Iran

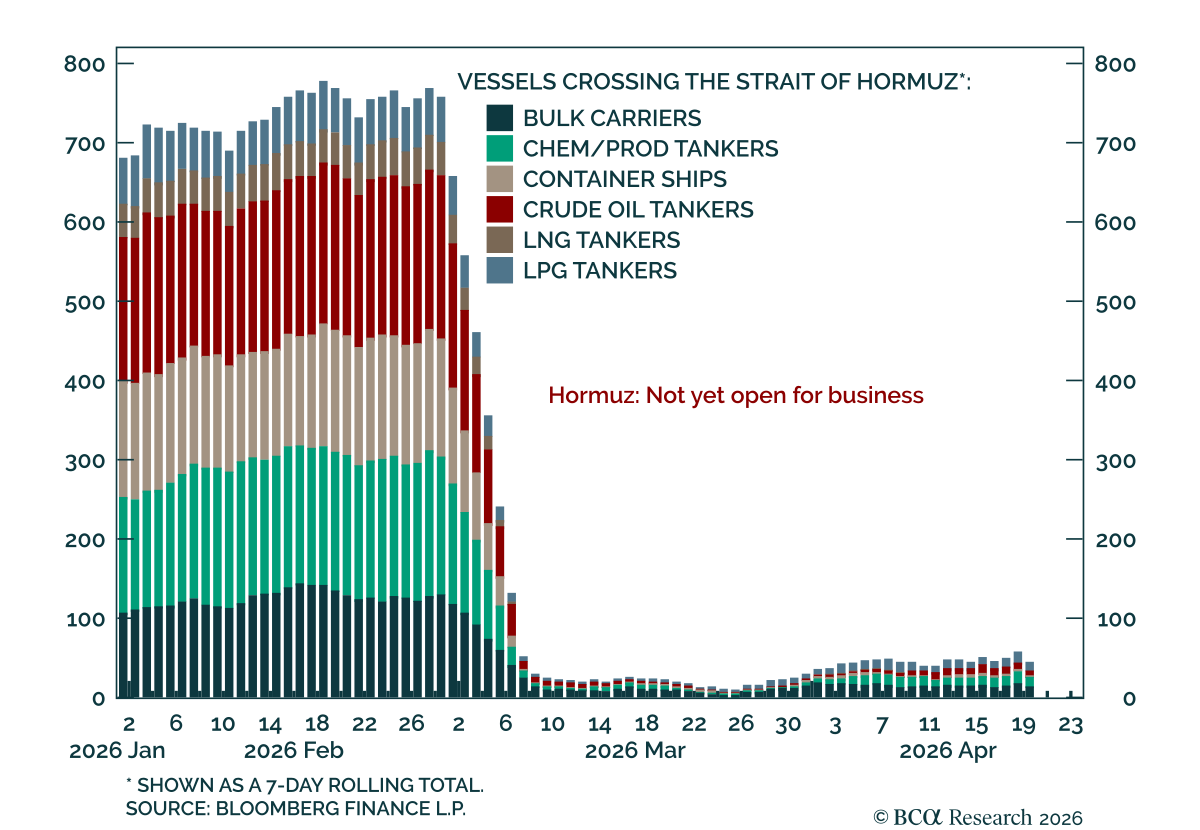

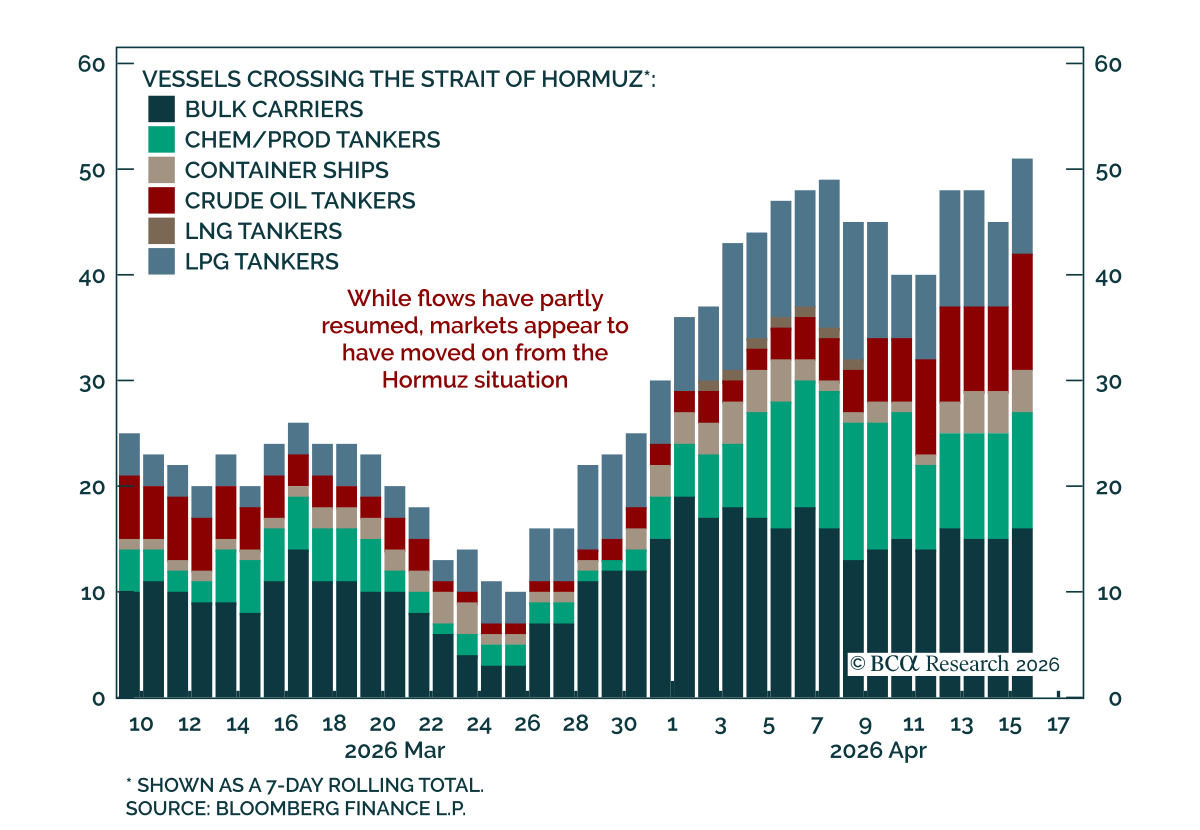

Weekend developments showed Hormuz traffic has not resumed yet, despite earlier signals that the Strait had reopened. Iran signaled the Strait was closed again, while the US seized an Iranian ship. There were also rumors of a second round of US-Iran…

Red Light. Green Light. So much for the “all clear” in the Hormuz saga.

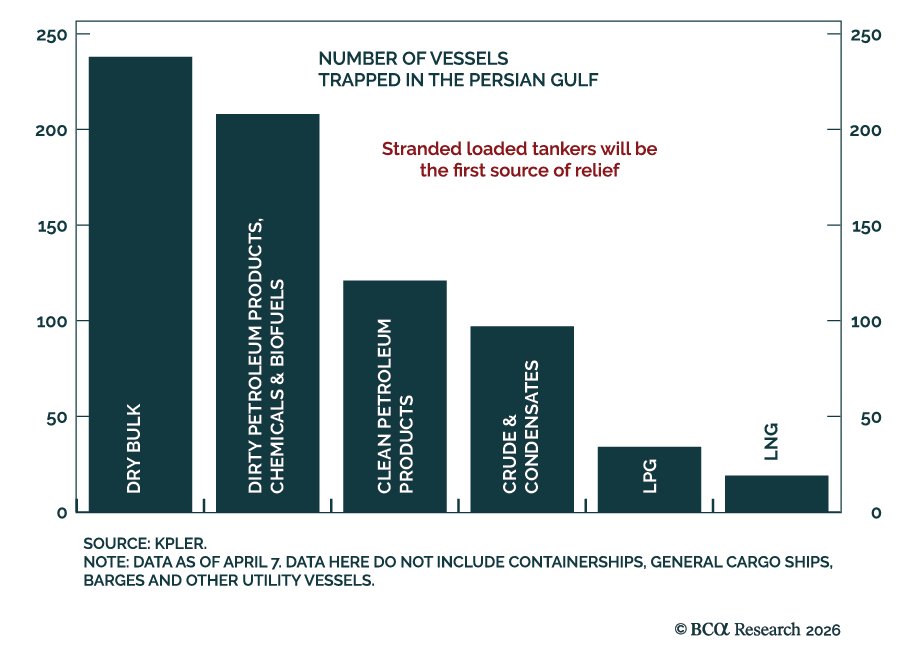

The reopening of the Strait of Hormuz shifts the focus from disruption to the pace of energy flow normalization. Our Chart Of The Week comes from Roukaya Ibrahim, Chief Commodity Strategist. Roukaya looks at how long it would take for energy markets to…

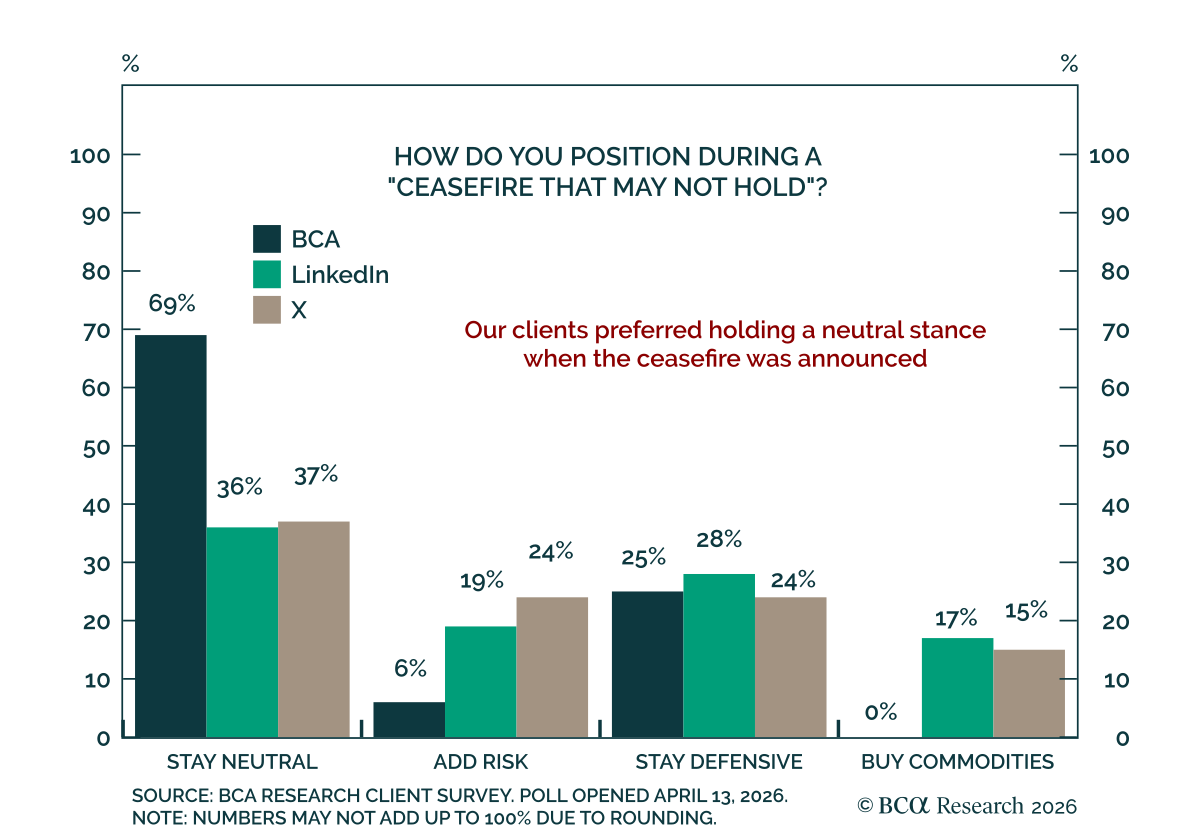

Our clients largely decided to maintain neutral positioning in the face of the initial US-Iran ceasefire. An overwhelming majority (69%) said they are staying neutral, compared with 25% staying defensive, 6% adding risk, and nobody adding commodities…

The Iran war is deescalating further — against our expectations — setting up an aggressive return to the risk-on rally.

The dollar’s pullback masks a quiet improvement in its cyclical backdrop, with growth, monetary policy, and flows turning in its favor. As markets fully price out geopolitical risk, the USD should decouple from oil and better reflect these gains, despite lingering structural headwinds.

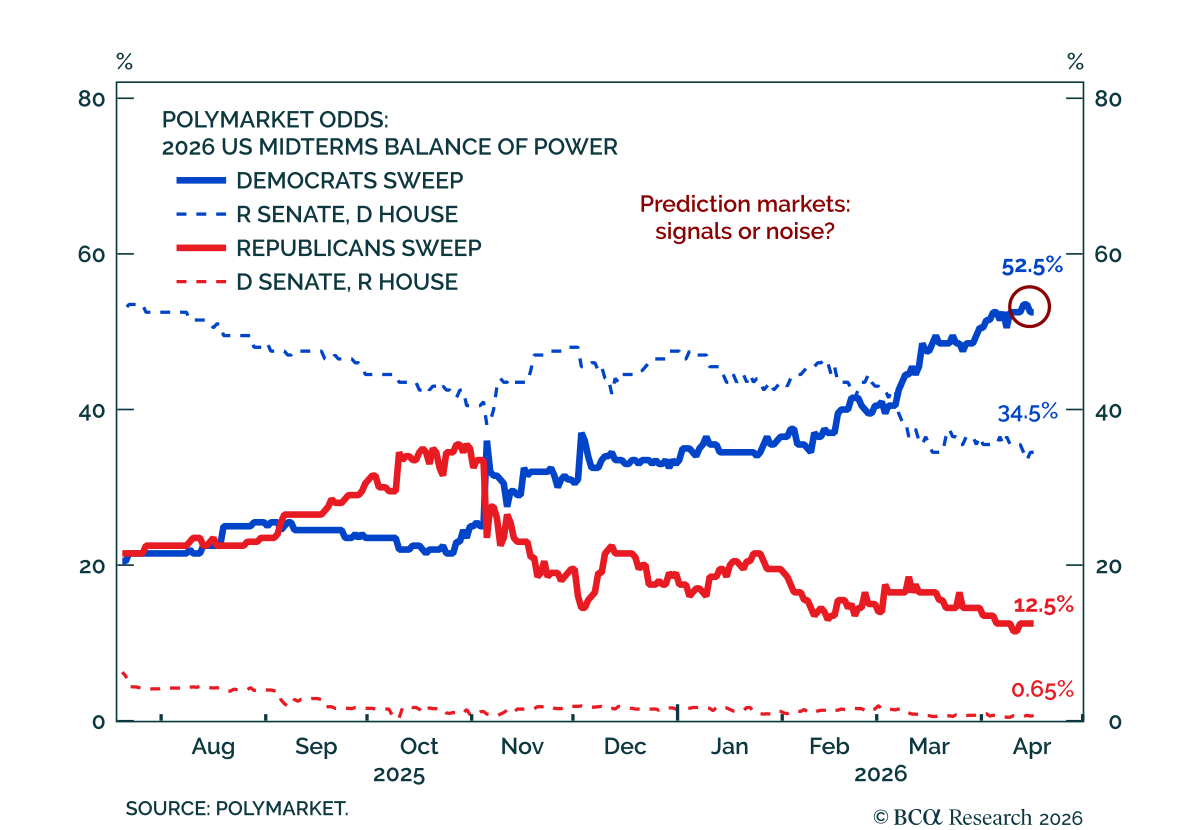

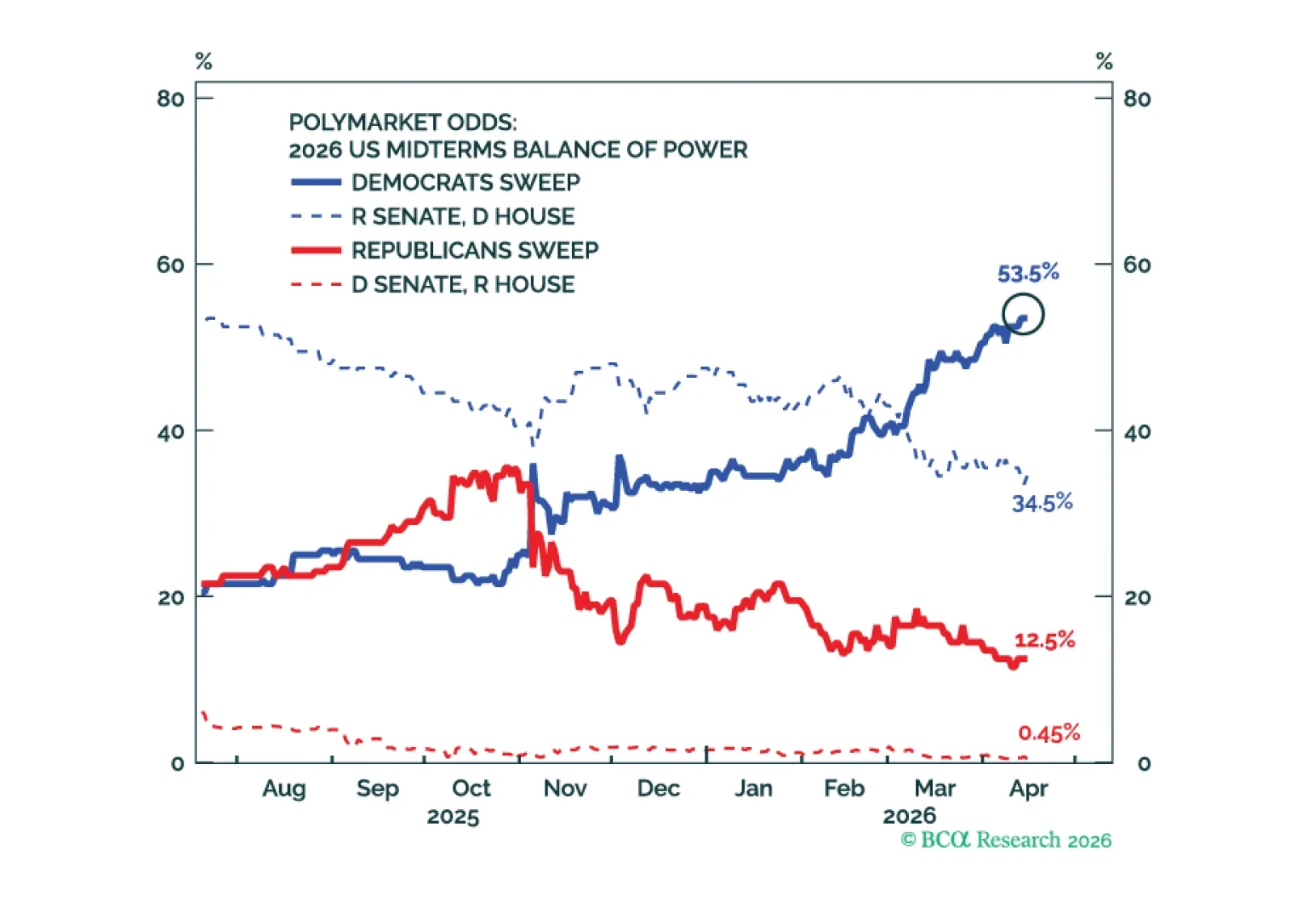

Our US Political strategists warn that markets may be underpricing a bifurcated political outcome. A prolonged Iran shock raises the odds of a Democratic Senate victory. The Hormuz-driven inflation spike has not yet fully transmitted to the broader economy.…

The April BCA Views discussion centered on whether markets have become too complacent about an Iran conflict that is not yet resolved. We held our monthly BCA Views meeting to assess the global economy and discuss our asset allocation views. The discussion…

Markets may be underpricing a bifurcated political outcome. Unless the Iran deescalation succeeds, the delayed economic fallout from the energy shock could materially worsen Republican prospects and raise the probability of a Democratic Senate victory.

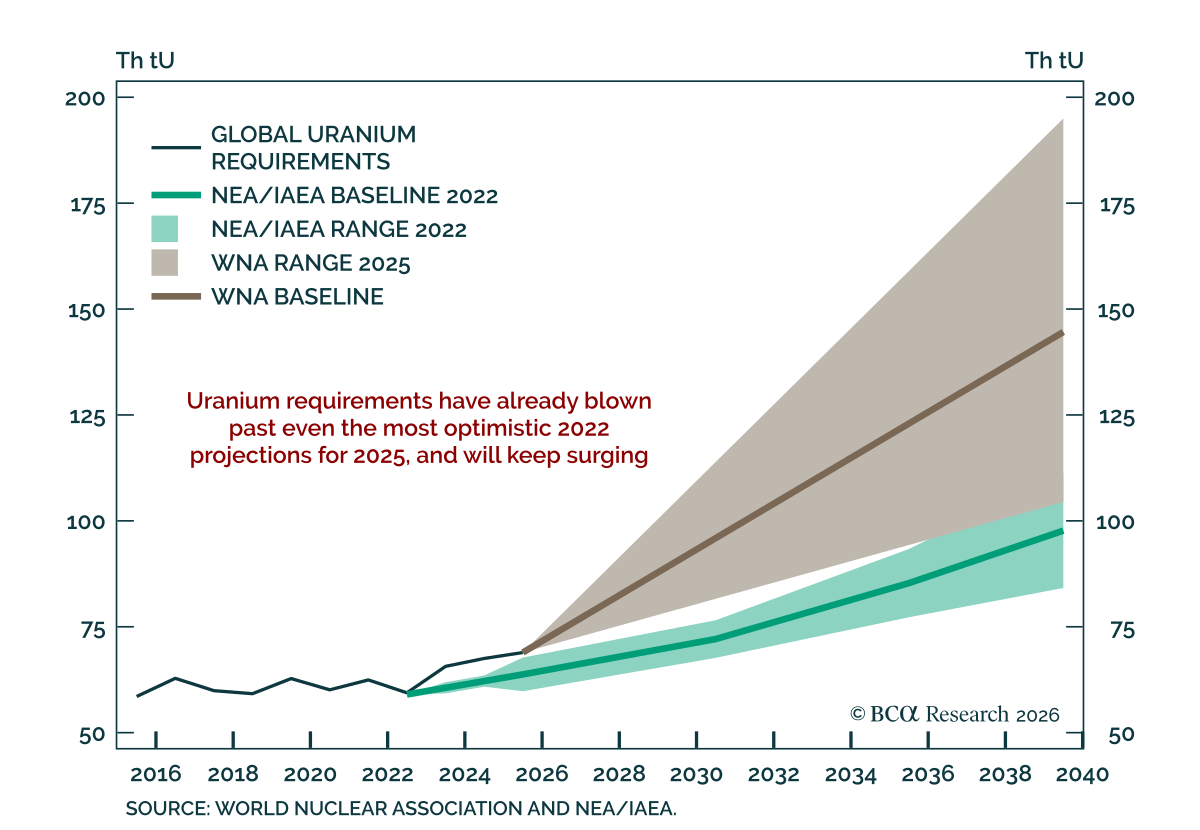

Our European and Commodity strategists maintain a bullish outlook on uranium, with structural supply and demand dynamics pointing to durable upside. Supply remains challenged despite some production growth, and the demand outlook has improved materially over…