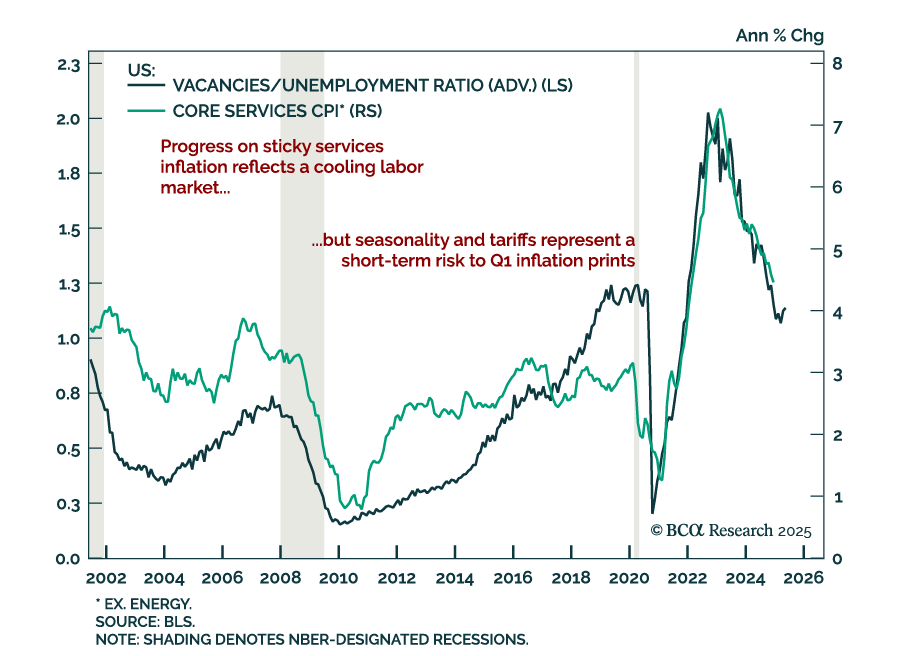

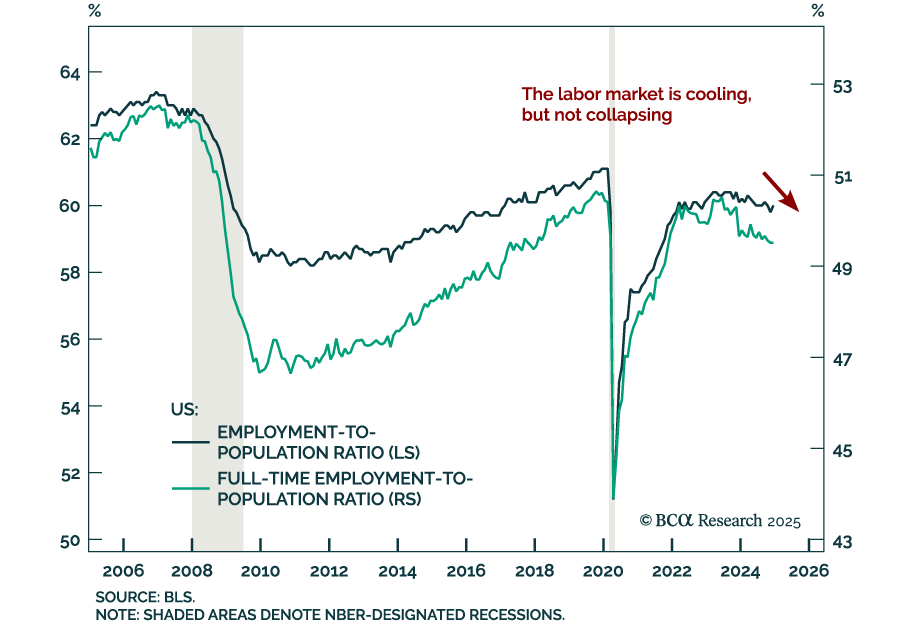

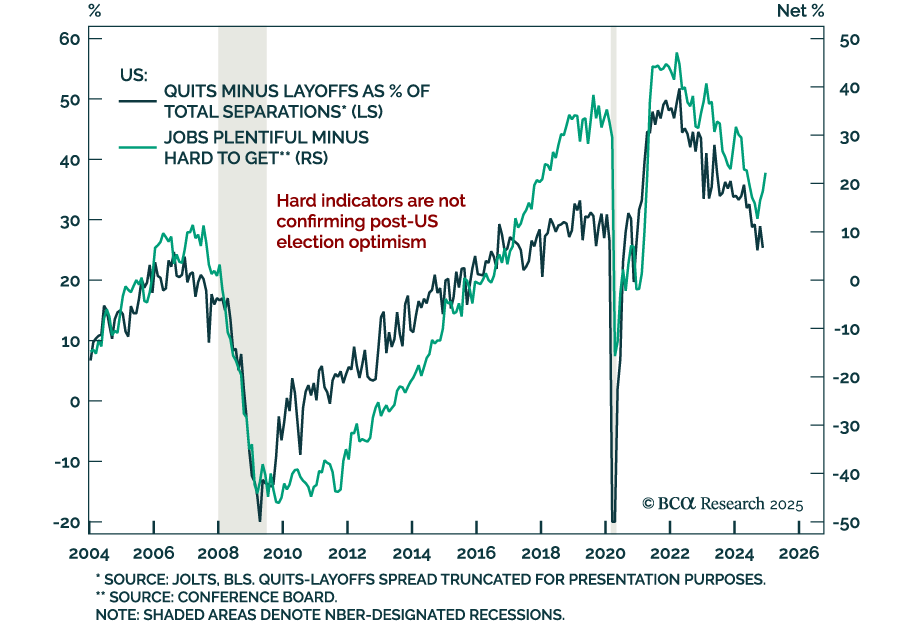

Labor Market

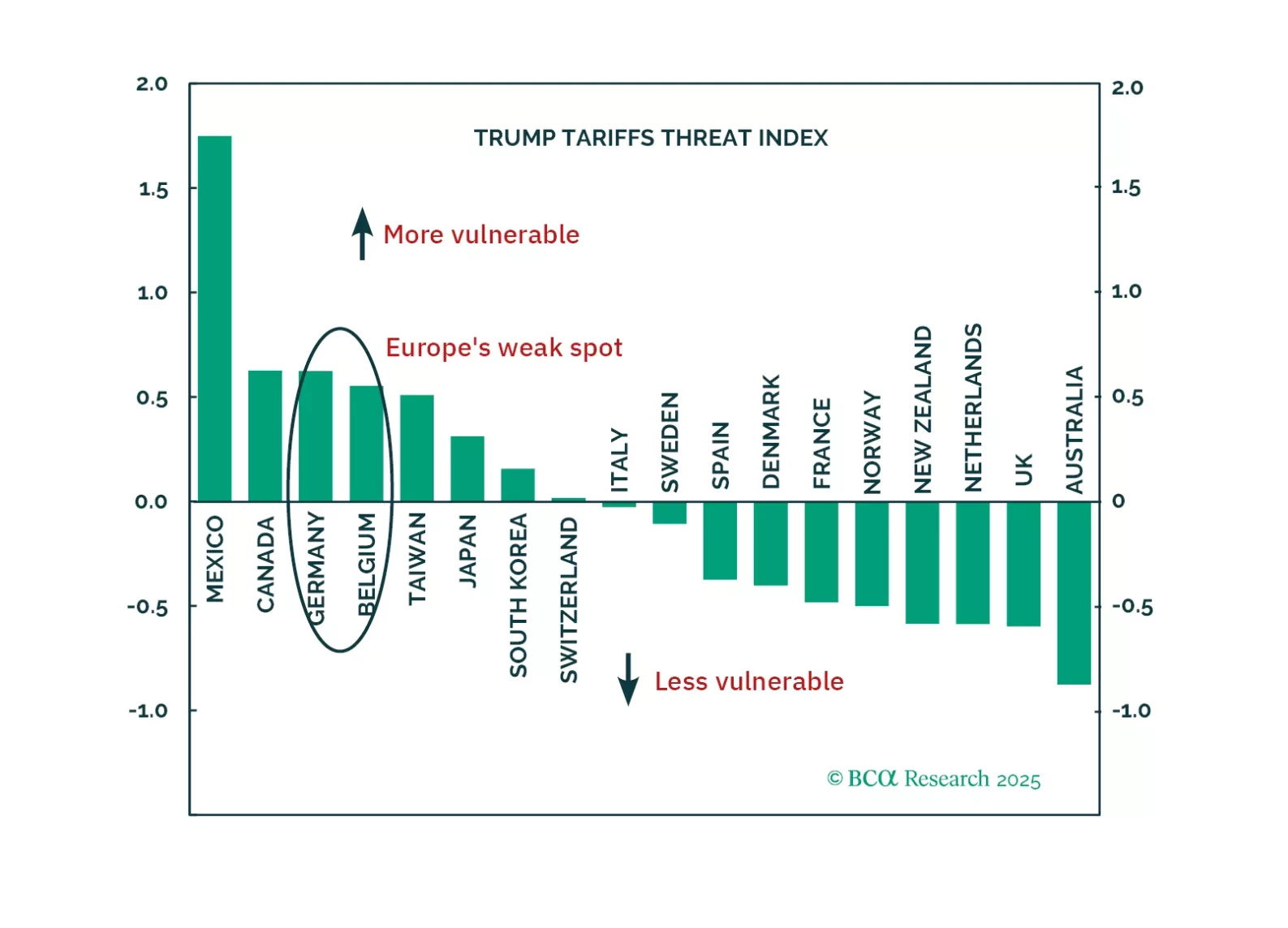

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

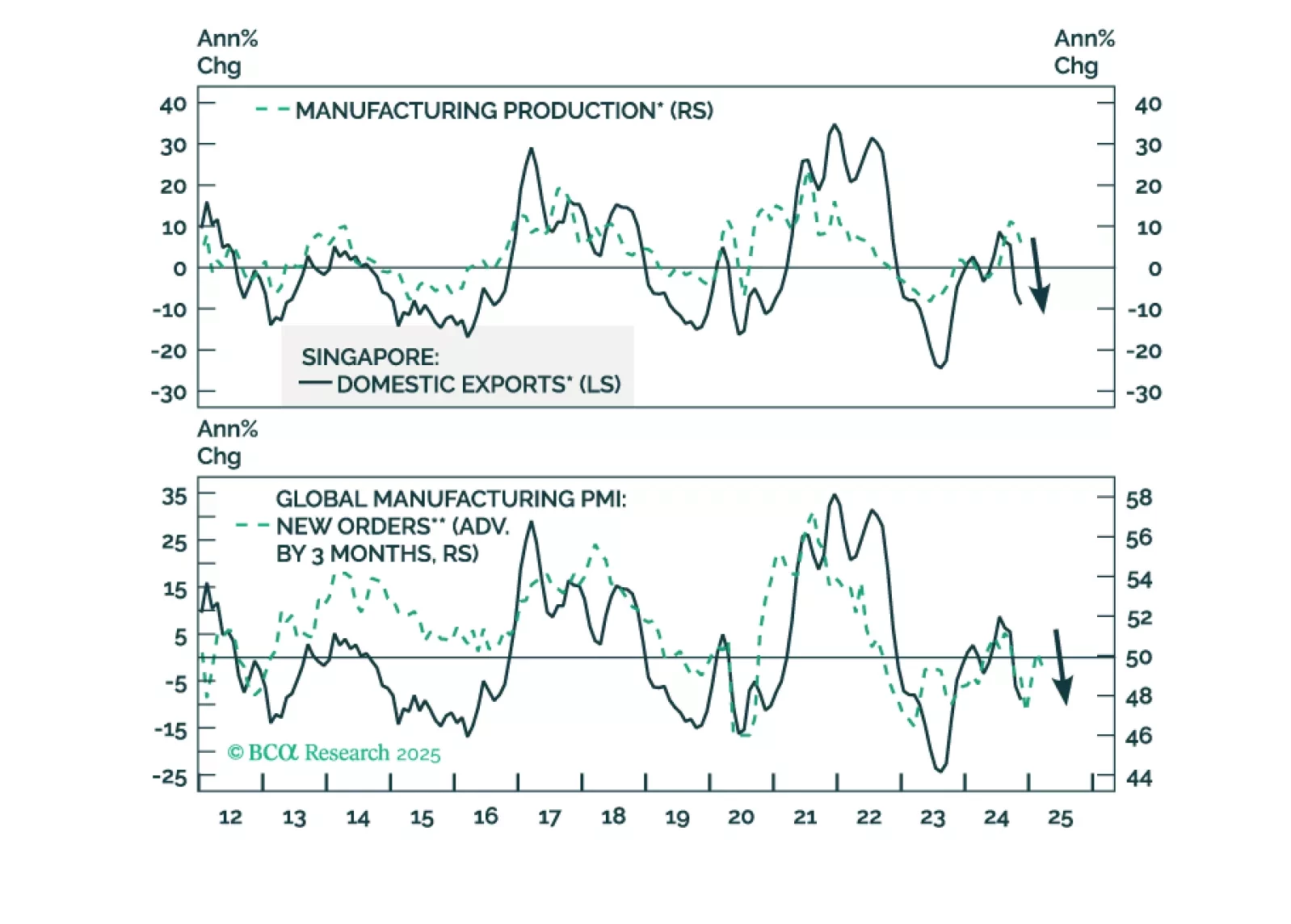

Can Singapore stocks continue the bull run into 2025? What does the city-state’s manufacturing and export outlook foretell? Is the Singapore dollar still competitive? See our analysis and investment recommendations in today’s report.

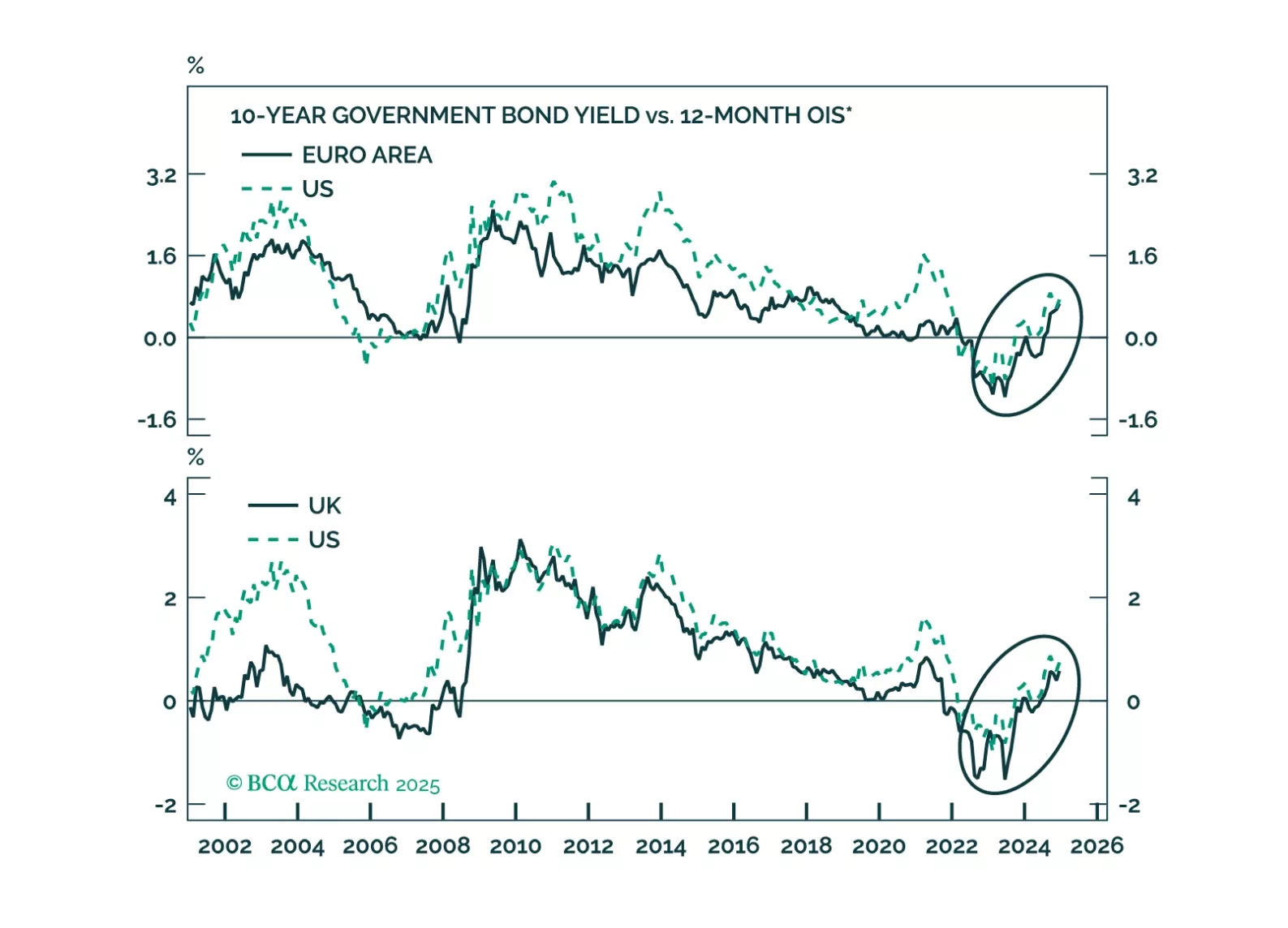

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?

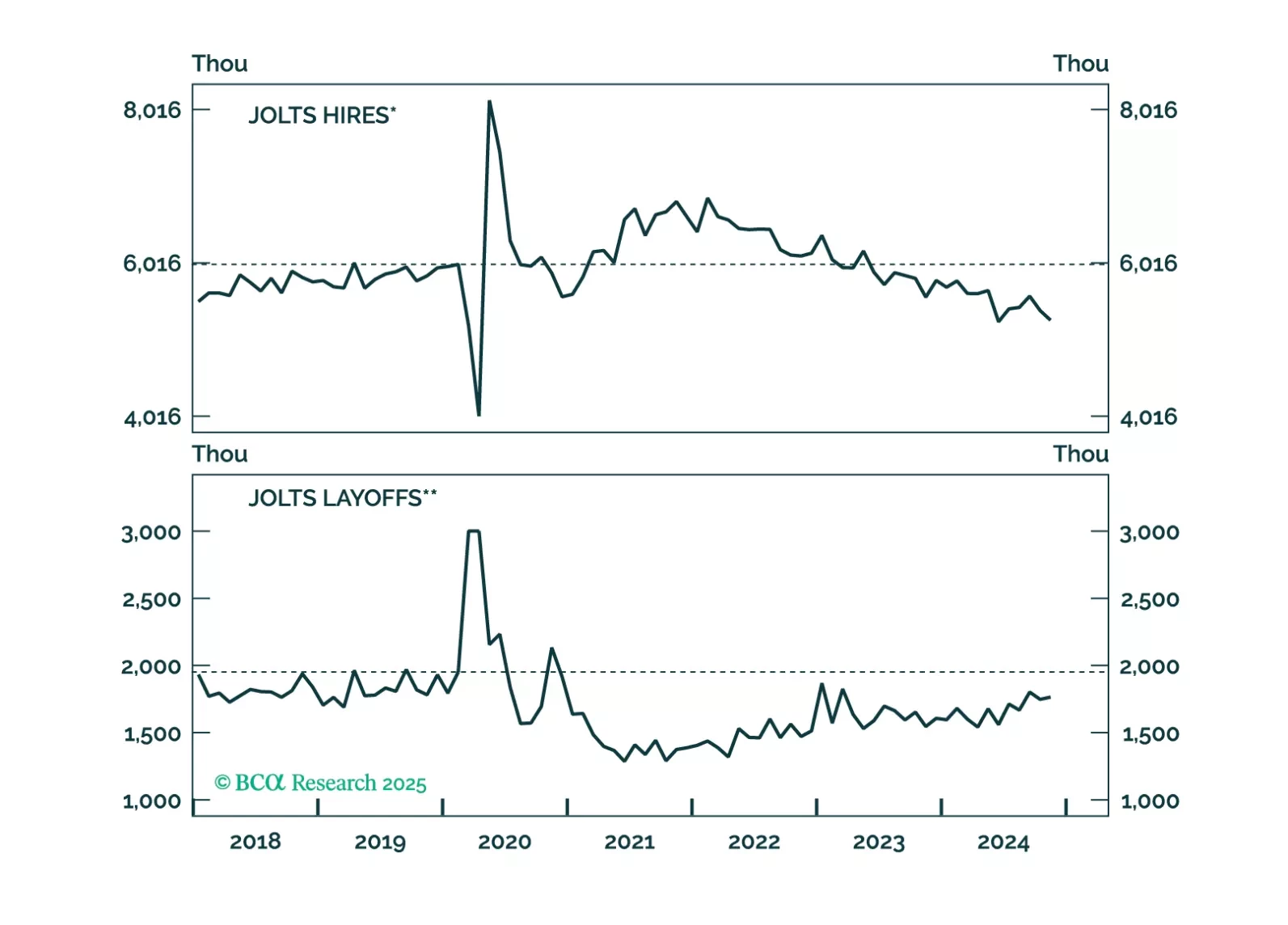

Thoughts on the increase in bond yields and this morning’s employment data.

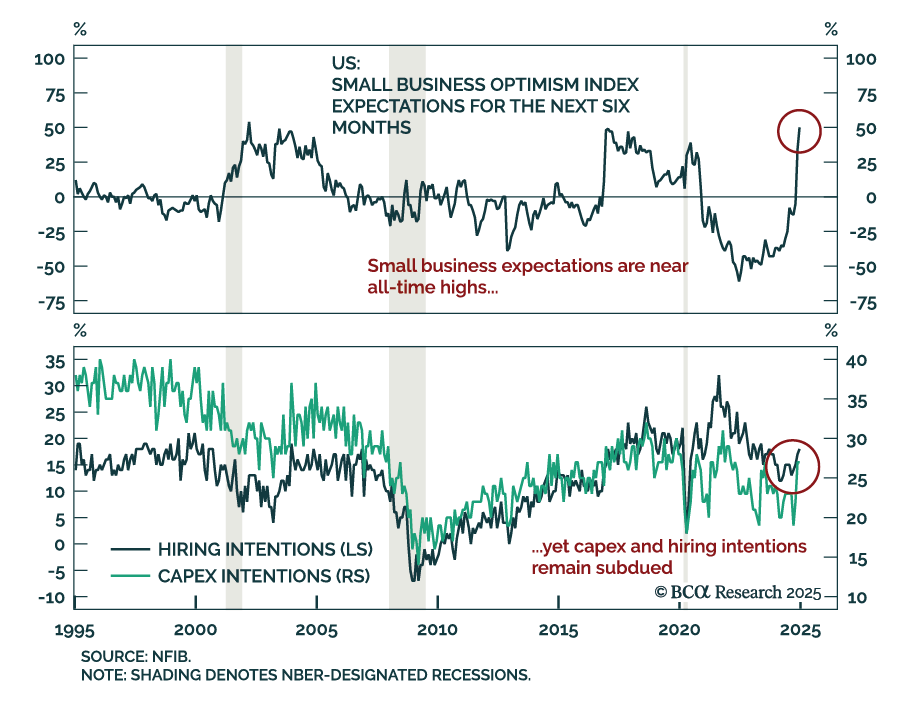

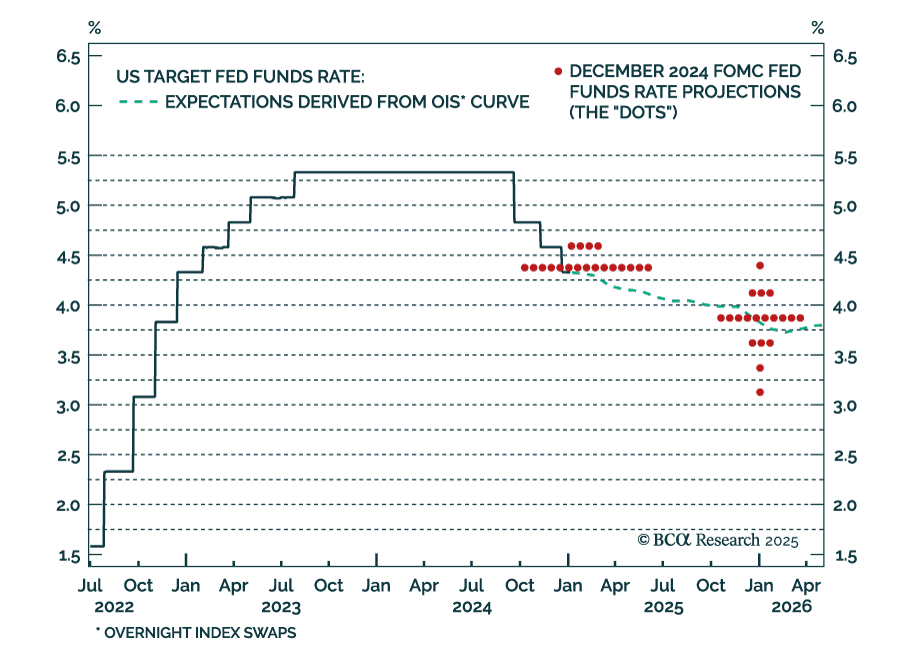

Paradoxically, raging optimism on the US economy is making a reacceleration in growth less likely in 2025. The reaction of the bond market has made the Fed rethink its cutting campaign. Markets are also constraining Trump’s agenda. US manufacturing will not recover with a surging dollar. Fears of inflation and debt sustainability have made moderate House Republicans push back against the President Elect’s wishes. Given the sky-high optimism embedded in asset prices, we believe a defensive portfolio stance is warranted on a 12-month horizon. Overweight gold to hedge the risk of a fiscal crisis.