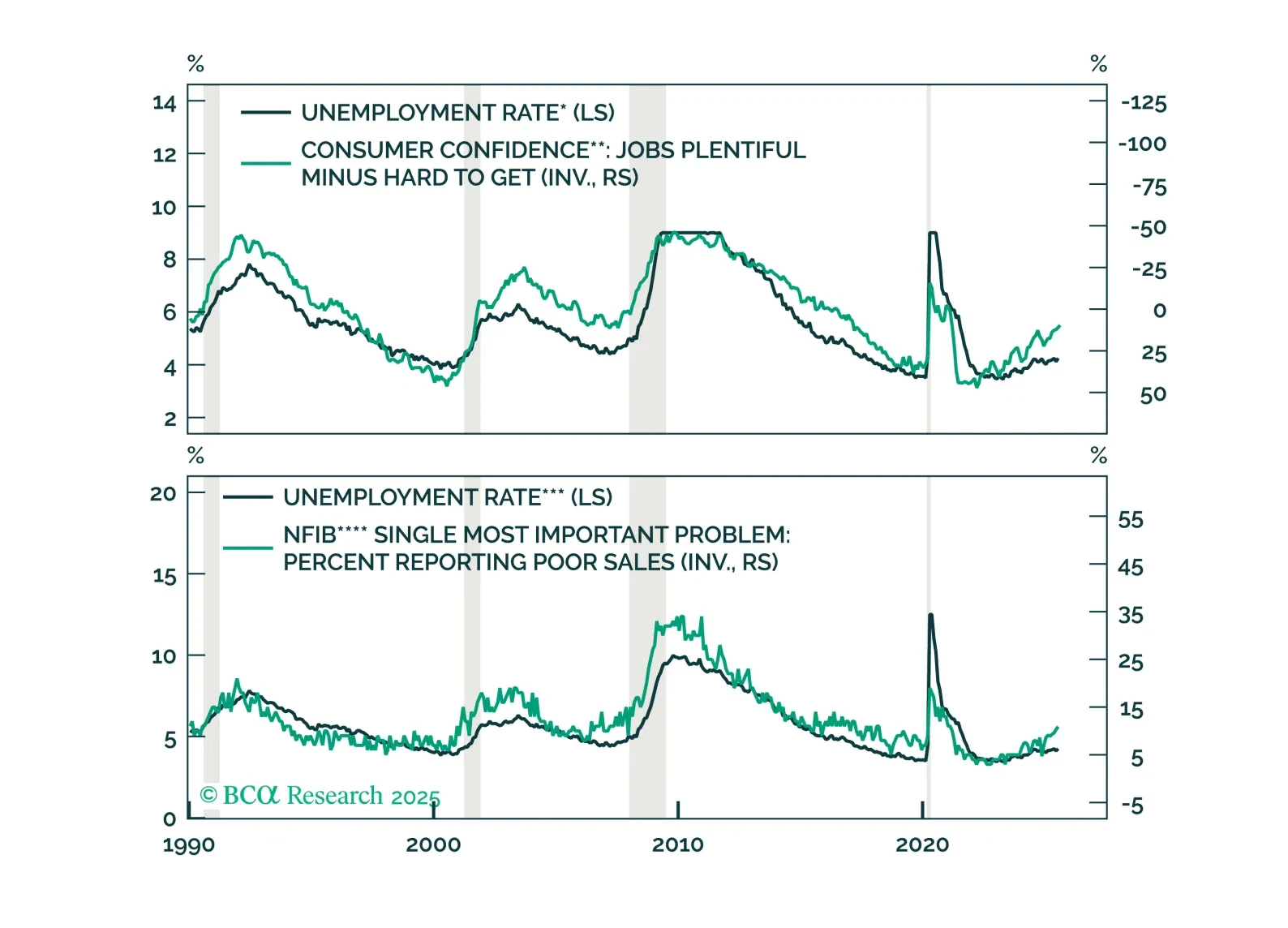

Labor Market

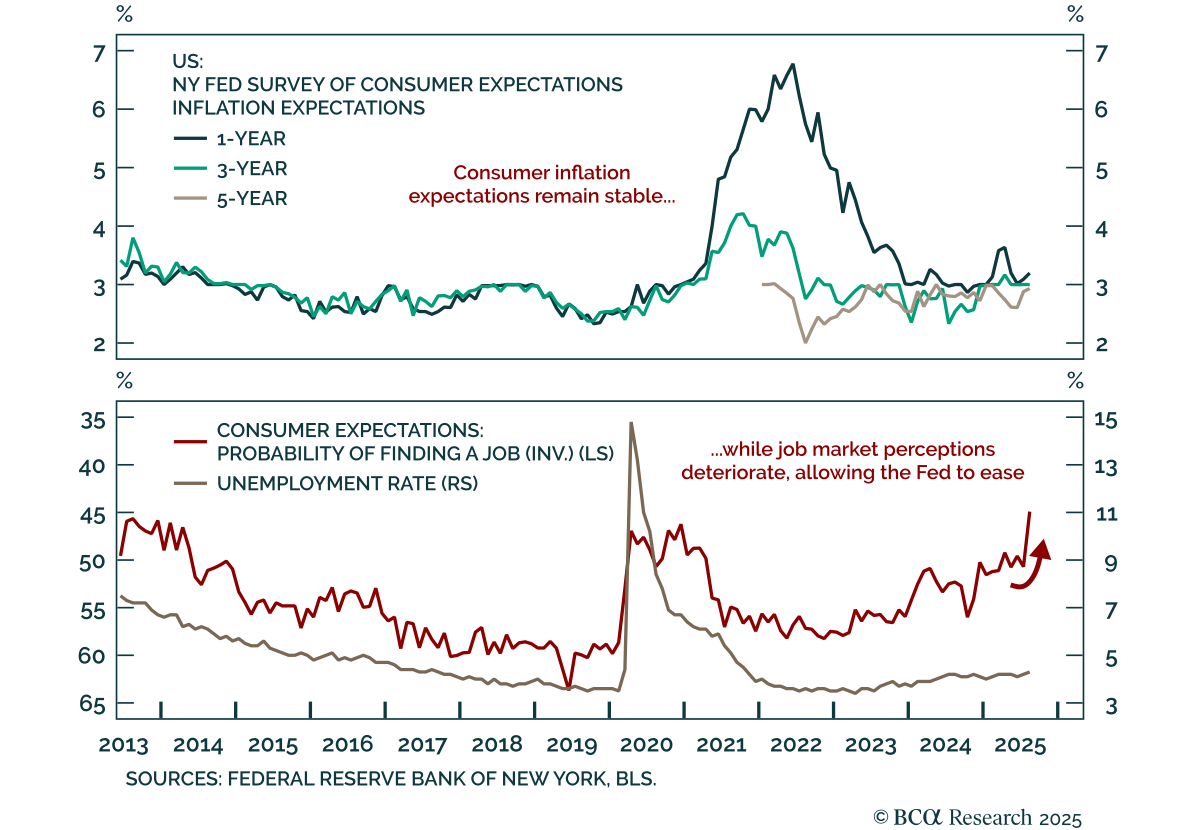

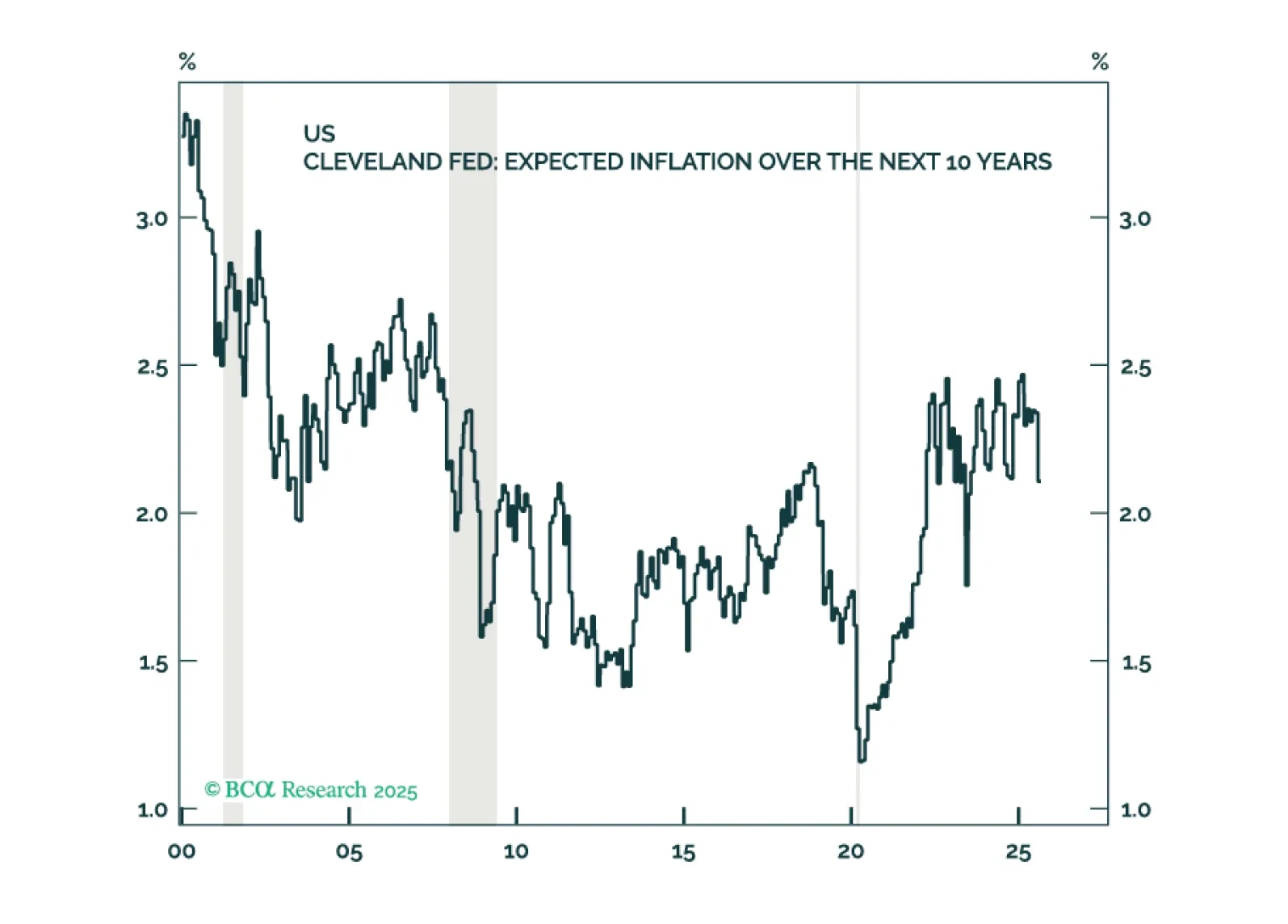

Stable long-term inflation expectations and weak labor perceptions support a defensive stance. The NY Fed Survey of Consumer Expectations showed 1-year inflation expectations ticking up to 3.2% in August, while the 3-year (3.0%) and 5-year (2.9%)…

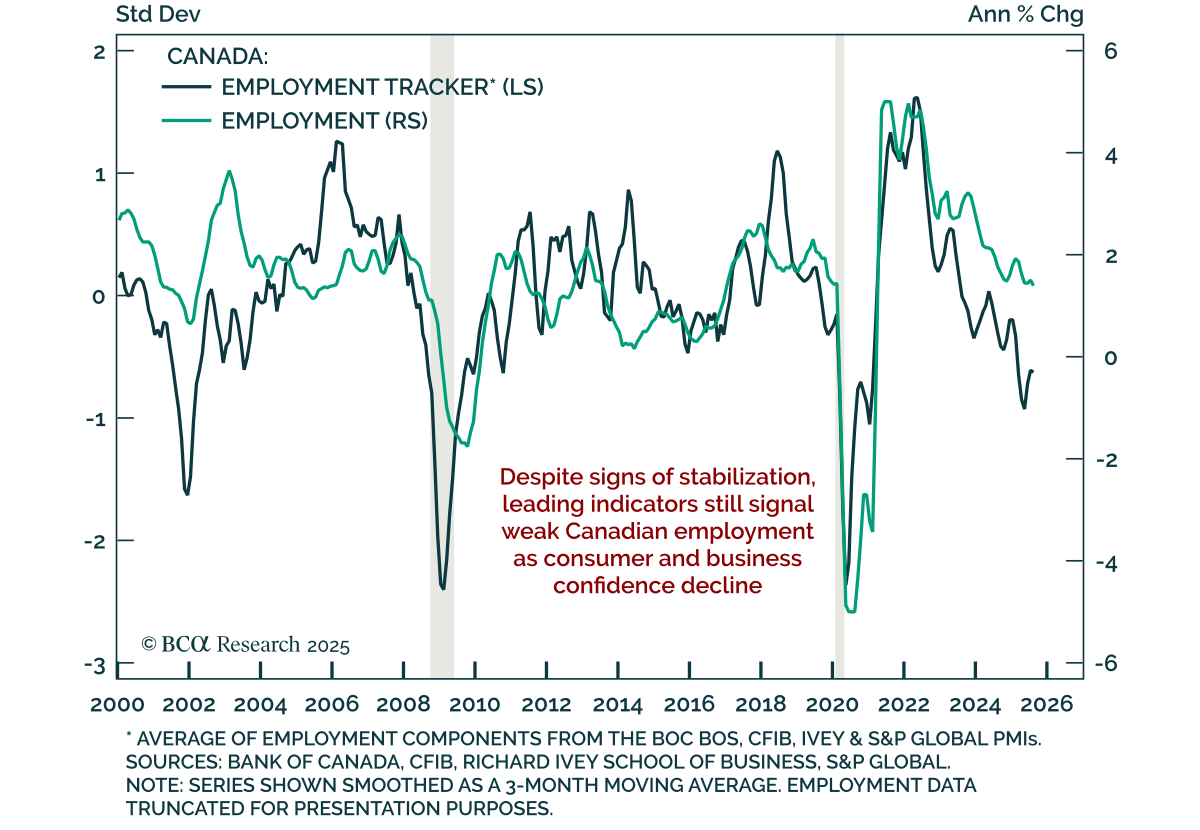

Canada’s August jobs report confirms the economy remains weak, supporting Canadian bonds and CAD steepeners. Employment fell by 66k, driven by declines in both part-time (-60k) and full-time (-6k) positions, against expectations for a modest gain. The…

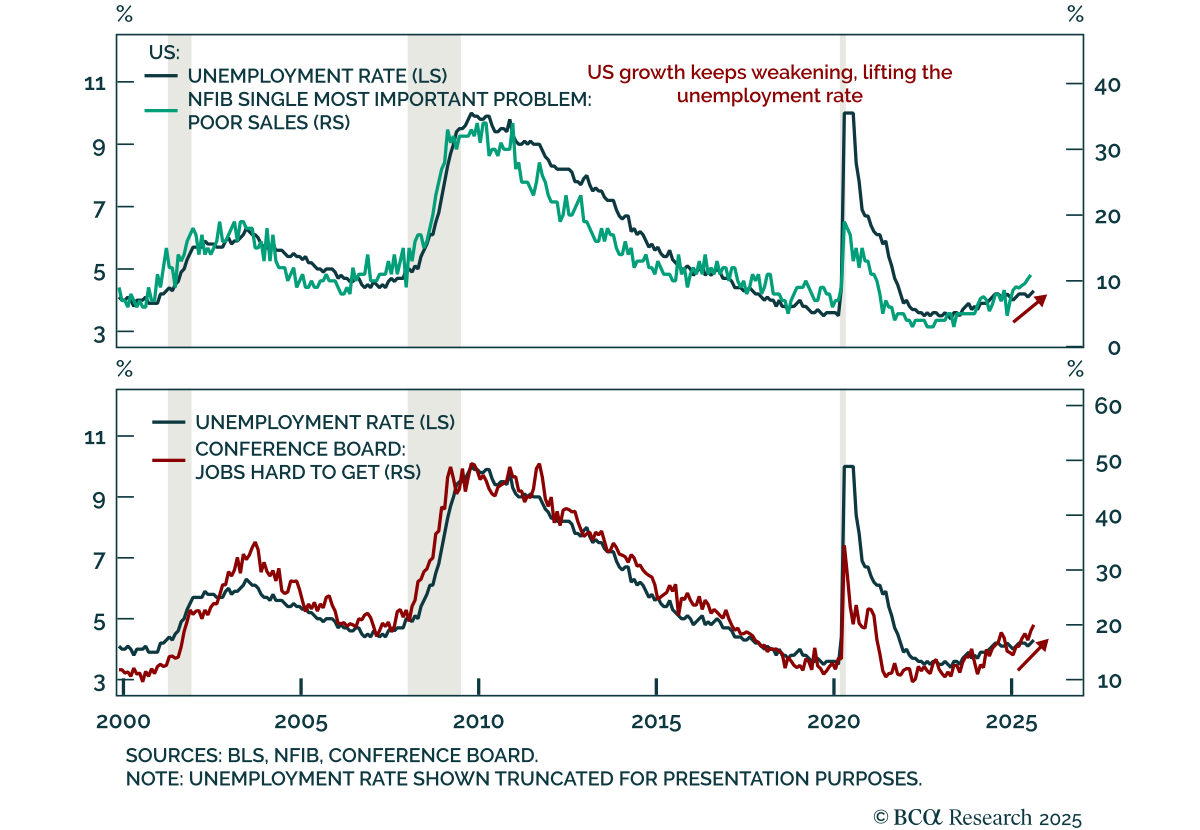

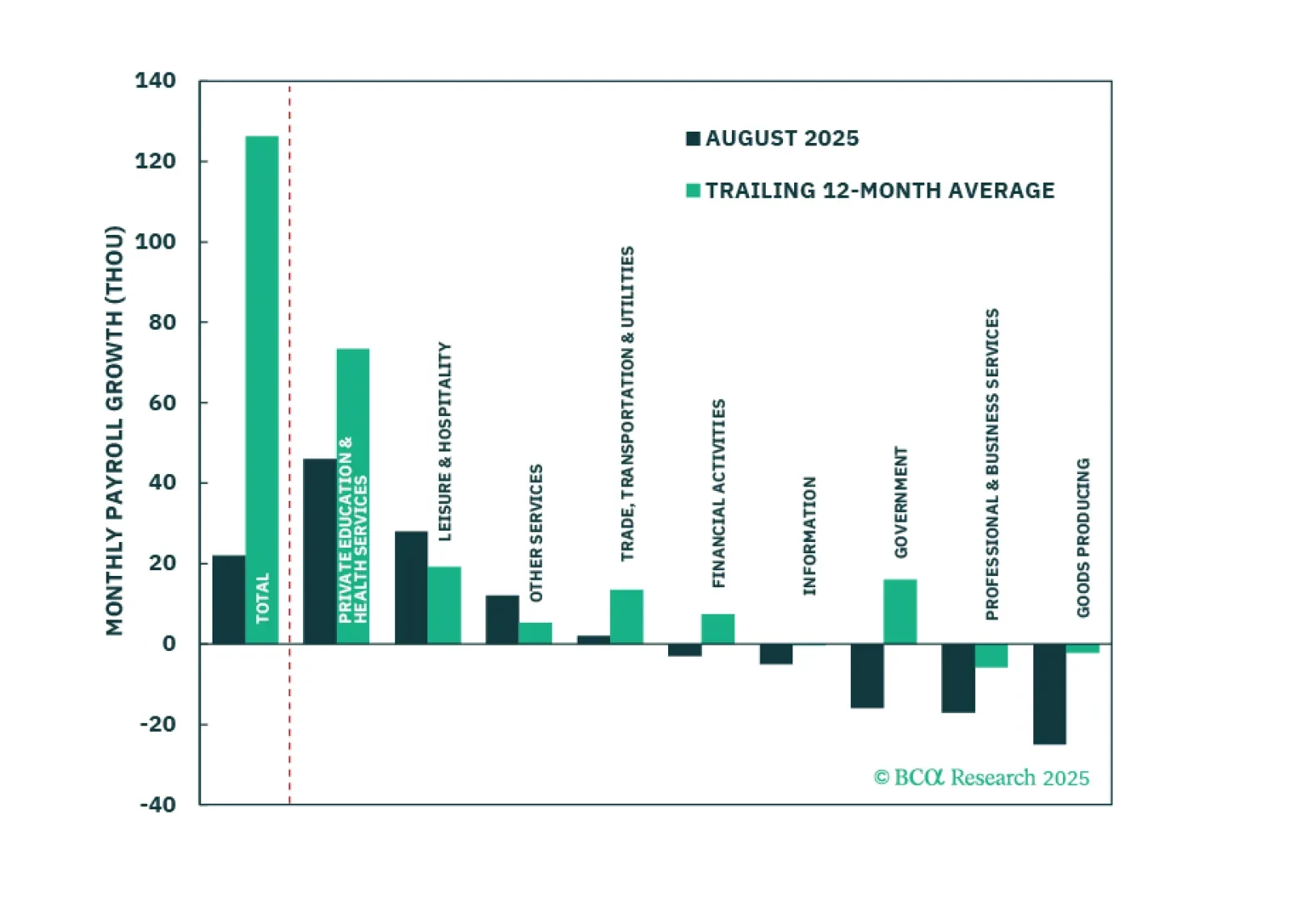

The August US employment report confirmed a significant labor market deceleration, keeping us modestly defensive. Nonfarm payrolls rose just 22k after 79k in July, while net revisions subtracted 21k from prior months. The 3-month average slowed to 29k,…

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.

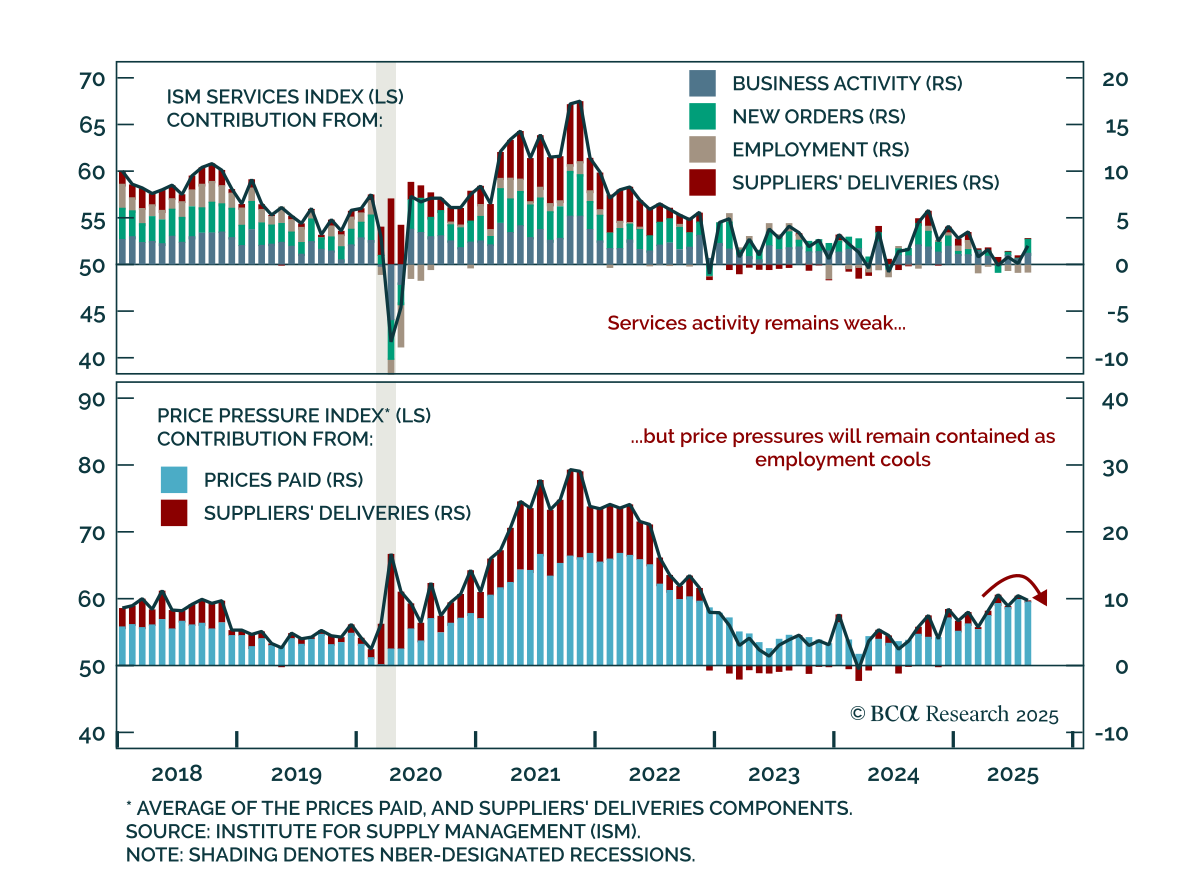

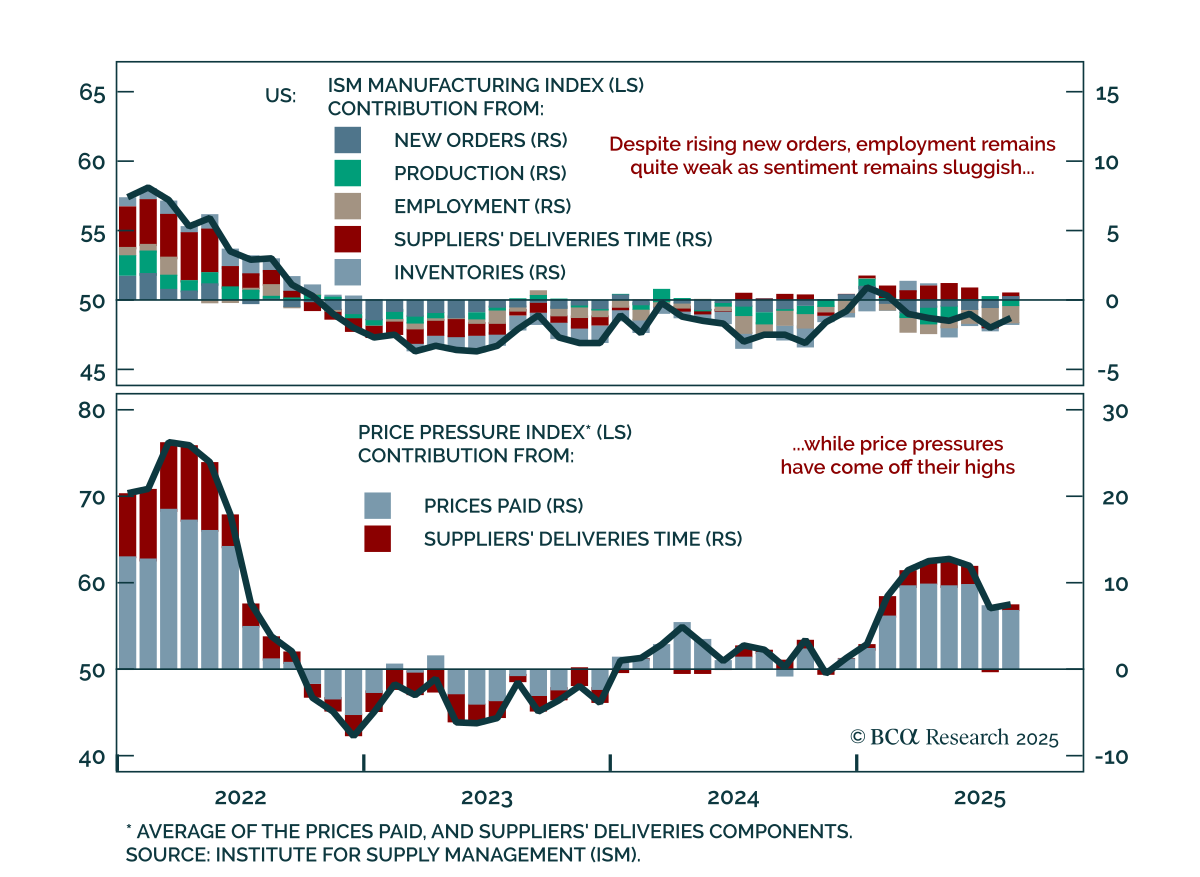

August ISM Services beat expectations, but employment weakness highlights fragile momentum. The index rose to 52.0 from 50.1, driven by business activity and new orders. However, the employment component stayed in contraction at 46.5. Inflation signals…

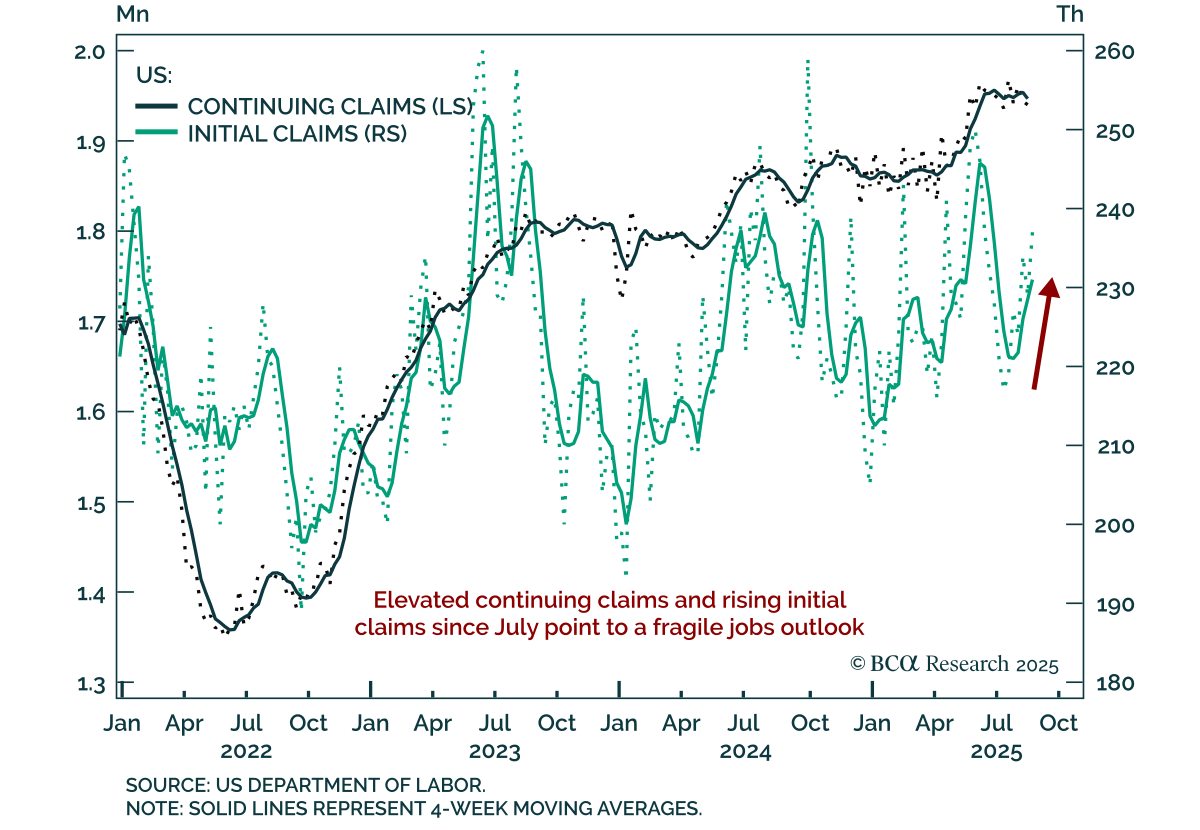

US jobless claims rose to 237k, the highest since July, underscoring fragile labor momentum. While still below the recent 250k peak, claims have been rising steadily since early July, suggesting the labor market weakness seen in the July employment…

US job openings fell to a 10-month low in July, underscoring continued labor market weakening. Openings declined to 7.18m from 7.36m. The decline was led by non-cyclical sectors such as education and health services, which had recently been drivers of…

Our Portfolio Allocation Summary for September 2025.

August ISM Manufacturing was mixed, with stronger orders offset by weak production and employment. The headline rose to 48.7 from 48.0, missing expectations. New orders beat estimates, rising into expansion at 51.4 and lifting the New…