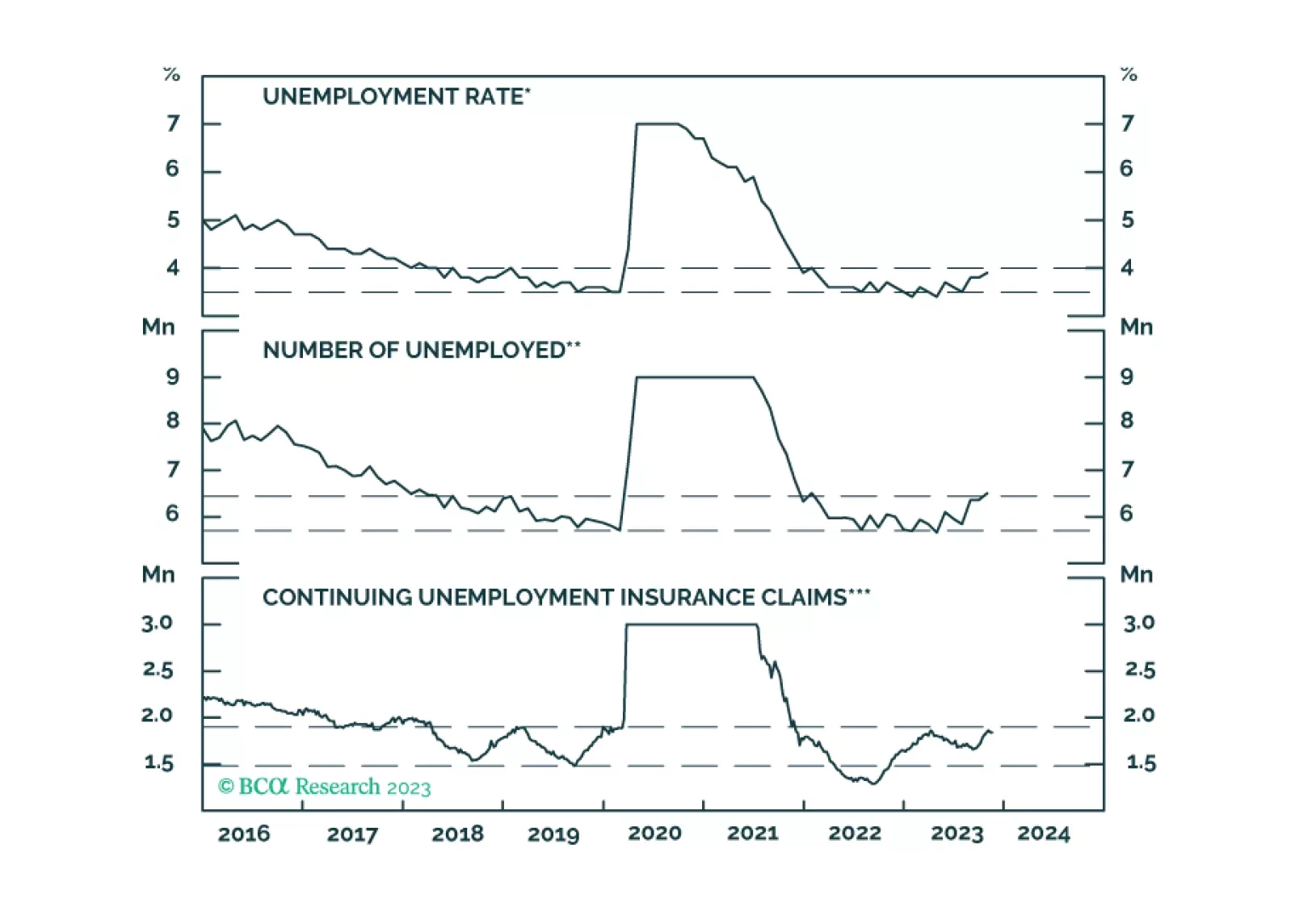

Labor Market

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

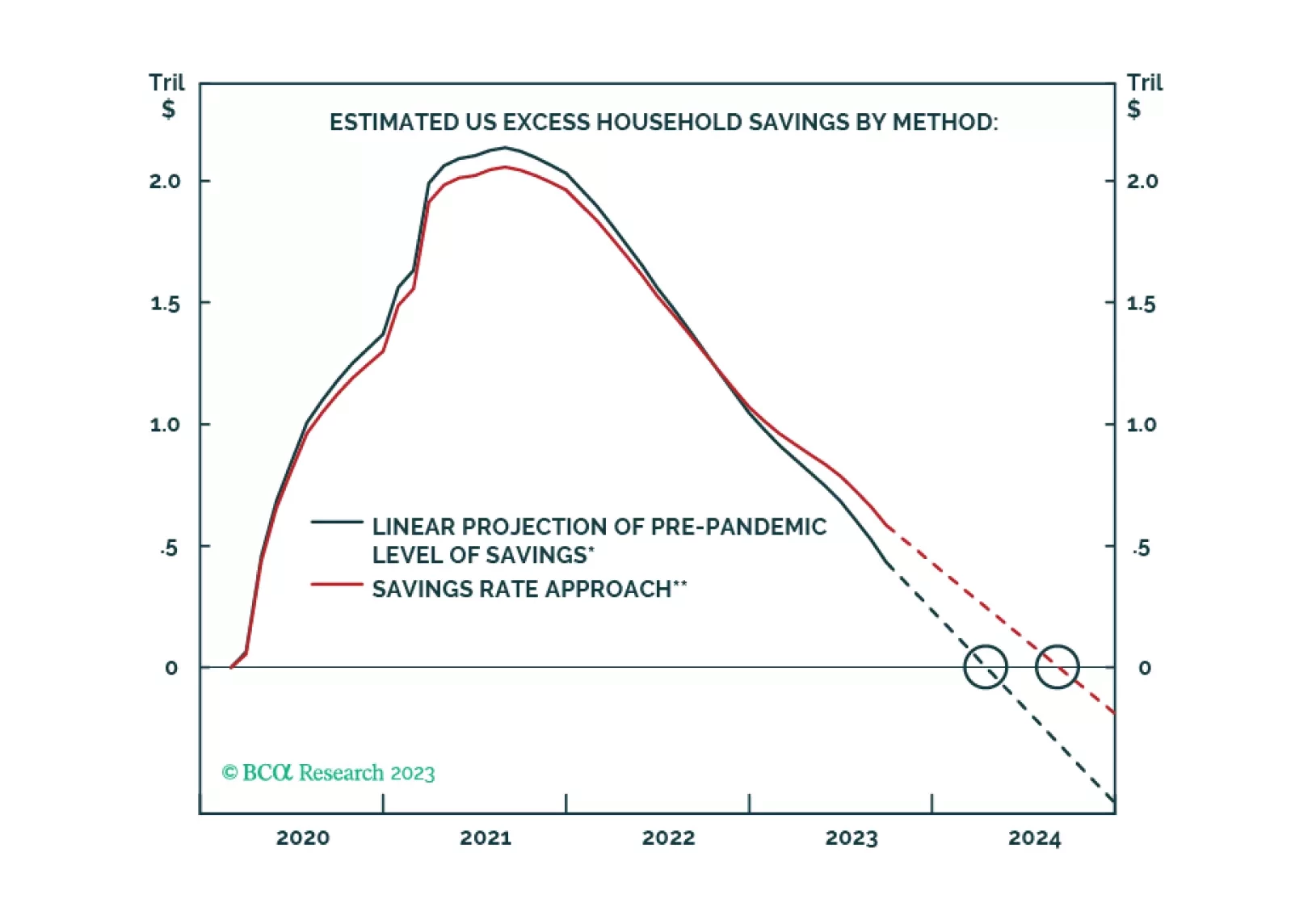

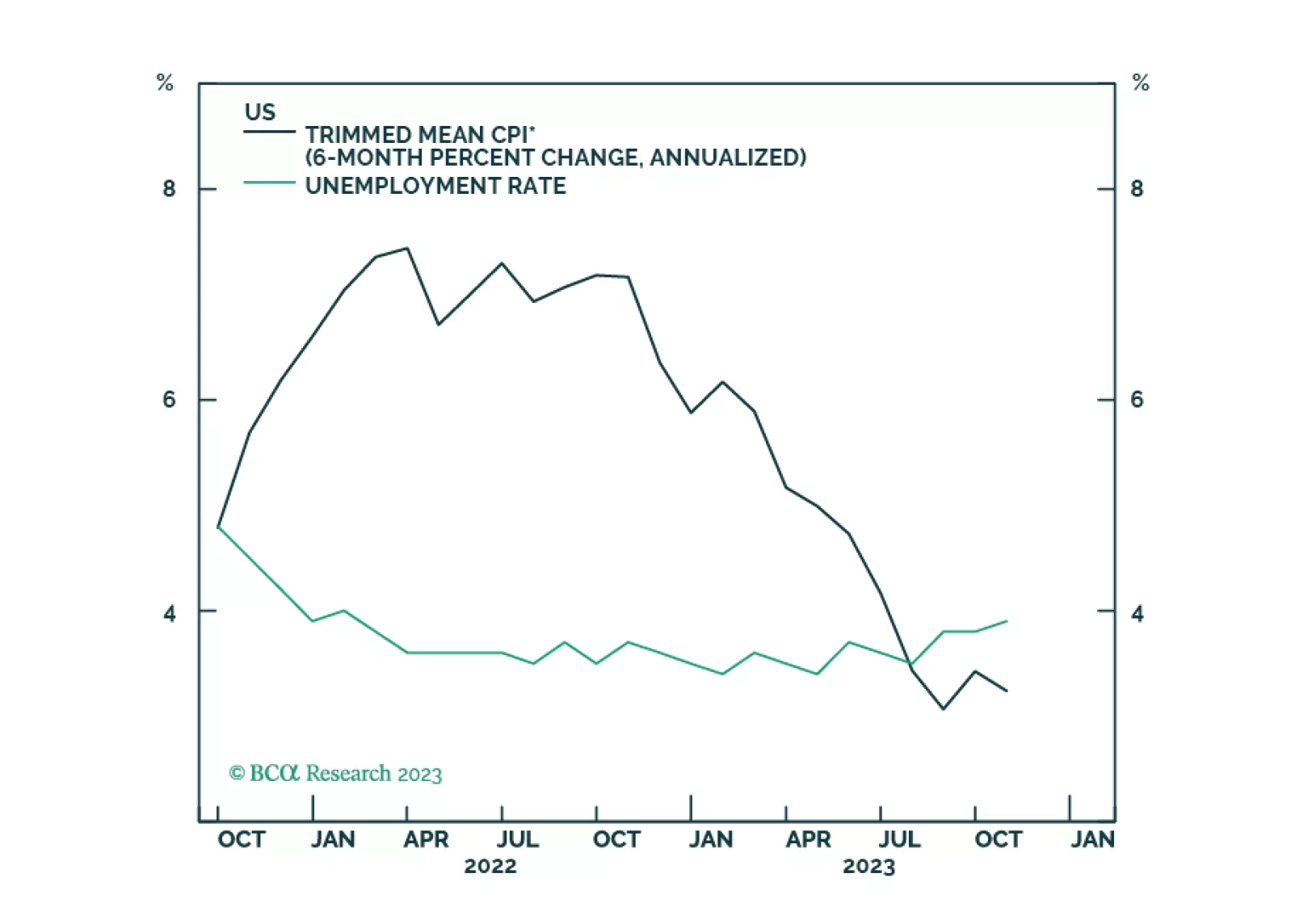

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

We investigate the recent increase in unemployment with the goal of determining whether it is flagging an imminent US recession.

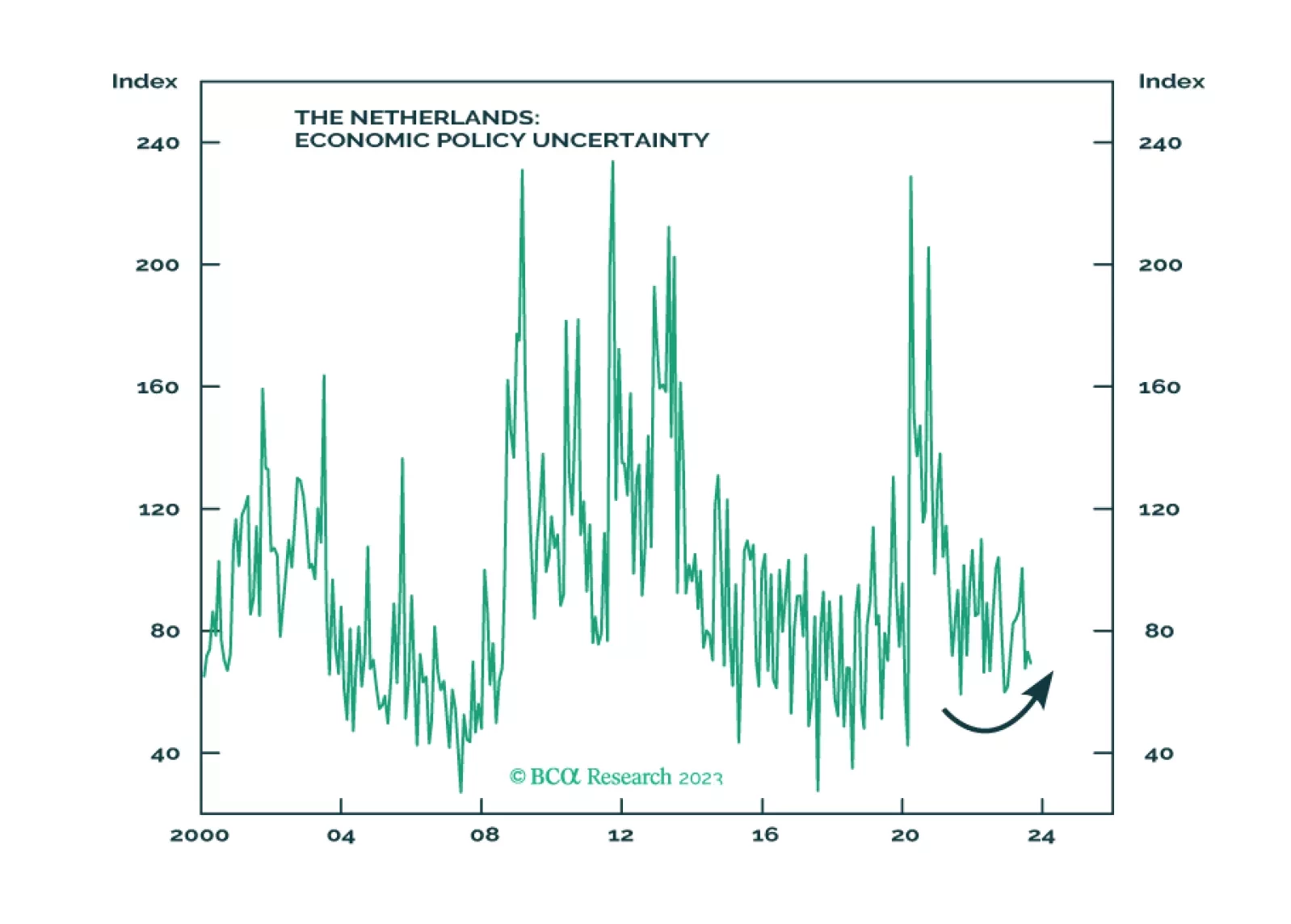

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.