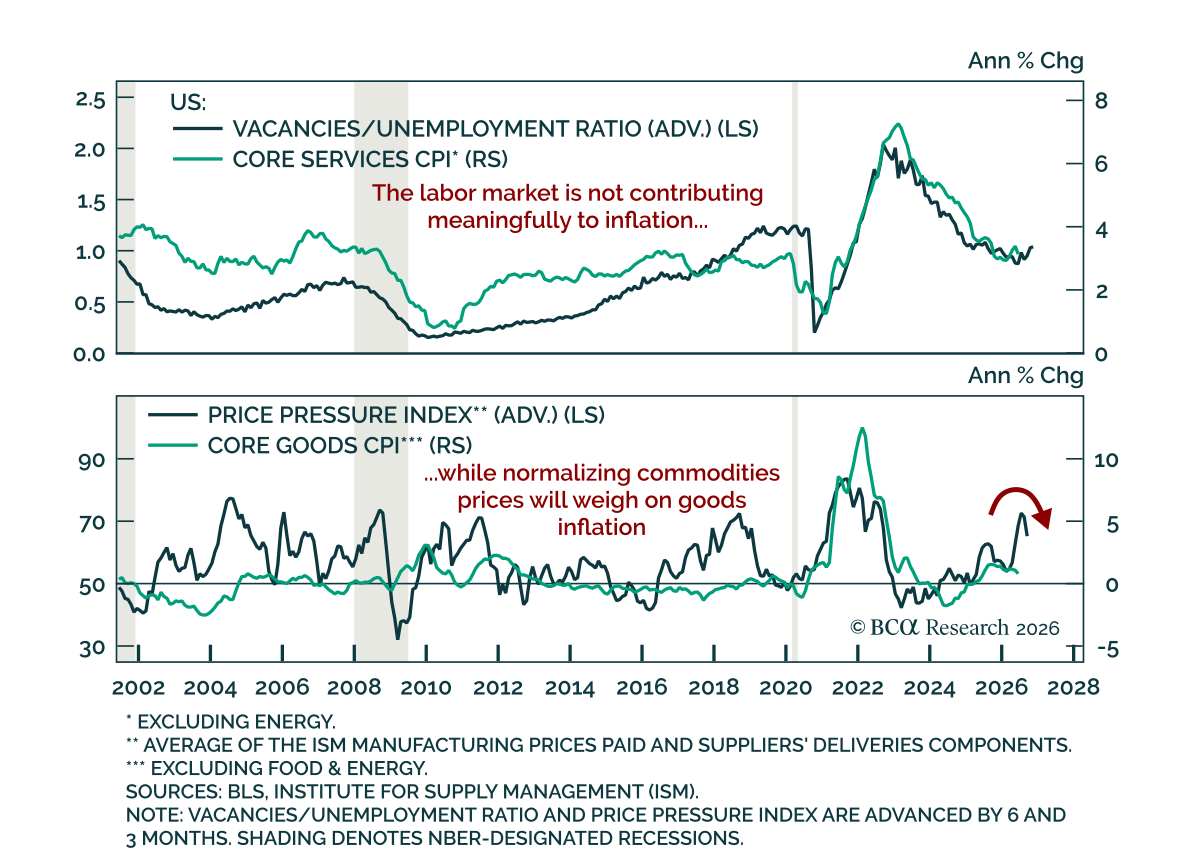

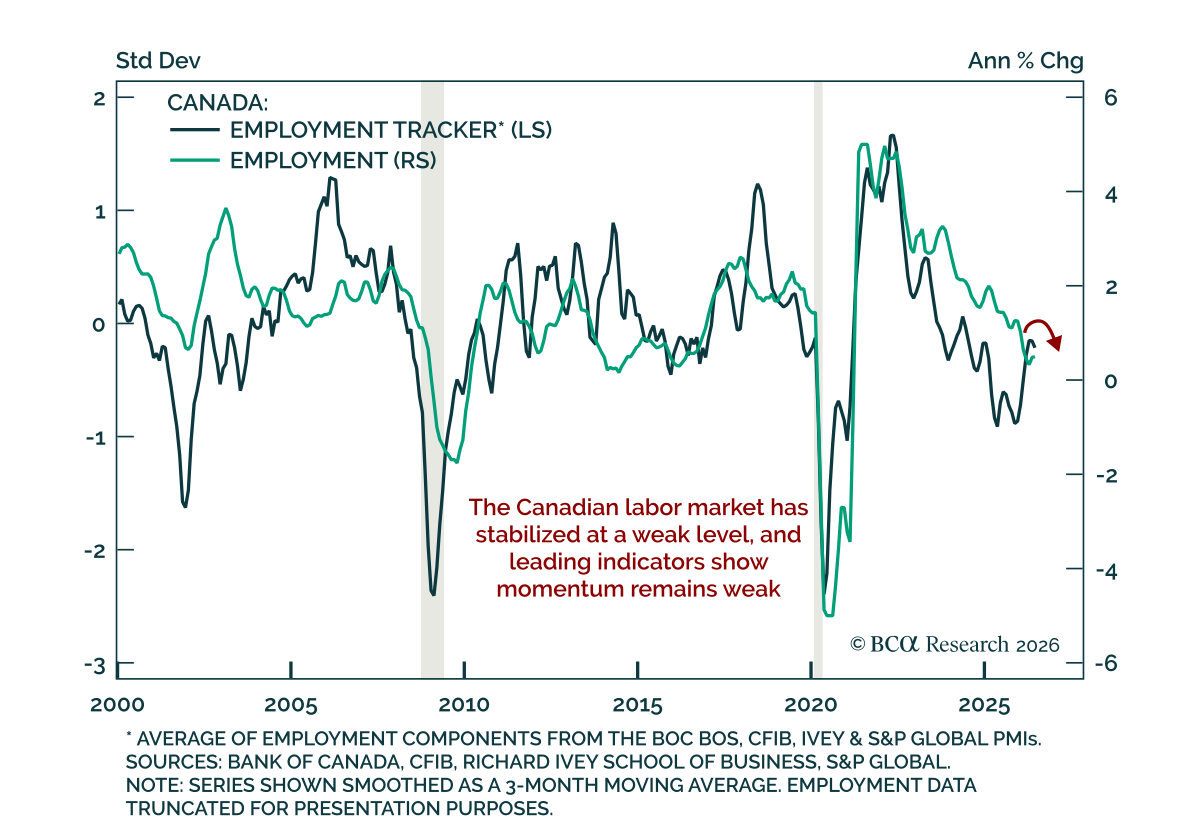

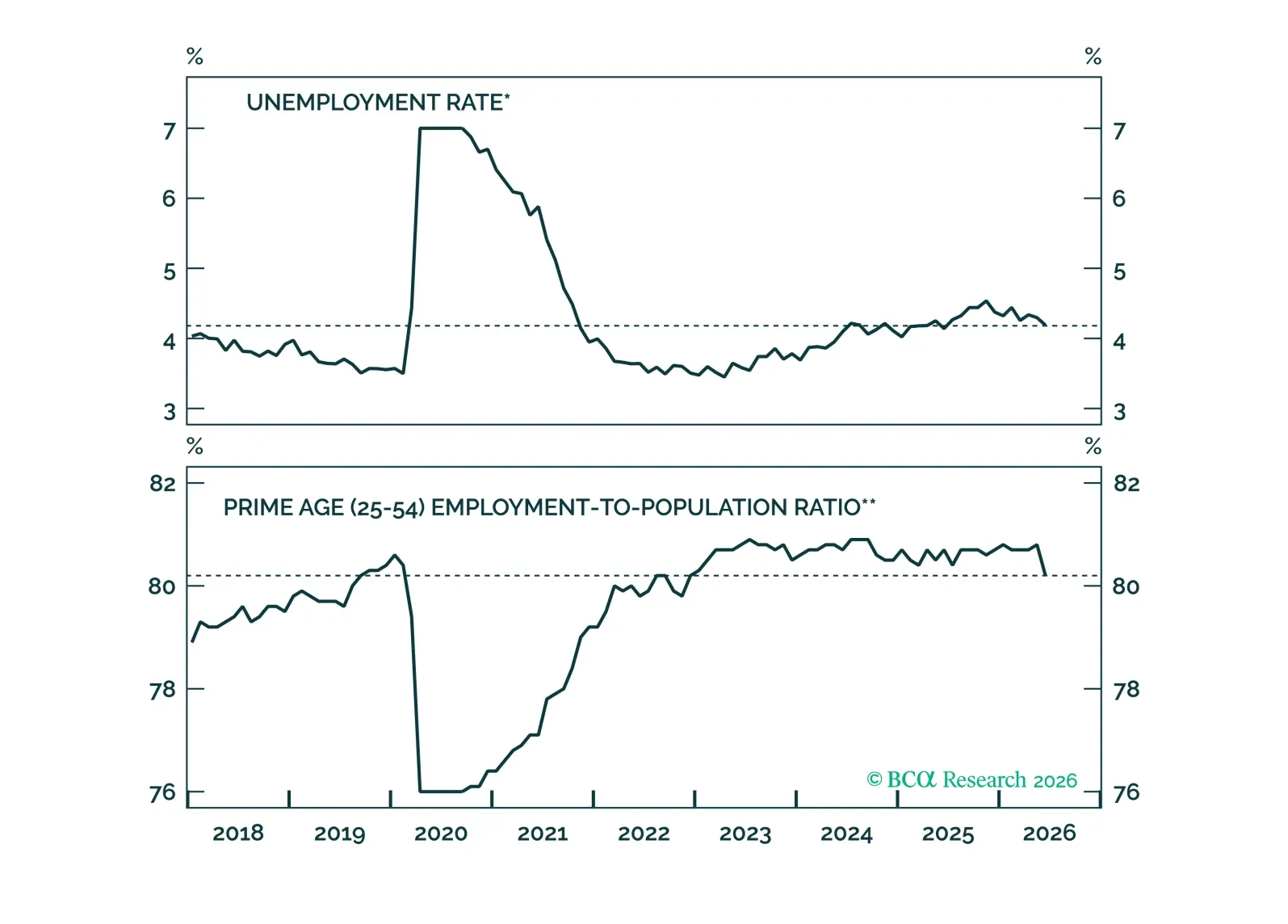

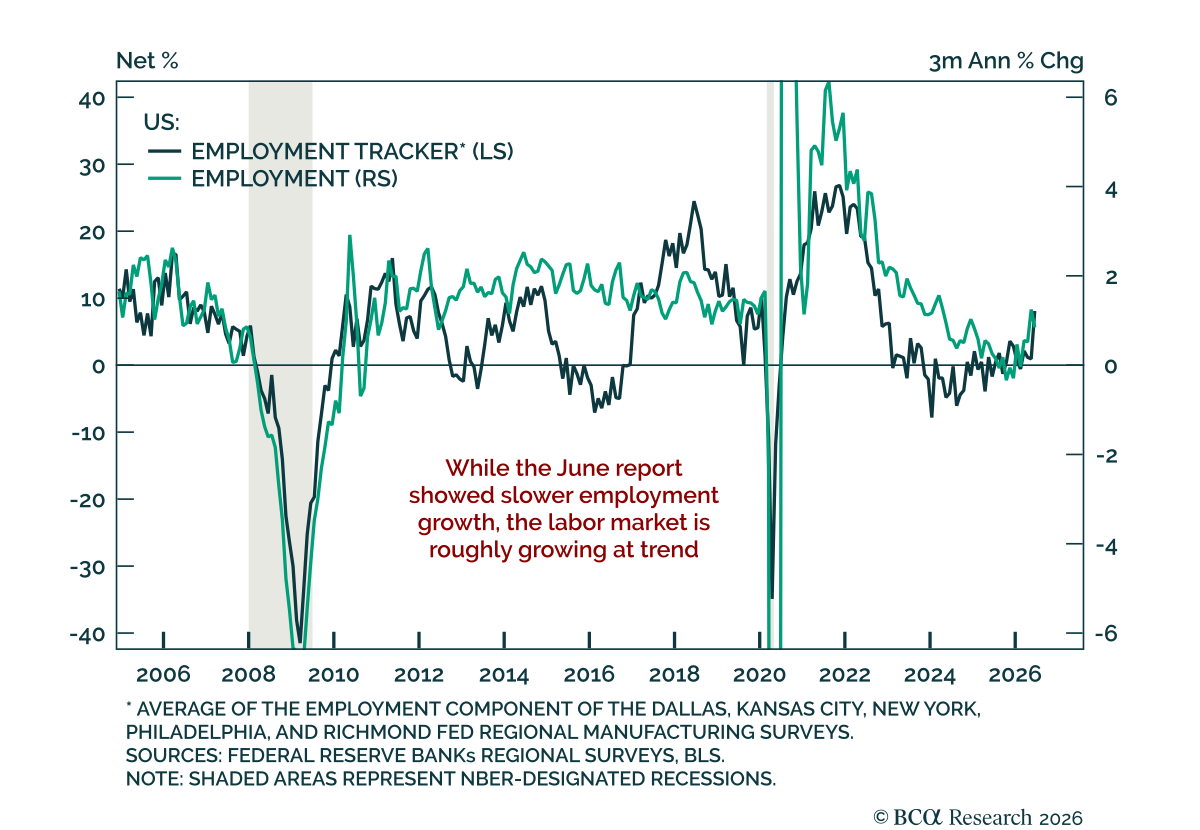

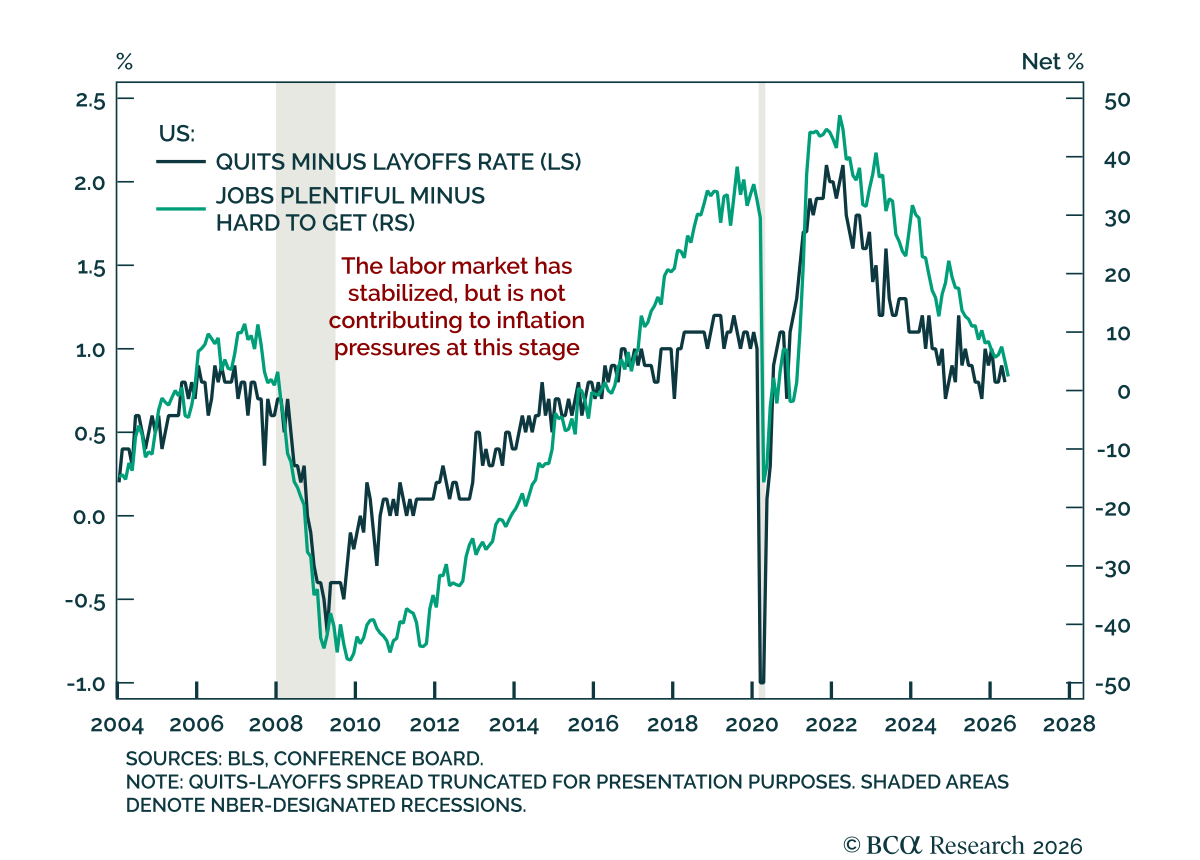

Labor Market

Most Fed and pundit assessments of inflation expectations are overly narrow, focusing too much on long-term market-based measures. We favor a more qualitative approach that asks whether the inflation outlook is influencing household and business decision making.

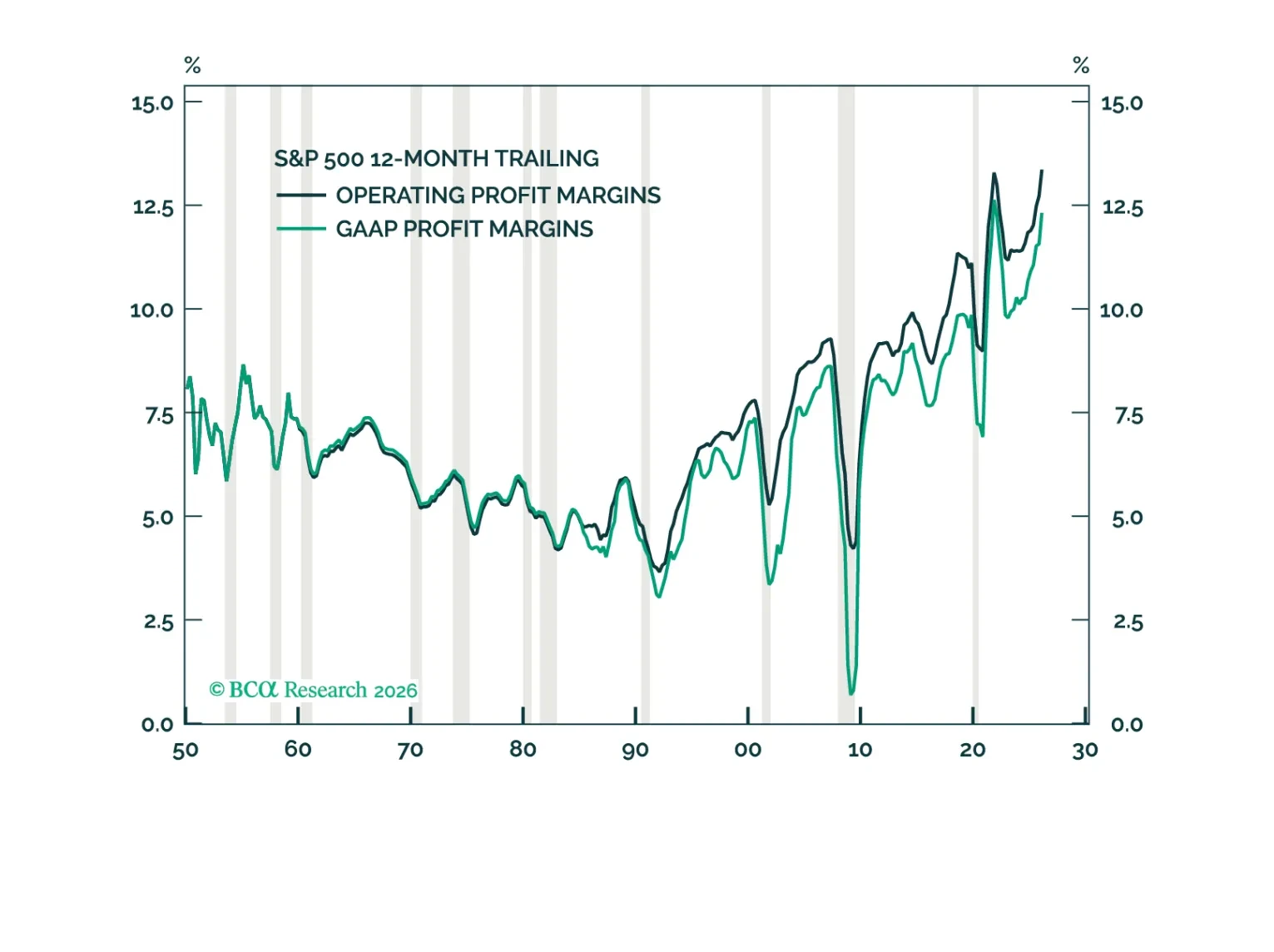

The Goldilocks environment for US profit margins should start to sour next year. Contrary to conventional wisdom, AI could end up eroding margins for both producers and consumers of artificial intelligence.

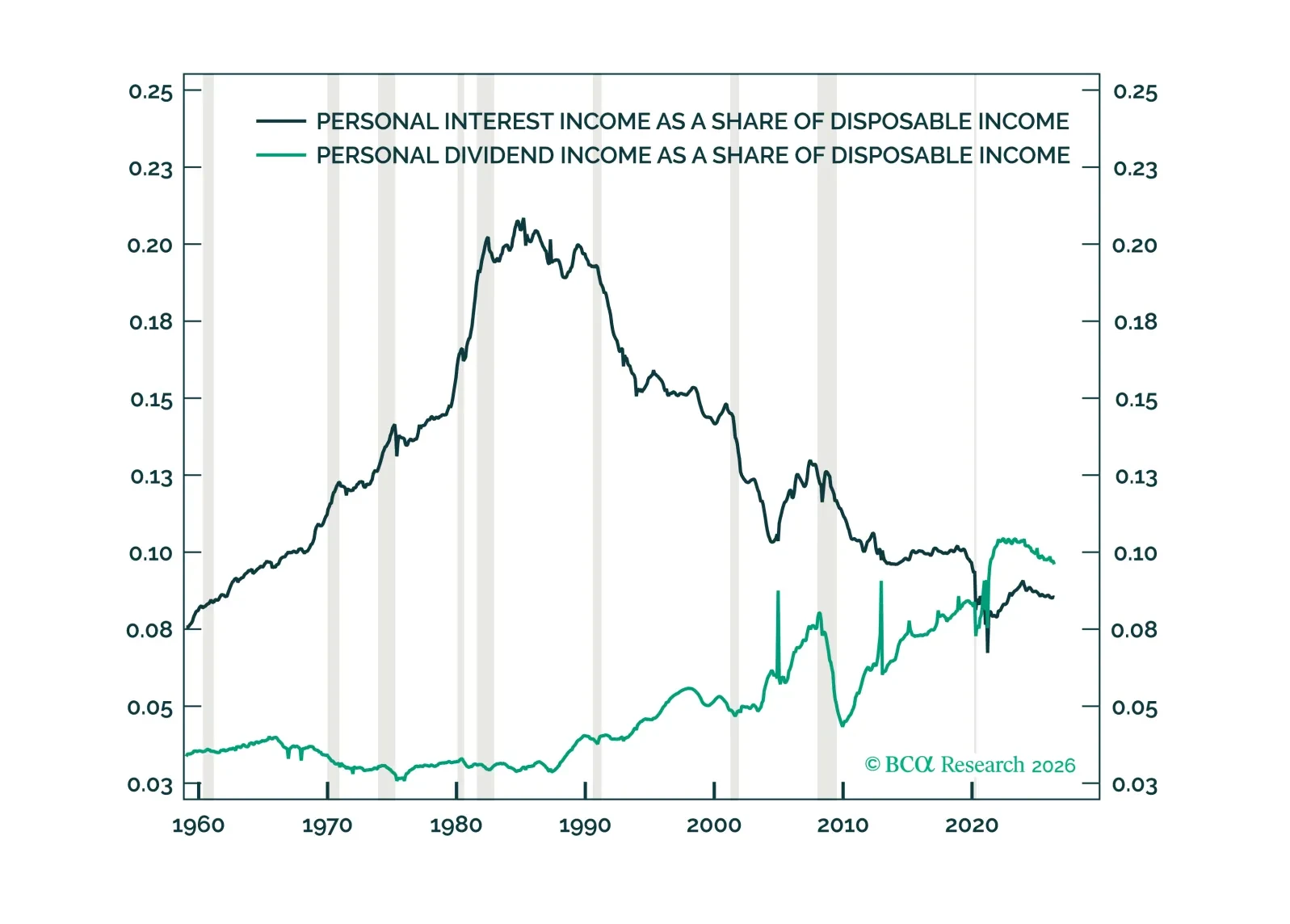

We are increasingly being asked if higher for longer interest rates could help spur consumption by boosting interest income. This report examines household income and balance sheet data to see if they might.

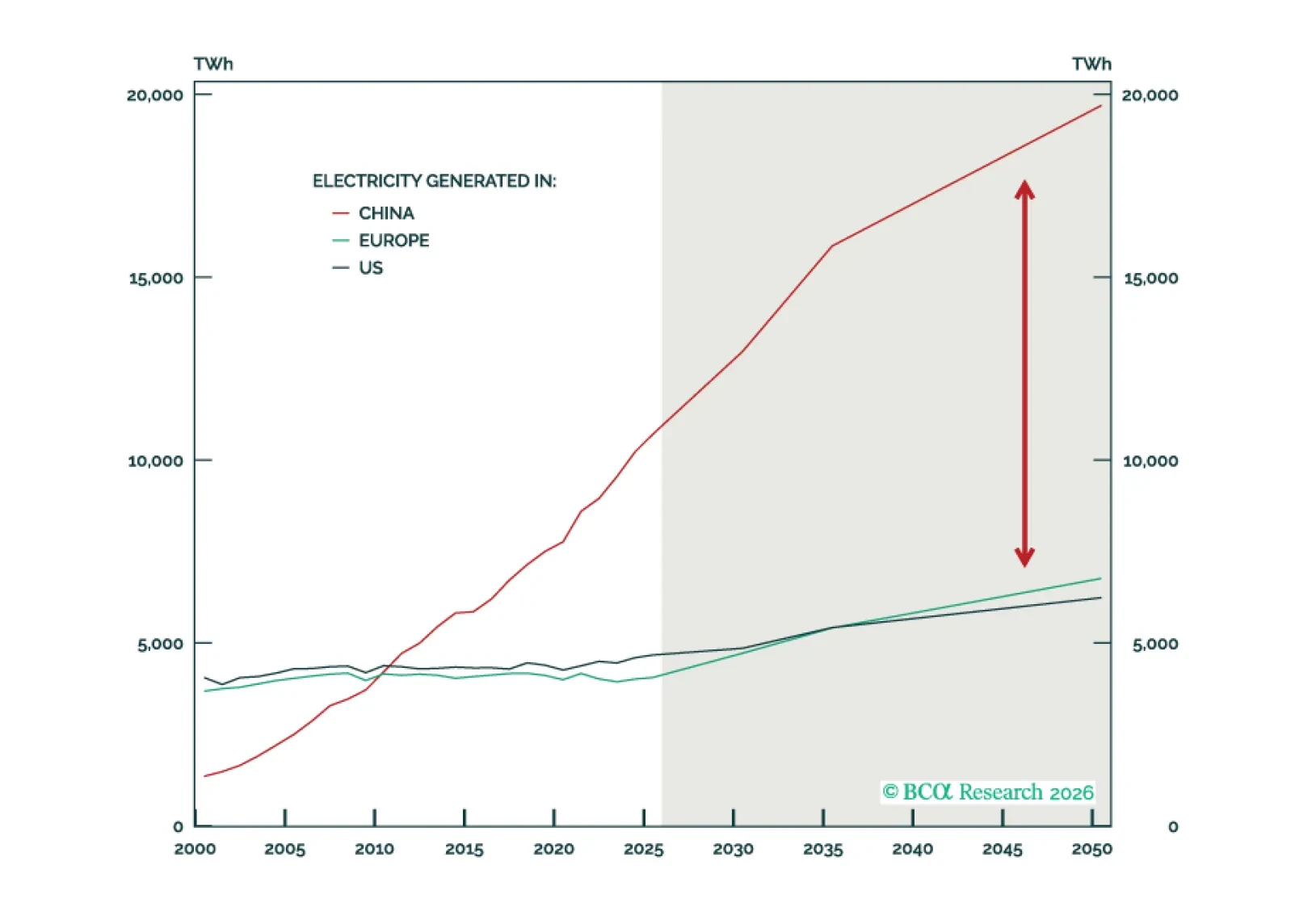

Section I maps how the broad distribution of wealth gains is supporting US consumption. Section II examines how countries can meet swelling electricity demand. The winners will find paths to build the infrastructure needed to power the high-tech future.

China holds a structural advantage in this "Age of Electricity" by operating the world's largest electricity system. However, this advantage has inherent limits, and the US remains competitive despite its challenges.