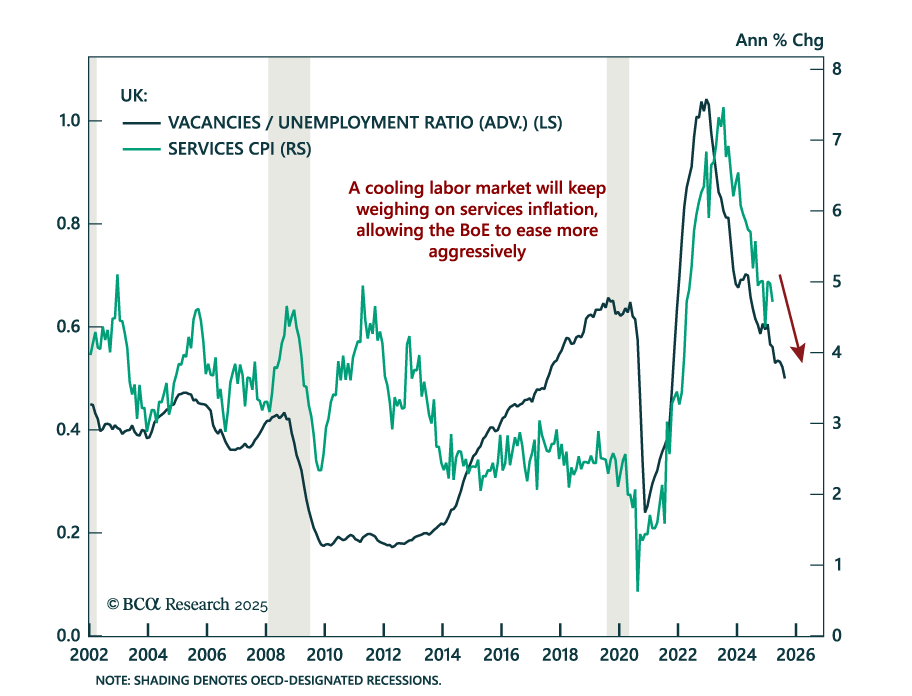

Labor Market

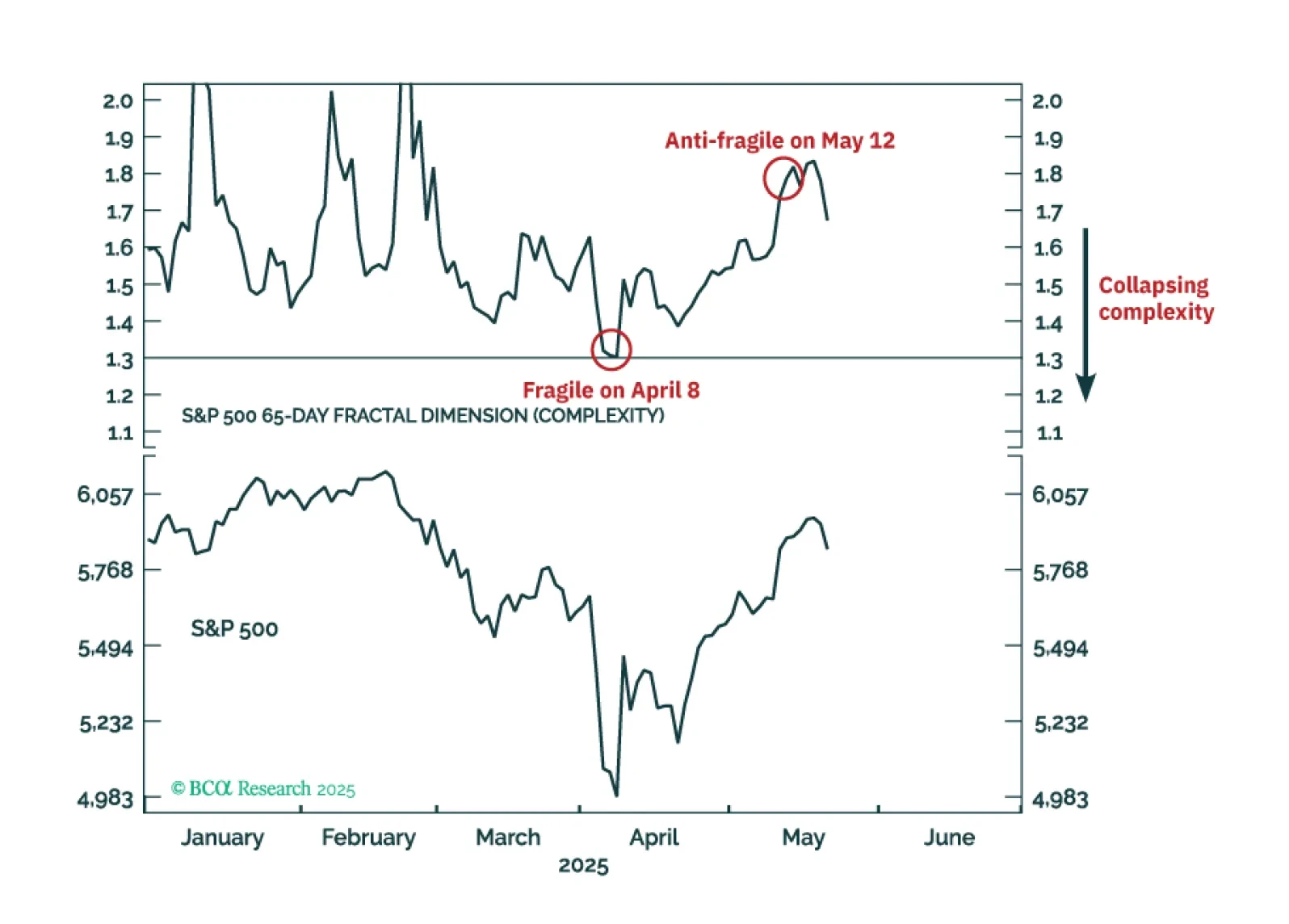

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.

Risk assets rallied hard following the Great Geneva De-escalation, but we are not enamored of risk assets’ risk-reward profile. Forward-looking survey data remain awful on balance and we continue to recommend a defensive asset allocation profile.

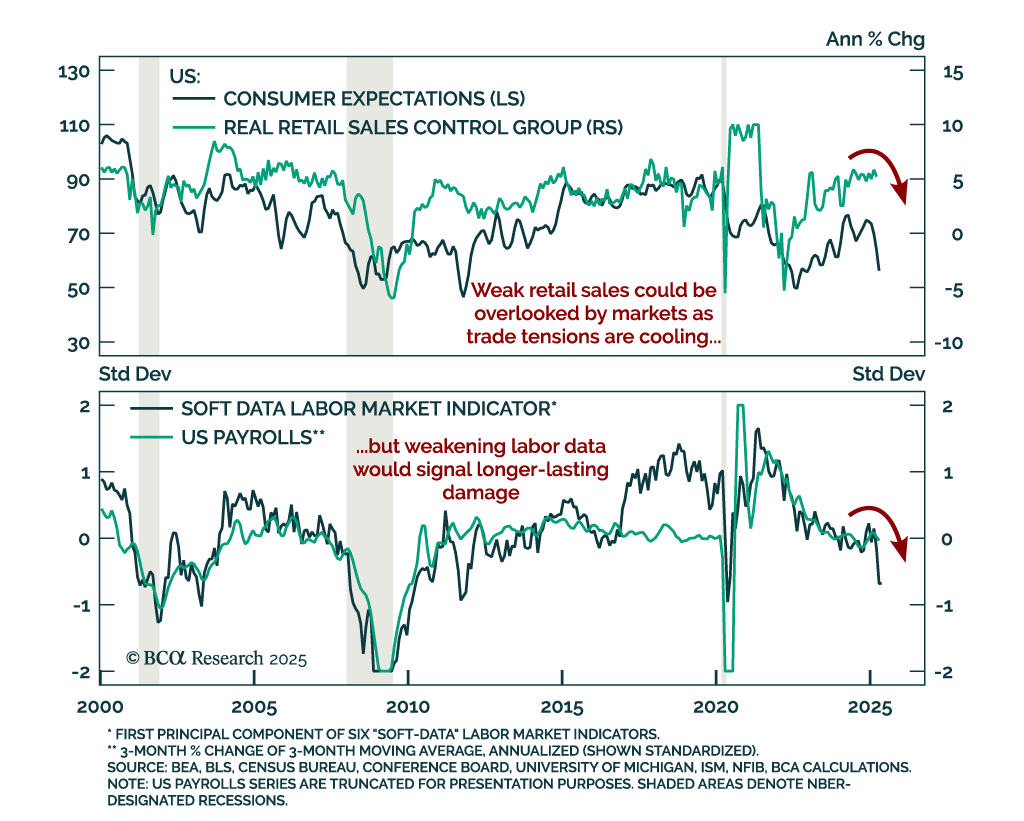

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.

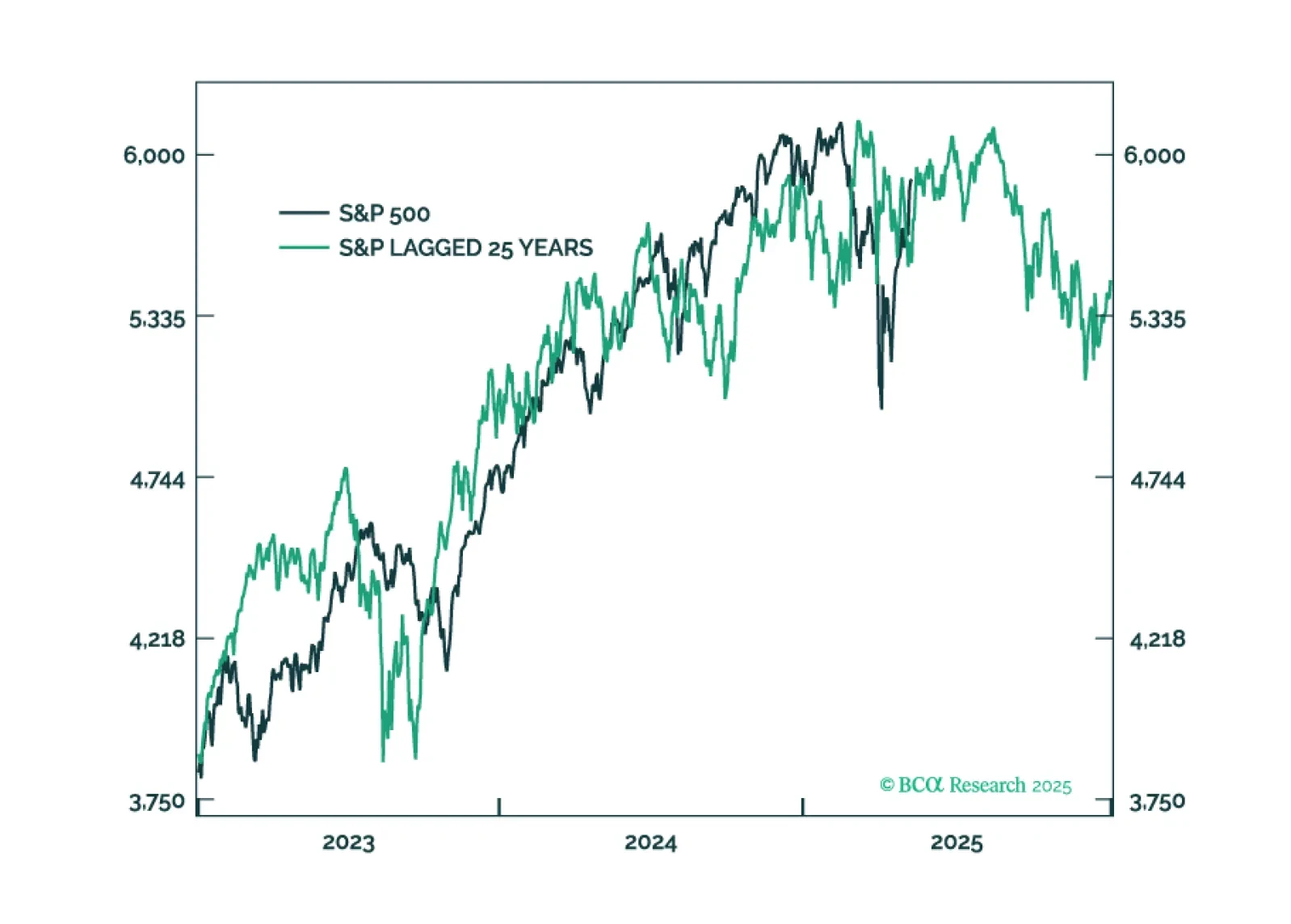

This year’s plunge in tech stocks followed by the recent strong countertrend rally is eerily reminiscent of 2000. But the market and economic parallels between 2025 and in 2000 run much deeper. This report lists 10 striking parallels between 2025 and 2020, then highlights some important differences, and ends by describing how the rest of 2025 might unfold based on a playbook that is: 2025 = ‘2000 with some tweaks.’

A weakening economy will apply downward pressure to Treasury yields, but the Trump term premium will keep long-dated yields higher than they would otherwise be. This makes Treasury curve steepeners the most attractive trade in US fixed income.

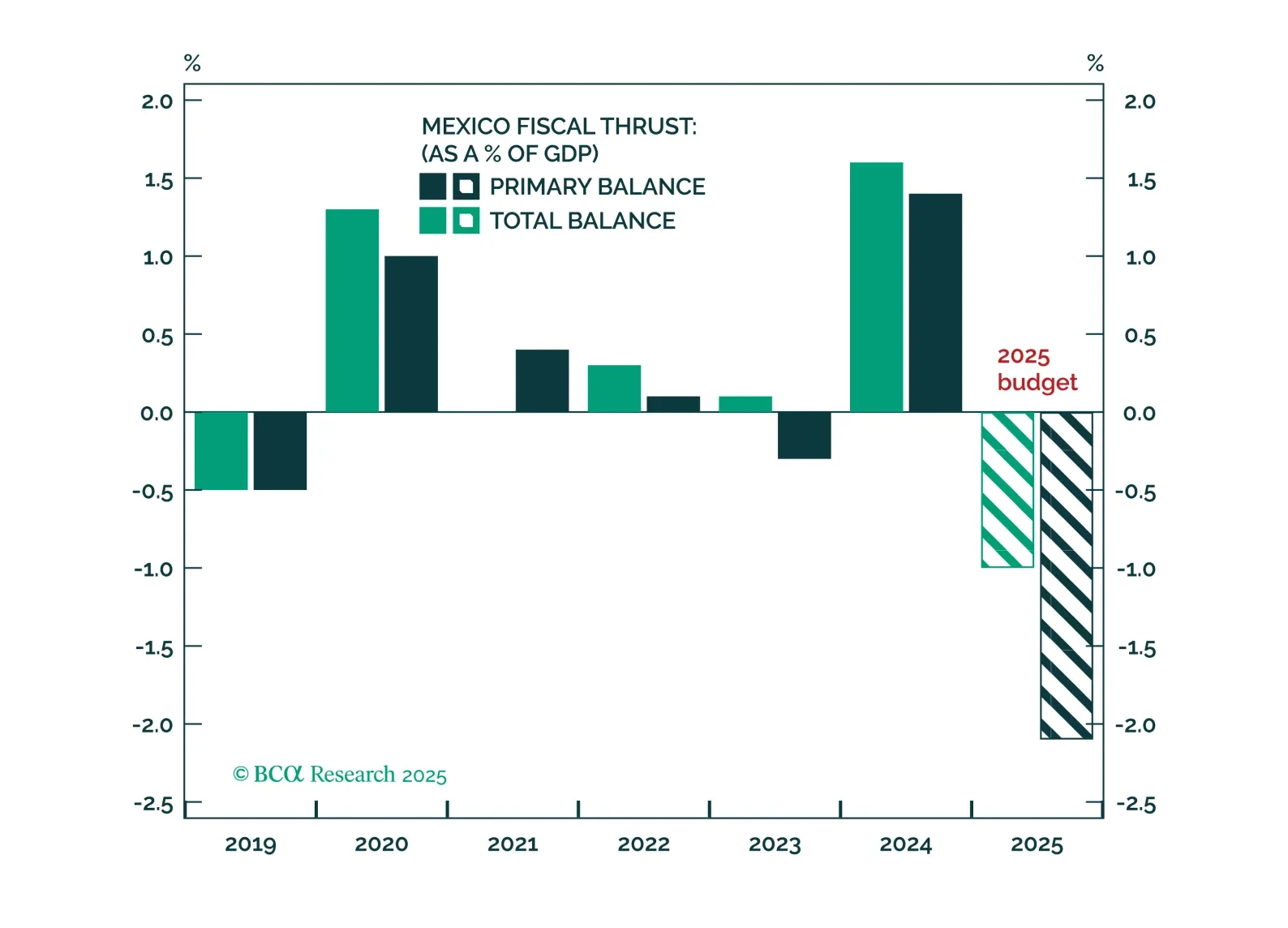

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.