Inflation

In Section I, we examine some concerning signs of US economic weakness that emerged in June. We also discuss portfolio positioning in the face of falling interest rates and cross-check our recommended US equity overweight in the face of extremely optimistic expectations about AI’s impact on growth. We conclude that defensive positioning continues to be warranted. In Section II, we dig into those optimistic expectations for AI. We find that the US equity market is significantly overvalued unless the deployment of AI technology causes a 10-to-20 year productivity surge in line with what occurred during the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. We doubt that AI will end up truly boosting economic activity by this magnitude.

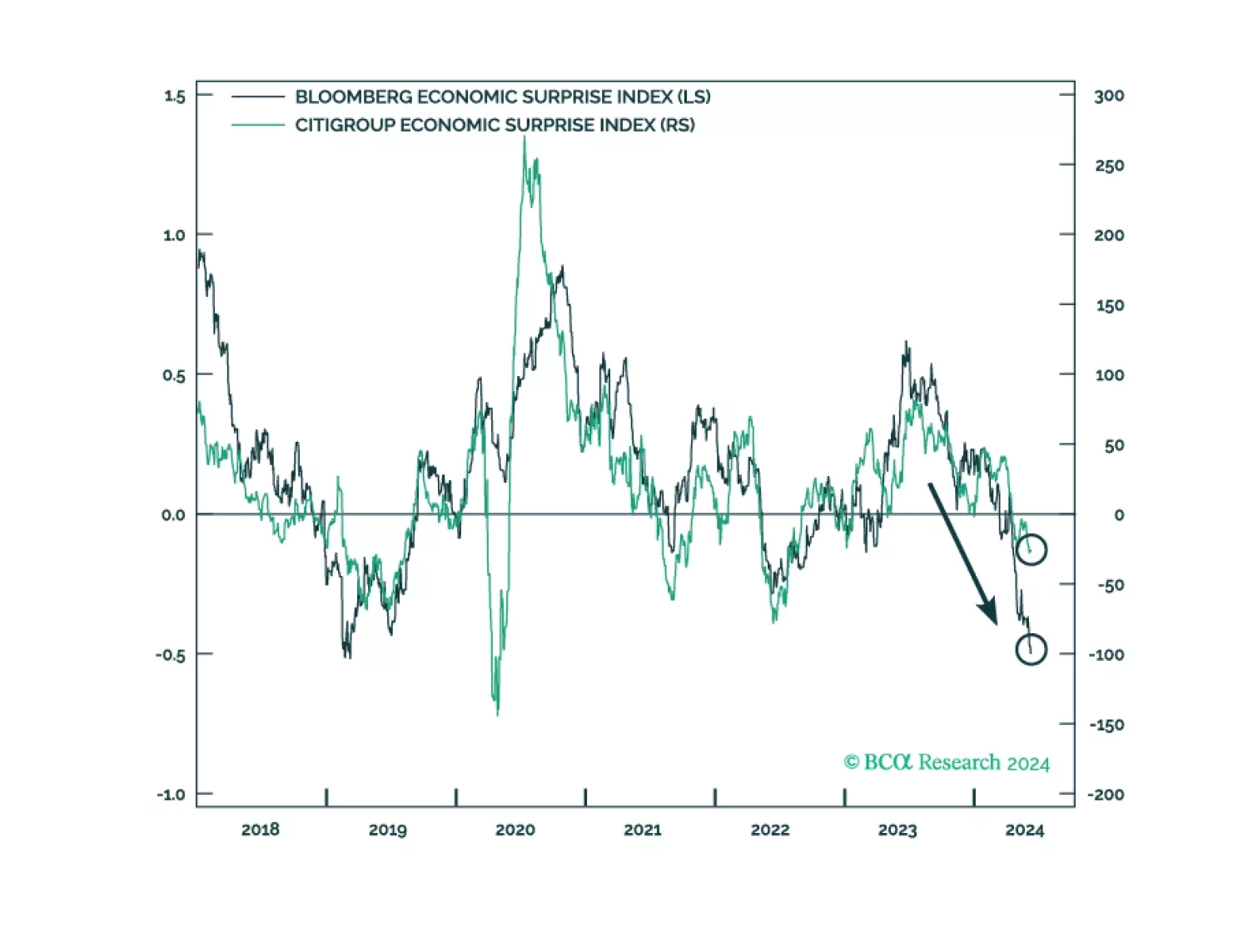

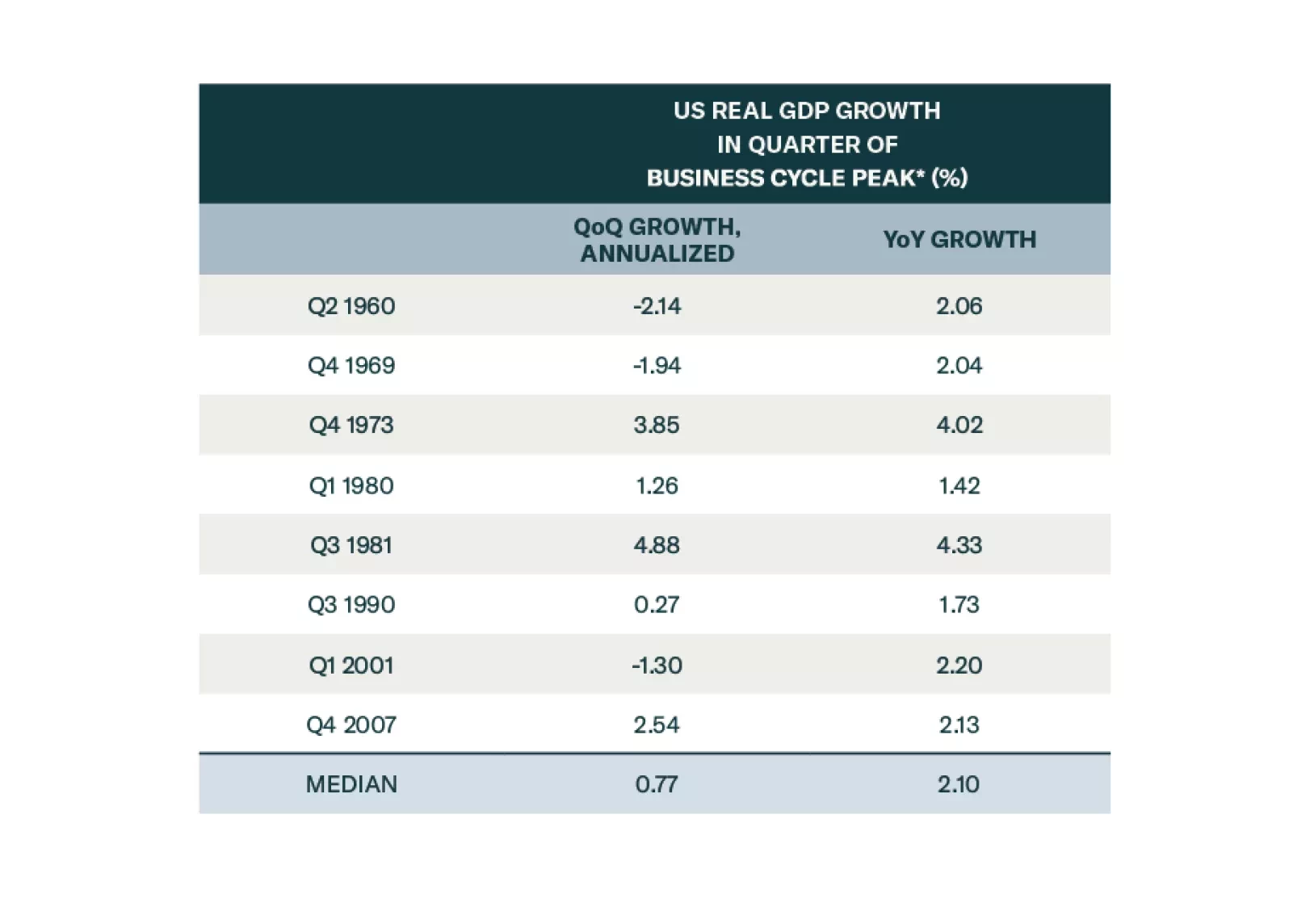

The consensus soft-landing narrative is wrong. The US will fall into a recession in late 2024 or early 2025. We were tactically bullish on stocks most of last year, turned neutral earlier this year, and are going underweight today. We conservatively expect the S&P 500 to drop to 3750 during the coming recession.

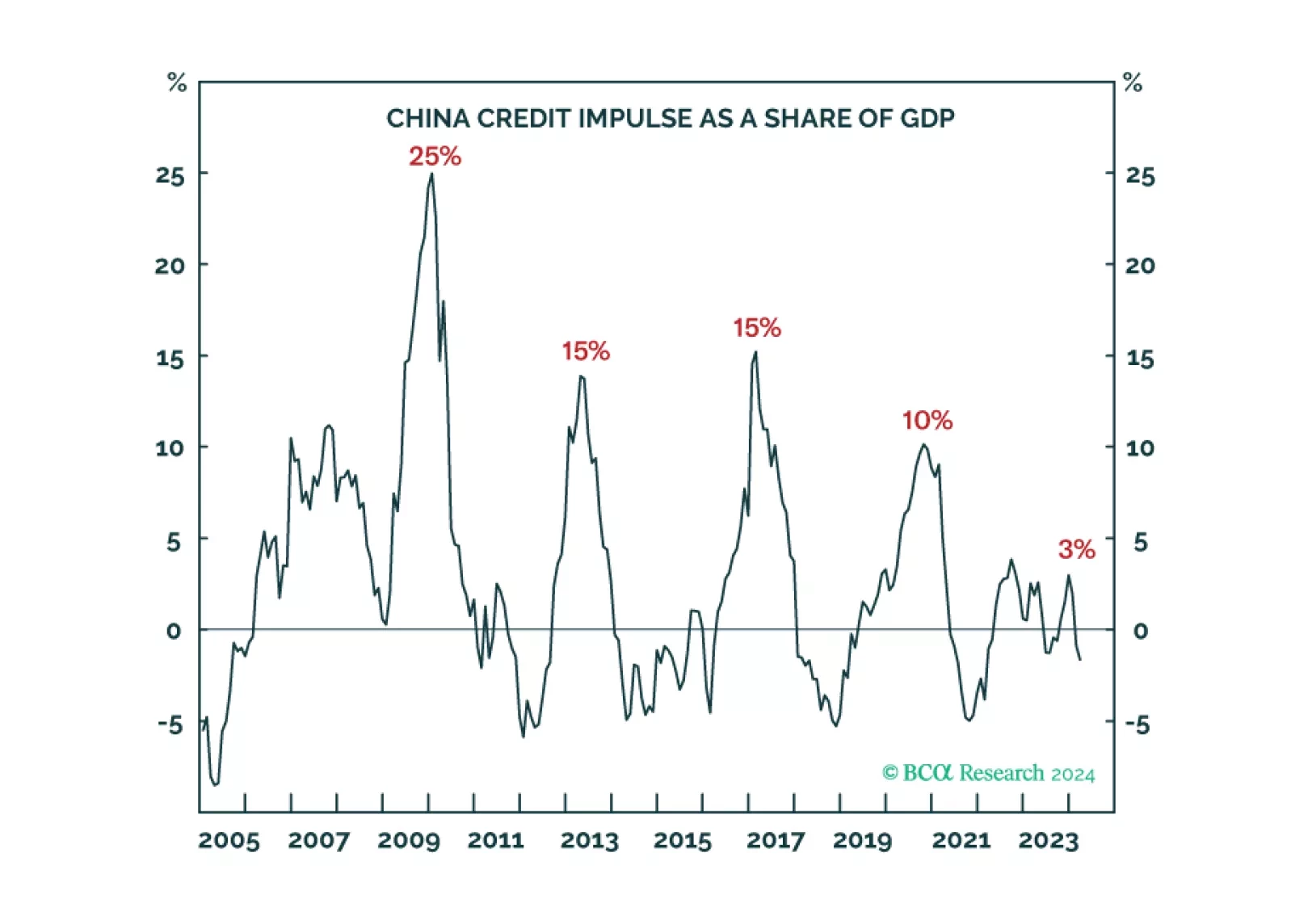

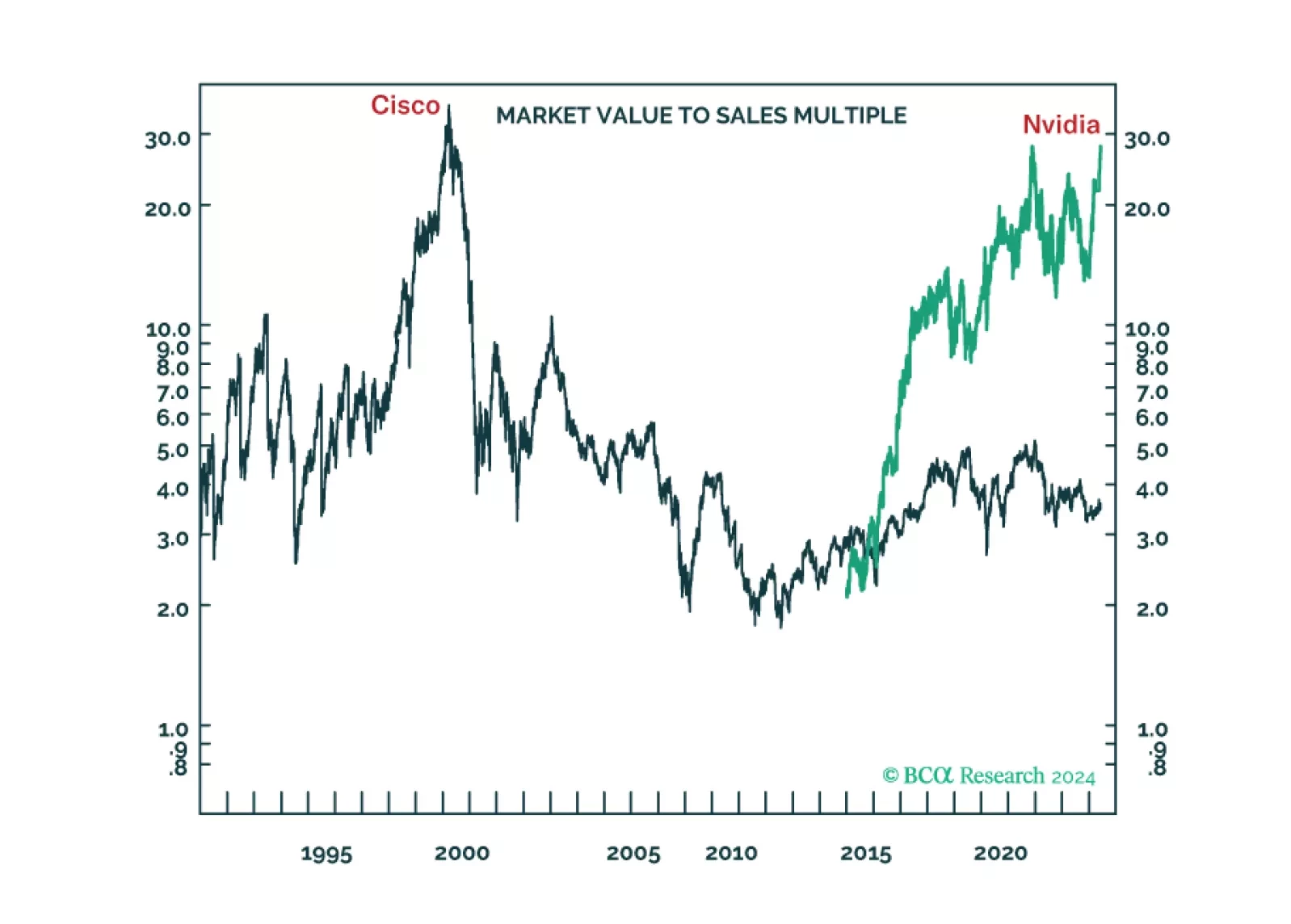

The end of China’s exponential credit growth will impede structural rallies in Chinese stocks and commodities, but US superstar stocks’ bubble-like valuations will impede them too. Leaving European stocks as the likely structural outperformer. Plus: copper is correcting, NVDA is consolidating.

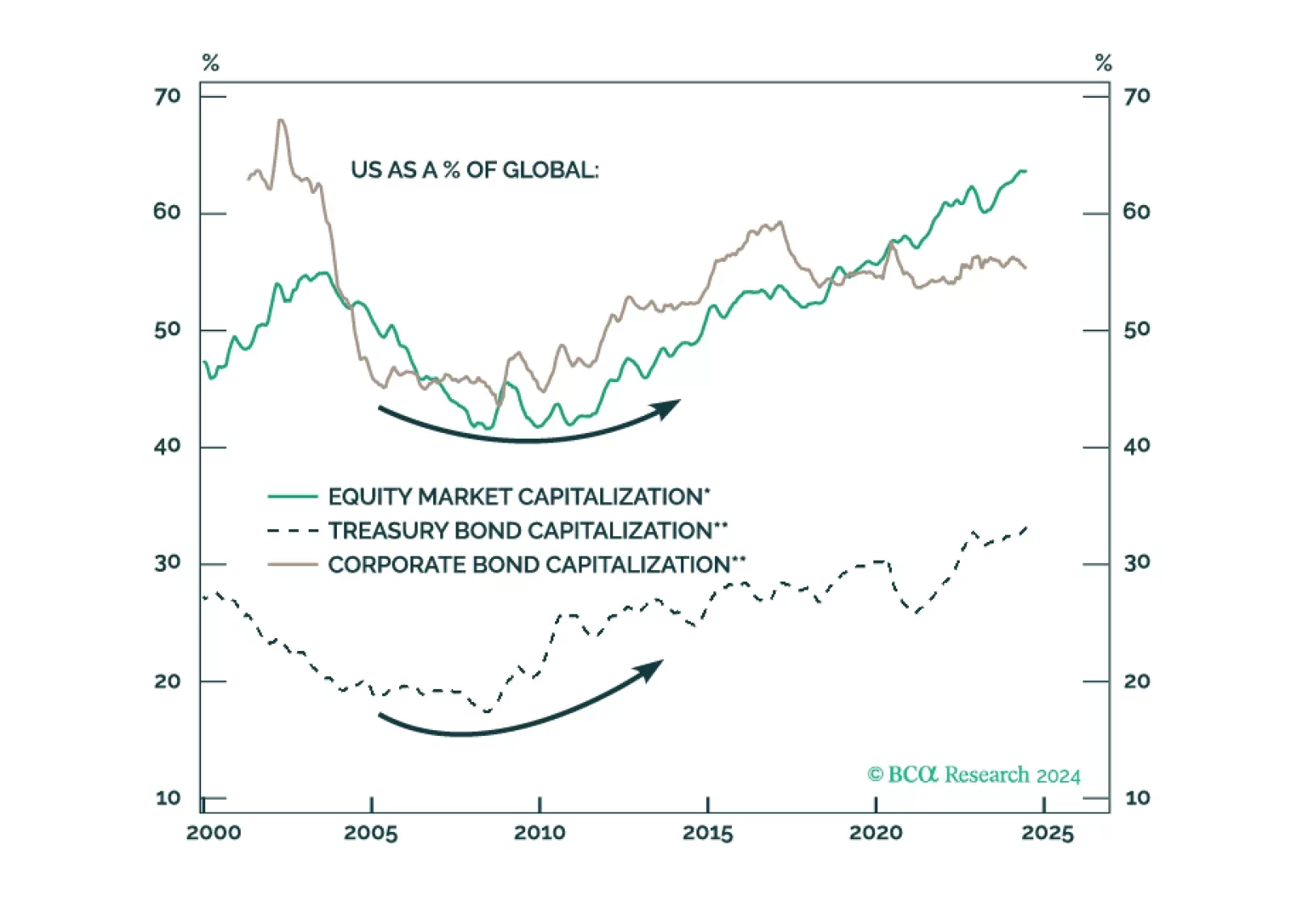

US assets and the US dollar should remain resilient relative to global peers over the next 12 months as policy uncertainty, election risk, and geopolitical risk reach a climax. After that, investors should reassess their regional allocation.

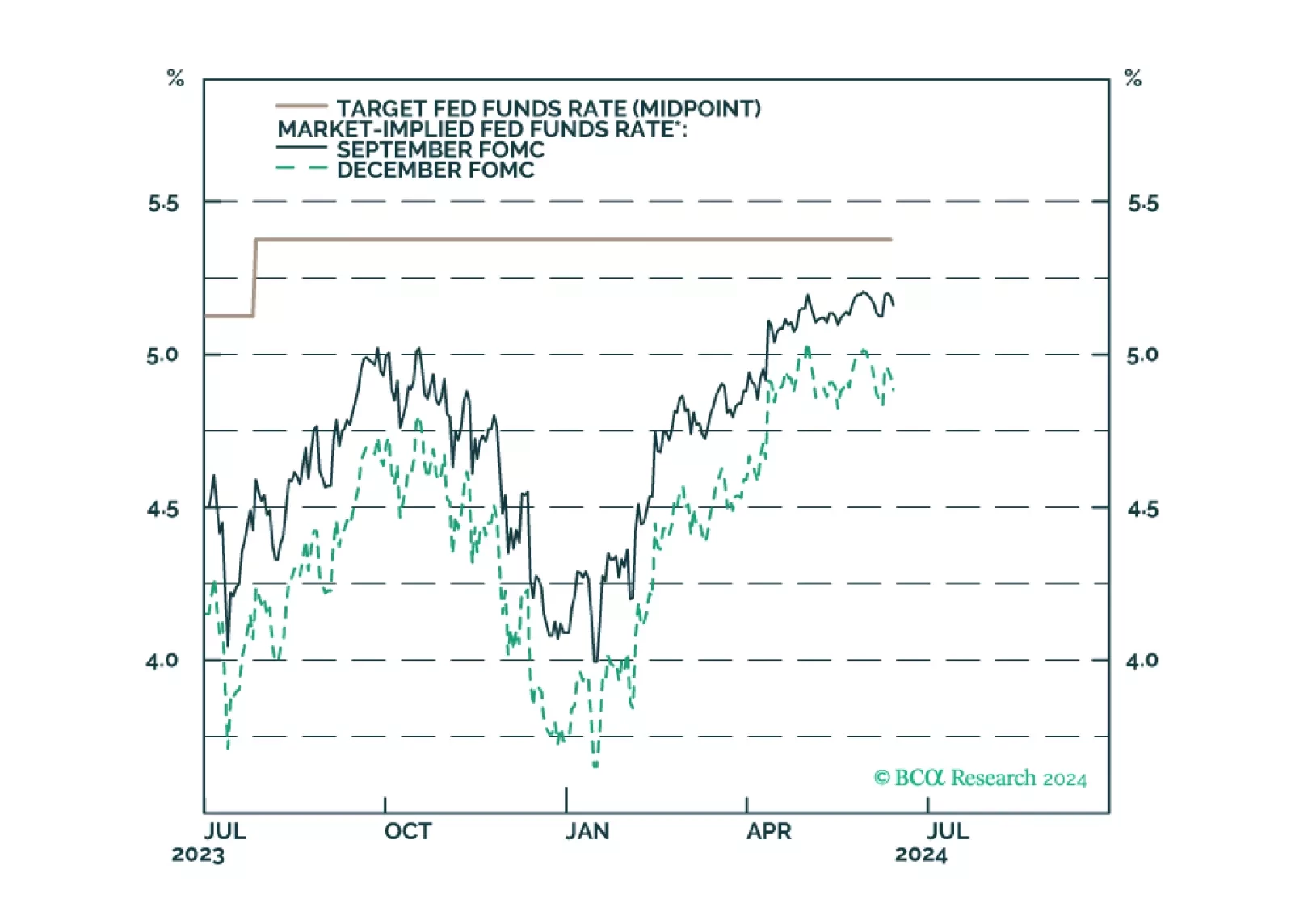

Our reaction to this morning’s CPI report and this afternoon’s FOMC meeting.

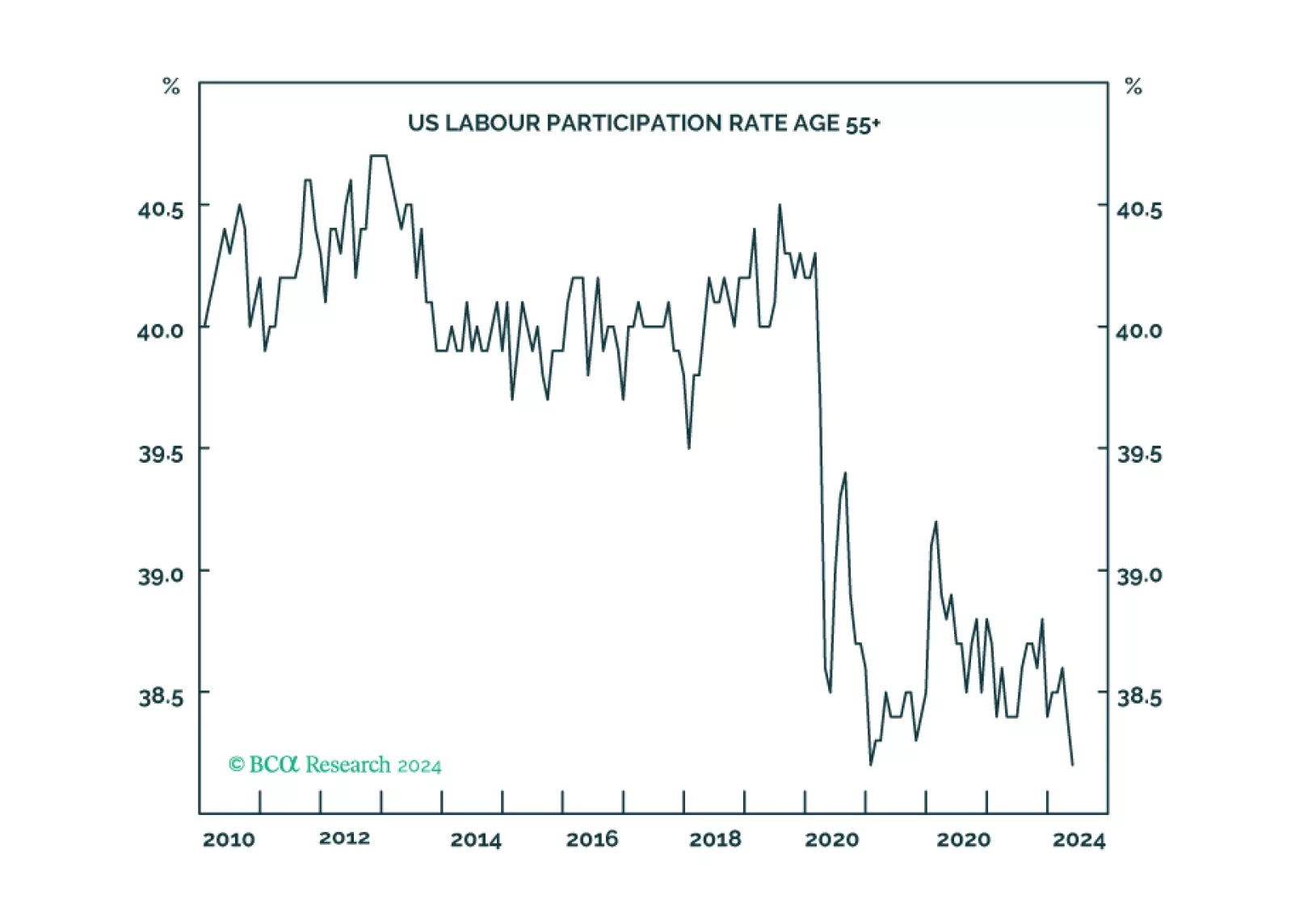

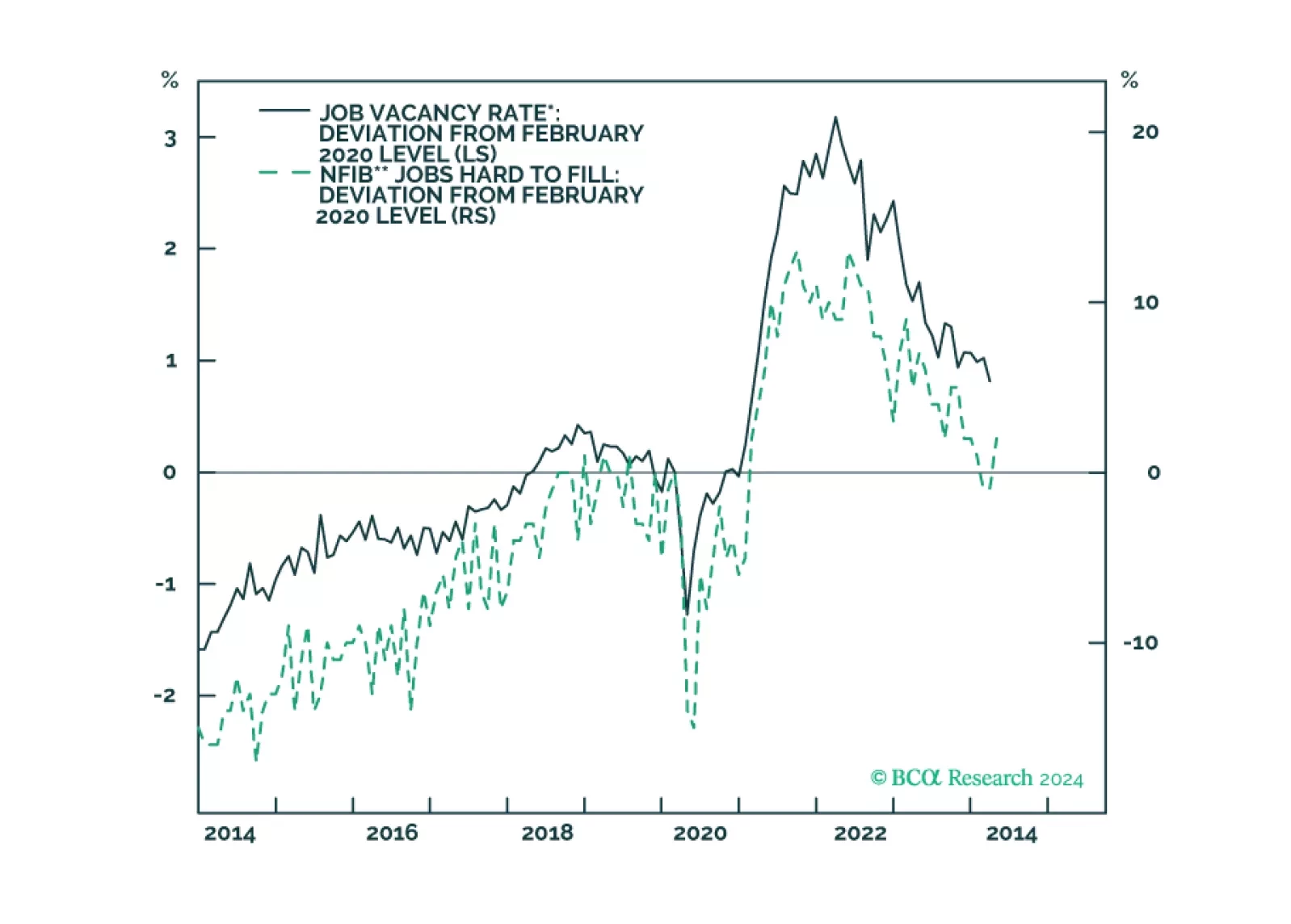

1 in 17 older Americans workers have gone missing either through ‘excess retirements’ or ‘excess mortality’. The consequent dislocation of the labour market means that the Fed’s work is not yet done. We go through some investment implications. Plus: the China and Japan rallies are exhausted.

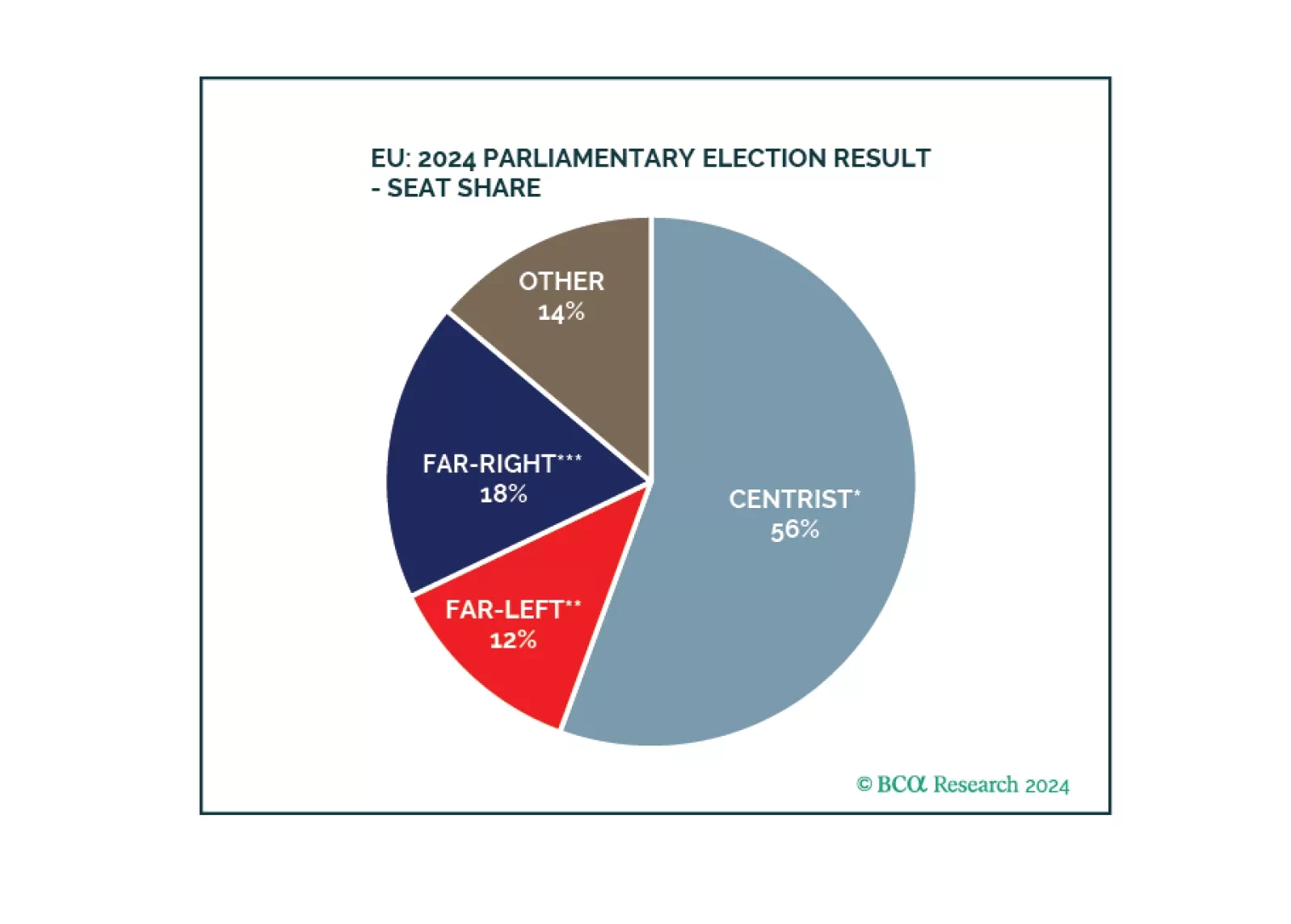

Europe did not witness a major policy reversal. Inflationary pressures are coming down, enabling the ECB to cut rates and European states to maintain soft budgets. Geopolitical challenges ensure that European parties continue to cooperate on national defense, economic security, and energy security.

The long-term winners from the generative-AI gold rush are unlikely to be the ‘picks and shovels’ stock Nvidia or the overvalued US superstars of Web 2.0. We discuss the structural investment implications. Plus: time to go tactically overweight global consumer discretionary (RXI).

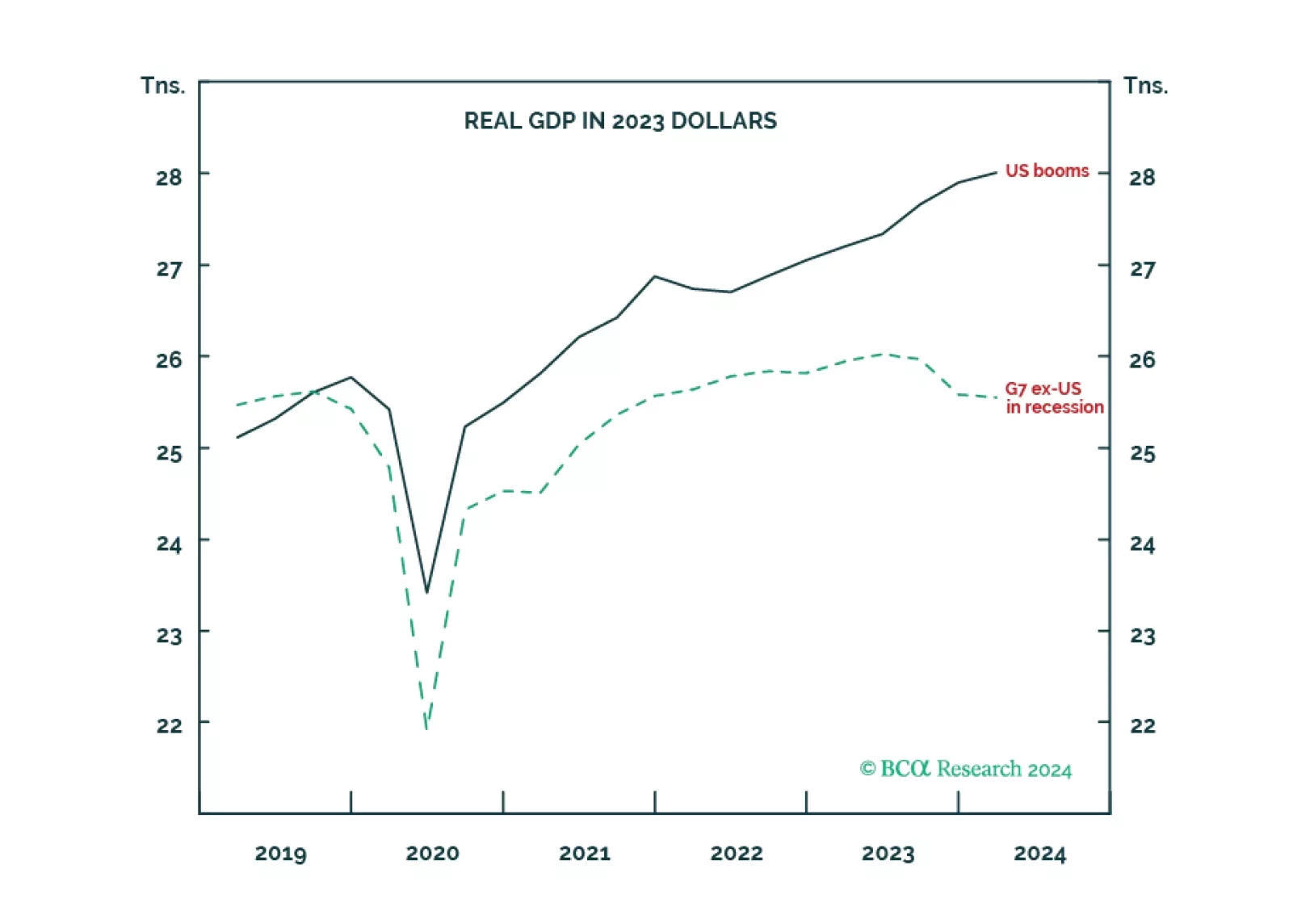

The economic schism in the world economy, between the non-US developed economy in recession and the US in strong growth, is unprecedented during our lifetimes. Now the schism will continue in reverse, as the non-US developed economy rebounds while the US fades. There are important implications for rates, the dollar, and sector and regional equity allocation which we discuss. Plus: base metals are a tactical short.

Our updated views on Treasury yields and Fed policy following this morning’s CPI report.