Labor Market

Highlights So What? Donald Trump's reelection depends on the timing of the next recession. Why? The midterm elections will not determine Trump's reelection chances. Rather, the timing of the next recession will. BCA's House View expects it by 2020. Otherwise, President Trump is favored to win. Trump may be downgrading "maximum pressure" on Iran, reducing the risk of a 2019 recession. Trade war with China, gridlock, and budget deficits are the most investment-relevant outcomes of U.S. politics in 2018-20. Feature The preliminary results of the U.S. midterm elections are in, with the Democrats gaining the House and failing to gain the Senate, as expected. Our view remains that the implications for investors are minimal. The policy status quo is now locked in - a gridlocked government is unlikely to produce a major change in economic policy over the next two years. While the election is to some extent a rebuke to Trump, this report argues that he remains the favored candidate for the 2020 presidential election - unless a recession occurs. A Preliminary Look At The Midterms First, the preliminary takeaways from the midterms, as the results come in: The Democrats took the House of Representatives, with a preliminary net gain of 27 seats, resulting in a 51%-plus majority, and this is projected to rise to 34 seats as we go to press Wednesday morning. This is above the average for midterm election gains by the opposition party, especially given that Republicans have held the advantage in electoral districting. Performance in the Midwest, other swing states, and suburban areas poses a threat to Trump and Republicans in 2020. Republicans held the Senate, with a net gain of at least two seats, for a 51%-plus majority. Democrats were defending 10 seats in states that Trump won in 2016. While Democrats did well in the Midwest, these candidates had the advantage of incumbency. On the state level, the Democrats gained a net seven governorships, two of them in key Midwestern states. The gubernatorial races were partly cyclical, as the Republicans had hit a historic high-water mark in governors' seats and were bound to fall back a bit. However, the Democratic victory in Michigan and Wisconsin, key Midwestern Trump states, is a very positive sign for the Democrats, since they were not incumbents in either state and had to unseat incumbent Governor Scott Walker in Wisconsin. (Their victory in Maine could also help them in the electoral college in 2020.) The governors' races also suggest that moderate Democrats are more appealing to voters than activist Democrats. Candidate Andrew Gillum's loss in Florida is a disappointment for the progressive wing of the Democratic Party.1 With the House alone, Democrats will not be able to push major legislation through. In the current partisan environment it will be nigh-impossible to reach the 60 votes needed to end debate in the Senate ("cloture"), and even then House Democrats will face a presidential veto. They will not be able to repeal Trump's tax cuts, re-regulate the economy, abandon the trade wars, resurrect Obamacare, or revive the 2015 Iranian nuclear deal. Like the Republicans after 2010, they will be trapped in the position of controlling only one half of one of the three constitutional branches. The most they can do is hold hearings and bring forth witnesses in an attempt to tarnish Trump's 2020 reelection chances. They may eventually bring impeachment articles against him, but without two-thirds of the Senate they cannot remove him from office (unless the GOP grassroots abandons him, giving senators permission to do so). U.S. equities generally move upward after midterm elections - including midterms that produce gridlock (Chart 1A & Chart 1B). However, the October selloff could drag into November. More worryingly, as Chart 1B shows, the post-election rally tends to peter out only six months after a gridlock midterm, unlike midterms that reinforce the ruling party. Chart 1AMidterm U.S. Elections Tend To Be Bullish...

Midterm U.S. Elections Tend To Be Bullish...

Midterm U.S. Elections Tend To Be Bullish...

Chart 1B... But Markets Lose Steam Six Months Post-Gridlock

... But Markets Lose Steam Six Months Post-Gridlock

... But Markets Lose Steam Six Months Post-Gridlock

However, the 2018 midterms could be mildly positive for the markets, as they do not portend any major new policies or uncertainty. Trump's proposed additional tax cuts would have threatened higher inflation and more Fed rate hikes, whereas House Democrats will not be able to raise taxes or cut spending alone. Bipartisan entitlement reform seems unlikely in 2018-20 given the acrimony of the two parties and structural factors such as inequality and populism. An outstanding question is health care, which Republicans left unresolved after failing to repeal Obamacare, and which exit polls show was a driving factor behind Democratic victories. Separately, as an additional marginal positive for risk assets, the Trump administration has reportedly granted eight waivers to countries that import Iranian oil. We have signaled that Trump's "maximum pressure" doctrine poses a key risk for markets due to the danger of an Iran-induced oil price shock. A shift toward more lax enforcement reduces the tail-risk of a recession in 2019 (Chart 2). Of course, the waivers will expire in 180 days and may be a mere ploy to ensure smooth markets ahead of the midterm election, so the jury is still out on this issue. Chart 2Rapid Increases In Oil Prices Tend To Precede Recessions

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

This brings us to the main focus of this report: what do the midterms suggest about the 2020 election? Bottom Line: The midterm elections have produced a gridlocked Congress. Trump can continue with his foreign policy, most of his trade policy, his deregulatory decrees, and his appointment of court judges with limited interference from House Democrats. The only thing the Democrats can prevent him from doing is cutting taxes further. He tends to agree with Democrats on the need for more spending! While the U.S. market could rally on the back of this result, we do not see U.S. politics being a critical catalyst for markets going forward. On balance, a gridlocked result brings less uncertainty than would otherwise be the case, which is positive for markets in the short term. The Midterms And The 2020 Election There is a weak relationship at best between an opposition party's gains in the midterms and its performance in the presidential election two years later. Given that the president's party almost always loses the midterms - and yet that incumbent presidents tend to be reelected - the midterm has little diagnostic value for the presidential vote, as can be seen in recent elections (Chart 3A & Chart 3B). Chart 3AMidterm Has Little Predictive Power For Presidential Popular Vote ...

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

Chart 3B... Nor For Presidential Electoral College Vote

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

Nevertheless, historian Allan Lichtman has shown that since 1860, a midterm loss is marginally negative for a president's reelection chances.2 And for Republicans in recent years, losses in midterm elections are very weakly correlated with Republican losses of seats in the electoral college two years later (Chart 4). Chart 4Republican Midterm Loss Could Foreshadow Electoral College Losses

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

Still, this midterm election does not give any reason to believe that Trump's reelection chances have been damaged any more than Ronald Reagan's were after 1982, or Bill Clinton's after 1994, or Barack Obama's after 2010. All three of these presidents went on to a second term. A midterm loss simply does not stack the odds against reelection. Why are midterm elections of limited consequence for the president? They are fundamentally different from presidential elections. For instance, "the buck stops here" applies to the president alone, whereas in the midterms voters often seek to keep the president in check by voting against his party in Congress.3 Despite the consensus media narrative, the president is not that unpopular. Trump's approval rating today is about the same as that of Clinton and Obama at this stage in their first term (Chart 5). This week's midterm was not a wave of "resistance" to Trump so much as a run-of-the-mill midterm in which the president's party lost seats. Its outcome should not be overstated. Bottom Line: There is not much correlation between midterms and presidential elections. The best historians view it as a marginal negative for the incumbent. This result is not a mortal wound for Trump. Chart 5President Trump Is Hardly Losing The Popularity Contest

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

2020: The Recession Call Is The Election Call The incumbent party has lost the White House every single time that a recession occurred during the campaign proper (Chart 6).4 The incumbent party has lost 50%-60% of the time if recession occurred in the calendar year before the election or in the first half of the election year. Chart 6A 2020 Recession Is Trump's Biggest Threat

A 2020 Recession Is Trump's Biggest Threat

A 2020 Recession Is Trump's Biggest Threat

This is a problem for President Trump because the current economic expansion is long in the tooth. In July 2019, it will become the longest running economic expansion in U.S. history, following the 1991-2001 expansion. The 2020 election will occur sixteen months after the record is broken, which means that averting a recession over this entire period will be remarkable. BCA's House View holds that 2020 is the most likely year for a recession to occur. The economy is at full employment, inflation is trending upwards, and the Fed's interest rate hikes will become restrictive sometime in 2019. The yield curve could invert in the second half of 2019 - and inversion tends to precede recession by anywhere from 5-to-16 months (Table 1). No wonder Trump has called the Fed his "biggest threat."5 Table 1Inverted Yield Curve Is An Ominous Sign

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

The risks to this 2020 recession call are probably skewed toward 2021 instead of 2019. The still-positive U.S. fiscal thrust in 2019 and possibly 2020 and the Trump administration's newly flexible approach to Iran sanctions, if maintained, reduce the tail-risk of a recession in 2019. If there is not a recession by 2020, Trump is the favored candidate to win. First, incumbents win 69% of all U.S. presidential elections. Second, incumbents win 80% of the time when the economy is not in recession, and 76% of the time when real annual per capita GDP growth over the course of the term exceeds the average of the previous two terms, which will likely be the case in 2020 unless there is a recession (Chart 7). Chart 7Relative Economic Performance Could Give Trump Firepower

Relative Economic Performance Could Give Trump Firepower

Relative Economic Performance Could Give Trump Firepower

The above probabilities are drawn from the aforementioned Professor Allan Lichtman, at American University in Washington D.C., who has accurately predicted the outcome of every presidential election since 1984 (except the disputed 2000 election). Lichtman views presidential elections as a referendum on the party that controls the White House. He presents "13 Keys to the Presidency," which are true or false statements based on historically derived indicators of presidential performance. If six or more of the 13 keys are false, the incumbent will lose. On our own reading of Lichtman's keys, Trump is currently lined up to lose a maximum of four keys - two shy of the six needed to unseat him (Table 2). This is a generous reading for the Democrats: Trump's party has lost seats in the midterm election relative to 2014; his term has seen sustained social unrest; he is tainted by major scandal; and he is lacking in charisma. Yet on a stricter reading Trump only has one key against him (the midterm). Table 2Lichtman's Thirteen Keys To The White House*

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

What would it take to push Trump over the edge? Aside from a recession (which would trigger one or both of the economic keys against him), he would need to see two-to-four of the following factors take shape: a serious foreign policy or military failure, a charismatic Democratic opponent in 2020, a significant challenge to his nomination within the Republican Party, or a robust third party candidacy emerge. In our view, none of these developments are on the horizon yet, though they are probable enough. For instance, it is easy to see Trump's audacious foreign policy on China, Iran, and North Korea leading to a failure that counts against him. Thus, as things currently stand, Trump is the candidate to beat as long as the economy holds up. What about impeachment and removal from office prior to 2020? As long as Trump remains popular among Republican voters he will prevent the Senate from turning against him (Chart 8). What could cause public opinion to change? Clear, irrefutable, accessible, "smoking gun" evidence of personal wrongdoing that affected Trump's campaigns or duties in office. Nixon was not brought down until the Watergate tapes became public - and that required a Supreme Court order. Only then did Republican opinion turn against him and expose him to impeachment and removal - prompting him to resign. Chart 8Trump Cannot Be Removed From Office

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

All that being said, Trump tends to trail his likeliest 2020 adversaries in one-on-one opinion polling. Given our recession call, we would not dispute online betting markets giving Trump a less-than-50% chance of reelection at present (Chart 9). The Democratic selection process has hardly begun: e.g. Joe Biden could have health problems, and Michelle Obama, Oprah Winfrey, or other surprise candidates could decide to run. The world will be a different place in 2020. Bottom Line: The recession call is the election call. If BCA is right about a recession by 2020, then Trump will lose. If we are wrong, then Trump is favored to win. Chart 9A Strong Opponent Has Yet To Emerge

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

Is It Even Possible For Trump To Win Again? Election Scenarios Is it demographically possible for Trump to win? Yes. In 2016 BCA dubbed Trump's electoral strategy "White Hype," based on his apparent attempt to increase the support and turnout of white voters, primarily in "Rust Belt" battleground states. While Republican policy wonks might have envisioned a "big tent" Republican Party for the future, demographic trends in 2016 suggested that this strategy was premature. Indeed, drawing from a major demographic study by the Center for American Progress and other Washington think tanks,6 we found that a big increase in white turnout and support was the only 2016 election scenario in which a victory in both the popular vote and electoral college vote was possible. In other words, while "Minority Outreach" have worked as a GOP strategy in the future, Donald Trump's team was mathematically correct in realizing that only White Hype would work in the actual election at hand. This strategy did not win Trump the popular vote, but it did secure him the requisite electoral college seats, notably from the formerly blue of Wisconsin, Michigan, and Pennsylvania. Comparing the 2016 results with our pre-election projections confirms this point: Trump won the very swing states where he increased white GOP support and lost the swing states where he did not. Pennsylvania is the notable exception, but he won there by increasing white turnout instead of white GOP support.7 Can Trump do this again? Yes, but not easily. Map 1 depicts the 2016 election results with red and blue states, plus the percentage swing in white party support that would have been necessary to turn the state to the opposite party (white support for the GOP is the independent variable). In Michigan, a 0.3% shift in the white vote away from Republicans would have deprived Trump of victory; in Wisconsin and Pennsylvania, a 0.8% shift would have done the same; in Florida, a 1.5% change would have done so. Map 1The 'White Hype' Strategy Narrowly Worked In 2016

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

Critically, the country's demographics have changed significantly since 2016 - to Trump's detriment. The white eligible voting population in swing states will have fallen sharply from 81% of the population to 76% of the population by 2020 (Chart 10). Chart 10Demographic Shift Does Not Favor Trump

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

Thus, to determine whether Trump still has a pathway to victory, we looked at eight scenarios, drawing on the updated Center for American Progress study. The assumptions behind the scenarios in Table 3 are as follows: Status Quo - This replicates the 2016 result and projects it forward with 2020 demographics. 2016 Sans Third Party - Replicates the 2016 result but normalizes the third party vote, which was elevated that year. Minority Revolt - In this scenario, Hispanics, Asians, and other minorities turn out in large numbers to support Democrats, even with white non-college educated voters supporting Republicans at a decent rate. The Kanye West Strategy - Trump performs a miracle and generates a swing of minority voters in favor of Republicans. Blue Collar Democrats - White non-college-educated support returns to 2012 norms, meaning back to Democrats. Romney's Ghost - White college-educated support returns to 2012 levels. White Hype - White non-college-educated support swings to Republicans. Obama versus Trump - White college-educated voters ally with minorities in opposition to a surge in white non-college-educated voters for Republicans. Table 3Assumptions For Key Electoral Scenarios In 2020

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

The results show that Trump's best chance at remaining in the White House is still White Hype, as it is still the only scenario in which Trump can statistically win a victory in the popular vote (Chart 11). Another pathway to victory is the "2016 Sans Third Party" scenario. But this scenario still calls for White Hype, since a third party challenger is out of his hands (Chart 12).8 Chart 11'White Hype' May Be Only Way To Secure Both Popular And Electoral College Vote...

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

Chart 12... Although Moving To The Center Could Still Yield Electoral College Vote

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

However, the data show that Trump cannot win merely by replicating his white turnout and support from 2016, due to demographic changes wiping away the thin margins in key swing states. He needs some additional increases in support. These increases will ultimately have to be culled from his record in office - which reinforces the all-important question of the timing of recession, but also raises the question of whether Trump will move to the center to woo the median voter. In the "Kanye West" and "Romney's Ghost" scenarios, Trump wins the electoral college by broadening his appeal to minorities and college-educated white voters. This may sound far-fetched, but President Clinton reinvented himself after the "Republican Revolution" of 1994 by compromising with Republicans in Congress. The slim margins in the Midwest suggest that the probability of Trump shifting to the middle is not as low as one might think. Especially if there is no recession. Independents remain the largest voting block - and they have not lost much steam, if any, since 2016. Moreover, the number of independents who lean Republican is in an uptrend (Chart 13). Without a recession, or a failure on Lichtman's keys, Trump will likely broaden his base. Chart 13Trump Shows Promise Among Independents

Trump Shows Promise Among Independents

Trump Shows Promise Among Independents

Bottom Line: Trump needs to increase white turnout and GOP support beyond 2016 levels in order to win 2020. Demographics will not allow a simple repeat of his 2016 performance. However, he may be able to generate the requisite turnout and support by moving to the center, courting college-educated whites and even minorities. His success will depend on his record in office. Investment Implications What are the implications of the above findings for 2018-20 and beyond? The Rust Belt states of Michigan, Pennsylvania, and Wisconsin will become pseudo-apocalyptic battlegrounds in 2020. The Democrats must aim to take back all three to win the White House, as they cannot win with just two alone.9 They are likely to focus on these states because they are erstwhile blue states and the vote margin is so slim that the slightest factors could shift the balance - meaning that Democrats could win here without a general pro-Democratic shift in opinion that hurts Trump in other key swing states such as Florida, North Carolina, or Arizona. The "Blue Collar Democrat" scenario, for instance, merely requires that white non-college-educated voters return to their 2012 level of support for Democrats. Joe Biden is the logical candidate, health permitting, as he is from Pennsylvania and was literally on the ballot in 2012! Moreover, these states are the easiest to flip to the Democratic side via the woman vote. In Michigan, a 0.5% swing of women to the Democrats would have turned the state blue again; in Pennsylvania that number is 1.6% and in Wisconsin it is 1.7% (Table 4). These are the lowest of any state. Women from the Midwest or with a base in the Midwest - such as Michelle Obama or Oprah Winfrey - would also be logical candidates. Table 4Women Voters May Hold The Balance

The 2020 U.S. Election: A "Way Too Soon" Forecast

The 2020 U.S. Election: A "Way Too Soon" Forecast

The Democrats could also pursue a separate or complementary strategy by courting African American turnout and support, especially in Florida, Georgia, and North Carolina. But it is more difficult to flip these states than the Midwestern ones. With the Rust Belt as the fulcrum of his electoral strategy and reelection, Trump has a major incentive to maintain economic nationalism over the coming two years. Trump may be more pragmatic in the use of tariffs, and will certainly engage in talks with China and others, but he ultimately must remain "tough" on trade. He has fewer constraints in pursuing trade war with China than with Europe. For the same Rust Belt reason, the Democrats, if they get into the Oval Office, will not be overly kind to the "butchers of Beijing," as President Clinton called the Chinese leadership in the 1992 presidential campaign (after the 1989 Tiananmen Square incident). Hence we are structurally bearish U.S.-China relations and related assets. Interestingly, if Trump moves to the middle, and tones down "white nationalism" in pursuit of college-educated whites and minorities, then he would have an incentive to dampen the flames of social division ahead of 2020. The key is that in an environment without recession, Trump has the option of courting voters on the basis of his economic and policy performance alone. Whereas if he is seen fanning social divisions, it could backfire, as Democrats could benefit from a sense of national crisis and instability in a presidential election. Either way, culture wars, controversial rhetoric, identity politics, unrest, and violence will continue in the United States as the fringes of the political spectrum use identity politics and wedge issues to rile up voters.The question is how the leading parties and their candidates handle it. What about after 2020? Are there any conclusions that can be drawn regardless of which party controls the White House? The two biggest policy certainties are that fiscal spending will go up and that generational conflict will rise. On fiscal spending, Trump was a game changer by removing fiscal hawkishness from the Republican agenda. Democrats are not proposing fiscal responsibility either. The most likely areas of bipartisan legislation in 2018-20 are health care and infrastructure - returning House Speaker Nancy Pelosi mentioned infrastructure several times in her election-night speech - which would add to the deficit. The deficit is already set to widen sharply, judging by the fact that it has been widening at a time when unemployment is falling. This aberration has only occurred during the economic boom of the 1950s and the inflation and subsequent stagflation beginning in the late 1960s (Chart 14). The current outlook implies a return of the stagflationary scenario. In the late 1960s, the World War I generation was retiring, lifting the dependent-to-worker ratio and increasing consumption relative to savings. Today, as Peter Berezin of BCA's Global Investment Strategy has shown, the Baby Boomers are retiring with a similar impact. Chart 14The Deficit Is Blowing Out Even Without A Recession

The Deficit Is Blowing Out Even Without A Recession

The Deficit Is Blowing Out Even Without A Recession

Trump made an appeal to elderly voters in the midterms by warning that unfettered immigration and Democratic entitlement expansions would take away from existing senior benefits. By contrast, Democrats will argue that Republicans want to cut benefits for all to pay for tax cuts for the rich, and will try to activate Millennial voters on a range of progressive issues that antagonize older voters. The result is that policy debates will focus more on generational differences. Mammoth budget deficits - not to mention trade war - will be good for inflation, good for gold, and a headwind for U.S. government bonds and the USD as long as the environment is not recessionary. The greatest policy uncertainties are health care and immigration. These are the two major outstanding policy issues that Republicans and Democrats will vie over in 2018 and beyond. While President Trump could achieve something with the Democrats on either of these issues with some painful compromises, it is too soon to have a high conviction on the outcome. But assuming that over the coming years some immigration restrictions come into play and that some kind of public health care option becomes more widely available, there are two more reasons to expect inflation to trend upward on a secular basis. Also on a secular basis, defense stocks stand to benefit from geopolitical multipolarity, especially U.S.-China antagonism. Tech stocks stand to suffer due to the trade war and an increasingly bipartisan consensus that this sector needs to be regulated. Matt Gertken, Vice President Geopolitical Strategy mattg@bcaresearch.com Marko Papic, Senior Vice President Chief Geopolitical Strategist marko@bcaresearch.com 1 Furthermore, victories on the state level, if built upon in the 2020 election, could give the Democrats an advantage in gerrymandering, i.e. electoral redistricting, which is an important political process in the United States. 2 Please see Allan J. Lichtman, Predicting The Next President: The Keys To The White House 2016 (New York: Rowman and Littlefield, 2016). 3 Please see Joseph Bafumi, Robert S. Erikson, and Christopher Wlezien, "Balancing, Generic Polls and Midterm Congressional Elections," The Journal of Politics 72:3 (2010), pp. 705-19. 4 Please see footnote 2 above. 5 Please see Sylvan Lane, “Trump says Fed is his ‘biggest threat,’ blasting own appointees,” The Hill, October 16, 2018, available at thehill.com. 6 Please see Rob Griffin, Ruy Teixeira, and William H. Frey, "America's Electoral Future: Demographic Shifts and the Future of the Trump Coalition," Center for American Progress, dated April 14, 2018, available at www.americanprogress.org. 7 In several cases, he did not have to lift white support by as much as we projected because minority support for the Democrats dropped off after Obama left the stage. 8 Interestingly, however, this scenario would result in an electoral college tie! Since the House would then vote on a state delegation basis, it would likely hand Trump the victory (and Pence would also win the Senate). 9 However, if they win Pennsylvania plus one electoral vote in Maine, they can win the electoral college with either Michigan or Wisconsin.

Highlights The End Of APP?: Economic growth in the euro area has lost momentum, but it is not clear that an extended period of below-trend growth is unfolding. With most measures of spare capacity showing a lack of it, the ECB must still move forward with its plans to begin removing policy accommodation. Policy Choices: If the ECB downgrades its growth and inflation forecasts next month, delaying the end of the APP into 2019 is unlikely, as is altering the country weightings within the APP portfolio. More plausible options include pushing out forward guidance on future rate hikes, extending the maturity of the existing bond holdings, or introducing a new TLTRO to support lending. Impact On European Bonds & The Euro: The ECB is most likely to take a less hawkish slant in December, but will not signal any rapid move to begin hiking rates. This outcome will be bearish for the euro, but only neutral at best for overvalued European government bonds. Feature For the European Central Bank (ECB), the countdown is on to the December policy meeting, when a final decision will have to be made on the end of the Asset Purchase Program (APP). The central bank has been signaling throughout 2018 that net new APP bond purchases will stop at the end of the year, with a potential interest rate increase coming in September 2019 at the earliest. That decision on APP, however, will be conditional on the ECB remaining confident in its forecast that inflation will sustainably return to the target of "just below" 2%. Slumping European economic growth in 2018 means that the ECB's forecasts may prove to be too optimistic. This is especially true given the risks to growth and financial stability stemming from Italy's fiscal policy debate with the European Union, softening Chinese demand for European exports, and the uncertainties related to U.S. trade protectionism and the final U.K.-E.U. Brexit deal. Some pundits are even suggesting that the ECB may be forced to extend the APP program beyond December - or look for other ways to prevent a tightening of monetary conditions - even with headline inflation and wage growth having picked up across most countries. Against this increasingly muddled backdrop, what can the ECB credibly announce in December? In this Special Report, jointly published by BCA's Global Fixed Income Strategy and Foreign Exchange Strategy services, we discuss the state of the euro area economy and then consider the ECB's next potential policy moves, with ramifications for European bond yields and the euro. Our conclusion is that there are a few policy tools available to the ECB in case of a prolonged slump in growth, without having to bring on the operational difficulties from extending the APP beyond December. Such a "dovish" shift would be bearish for the euro but neutral, at best, for European government bonds which remain deeply overvalued. ECB Policy Dilemma: Slowing Growth Vs. Accelerating Inflation At last month's monetary policy meeting, ECB President Mario Draghi noted that the slowing economy was merely returning to trend (or potential) growth from an unsustainably fast pace in 2017 that was fueled by strong export demand. Looking at the broad swath of euro area economic data, Draghi's relatively optimistic assessment is not far off the mark. The euro zone has seen a clear loss of economic growth momentum since the start of the year (Chart 1). The initial read on real GDP for the third quarter, released last week, showed a deceleration to a below-potential quarterly growth pace of 1.7%. The manufacturing purchasing managers index (PMI) has fallen from a peak of 61 in December 2017 to 52 in October, mirroring a -1% decline in the OECD's leading economic indicator for the region. Chart 1A European Growth Slump, Not Yet A Downtrend

A European Growth Slump, Not Yet A Downtrend

A European Growth Slump, Not Yet A Downtrend

Yet not all the economic news has been that weak. Both consumer and business confidence remain at elevated levels according to the European Commission (EC) surveys, consistent with above-trend real GDP growth (bottom two panels). Even though exports have weakened substantially from the booming pace in 2017 - largely due to China's slowing growth - the EC survey on firms' export order books remains at robust levels and overall export growth has rebounded of late (Chart 2). The current conditions component of the euro area ZEW index has also ticked higher (top panel), as has the bank credit impulse (bottom panel). Chart 2Not All The Economic News Is Bad

Not All The Economic News Is Bad

Not All The Economic News Is Bad

The bigger issue for the ECB is that the recent cooling of growth comes at a time when, by almost all measures, there is little economic slack in the euro area. Capacity utilization is running at an 11-year high of 84%, while the output gap is effectively closed according to estimates from the IMF (Chart 3). Chart 3No Spare Capacity In Europe

No Spare Capacity In Europe

No Spare Capacity In Europe

With that gap projected to turn positive in 2019, core inflation in the euro zone should be expected to drift higher. Yet core inflation now remains stuck around 1%, well below the headline inflation figure of 2% that has been heavily influenced by past increases in energy prices (bottom panel). The labor market is sending signals that the current period of low euro area inflation may be turning around. The unemployment rate for the entire region fell to a 10-year low of 8.1% in September, well below both the ECB's latest 2018 forecast and the OECD's estimate of the full employment NAIRU (Chart 4). This tightening labor market is a broad-based phenomenon across the euro area, with nearly 80% of countries in the region having an unemployment rate below NAIRU (middle panel).1 The last two times there was such a broad-based decline in unemployment in the region, in 2001-02 and 2006-07, a significant tightening of monetary policy was required as measured by a simple Taylor Rule. Chart 4Broad-Based Labor Market Strength

Broad-Based Labor Market Strength

Broad-Based Labor Market Strength

Already, the tightening labor market is starting to put upward pressure on labor costs. The annual growth in wages & salaries accelerated to just over 2% in the second quarter of 2018. Similar to the fall in unemployment rates, the faster wage growth has also been widely seen throughout the region, with nearly three-quarters of euro area countries showing faster wage growth from one year ago (bottom panel). The mix of slowing growth momentum with some inflationary pressures can be seen in our ECB Monitor, which measures the cyclical pressures to tighten or ease monetary policy in the euro area. The Monitor had been signaling a need for tighter policy for most of the past two years, but has now fallen back to levels consistent with no change in policy (Chart 5). When breaking down the Monitor into its inflation and growth components, the latter has fallen the most. The inflation components remain in the "tight money required" zone above the zero line. Chart 5Our ECB Monitor Says 'Do Nothing'

Our ECB Monitor Says 'Do Nothing'

Our ECB Monitor Says 'Do Nothing'

Looking across the balance of the euro area data, President Draghi's assessment that the recent economic weakness is not the beginning of a sustained move to below-trend growth is justified. Given the broad evidence pointing to a lack of excess capacity across the euro area economy, it will take a much bigger growth slump before the ECB can shift to a more dovish policy bias. The critical series to monitor will be business confidence, capital spending and export orders. All are at risk of downshifting due to slowing global trade activity and sluggish Chinese demand. BCA's China experts continue to have doubts that the Chinese government will undertake any typical initiatives to stimulate demand, like interest rate cuts or fiscal spending, given worries about high domestic debt levels. Without the impetus from strong Chinese import demand boosting euro area exports, the current tightness of euro area labor markets, and uptrend in wage growth, may be at risk of a reversal, as we discussed in a recent Special Report.2 Bottom Line: Economic growth in the euro area has lost momentum, but it is not clear that an extended period of below-trend growth is unfolding. With most measures of spare capacity showing a lack of it, the ECB must still move forward with its plans to begin removing policy accommodation. What Tools Are Available For The ECB? Net-net, when looking at the broad balance of growth and inflation data at the moment, there is not yet enough evidence to suggest that the ECB needs to back away from its current plans to end net new APP purchases in December. That does not mean that the ECB would not consider changes to its total mix of monetary policy measures. The ECB has treated the APP, which began in 2015, as a "deflation fighting tool" during a period when there was excess capacity and very low inflation in the euro area. That is no longer the case, so it will be difficult for the ECB Governing Council to argue in December that new APP purchases are still necessary. It would take a substantial downward adjustment to the ECB growth and inflation forecasts, with a subsequent upward revision to the expectations for the unemployment rate, for the ECB to reconsider the plans to stop new bond purchases at year-end. Yet the ECB has also made it clear that interest rate hikes will not happen soon after the APP purchases end. Going back over the entire 20-year history of the ECB, there have only been three tightening episodes through rate hikes: 1999-2000, 2003-07 and 2011. In all three cases, what prompted the rate hikes was a period of broad-based increases in euro zone inflation that followed a period of equally broad-based euro zone economic growth. This can be seen in Chart 6, which shows "diffusion indices", or breadth across countries, for euro area real GDP and inflation. A higher number means that a greater percentage of individual nations is experiencing faster growth or inflation, and vice versa. During those three previous tightening cycles, the diffusion indices all reached elevated levels for growth and, more importantly, inflation. With more countries enjoying the upturn, the ECB could be more confident in seeing the need for interest rate increases to cool off demand to prevent an inflation overshoot. Chart 6No Need For ECB Rate Hikes Anytime Soon

No Need For ECB Rate Hikes Anytime Soon

No Need For ECB Rate Hikes Anytime Soon

At the moment, the diffusion indices are quite low, suggesting that few countries are witnessing accelerating growth or inflation. This means that there is no pressure for the ECB to move up its current dovish guidance to the markets about the timing of the first rate hike in late 2019. That also means that there is a risk that the ECB is forced to consider options for providing additional monetary accommodation if there was a large enough downgrade to its growth and inflation forecasts. If the ECB were to indeed lower its growth forecasts in December and consider additional easing options, there are only four plausible options at their disposal: 1) Extending the APP purchases beyond December, either at the current pace of €15bn/month or a slower pace between €5-10bn/month Extending the APP into 2019 is the least likely choice because the ECB is already close to some of the self-imposed constraints on its government bond holdings. The ECB has set a limit of owning no more than 33% of an individual country's allowable government bonds, with maturities of between 1-31 years. Right now, the ECB owns about 31% of all eligible German government debt (Chart 7), and would breach that 33% level sometime in the first half of 2019 if the current pace of buying was maintained without any increase in German bond issuance (i.e. smaller budget surpluses).3 A similar outcome would also occur for smaller bond markets, like the Netherlands and Finland (bottom panel). Chart 7ECB Will Hit Country Issuer Limits If Current APP Is Maintained

ECB Will Hit Country Issuer Limits If Current APP Is Maintained

ECB Will Hit Country Issuer Limits If Current APP Is Maintained

Of course, this is a self-imposed rule by the ECB that can easily be changed. That already occurred back in 2016 when the ECB allowed the purchase of bonds below the deposit rate as part of its APP operations. This meant that the ECB would buy bonds with negative yields, essentially guaranteeing a loss assuming that the bonds were held to maturity. Yet given how much emphasis the ECB has placed on abiding by the issuer limits, we think the ECB would consider other policy choices before raising them. 2) Changing the composition of the APP portfolio Changing the mix of bonds within the APP portfolio is a more likely option, but even this has its limits. The ECB could choose to buy more corporate bonds or covered bonds, but those are less liquid markets where there is arguably more evidence that ECB buying has impacted market functionality. The ECB may be reluctant to take on more credit risk in its bond portfolio, as well. At the country level, the ECB could choose to move away from using its Capital Key weightings to determine the allocation of its bond purchases by country. In the current heated political atmosphere in Europe, however, with the populist Italian government in a very public battle with the E.U. over its 2019 budget, the ECB will not want to be seen as favoring any country more than another by buying more government bonds in places like Italy or Spain over Germany and France. That can already be seen in how bond purchases have been allocated in 2018, with purchases sticking closer to the Capital Key weightings in Italy and France from the larger weightings seen in 2017 (Charts 8 & 9). Chart 8The ECB Capital Key ...

The ECB Capital Key...

The ECB Capital Key...

Chart 9... Is Not Always Adhered To

...Is Not Always Adhered Too

...Is Not Always Adhered Too

A more likely reallocation of bond holdings could occur within each country by adjusting the maturities held within the ECB's portfolio. Following the template of the Fed's 2012 "Operation Twist", the ECB could aim to sell shorter-dated bonds in exchange for longer-maturity debt, thereby exacting a flattening influence on government yield curves. There is scope for that in Germany, where the weighted-average-maturity (WAM) of the ECB's bond holdings has decline by 18 months since peaking in late 2015 (Chart 10). Large declines in WAW have also occurred for Spanish, Italian and Portuguese bonds owned by the ECB, if policymakers were willing to take on more duration risk in the Periphery. Chart 10The ECB Has Room To Extend Its APP Maturities

The ECB Has Room To Extend Its APP Maturities

The ECB Has Room To Extend Its APP Maturities

3) Extend forward guidance on the first rate hike The easiest option for the ECB in the event of a downgrade of its growth/inflation projections is to simply extend the forward guidance on the timing of the first interest rate hike. Right now, our Months-to-Hike indicators, which measure the time until a full rate hike is discounted in the European Overnight Index Swap (OIS) curve, are discounting a hike of 10bps by November 2019 and a hike of 25bps by May 2020 (Chart 11). The ECB could easily signal that any rate hike, of any size, would not occur before the latter half of 2020 if an additional easing move was required. This would mostly likely result in lower bond yields and a weaker euro, all else equal, helping easy monetary conditions in the euro area. Chart 11Extending Forward Guidance Is An Option

Extending Forward Guidance Is An Option

Extending Forward Guidance Is An Option

4) Introduce a new Targeted Long-Term Lending Operation (TLTRO) One final intriguing option for an ECB policy ease would be the introduction of another TLTRO. The last such targeted lending program occurred in 2016, but the first wave of the much larger program that began in 2014 has already started to run off the ECB's balance sheet. This is the most effective way to get European banks to extend credit to borrowers at lower interest rates, since the banks would be able to fund that borrowing via the TLTRO at a rate lower than market rates. President Draghi did note last month that some members of the Governing Council brought up the idea of a new TLTRO at the ECB's policy meeting, and some well-known investment banks have recently discussed the implications of a new operation. In our view, a new TLTRO is the most effective way for the ECB to provide stimulus via lower private borrowing rates. It would also help offset any negative ramifications of the reduction of the ECB's balance sheet from the expiration of prior TLTROs. This would likely only happen, though, if there was evidence that the credit channel was impaired in the euro area. The previous TLTROs occurred after a period when banks were tightening credit standards, corporate borrowing rates and credit spreads were widening, European bank stocks were falling and European bank lending standards were becoming more restrictive (Chart 12). Chart 12A New TLTRO? Watch Lending Standards

A New TLTRO? Watch Lending Standards

A New TLTRO? Watch Lending Standards

Today, bank stocks are falling and corporate bond yields/spreads are low but slowly rising, while European banks are actually easing lending standards according to the ECB's Q3 Bank Lending Survey. If the latter were to flip into the "tightening standards" zone, without any rebound in European bank shares or decline in corporate borrowing rates, the ECB could be tempted to go down the TLTRO route once again. Bottom Line: If the ECB downgrades its growth and inflation forecasts next month, delaying the end of the APP into 2019 is unlikely, as is altering the country weightings within the APP portfolio. More plausible options include pushing out forward guidance on future rate hikes, extending the maturity of the existing bond holdings, or introducing a new TLTRO to support lending. Likely ECB Options & Investment Implications In our view, the most realistic outcomes for the December ECB meeting can be boiled down to two decisions, conditional on how the ECB's economic forecasts are presented: 1) Unchanged growth & inflation forecasts: The ECB will signal the end of new APP bond purchases at the end of December, while maintaining the current forward guidance on rate hikes that no move will occur until at least September 2019. 2) Downgraded growth & inflation forecasts: The ECB will signal the end of new APP bond purchases at the end of December, but will also push out forward guidance on the first rate hike to at least sometime in mid-2020. In the latter scenario, the ECB could also consider two other options: extending maturities within its German bond holdings, or announcing a new TLTRO. We think that the ECB will wait to see how financial markets absorb the end of new APP buying before considering any move on maturity extension. At the same time, the ECB would signal that a TLTRO is a possibility if lending standards deteriorate and borrowing rates climb higher. While the ECB has talked a lot about how they will continue to reinvest the proceeds of maturing bonds in its portfolio, similar to what the Federal Reserve did after it ended its QE buying, the bigger impact on bond yields will come from a worsening of the supply/demand balance for European bonds. The ECB has been buying amounts greater than the entire net bond issuance of all euro area governments since the APP started in 2015, which has created a scarcity of risk-free sovereign debt for private investors. The result: extremely low bond yields, with a negative term premium (Chart 13). Reduced ECB buying will result in more bonds that have to be purchased by private investors, and a less negative term premium, going forward. Chart 13Bund Term Premium Unwind?

Bund Term Premium Unwind?

Bund Term Premium Unwind?

How high euro area bond yields eventually go will then be determined by more traditional factors, like inflation expectations and the expected path of ECB rate hikes. Going back to the ECB's previous tightening cycles over its existence, actual rate hikes did now occur before inflation expectations - as measured by 5-year CPI swaps, 5-years forward - rose above 2% (Chart 14). Those inflation expectations are now 32bps below that level, and the ECB will not begin to shift to less dovish forward guidance unless the markets begin to discount more stable inflation close to the ECB's "near 2%" target. Chart 14Not Enough Inflation (Yet) To Justify Rate Hikes

Not Enough Inflation (Yet) To Justify Rate Hikes

Not Enough Inflation (Yet) To Justify Rate Hikes

Dovish guidance on future ECB rate hikes will continue to widen the U.S.-Europe interest rate differentials that have helped weaken the euro versus the U.S. dollar in 2018 (Chart 15). This will continue to put downward pressure on EUR/USD cross, particularly with neutral momentum and positioning indicators suggesting that the euro is not yet oversold (bottom panel). Chart 15Likely ECB Actions Are Euro-Bearish

Likely ECB Actions Are Euro-Bearish

Likely ECB Actions Are Euro-Bearish

Bottom Line: The ECB is most likely to take a less hawkish slant in December, but will not signal any rapid move to begin hiking rates. This outcome will be bearish for the euro, but only neutral at best for overvalued European government bonds. Robert Robis, CFA, Senior Vice President Global Fixed Income Strategy rrobis@bcaresearch.com 1 Since not every country in the euro area is also part of the OECD, we could only use 14 of the 19 countries in the euro area in the indicator shown in the middle panel of Chart 5. 2 Please see BCA Foreign Exchange Strategy/Global Fixed Income Strategy Special Report, "Will Rising Wages Cause An Imminent Change In Policy Direction In Europe And Japan?, dated October 6th 2018, available at fes.bcaresearch.com and gfis.bcaresearch.com. 3 The ECB does allow the purchase of both federal government bonds, as well as the debt of government agencies and supranationals, as part of its APP. For our projections, we have assumed that of the €15bn in net new bonds that the ECB buys each month, 82% are debt issued by government-related entities (i.e. 18% goes to credit instruments like corporate bonds and covered bonds), with 10% of those government purchases going to supras. From that reduced number, we assume anywhere from 10-30% of purchases go to agencies, depending on the country. For the sake of simplicity, we also assume a pace of net government bond issuance in line with that seen over the past year, rather than make specific assumptions on changes in individual country budget deficits.

Highlights Did October's equity rout ... : Before bouncing back in its final two sessions, October was the S&P 500's 12th-worst month of the postwar era. ... represent a watershed for financial markets?: Shaken investors have begun asking if the equity bull market is finally over, and if Treasury yields are in the process of making their cyclical highs. Not according to the macro backdrop, which still supports risk assets, ... : There is no recession in sight. An earnings contraction sufficient to induce an equity bear market, or a meaningful pickup in defaults, isn't imminent. ... or our rates checklist, which still supports a bearish take: Inflation may be taking its time, but nothing on our rates checklist calls for increasing duration in a bond portfolio. Feature U.S. equity investors were relieved to close the books on October, which was a notably bad month for the S&P 500. Its 7% loss was good for 33rd-worst in the postwar record books, and just missed being a -2 standard-deviation event. Had the month ended before its robust bounce in the final two sessions, it would have been the 12th-worst, two-and-a-half standard deviations below the mean (Chart 1). At its lowest point, a half-hour before the October 29th close, the index was down a whopping 10.5% for the month. Chart 1Standing Out From The Crowd

Standing Out From The Crowd

Standing Out From The Crowd

The price action understandably unnerved investors. Monthly declines of this magnitude are almost always associated with bear markets; just seven of the thirty-two larger declines occurred outside of bear markets, two of them by the skin of their teeth. Decomposing the equity returns into changes in earnings estimates and changes in forward multiples shows that sharp multiple contraction is a feature of nearly every bad month (Table 1). Table 1Worst Postwar Monthly Declines

Checking In On Our Rates View

Checking In On Our Rates View

It is estimate growth - a robust 0.8% - that makes October something of an outlier among the S&P 500's worst months, and we expect growing forward earnings will keep the S&P out of a bear market for another year, especially now that its multiple is more than 15% off its peak. Earnings growth should also keep spread product out of trouble for the time being. Although we recommend no more than an equal weight in corporate bonds, modest spread widening has boosted their total return prospects. Too Legit To Quit We expect that earnings will keep growing because they rarely contract in a meaningful way outside of recessions. With monetary accommodation likely reinforcing certain fiscal stimulus over the coming year, it is hard to see how the next U.S. recession will occur before 2020. As our U.S. bond strategists pointed out last week, the ongoing market implications of last month's equity decline depend on what precipitated it.1 Was it a simple correction sparked by a valuation reset, or has the market begun to sniff out an economic slowdown? With forward four-quarter earnings growing by an annualized 9.5% in October, it appears that the selloff was nothing more than a valuation reset. As our bond strategists point out, the picture was much different when the S&P 500 corrected in the summer of 2015 and the winter of 2015-16. Those corrections unfolded against the backdrop of a global manufacturing recession (Chart 2). The U.S. economy is not bulletproof, and slowing global growth and tighter financial conditions will eventually bring it to heel, but we think the next recession is still too far down the line for markets to begin selling off in advance of it. Chart 2The Fundamentals Are Much Improved From 2015-16

The Fundamentals Are Much Improved From 2015-16

The Fundamentals Are Much Improved From 2015-16

Checking In With Our Rates Checklist If macro conditions really did change for the worse last month, our bearish rates view may no longer apply, and we would have to rethink our underweight Treasury and below-benchmark-duration calls. We introduced our rates checklist in September to identify and track the key series that could trigger a view change. We review it now to see if perceptions of the Fed, inflation measures, labor-market developments, or financial-market excesses suggest that rates may be at a turning point (Table 2). Table 2Rates View Checklist

Checking In On Our Rates View

Checking In On Our Rates View

Market Perceptions Of The Fed We continue to scratch our head over markets' refusal to take the FOMC's terminal-rate projections seriously. The overnight index swap (OIS) curves are calling for a measly two hikes over the next 12 months ... and the next 18 months ... and the next 24 as well (Chart 3). That would leave the terminal fed funds rate for this tightening cycle at a mere 2.75%. The median projection among FOMC voters is 3 1/8%, and we're looking for anywhere from 3.5 to 4%. We will have to start backing off once the gap between our expectations and the market's expectations begins to close, but it's only widened since we established the checklist. Chart 3Stubbornly Staying Behind The Curve

Stubbornly Staying Behind The Curve

Stubbornly Staying Behind The Curve

We get to our 3.5-4% estimate on the premise that measured inflation will pick up enough to force the Fed to keep hiking beyond its own expectations in a bid to keep inflation from getting out of hand. Client meetings suggest that investors find our inflation call hard to swallow. Some eye-rolling when we mention the Phillips Curve is understandable, but our view is ultimately based on capacity constraints. Tepid investment in the years following the crisis have left the economy's productive potential ill-suited to meet the surge in aggregate demand provoked by tax cuts and fiscal stimulus. An inverted curve would indicate that the bond market has begun to anticipate that rate hikes will soon stifle the economy's momentum. For all the hand-wringing in the media about flattening over the 2-year/10-year segment of the curve, our preferred 3-month/10-year measure remains nowhere near inverting (Chart 4). The yield curve tends to invert way ahead of a recession, so we would look for other indicators to corroborate its message before we changed our big-picture take. We also note that a bear flattening would support below-benchmark-duration positioning. Chart 4The Fed Hasn't Gone Too Far Yet

The Fed Hasn't Gone Too Far Yet

The Fed Hasn't Gone Too Far Yet

Bottom Line: The bond market remains well behind the Fed, and the Fed may well wind up behind the economy. A broad repricing of the Treasury curve awaits. Inflation Measures Inflation's slow creep has gotten a little slower since we initially rolled out the checklist. Headline PCE and CPI have hooked downward, though their uptrends remain intact (Chart 5). Looking forward, continued tightening of the output gap should boost inflation (Chart 6), though long-term expectations have stalled for now (Chart 7). Inflation is the only section of the checklist that has backslid since September, but not by nearly enough to justify checking any of the boxes. Chart 5Two Steps Forward, One Step Back

Two Steps Forward, One Step Back

Two Steps Forward, One Step Back

Chart 6An Economy Running Hot ...

An Economy Running Hot ...

An Economy Running Hot ...

Chart 7... Will Eventually Produce Inflation

... Will Eventually Produce Inflation

... Will Eventually Produce Inflation

Labor Market Indicators The first item on our list of labor-market indicators is the unemployment gap, the difference between the unemployment rate and NAIRU. NAIRU (the Non-Accelerating-Inflation Rate of Unemployment), is the estimate of the lowest sustainable unemployment rate. The actual rate fell below NAIRU in early 2017, and the gap has been getting steadily more negative ever since (Chart 8, top panel). A negative gap is associated with higher compensation, but the wage response has been muted so far (Chart 8, bottom panel). Chart 8Supply And Demand

Supply And Demand

Supply And Demand

Friday's October employment report pointed to further downward pressure on the unemployment gap. The three-month moving average of net payroll additions came in at 218,000, keeping job growth for the last seven years at around 200,000/month (Chart 9). If the trend were to continue for another twelve months, and population growth and the labor force participation rate (Chart 10, middle panel) were to remain constant, the Atlanta Fed Jobs Calculator2 projects that the unemployment rate will fall to 3%. Chart 9A Steady, Job-Rich Recovery

A Steady, Job-Rich Recovery

A Steady, Job-Rich Recovery

Chart 10As 'Hidden' Unemployment Shrinks ...

As "Hidden" Unemployment Shrinks …

As "Hidden" Unemployment Shrinks …

We understand investors' impatience with the Phillips Curve. We admit to being surprised that compensation growth hasn't shown more life to this point (Chart 11). Just because wage gains have been sluggish out of the gate, however, doesn't mean they won't speed up in the future. Ancillary indicators like the broader definition of unemployment that includes discouraged and involuntary part-time workers (Chart 10, top panel), and the ratio of workers voluntarily leaving their jobs (Chart 10, bottom panel), reinforce the unemployment rate's signal that the labor market is on its way to becoming as tight as a drum. Chart 11... Wages Should Rise

... Wages Should Rise

... Wages Should Rise

Broader Indications Of Instability The final three items on our checklist are meant to flag factors that could bump the Fed off its gradual rate-hiking pace. Overheating would encourage the Fed to move more quickly, but there is nothing in the main cyclical elements of the economy that stirs concern (Chart 12). The Fed might move faster if its third mandate - preserving financial stability - dictated it, but the Fed has been quiet about financial-sector imbalances since Governor Brainard expressed concern about corporate lending two months ago. Finally, the Fed is not oblivious to economic strain in the rest of the world, but conditions in even the most vulnerable emerging markets are far from triggering some sort of "EM put." Chart 12No Sign Of Overheating Yet

No Sign Of Overheating Yet

No Sign Of Overheating Yet

Investment Implications We remain constructive on the economy and markets in the absence of a near-term catalyst to cut off the expansion, the credit cycle and/or the equity bull market. Like our bond strategists, we simply think the U.S. economy is too healthy to merit revising our bearish view on rates. The implication for investors with a balanced mandate is to continue to underweight Treasuries. Within fixed-income portfolios, investors should continue to maintain below-benchmark duration. No investment stance is forever, and we are counting on our checklist to help keep us alert to an approaching inflection point in rates, but the coast is clear for now. Doug Peta, Senior Vice President U.S. Investment Strategy dougp@bcaresearch.com 1 Please see BCA Research's U.S. Bond Strategy Weekly Report, "What Kind Of Correction Is This?," published October 30, 2018. Available at usbs.bcaresearch.com. 2https://www.frbatlanta.org/chcs/calculator.aspx?panel=1

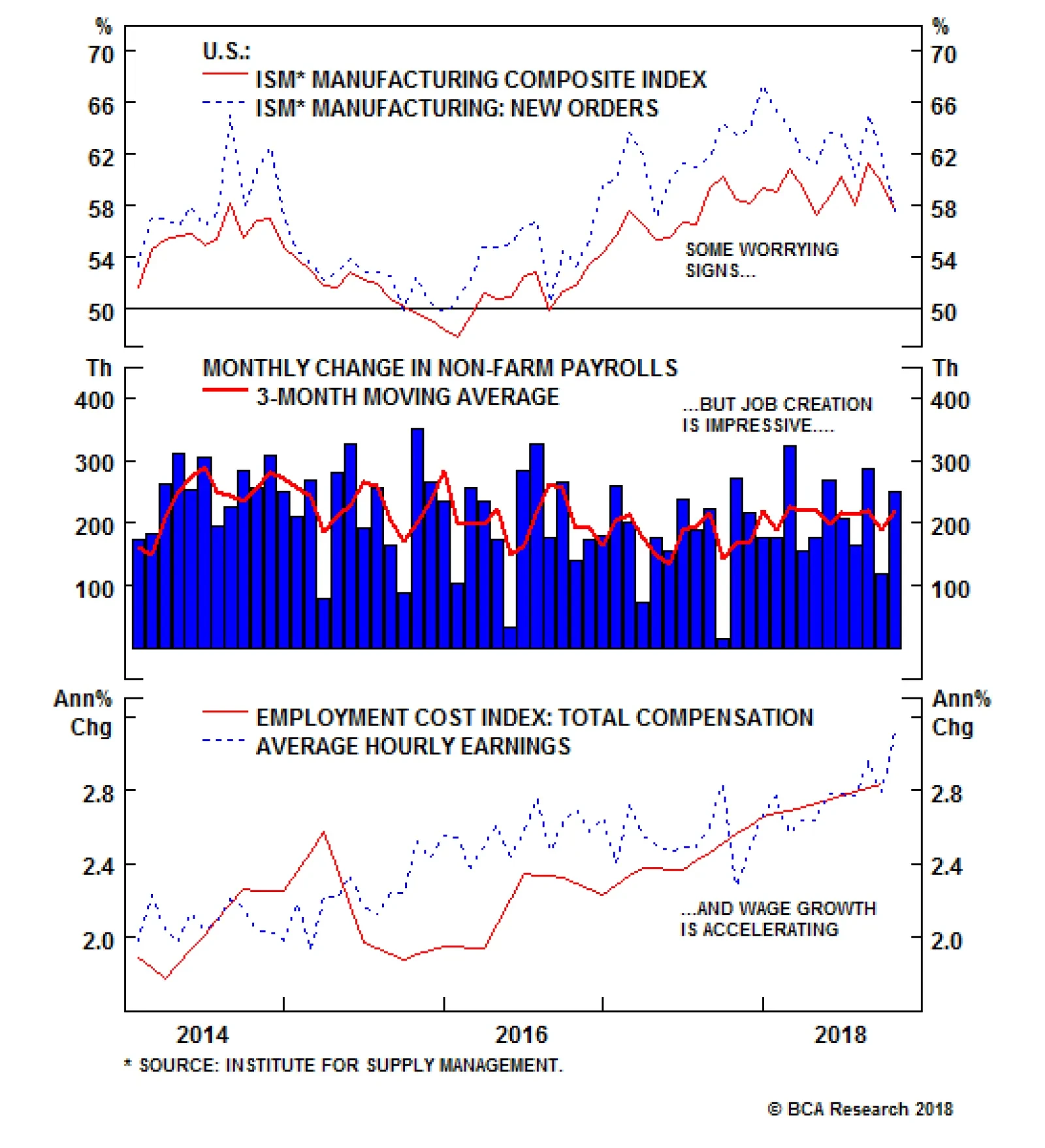

The equity market of late has been highly sensitive to any signs that the U.S. has reached peak economic and profit growth for the cycle, especially given this year’s disappointing housing data. The drop in both the ISM manufacturing composite index and the…

Highlights Duration: Foreign economic growth continues to diverge negatively from growth in the United States. The resulting upward pressure on the U.S. dollar will eventually drag U.S. growth down, and could temporarily threaten the cyclical uptrend in Treasury yields. But so far there is no evidence that dollar strength is too much for the U.S. economy to handle. Investors should maintain below-benchmark duration until signs of contagion are more apparent. Yield Curve: A reading of the macro drivers of the yield curve suggests that the slope of the curve will not steepen or flatten dramatically during the next 6-12 months. In this environment, trades that are long the belly of the curve and short a duration-matched barbell consisting of the short and long ends will profit, due to extremely attractive valuation. We currently recommend going long the 7-year bullet and short the 1/20 barbell. Feature If investors were already worried about the impact of restrictive Fed policy on credit spreads and equities, the minutes from September's FOMC meeting - released last Wednesday - did nothing to calm their nerves. The minutes revealed that "a few participants expected that policy would need to become modestly restrictive for a time" while an additional "number" of participants "judged that it would be necessary to temporarily raise the federal funds rate above their assessments of its longer-run level." There is a small distinction between the "few" participants who expect that a fed funds rate above the estimated longer-run neutral level of 3% will be necessary because restrictive monetary policy will be warranted and the "number" of participants who think that the fed funds rate will move above 3% without policy turning restrictive. However, the main takeaway for investors should be that a large portion of the committee expects that rate hikes will continue until the fed funds rate is at least above 3%. In last week's report we explored the risk that higher yields lead to an excessive tightening of financial conditions and actually sow the seeds of their own decline.1 But we do not view that as the greatest threat to our recommended below-benchmark portfolio duration stance. The biggest risk to that view comes from the ongoing divergence between strong U.S. and weak foreign economic growth. No Contagion... Yet Chart 1 shows that, since 1993, every time our Global (ex. U.S.) Leading Economic Indicator (LEI) has fallen below zero, the U.S. LEI has eventually followed. But while the Global (ex. U.S.) LEI has now been below zero for nine consecutive months, there is so far no evidence of contagion into the United States. The resilience of the U.S. economy probably explains why the September FOMC minutes only briefly mentioned the risk from weak foreign growth. Chart 1U.S. And Foreign Growth Continue To Diverge

U.S. And Foreign Growth Continue To Diverge

U.S. And Foreign Growth Continue To Diverge

From the minutes:2 The divergence between domestic and foreign economic growth prospects and monetary policies was cited as presenting a downside risk because of the potential for further strengthening of the U.S. dollar... But: Participants generally agreed that risks to the outlook appeared roughly balanced. The concern is that, much like in the 2014-16 period, the divergence in growth between the U.S. and the rest of the world puts so much upward pressure on the dollar that it eventually drags U.S. growth and bond yields lower. But despite this year's 4.6% appreciation in the trade-weighted dollar, we have yet to see any impact on our Fed Monitor and Treasury yields remain in an uptrend (Chart 2). This suggests that we have not yet reached peak divergence between U.S. and foreign growth. Further divergence and dollar strength is necessary before the U.S. economy is negatively impacted. Chart 2More $ Strength Required

More $ Strength Required

More $ Strength Required

The reason why the dollar's recent appreciation has not yet exerted a discernible impact on the U.S. economy might be because overall global GDP growth is on a more solid footing than it was in 2014-16 (Chart 3). The IMF forecasts that global GDP growth will be 3.7% in 2018 and 2019, compared to 3.5% in 2015. Meanwhile, the moderation in Eurozone growth represents a decline from lofty 2017 GDP growth of 2.4%. Even in emerging markets, where the global growth slowdown is most apparent, the IMF is still forecasting GDP growth of 4.7% for both 2018 and 2019, a far cry from the 4.3% seen in 2015 (Chart 3, bottom panel). Chart 3Global Growth Stronger Than 2014-16

Global Growth Stronger Than 2014-16

Global Growth Stronger Than 2014-16

Of course, IMF forecasts can always change, and they likely will be revised lower if current trends continue. However, the key point for bond investors is that the global economy is in much better shape than it was between 2014 and 2016. This means that non-U.S. growth needs to see further significant weakness before the uptrend in U.S. Treasury yields is threatened. Bottom Line: Foreign economic growth continues to diverge negatively from growth in the United States. The resulting upward pressure on the U.S. dollar will eventually drag U.S. growth down, and could temporarily threaten the cyclical uptrend in Treasury yields. But so far there is no evidence that dollar strength is too much for the U.S. economy to handle. Investors should maintain below-benchmark duration until signs of contagion are more apparent. Can Uncertainty Steepen The Yield Curve? The yield curve has steepened somewhat during the past few weeks, the result of much higher yields at the long-end of the curve and short-end yields that have been roughly unchanged. We think Fed communication has been an important catalyst for this curve action. Specifically, the Fed's deliberate attempt to introduce uncertainty around its estimates of the neutral fed funds rate.3 Bond investors are finally getting the message that the Fed's median forecast of a 3% longer-run fed funds rate is not written in stone. Depending on the economic outlook, the funds rate could peak for the cycle at a level that is well above or below 3%. Given the recent spate of strong U.S. economic data, the market is starting to discount a peak that is above 3%, no matter what median forecast appears in the Fed's dots. This raises the question of whether a further un-anchoring of long-dated yields could occur. Is it possible that the yield curve will continue to steepen, even with the Fed lifting short rates at a gradual pace of 25 basis points per quarter? Below, we review a few different macro drivers of the yield curve and conclude that neither a large steepening nor large flattening is likely during the next 6-12 months. Nominal GDP Growth One useful rule-of-thumb for when monetary policy turns restrictive is when the 10-year Treasury yield exceeds the rate of growth in nominal GDP. In the past, a 10-year yield above the rate of growth in nominal GDP has coincided with downward pressure on core inflation (Chart 4). With that in mind, we note that nominal GDP has grown by 5.44% during the past year, by 3.98% (annualized) during the past two years and by 3.85% (annualized) during the past three years. Chart 410-Year Yield & Nominal GDP

10-Year Yield & Nominal GDP

10-Year Yield & Nominal GDP

We discount the recent 5.44% growth rate because it was largely fueled by fiscal thrust that will fade in the coming quarters. This leaves us with a recent trend of 3.85% - 4% in nominal GDP growth. Even with no further deterioration in growth as the cycle matures, this puts an approximate cap on how high long-dated yields can rise before policy becomes restrictive and the cycle starts to turn. With the 10-year Treasury yield already at 3.19%, it can rise by between 66 bps and 81 bps before it reaches that range. If that adjustment were to occur very quickly, then the yield curve would steepen sharply and then re-flatten as the Fed lifted rates to catch up with the long end. Alternatively, if that adjustment were to occur over a period of 6-9 months, with the Fed hiking at a pace of 25 bps per quarter, the slope of the yield curve would be roughly unchanged. Wage Growth While nominal GDP growth is useful for thinking about long-maturity yields, wage growth correlates quite strongly with the slope of the yield curve itself. Specifically, rapid wage gains tend to coincide with curve flattening, and vice-versa. In fact, a typical cyclical pattern is that first the yield curve flattens and then wage growth accelerates to catch up with the curve (Chart 5). It would be highly unusual for the yield curve to steepen significantly while wage growth is rising, which it finally appears to be doing. Chart 5Higher Wage Growth = Flatter Curve

Higher Wage Growth = Flatter Curve

Higher Wage Growth = Flatter Curve

We cannot completely rule out the possibility that stronger productivity growth actually causes unit labor costs to decelerate even as "top line" wage pressures mount. Unit labor costs are essentially the ratio of wages (compensation per hour) to productivity (output-per-hour), and the bottom panel of Chart 5 shows that a deceleration in unit labor costs could cause the yield curve to steepen. However, we note that there is not much precedent for strong productivity growth overwhelming an acceleration in wages, causing unit labor costs to diverge from other wage measures. For example, even as productivity growth strengthened in the 1990s, unit labor costs continued to rise alongside other measures of wage growth. Inflation Expectations We have frequently noted that inflation expectations embedded in long-dated Treasury yields remain too low compared to levels that are consistent with inflation being well-anchored around the Fed's 2% target. It stands to reason that long-maturity TIPS breakeven inflation rates could steepen the yield curve as they adjust higher. However, the 10-year TIPS breakeven inflation rate is currently 2.11%, only slightly below the range of 2.3% to 2.5% that has historically been consistent with well-anchored inflation expectations (Chart 6). In other words, the upside in long-dated breakevens is now fairly limited. In contrast, the 2-year TIPS breakeven inflation rate stands at only 1.70%, still considerably below "well-anchored" levels (Chart 6, bottom panel). Chart 6More Upside In Short-Dated Breakevens

More Upside In Short-Dated Breakevens

More Upside In Short-Dated Breakevens

Further, since the financial crisis, breakevens at both the short- and long-ends of the curve have been driven by trends in the actual inflation data (Chart 7). If it is rising realized inflation that has driven both the 2-year and 10-year TIPS breakeven inflation rates higher this cycle, and the 2-year rate is further away from target than the 10-year rate, then it stands to reason that inflation expectations are more likely to exert flattening pressure on the nominal yield curve than steepening pressure. Chart 7Realized Inflation Is Driving Expectations

Realized Inflation Is Driving Expectations

Realized Inflation Is Driving Expectations

Rate Volatility & The Term Premium One final macro driver that could steepen the yield curve would be a spike in interest rate volatility and an increase in the term premium at the long-end of the curve. Our prior research has shown that implied interest rate volatility is linked to uncertainty about the macro environment, and Chart 8 shows that the MOVE index of implied interest rate volatility has tended to track the dispersion of individual forecasts of 3-month T-bill rates and GDP growth. In this context, it should not be surprising that implied volatility fell to very low levels when interest rates were pinned at zero and not expected to move for an extended period. Chart 8Macro Uncertainty & Rate Volatility

Macro Uncertainty & Rate Volatility

Macro Uncertainty & Rate Volatility

But, as was mentioned above, the Fed has been trying scale back its forward guidance and inject some uncertainty into the market. Indeed, we think this is one reason why the yield curve steepened and rate volatility increased during the past few weeks. Taking a broader view, we also observe that, historically, macro uncertainty and implied interest rate volatility have tended to fall when the Fed is hiking rates, only spiking once monetary policy becomes restrictive and the economic recovery is threatened. The yield curve is typically inverted by that point. This leaves us to conclude that some further increase in interest rate volatility from exceptionally low levels is possible, but a large spike is unlikely until monetary policy becomes restrictive. Investment Implications A survey of the macro drivers of the yield curve leaves us to conclude that the most likely outcome for the next 6-12 months is that the slope of the curve remains close to its current level, meaning that the curve undergoes a roughly parallel upward shift as the Fed continues to lift rates. However, if nominal GDP growth fails to decelerate from its current 5.44% clip, it is possible that the yield curve steepens first and then flattens as the Fed lifts rates more quickly to catch up. This is not the most likely outcome, but rather a risk to our base case scenario. The final piece of the puzzle is the observation that curve steepener trades continue to look attractively priced. Our current recommendation is to favor the 7-year bullet over a duration-matched barbell consisting of the 1-year and 20-year notes. This trade offers a spread of +8 bps above the reading from our fair value model (Chart 9). Or alternatively, our model shows that the 1/7/20 butterfly spread is currently priced for 29 bps of 1/20 curve flattening during the next six months (Chart 9, bottom panel). Chart 9Curve Steepeners Are Still Attractive

Curve Steepeners Are Still Attractive

Curve Steepeners Are Still Attractive

That much curve flattening is highly unlikely in the current macro environment, and we continue to recommend curve steepener trades to profit from an unchanged yield curve during the next six months. Bottom Line: A reading of the macro drivers of the yield curve suggests that the slope of the curve will not steepen or flatten dramatically during the next 6-12 months. In this environment, trades that are long the belly of the curve and short a duration-matched barbell consisting of the short and long ends will profit, due to extremely attractive valuation. We currently recommend going long the 7-year bullet and short the 1/20 barbell. Ryan Swift, Vice President U.S. Bond Strategy rswift@bcaresearch.com 1Please see U.S. Bond Strategy Weekly Report, "Rate Shock", dated October 16, 2018, available at usbs.bcaresearch.com 2https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20180926.pdf 3Please see U.S. Bond Strategy Weekly Report, "Rigidly Defined Areas Of Doubt And Uncertainty", dated June 19, 2018, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification