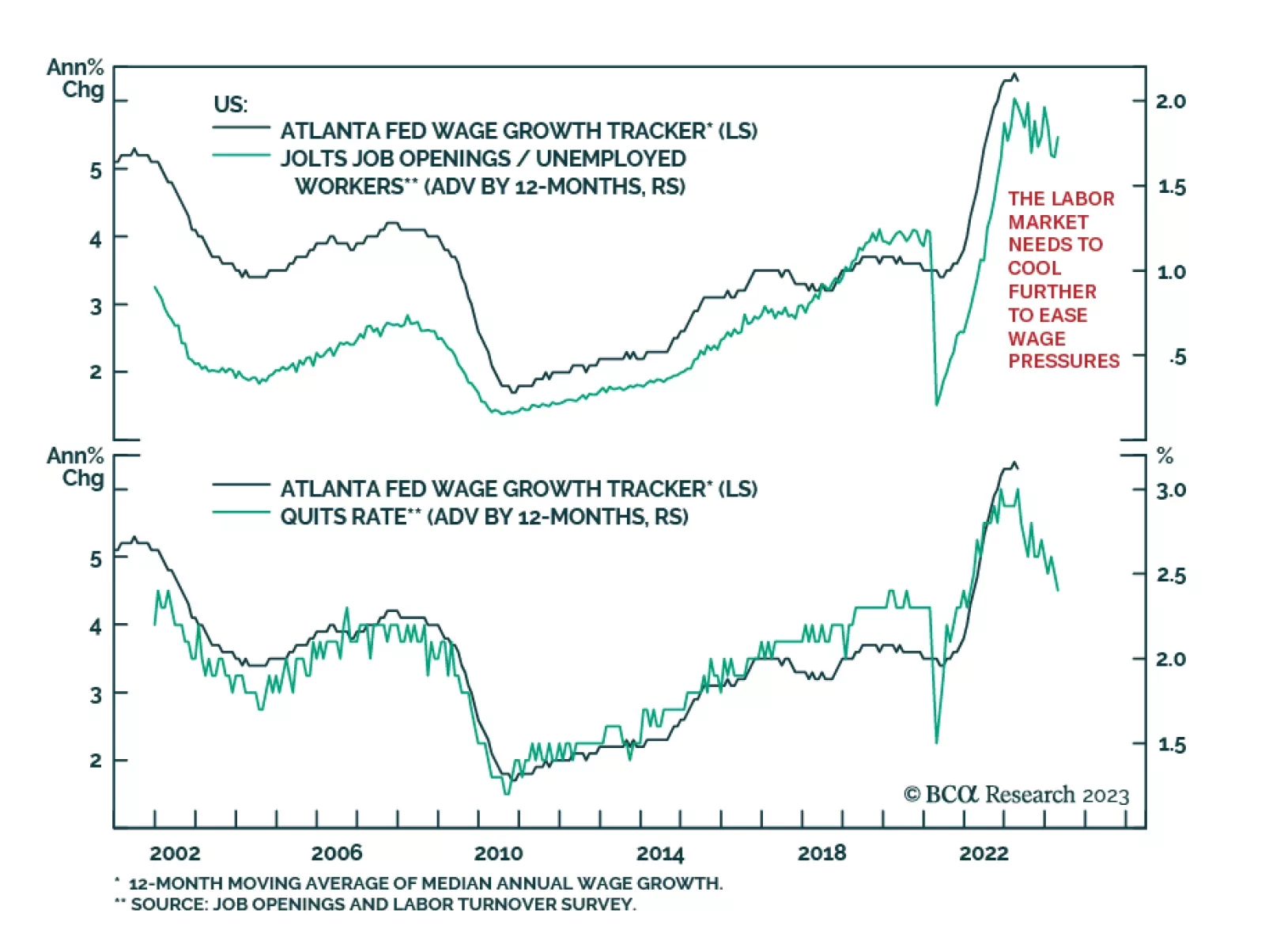

Labor Market

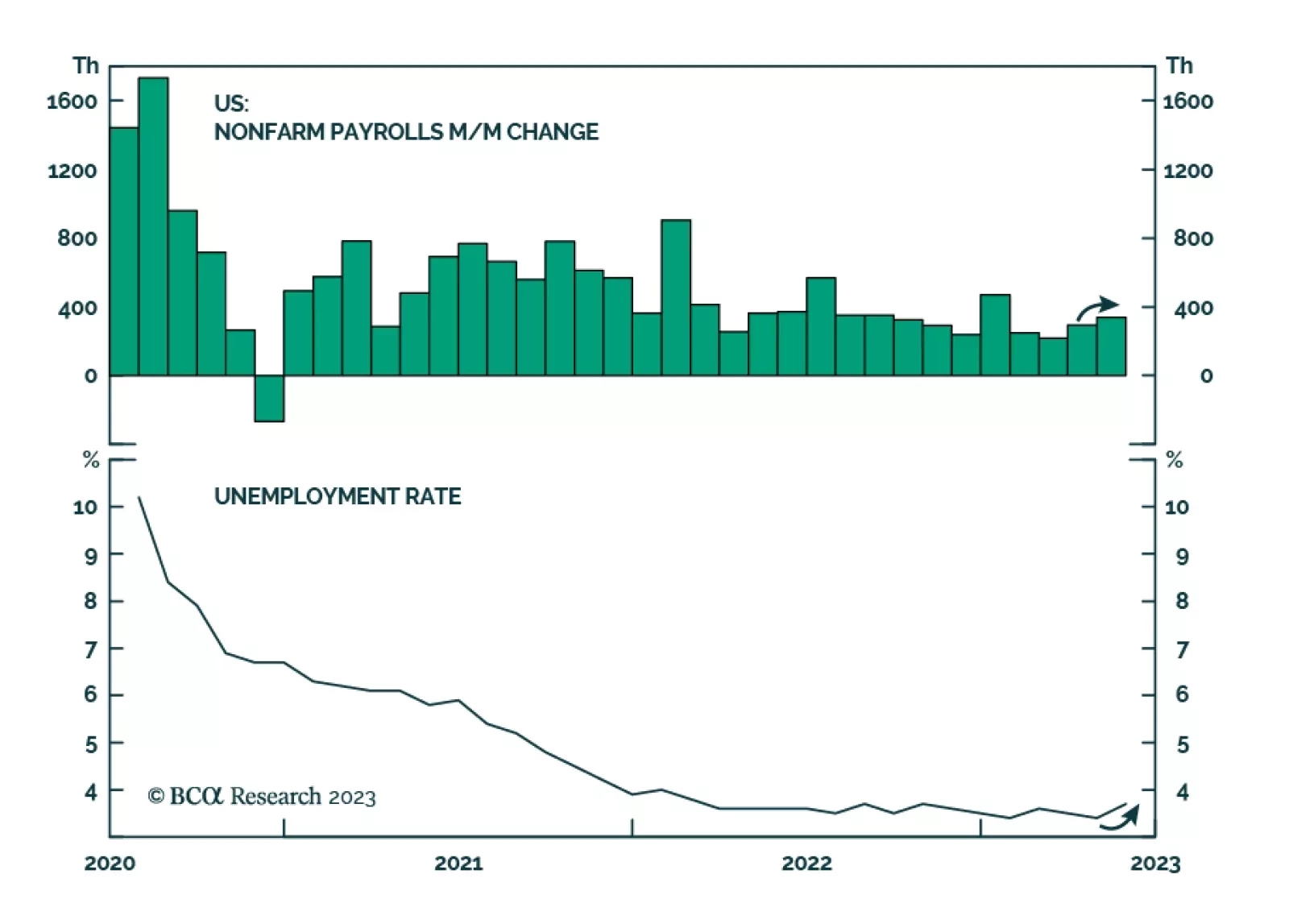

The Fed is still on track for a June pause, even after May’s strong nonfarm payroll print.

President Erdogan and the Justice and Development Party emerged as the winner of the Turkish general election which was concluded yesterday. This victory means that their expansive policies of the past decade will continue, and Turkish assets will suffer. Across the Aegean, the Greeks voted to reelect the New Democrats under the leadership of Prime Minister Mitsotakis. Their fiscal prudence and structural reforms will be continued as voters had rewarded them with another term in office. Go long Greek versus Turkish equities.

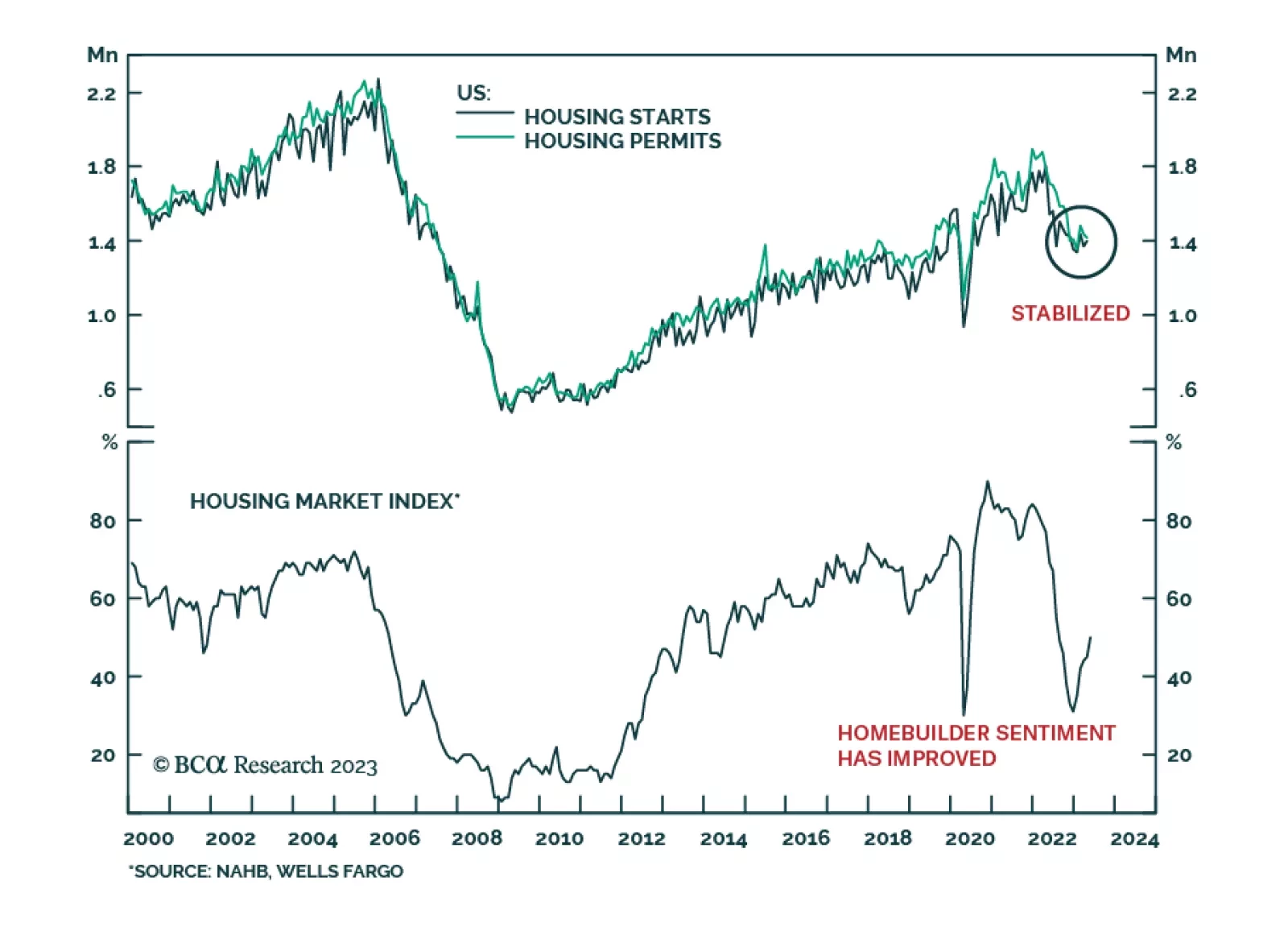

Once the debt ceiling soap opera ends, investors will likely turn their attention to some of the tailwinds supporting stocks. These include stronger earnings growth, diminished bank stresses, better housing data, early signs of an upleg in the manufacturing cycle, the prospects of an AI-driven productivity boom, and the fact that labor slack has managed to increase without rising unemployment. Investors should resist turning bearish on stocks for now but look to become more defensive later this year.

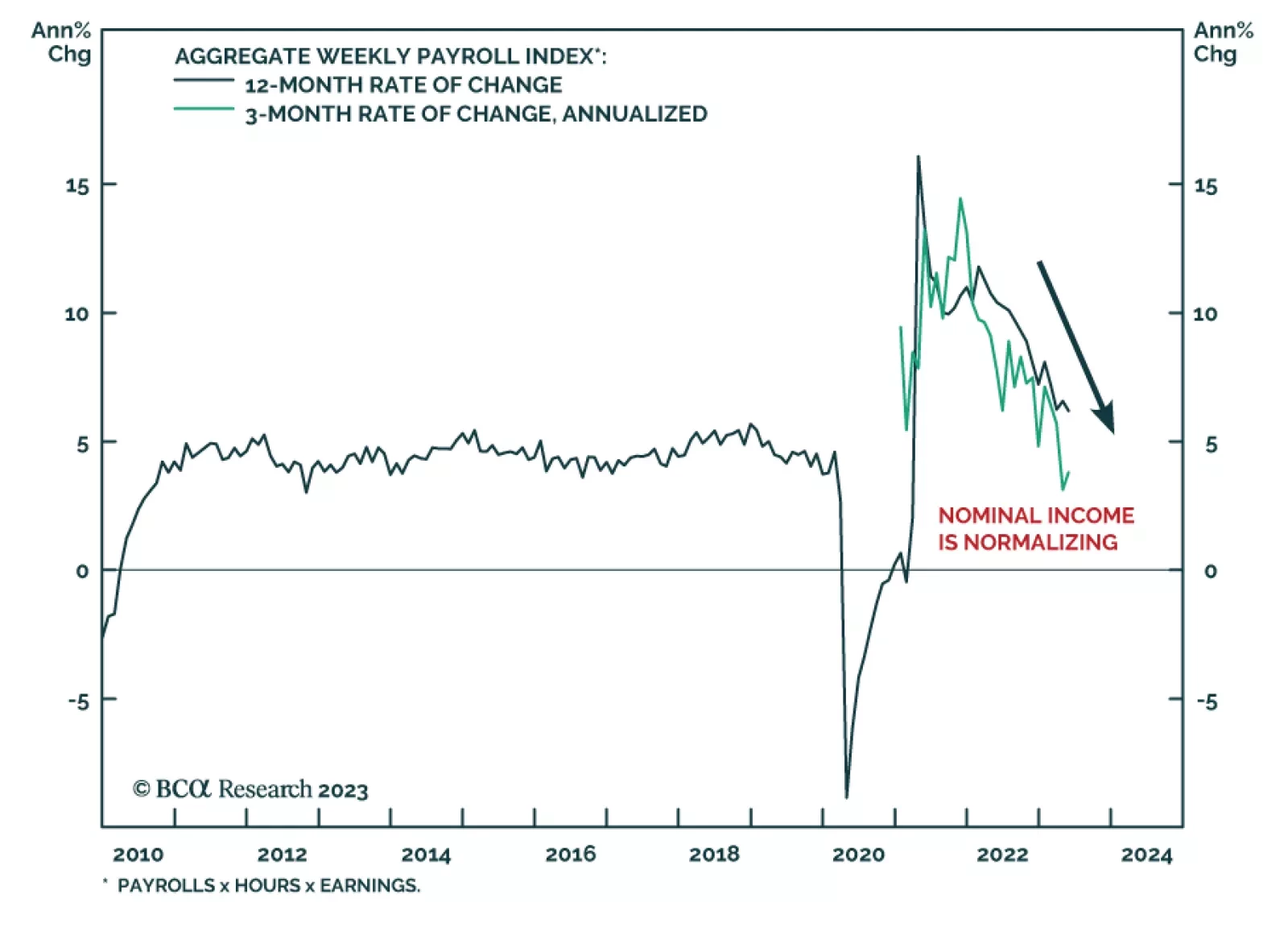

The consumption outlook remains solid thanks to households’ sizable excess savings, incomes that will be boosted by a tight labor market and ample capacity to add debt to augment their buying power.

Financial commentators, politicians and policymakers have increasingly been blaming stubbornly high inflation on companies pursuing aggressive pricing strategies to boost earnings and margins. In this Special Report, we investigate the concept of “greedflation” – companies persistently raising prices faster than costs are increasing to pad profit margins - and see if the associated conclusions about corporate pricing power and inflation are borne out by the data in the US, euro area and UK.