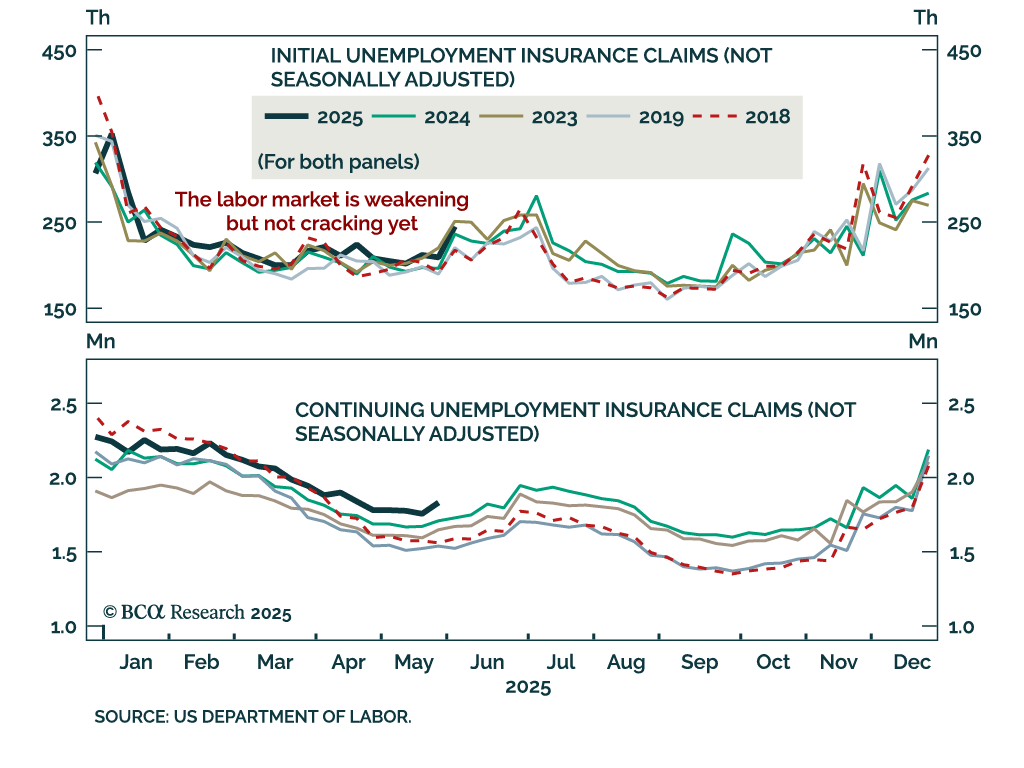

Labor Market

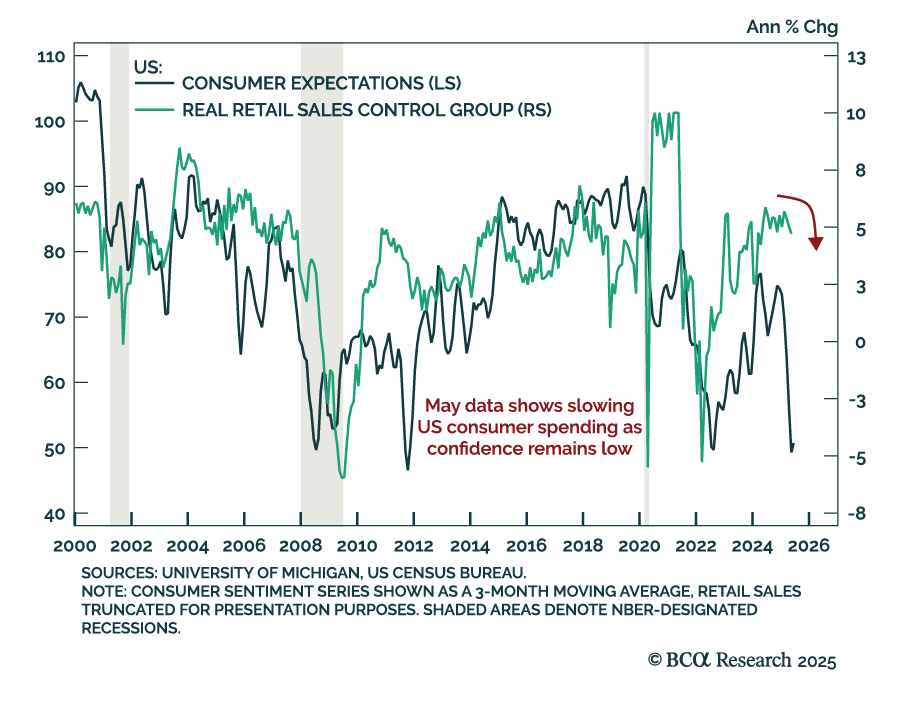

US May retail sales missed expectations, reinforcing our defensive allocation stance. Headline sales fell 0.9% m/m from a downwardly revised -0.1%. Core sales dropped 0.1%, while the control group rose 0.4%, beating estimates. Auto sales were especially weak…

Following a rapid-fire review of issues related to household balance sheets, durable goods demand, the impact of tariffs, DOGE’s capacity to move the budget needle and the labor market’s ongoing cooling, we reiterate our defensive asset allocation recommendations.

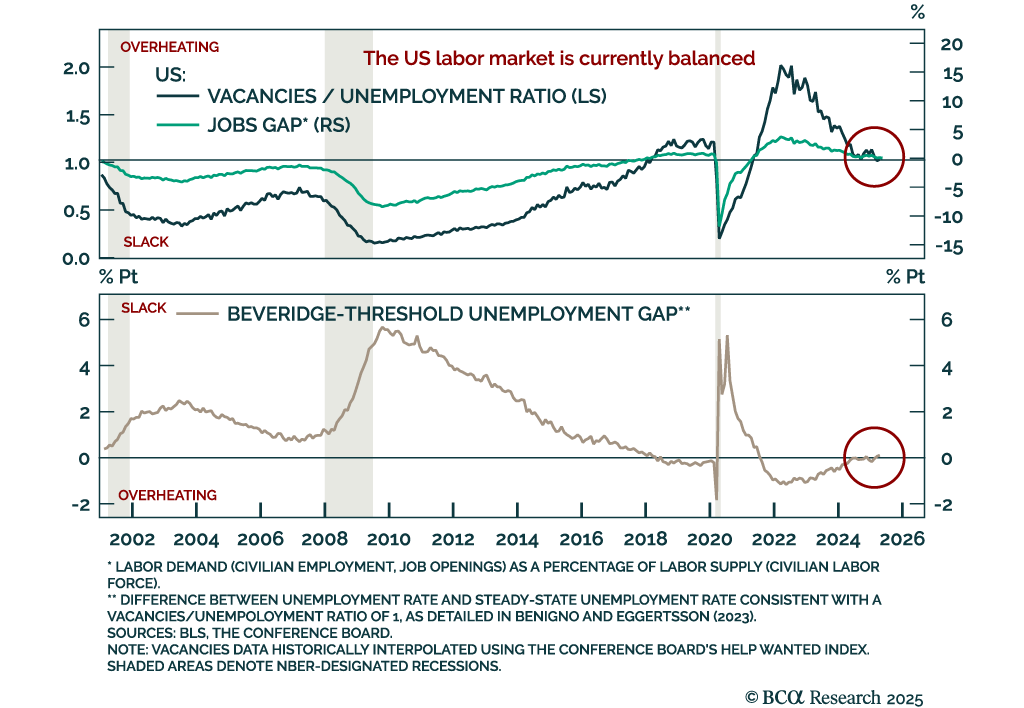

The US labor market appears balanced but at a pivotal point, with further weakness likely to prompt a shift to maximum defensiveness. After running the hottest since the 1960s, the labor market has gradually cooled. That rebalancing sparked a brief growth…

Provided that humanity can overcome the existential risks posed by AI, real incomes will rise. Although most workers will ultimately gain from the transition to an AI-dominated economy, the biggest winners will be those who control the land and the natural resources beneath it.

Further labor market deterioration would trigger a shift to maximum underweight in equities. While soft indicators have markedly deteriorated, hard labor data remains relatively resilient, though it has clearly weakened. The labor market is still in…

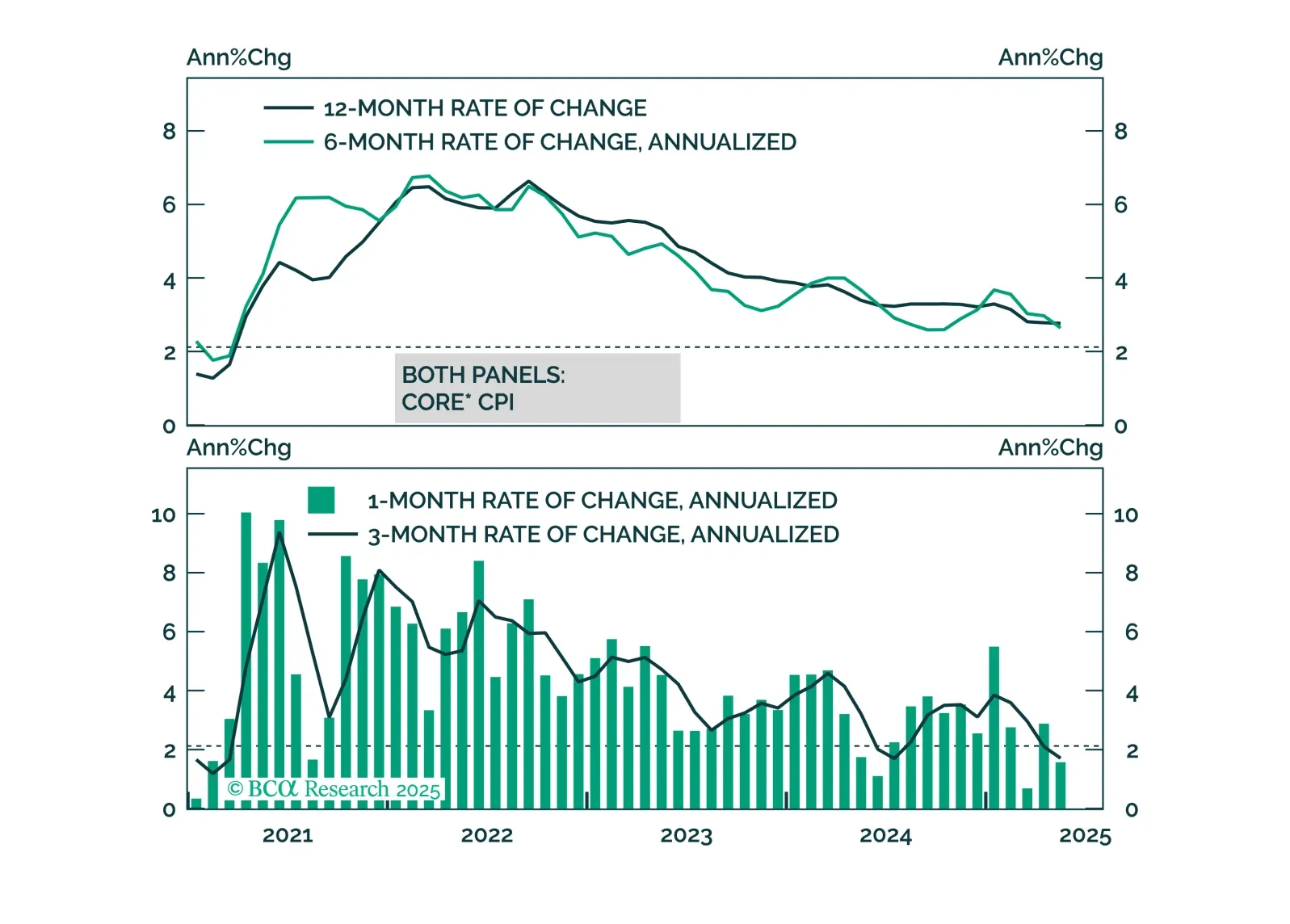

Colder May CPI reinforces our overweight in government bonds and tactical steepener trades as growth slows and the Fed stays cautious. Headline inflation rose 0.1% (2.4% y/y), below expectations, as did core CPI (2.8% y/y). Goods inflation was flat, and…

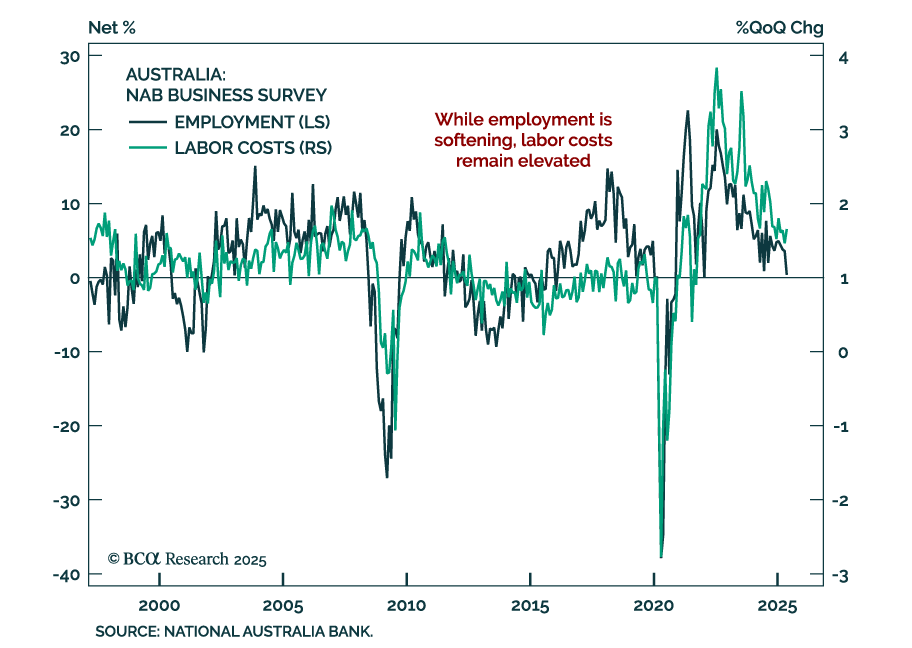

Mixed signals from the NAB Business Survey reinforce our underweight in Australian government bonds and long AUD exposure. In May, business confidence rebounded slightly, rising to 2 from -1, but current conditions dipped to 0 from 2. Profitability continued…

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

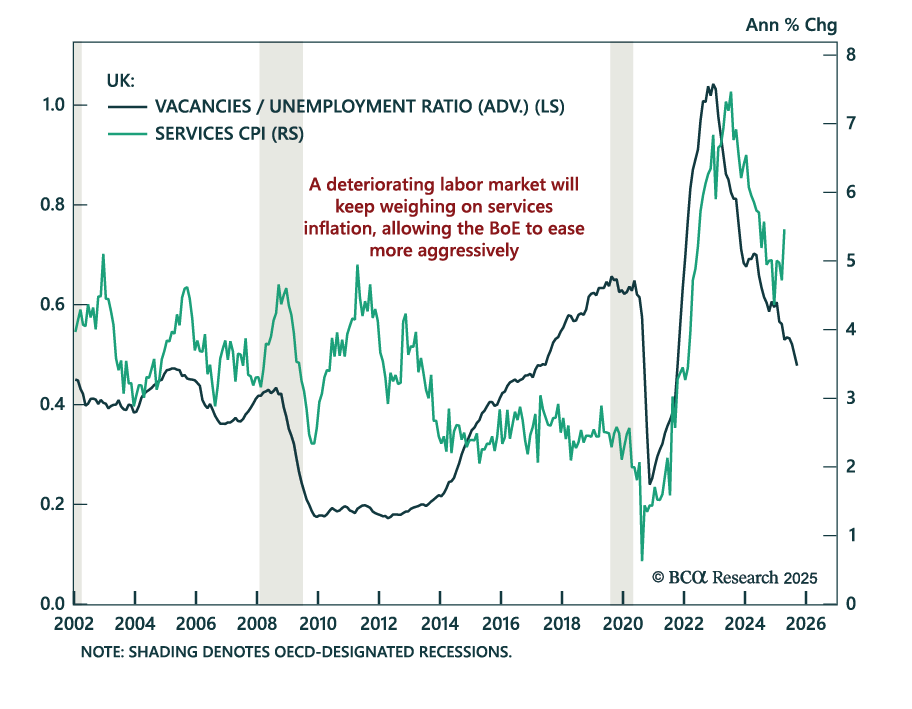

UK labor market deterioration reinforces our overweight on Gilts and dovish BoE policy trades. Payrolls fell by 109k in May, an acceleration from the 55k revised decline for April (originally reported as -33k), and job vacancies continued to slide. Slower…

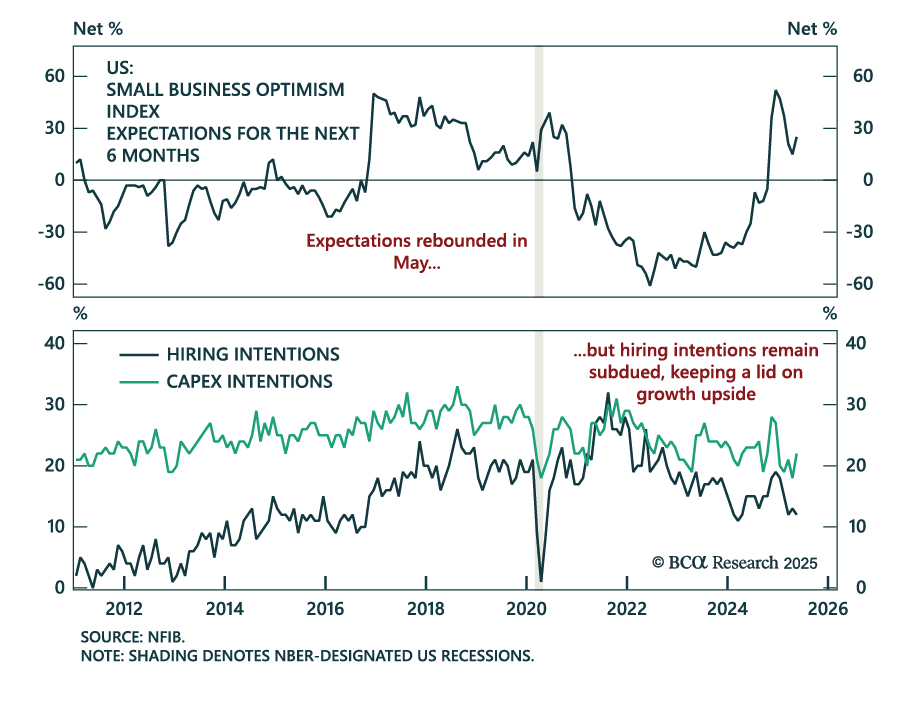

Small business confidence improved in May, but hiring intentions fell and activity remains sluggish, reinforcing our cautious equity stance. The NFIB Small Business Optimism Index rose to 98.8, beating expectations. However, most of the improvement came from…