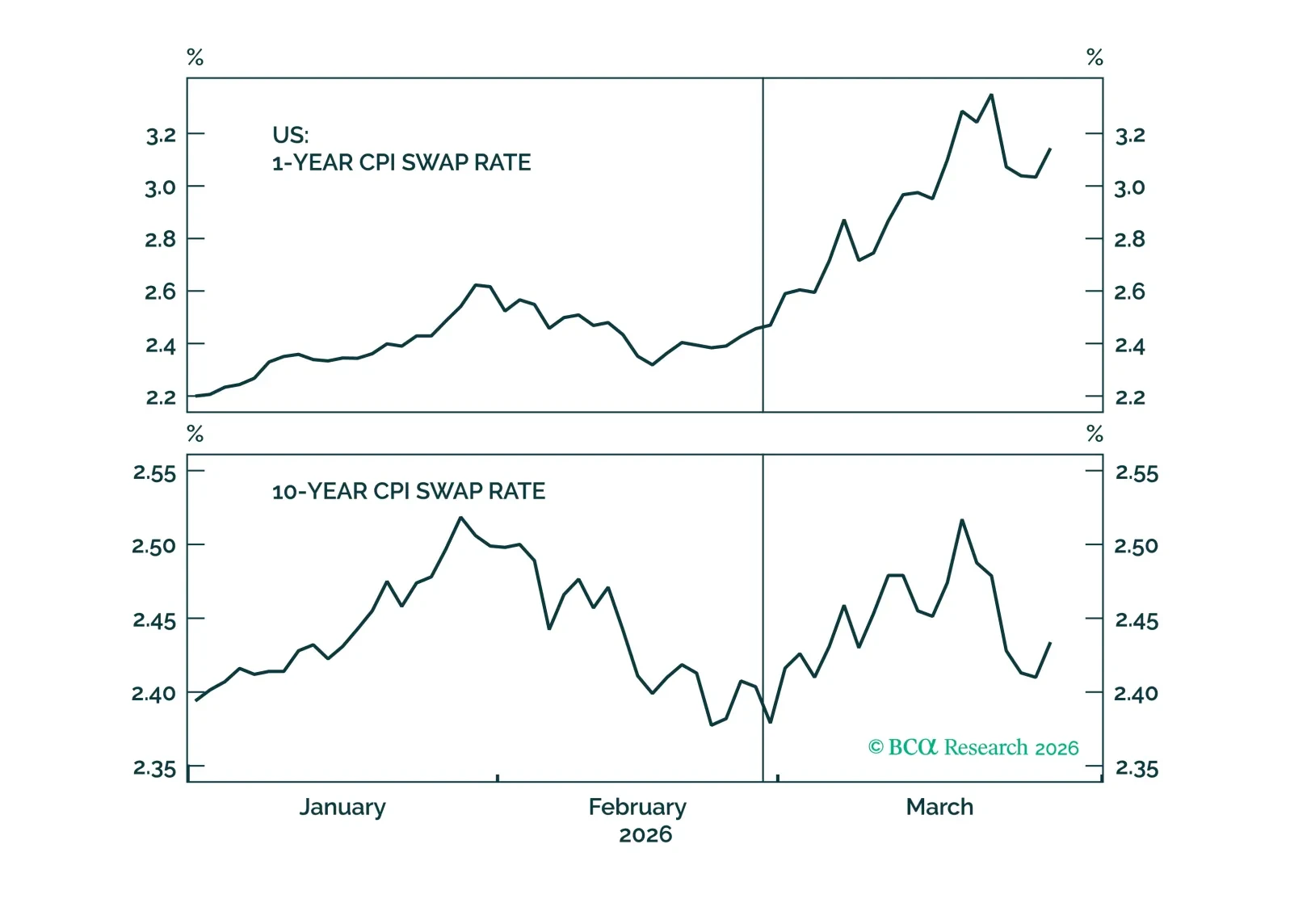

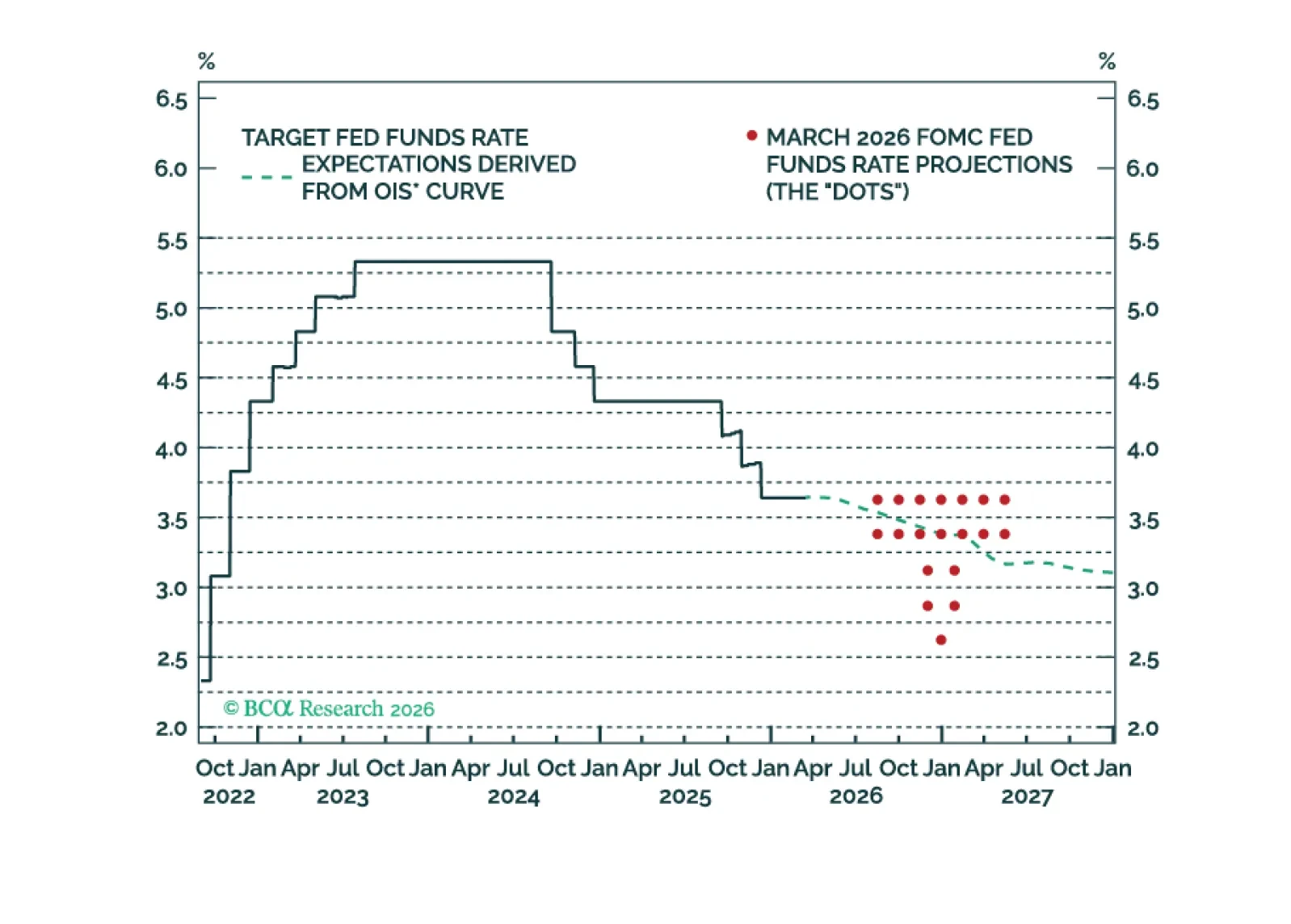

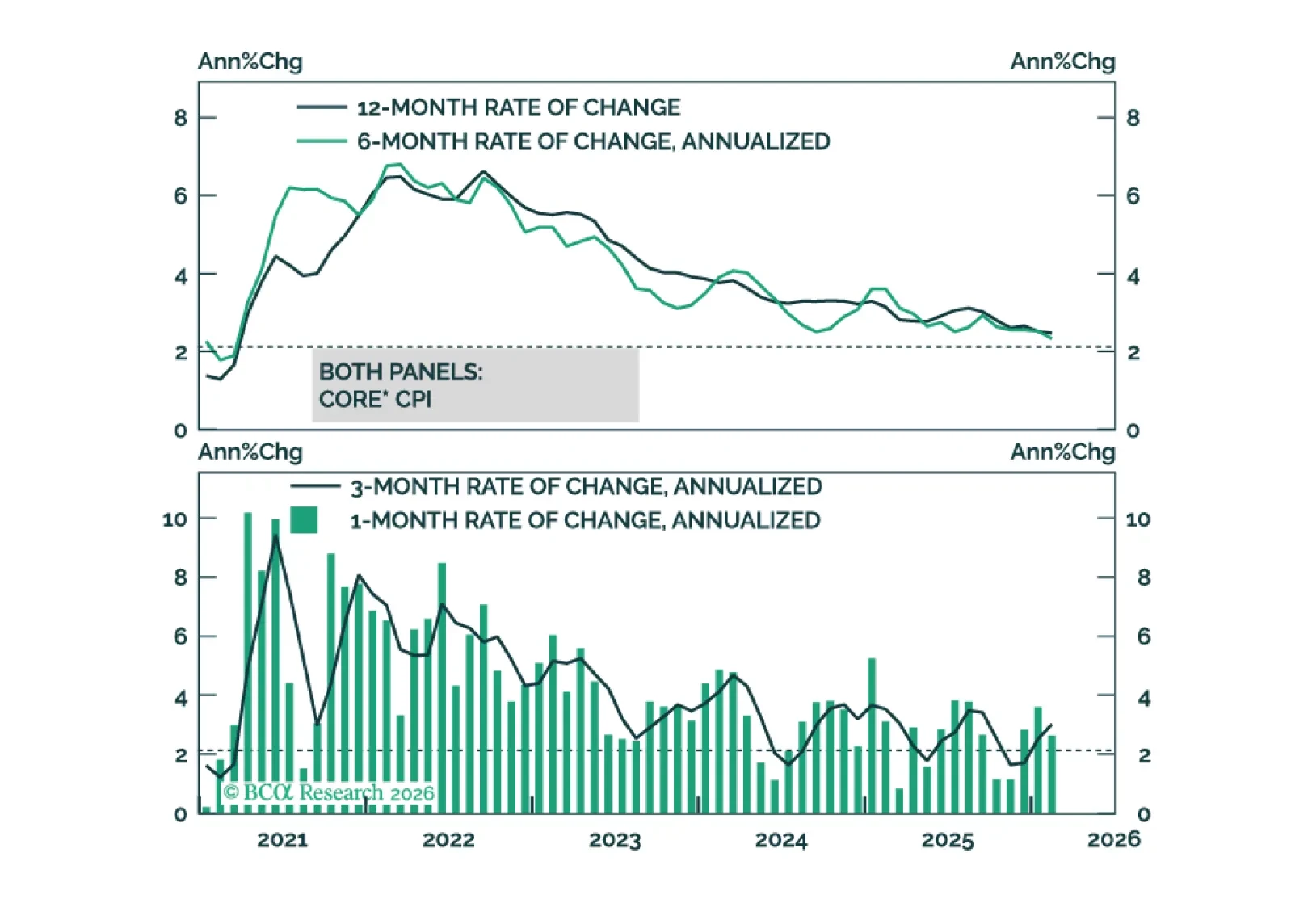

The Fed will not cut rates again until core inflation trends lower. This remains likely as the tariff impact on goods inflation wanes, but the recent energy price shock could delay any meaningful downtrend.

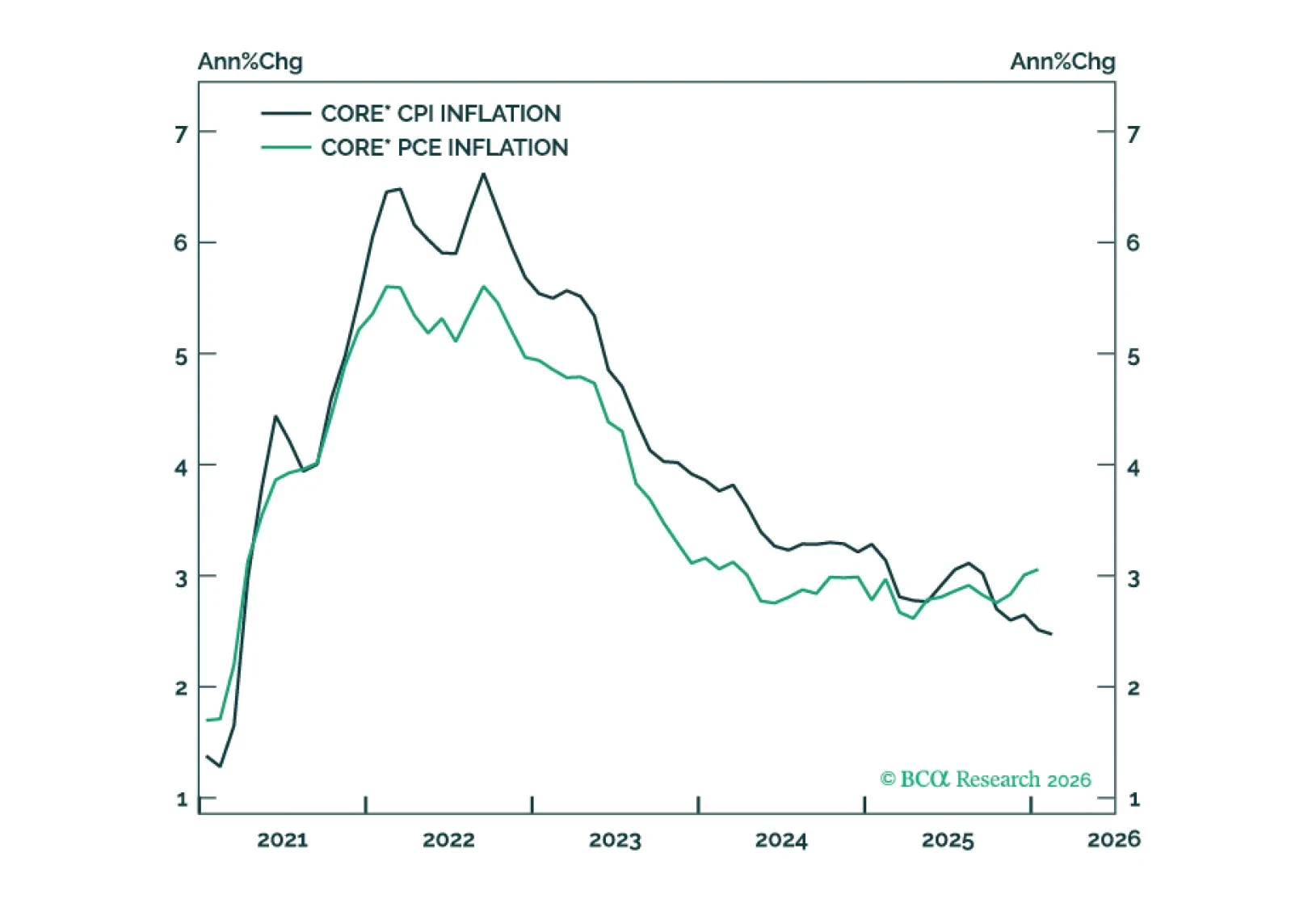

The gap between PCE and CPI inflation will narrow within the next few months, mostly driven by core PCE inflation converging toward its trimmed mean.

The recent oil price shock reinforces our view that inflation will surprise to the upside during the next few months but fall rapidly in H2 2026.

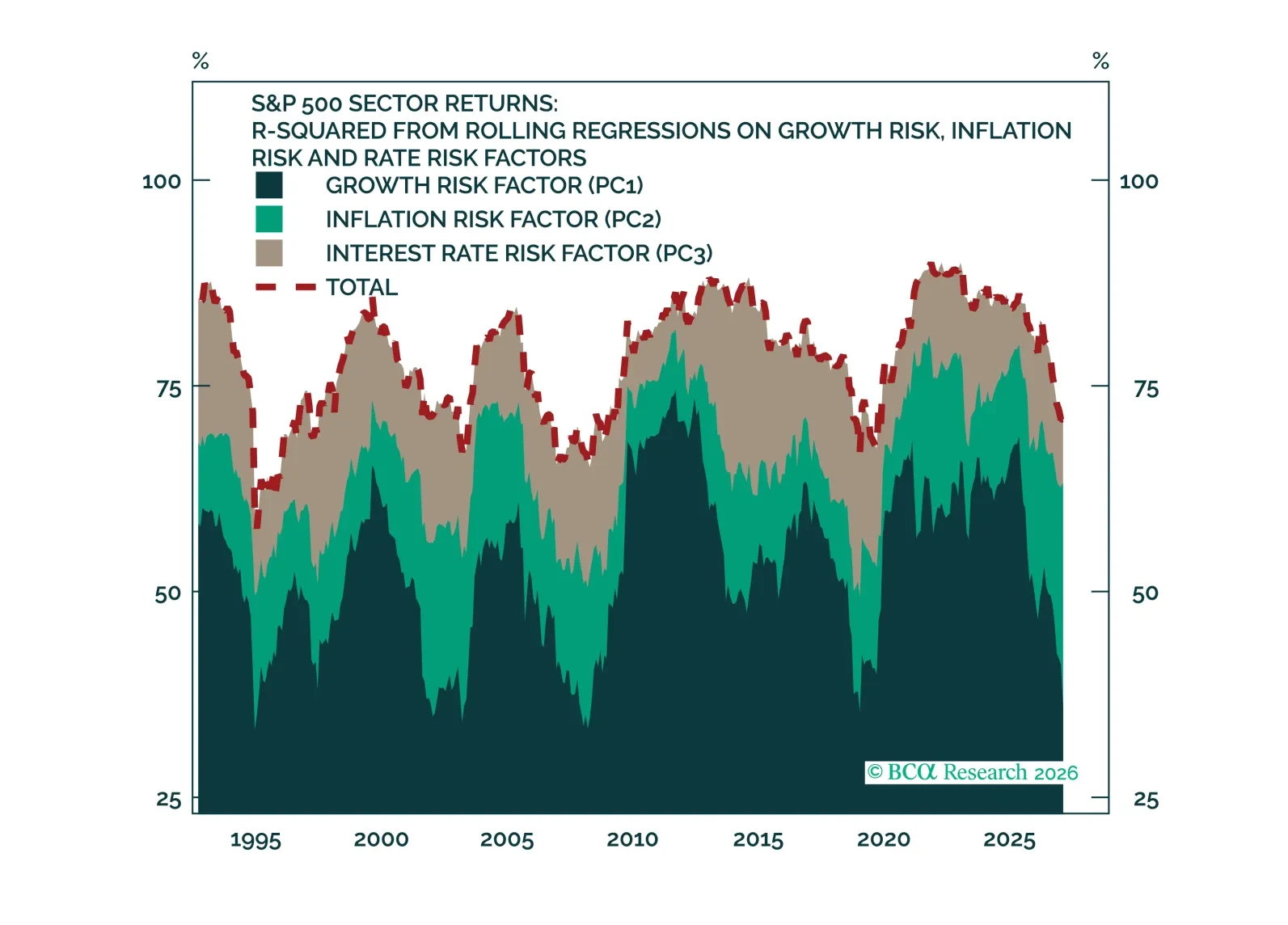

Growth, inflation, and rate risk drive sector returns and fundamentals, but macro’s explanatory power is at multi-decade lows. Long/short industry-group baskets show the equity market has turned pessimistic about growth, a potential opportunity as the macro data firm. The market’s inflation view has climbed, a move that may be harder to fade given rising oil prices.

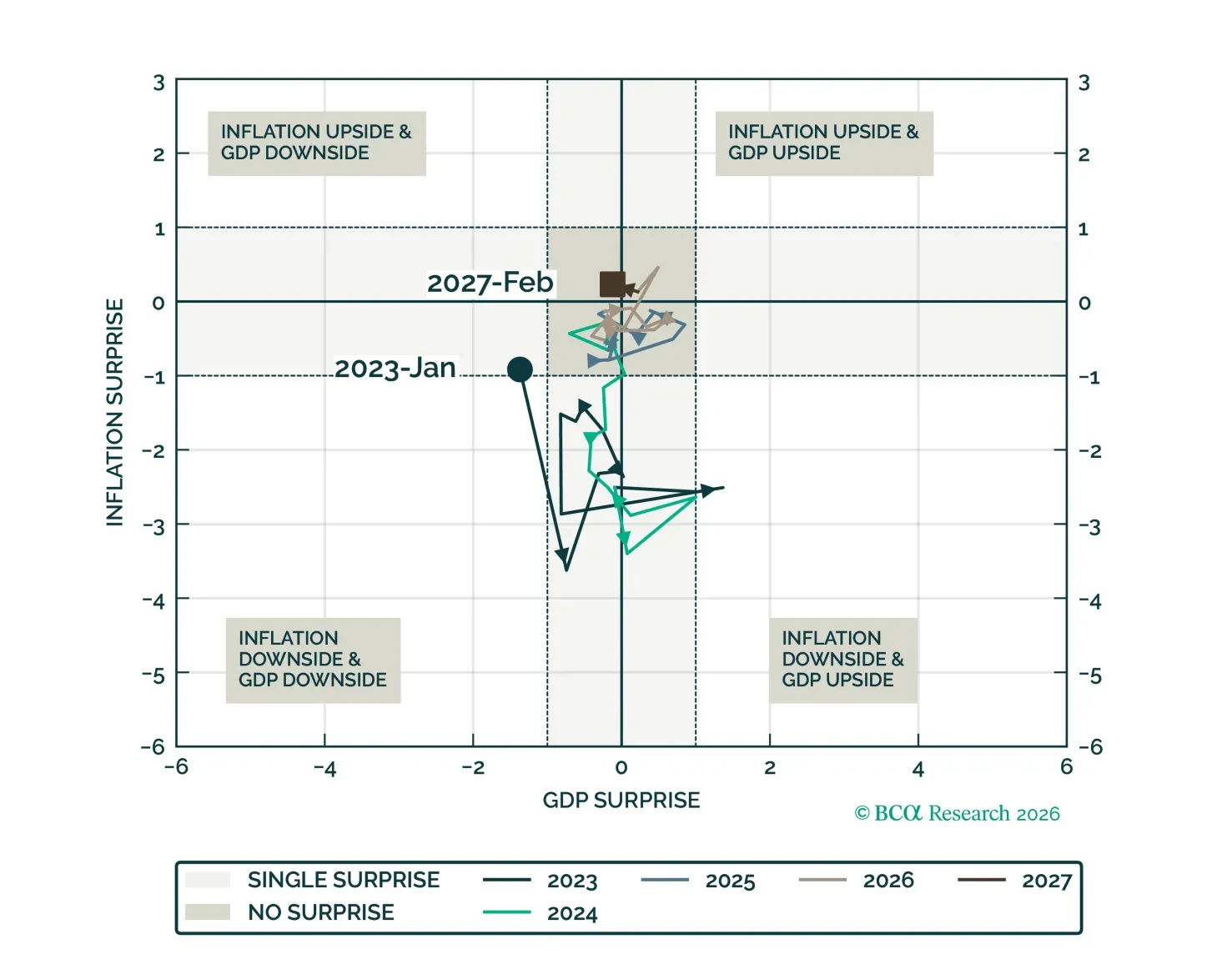

We introduce our Macro Regime Indicators (MRI), a framework for forecasting growth and inflation surprises in the US. The MRI on the economy shows no substantial mispricing in either growth or inflation over the next 12 months.

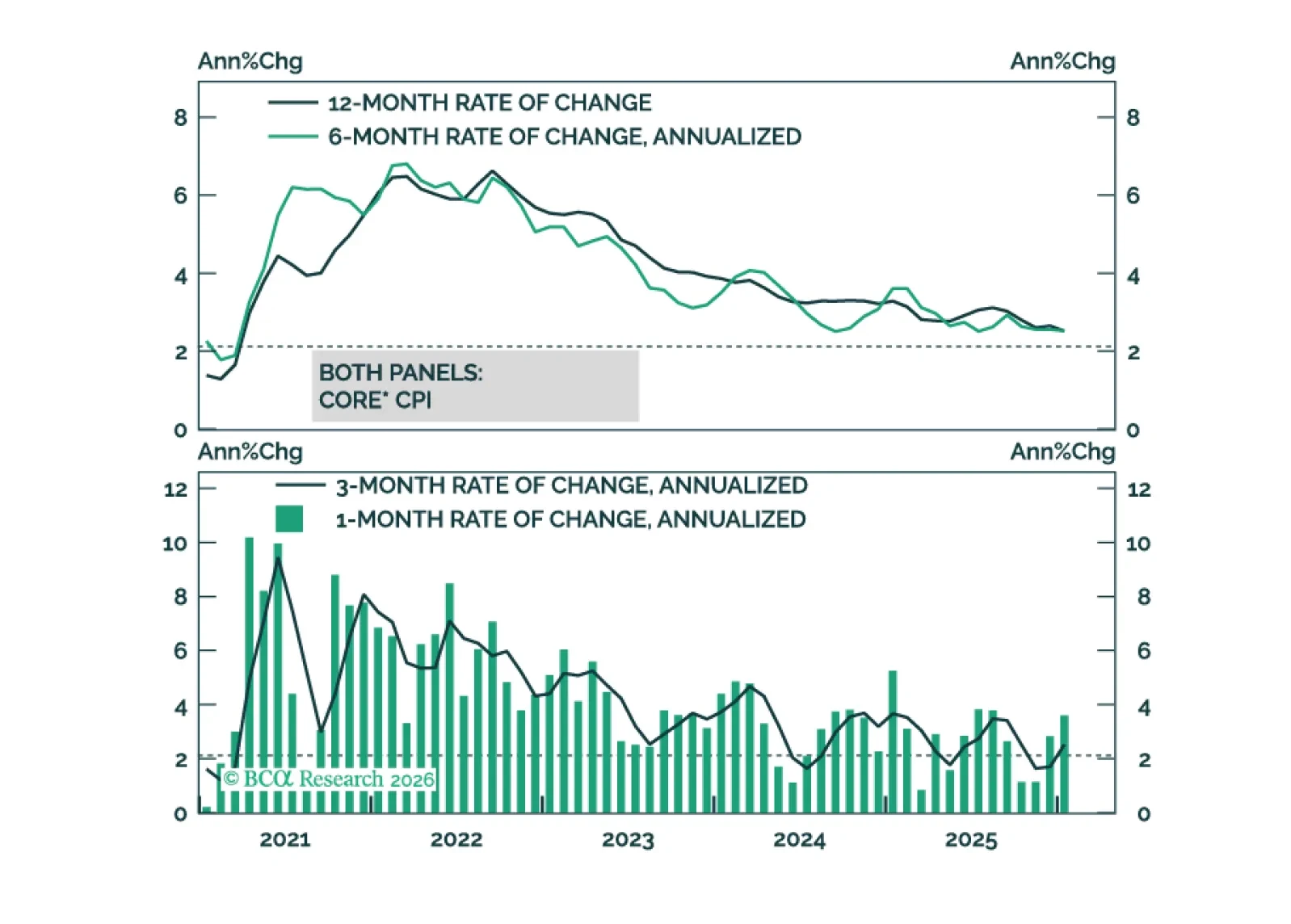

Core inflation will get close to the Fed’s 2% target by the end of this year.

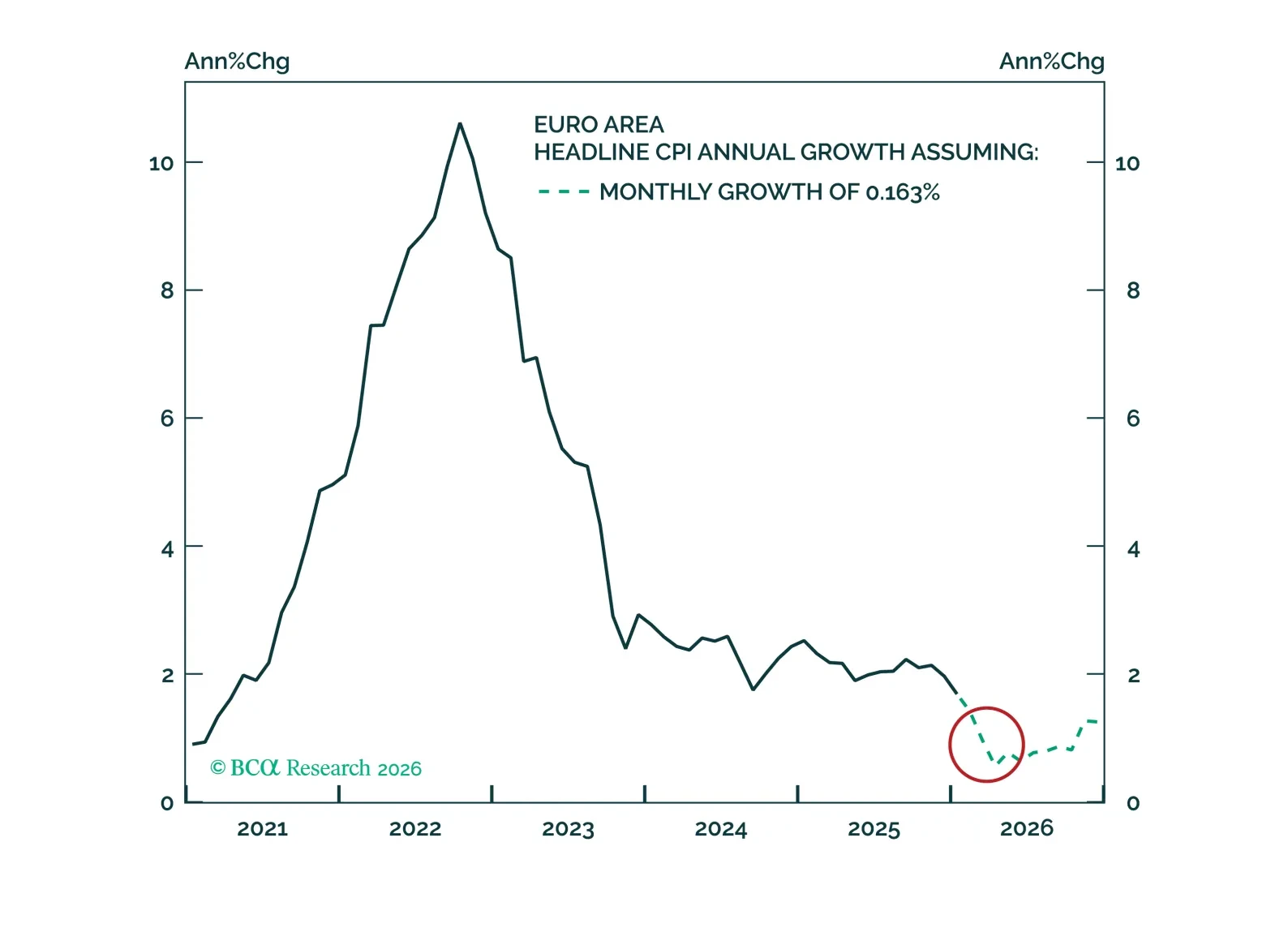

The ECB is about to make its first policy mistake in the current cycle by being complacent about the downside risks to inflation. The confluence of base effects, a stronger euro, food and energy deflation, and rapid services disinflation will push headline inflation closer to 1% in the first half of the year. This significant undershoot will force the ECB to deliver reflationary cuts. Go long the September 2026 3-month Euribor futures and tactically reduce exposure to inflation-linked bonds in the Eurozone.