Labor Market

Highlights Increasing consumption should be a lot easier than increasing savings. After all, most people like to spend! It is getting them to work that should be challenging. Yet, the conventional wisdom is that deflation is a much tougher problem to overcome than inflation. It is true that the zero-bound constraint on interest rates makes it more difficult for central banks to react to deflationary forces. However, monetary policy is not the only game in town; fiscal policy becomes more effective as interest rates fall because governments can stimulate the economy without incurring onerous financing costs. When the borrowing rate is below the growth rate of the economy, the more profligate a government has been in the past, the more profligate it can be in the future, while still maintaining a stable debt-to-GDP ratio. The pandemic banished the bond vigilantes. Governments ran massive budget deficits, but bond yields still dropped. While budget deficits will decline from their highs, fiscal policy will remain structurally more accommodative in the post-pandemic period. The combination of easier fiscal policy, increased household net worth, and other factors has raised the neutral rate of interest in the US and most other economies. This means that monetary policy is currently much more stimulative than widely believed. This is good news for equities and other risk assets in the near term, even if it does produce a major hangover down the road. New trade: Short US consumer discretionary stocks relative to other cyclicals. Consumer durable goods spending will slow as services spending and capex continue to recover. A Paradoxical Problem Economic pundits like to say that deflation is a tougher problem to overcome than inflation. We hear this statement so often that we do not think twice about it. In many respects, it is a rather strange perspective. Inflation results from too much spending relative to output, whereas deflation results from too little spending. Yet, people like to spend! One would think it would be much easier to get people to consume than to get them to work. The claim that deflation is a bigger problem than inflation is really just a statement about the limits of monetary policy. If the economy is overheating, central banks can theoretically raise rates as high as they want. In contrast, if the economy is in a deflationary funk, the zero-bound constraint limits how far interest rates can fall. Fortunately, there are other ways of stimulating the economy when interest rates cannot be cut any further. Most notably, governments can utilize fiscal policy by cutting taxes, spending more on goods and services, or increasing transfer payments. Getting Paid To Eat Lunch When interest rates are very low, not only is fiscal stimulus a free lunch, but you actually get paid for eating more. If the borrowing rate is below the growth rate of the economy, the more profligate a government has been in the past, the more profligate it can be in the future, while still maintaining a stable debt-to-GDP ratio. This sounds so counterintuitive that it is worth thinking through a simple example. Suppose you currently earn $100,000 per year and expect your income to rise by 8% per year. You have $100,000 in debt, which incurs an interest rate of 3%, and want to keep your debt-to-income ratio constant at 100% over time. Next year, your income will be $108,000, so you should target a debt level of $108,000. Thus, this year, you can spend $105,000 on goods and services, make $3,000 in interest payments, and take on $8,000 in additional debt. Now, suppose you have been spendthrift in the past and have accumulated $200,000 in debt. You still want to keep your debt-to-income ratio constant, but this time at 200%. How much can you spend this year? The answer is $110,000. If you spend $110,000 and pay an additional $6,000 in interest, your cash outflows will exceed your income by $16,000, taking your debt to $216,000 — exactly twice next year’s income. Notice that by maintaining a higher debt balance, you can actually spend $5,000 more while still keeping your debt-to-income ratio constant. Appendix A proves this point mathematically. One might protest that the interest rate you face would be higher if you had more debt. Fair enough, although in our example, the interest rate would need to rise above 5.5% for spending to decline. The more important point is that unlike people, governments which issue debt in their own currencies get to choose whatever interest rate they want. Granted, if central banks set interest rates too low, the economy will overheat, leading to higher inflation. But this just reinforces the point we made at the outset, which is that inflation and not deflation is the real constraint to macroeconomic policy. A Blissful Outcome For Stocks We would not have waded through this theoretical discussion if it did not serve a practical purpose. In April of last year, we wrote a controversial report asking if, paradoxically, the pandemic could turn out to be good for stocks.

Chart 1

We noted that by combining monetary easing with fiscal stimulus, policymakers could steer equity markets towards a “blissful outcome” where the economy was operating at full capacity, yet interest rates were lower than they were before (Chart 1). If such a blissful state were reached, earnings would return to their pre-pandemic level, but the discount rate would remain below its pre-pandemic level, thus allowing stock prices to rise above their pre-pandemic peak. In the months following our report, the stock market played out this narrative. From Blissful To Blissless? Chart 2Both The Fed And Investors Have Lowered Their Estimate Of The Neutral Rate

Both The Fed And Investors Have Lowered Their Estimate Of The Neutral Rate

Both The Fed And Investors Have Lowered Their Estimate Of The Neutral Rate

More recently, bond yields have risen, stoking fears that we are moving towards less auspicious conditions for equities. There is no doubt that many central banks are looking to normalize monetary policy. That said, what central banks regard as normal today is very different from what they thought was normal in the past. Back in 2012, when the Fed began publishing its “dot plot,” the FOMC thought the neutral rate of interest was around 4.25%. Today, it thinks the neutral rate is only 2.5%. And based on the New York Fed’s survey of market participants and primary dealers, investors believe the neutral rate is even lower than the Fed’s estimate (Chart 2). Even if the Fed did not face political pressure to keep interest rates low, it probably would not want to raise them all that much anyway. The same applies to most other central banks. Why The Neutral Rate Is Higher Than The Fed Believes There are at least four reasons to think that the neutral rate of interest is higher than what the Fed believes: Reason #1: The drag on growth from the household deleveraging cycle is ending As a share of disposable income, US household debt has declined by nearly 40 percentage points since 2008. Debt-servicing costs are now at record low levels (Chart 3). The Fed’s Senior Loan Officer Survey points to an increasing willingness to lend (Chart 4). The Conference Board’s Leading Credit Index also remains in easing territory (Chart 5). Chart 3The Deleveraging Cycle Has Run Its Course

The Deleveraging Cycle Has Run Its Course

The Deleveraging Cycle Has Run Its Course

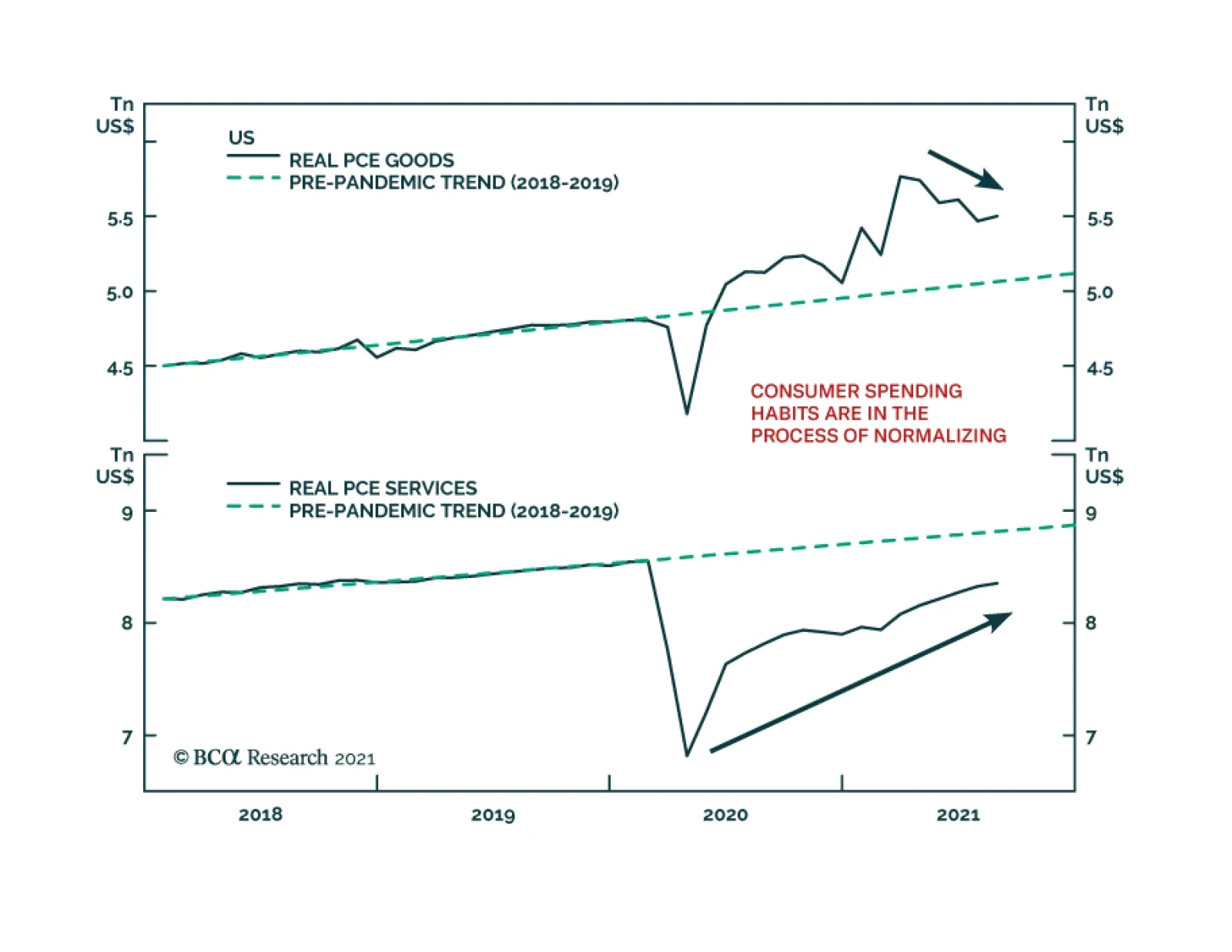

Real personal consumption increased by only 1.6% in Q3. However, this was largely driven by a 54% drop in auto spending on the back of the semiconductor shortage. While vehicle purchases normally account for only 4% of consumer spending, the sector still managed to shave 2.4 percentage points off GDP growth in Q3. Chart 4Banks Are Easing Credit Standards

Banks Are Easing Credit Standards

Banks Are Easing Credit Standards

Chart 5A Positive Signal For Credit Growth

A Positive Signal For Credit Growth

A Positive Signal For Credit Growth

Spending on services rose by 7.9%, an impressive feat considering the quarter saw the peak in the Delta variant wave. Reason #2: Fiscal policy is likely to remain accommodative in the post-pandemic period The combination of lower real rates and higher debt levels has increased the budget deficit consistent with a stable debt-to-GDP ratio in the US and most developed markets (Chart 6). This point has not been lost on governments. While the flow of red ink will abate, the IMF estimates that the US cyclically-adjusted primary budget deficit will be 3% of GDP larger in 2022-26 than it was in 2014-19. The IMF also expects most other advanced economies to run larger budget deficits (Chart 7).

Chart 6

Chart 7

Chart 8A Record Rise In Household Net Worth

A Record Rise In Household Net Worth

A Record Rise In Household Net Worth

Reason #3: Higher asset prices will bolster spending According to the Federal Reserve, US household net worth rose by over 113% of GDP between 2019Q4 and 2021Q2, the largest six-quarter increase on record (Chart 8). Empirical estimates of the wealth effect suggest that households spend about 5-to-8 cents on goods and services for every additional dollar of housing wealth, and 2-to-4 cents for every additional dollar of equity wealth. Based on the latest available data, we estimate that US homeowner equity has increased by $5 trillion since the start of 2020, while household equity holdings have increased by $15.8 trillion. Together, this would translate into 2.5%-to-4% of GDP in additional annual consumption. And this does not even include any spending arising from the $2.4 trillion in incremental bank deposits that households have amassed since the start of the pandemic. Chart 9Most Of The Deceleration In US Potential Real GDP Growth Has Already Occurred

Most Of The Deceleration In US Potential Real GDP Growth Has Already Occurred

Most Of The Deceleration In US Potential Real GDP Growth Has Already Occurred

Reason #4: Population aging will drain savings Aging populations can affect the neutral rate either by dragging down investment demand or reducing savings. The former would lead to a lower neutral rate, while the latter would lead to a higher rate. As Chart 9 shows, most of the decline in US potential GDP growth has already occurred. According to the Congressional Budget Office, real potential GDP growth fell from over 3% in the early 1980s to about 1.8% today, mainly due to slower labor force growth. The CBO expects potential growth to edge down to 1.5% over the next few decades. The average age of the US capital stock is now the highest on record (Chart 10). Whereas real business fixed investment is 6% below its pre-pandemic trend, core capital goods orders – a leading indicator for capex – are 17% above trend. Capex intentions remain near multi-year highs (Chart 11). All this suggests that investment spending is unlikely to fall much in the future. Chart 10The Average Age Of The US Capital Stock Is Now The Highest On Record

The Average Age Of The US Capital Stock Is Now The Highest On Record

The Average Age Of The US Capital Stock Is Now The Highest On Record

Chart 11Capex Intentions Remain At Lofty Levels

Capex Intentions Remain At Lofty Levels

Capex Intentions Remain At Lofty Levels

Chart 12

In contrast, the depletion of national savings from an aging population is just beginning. Baby boomers are leaving the labor force en masse. They hold over half of US household wealth, considerably more than younger generations (Chart 12). As baby boomers transition from net savers to net dissavers, national savings will fall. UnTaylored Monetary Policy The Taylor Rule prescribes the Fed to hike rates by between 50-to-100 bps for each percentage point that output rises relative to its potential. Over the past decade, the Fed has favored the higher output gap coefficient, meaning that a permanent one percentage-point increase in aggregate demand should translate, all things equal, into a one percentage-point increase in the neutral rate of interest. Taken at face value, the combination of increased household wealth and looser fiscal policy may have raised the neutral rate in the US by more than five percentage points since the pandemic. This estimate, however, does not consider feedback loops: A higher term structure for interest rates would depress asset prices, thus obviating some of the wealth effect. Higher rates would also reduce the incentive for governments to run large budget deficits. Taking these feedback loops into account, a reasonable estimate is that the neutral rate in the US is about 2% in real terms, or slightly over 4% in nominal terms based on current long-term inflation expectations. This is close to the historic average for real rates, although well above current market pricing. The implication for investors is that US monetary policy is currently more stimulative than widely believed. This is the good news. The bad news is that in the absence of fiscal tightening, the Fed will eventually be forced to raise rates by more than investors are discounting. Higher Inflation Won’t Force The Fed’s Hand… Just Yet When will the Fed be forced to move away from its baby-step approach to monetary policy normalization and adopt a more aggressive stance? Our guess is not for another two years. Last week, we argued that inflation in the US and many other countries is likely to follow a “two steps up, one step down” trajectory of higher highs and higher lows over the remainder of the decade. We are currently near the top of those two steps: Most of the recent increase in inflation has been driven by surging durable goods prices (Chart 13). Considering that durable goods prices usually fall over time, this is not a sustainable source of inflation. Chart 13ADurable Goods Spending Has Further To Fall (I)

Durable Goods Spending Has Further To Fall (I)

Durable Goods Spending Has Further To Fall (I)

Chart 13BDurable Goods Spending Has Further To Fall (II)

Durable Goods Spending Has Further To Fall (II)

Durable Goods Spending Has Further To Fall (II)

In modern service-based economies, structurally high inflation requires rapid wage growth. While US wage growth has picked up recently, most of the increase in wages has occurred at the bottom end of the income distribution (Chart 14). The Fed welcomes this development, given its expanded mandate to pursue “inclusive growth.” At some point in the future, long-term inflation expectations could become unmoored. However, that has not happened yet, whether one looks at market-based or survey-based expectations (Chart 15). Thus, for now, investors should remain constructive on stocks. Chart 14Wages At The Bottom End Of The Income Distribution Are Rising Briskly

Wages At The Bottom End Of The Income Distribution Are Rising Briskly

Wages At The Bottom End Of The Income Distribution Are Rising Briskly

Chart 15

New Trade: Short Consumer Discretionary Stocks Relative To Other Cyclicals We continue to favor cyclical stocks over defensives. Within the cyclical category, however, we are cautious on consumer discretionary names. Spending on consumer durable goods still has further to fall in order to return to trend. Durable goods prices will also come down, potentially squeezing profit margins. Go short the Consumer Discretionary Select Sector SPDR Fund (XLY) versus an S&P 500 sector-weighted basket of the Industrial Select Sector SPDR Fund (XLI), the Energy Select Sector SPDR Fund (XLE), and the Materials Select Sector SPDR Fund (XLB). Appendix A

Image

Peter Berezin Chief Global Strategist pberezin@bcaresearch.com View Matrix

Image

Special Trade Recommendations This table provides trade recommendations that may not be adequately represented in the matrix on the preceding page.

Image

Current MacroQuant Model Scores

Image

Highlights Bank of Canada: Rising inflation, high capacity utilization, and monetary policy constraints will force the Bank of Canada to taper further and move up the timing of its first rate hike to H1/2022. Stay underweight Canadian government bonds in global government bond portfolios. Also, upgrade Canadian real return bonds to neutral within the underweight allocation to better reflect the mixed signals from our suite of Canadian inflation breakeven indicators. Bank of England: Markets have aggressively shifted UK interest rate expectations, with a rate hike now expected before year-end. We expect that outcome to occur, but the vote will be close. Stay underweight UK Gilts in global bond portfolios. Maintain a curve steepening bias that would win if a hike is delayed to 2022 or, counterintuitively, even if the Bank of England does indeed hike in November or December - longer-term UK yields are still too low relative to the likely peak in Bank Rate. Feature Chart of the WeekAn Inflation Shock For Bond Yields

An Inflation Shock For Bond Yields

An Inflation Shock For Bond Yields

Steadily climbing inflation expectations, fueled by rising energy prices and persistent supply-chain disruptions, remain a thorn in the side of global bond markets. 10-year US TIPS breakevens have climbed to a 15-year high of 2.7%, while breakevens on 10-year German inflation-linked bonds are at a 9-year high of 2%. Rising inflation expectations are keeping upward pressure on nominal bond yields in the major developed economies, as markets start to slowly reprice the pace and timing of future interest rate increases (Chart of the Week). Market expectations on interest rates, however, can adjust much more quickly when policymakers change their tune. We have already seen that recently in smaller countries like Norway and New Zealand. Rate hikes delivered by the Norges Bank and Reserve Bank of New Zealand over the past month - which were telegraphed well in advance by the central banks – were a negative shock that pushed up bond yields in those countries. The next central bank “liftoff” within the developed economies is expected to occur in the UK and Canada, according to pricing in overnight index swap (OIS) curves (Table 1). In this report, we consider the outlook for monetary policy and government bond yields in both countries, which represent two of our highest conviction underweight recommendations. Table 1Markets Are Pulling Forward Rate Hikes

UK & Canada: Next Up For A Rate Hike?

UK & Canada: Next Up For A Rate Hike?

Canada: Watch For A Bond Bearish Policy Shift In Canada, given the economic backdrop and policy constraints, we believe the Bank of Canada (BoC) will have to deliver on the hawkish market-implied path for interest rates, which calls for an initial rate hike to occur in Q2/2022 – much sooner than the central bank’s current messaging on liftoff. Chart 2ACanadian Inflation Not Looking So "Transitory" Anymore

Canadian Inflation Not Looking So 'Transitory' Anymore

Canadian Inflation Not Looking So 'Transitory' Anymore

First on the BoC’s mind is inflation. Canadian CPI inflation came in at 4.4% year-over-year in September, blowing through analyst expectations and hitting an 18-year high (Charts 2A and 2B). The CPI-trim, a measure of core inflation which strips out extreme price movements, hit 3.4% year-over-year, the highest reading since 1991. All eight major components of the CPI rose on a yearly basis. On an annualized monthly basis, the energy-driven Transportation aggregate declined and less volatile components like Shelter (+1.1%) and Clothing (+0.7%) led the pack in terms of their contribution to the overall figure.

Chart 2

The data show that inflationary pressures are clearly broadening out in the Great White North, no longer constrained to “transitory” sectors. The effect of this inflationary pressure is also starting to make its mark on consumer and business sentiment. Chart 3Rising Inflation Expectations Are Hurting Canadian Consumer Sentiment

Rising Inflation Expectations Are Hurting Canadian Consumer Sentiment

Rising Inflation Expectations Are Hurting Canadian Consumer Sentiment

According to the BoC Survey of Consumer Expectations, the 1-year-ahead forecast of inflation reached a series high of 3.7% in Q3/2021 (Chart 3). While longer-term inflation expectations are more subdued, that doesn’t mean that inflation is not a worry for the Canadian consumer. With inflation expected to run much higher than expected wage growth (+2%) over the next year, consumers expect a decline in their real purchasing power. Correspondingly, consumer confidence is taking a hit—the Bloomberg/Nanos consumer sentiment index has fallen 7.3 points since the July peak. Canadian businesses are much more upbeat. The overall summary indicator from the BoC’s Business Outlook Survey for Q3/2021 climbed to the highest level in the 18-year history of the series (Chart 4). Firms reported continued expectations of strong demand, but with capacity constraints starting to weigh on sales - a quarter of firms surveyed reporting that a lack of capacity and skills will have a negative impact on sales over the next twelve months. In response, more companies are planning on increasing capital expenditure and hiring over the next year (Chart 4, middle panel). More than half of firms surveyed by the BoC indicated that investment spending will be higher over the next two years compared to typical pre-pandemic levels. Chart 4Canadian Businesses Are Brushing Up Against Capacity Constraints

Canadian Businesses Are Brushing Up Against Capacity Constraints

Canadian Businesses Are Brushing Up Against Capacity Constraints

However, hiring plans will likely face difficulty, given the large share of firms (64%), reporting more intense labor shortages (Chart 4, bottom panel). A net 50% of respondents now expect wage growth to accelerate over the coming year, driven by a need to attract and retain workers amid strong labor demand. With regards to inflation, the BoC Business Outlook Survey measures the share of respondents that expect inflation over the next two years to fall within four different ranges—below 1%, between 1% and 2%, between 2% and 3%, and above 3% (Chart 5). We can “back out” a point estimate of expected inflation for Canadian firms by assigning a specific level to each of these ranges – 0.5, 1.5%, 2.5%, and 3.5%, respectively – and using the shares of respondents to calculate a weighted average expected inflation rate for the next two years.1 Based on this estimate, Canadian business inflation expectations have bounced rapidly since the 2020 trough and are now at all-time highs. The BoC has already begun to respond to the normalization of the economy and rising inflationary pressures indicated by its business survey by tapering the pace of its bond buying program. The Bank is now targeting weekly bond purchases of C$2bn, down from C$5bn at the start of the program and with another reduction expected at this week’s policy meeting (Chart 6). The size of the balance sheet has also fallen in absolute terms, driven by the Bank drawing down its holdings of treasury bills to virtually zero while also ending pandemic emergency liquidity programs. Chart 5Putting A Number To Canadian Business Inflation Expectations

Putting a Number To Canadian Business Inflation Expectations

Putting a Number To Canadian Business Inflation Expectations

Chart 6The BoC Is Moving Towards Normalizing Policy

The BoC Is Moving Towards Normalizing Policy

The BoC Is Moving Towards Normalizing Policy

The BoC now owns a massive 36.5% of Canadian government bonds outstanding – a share acquired in a very short time for this pandemic-era stimulus program. Thus, tapering now is not only necessary from a forward guidance perspective, signaling an eventual shift to less accommodative monetary policy and rate hikes, but also to ensure liquidity in the Canadian sovereign bond market. The remaining BoC tapering will be fairly quick, setting up the more important shift to the timing of the first rate increase. The Canadian OIS curve is currently pricing in BoC liftoff in April 2022, ahead of the BoC’s current guidance of a likely rate hike in the second half of the year (Chart 7). Given the developments on the inflation front, we are inclined to side with the market’s assessment of an earlier hike.

Chart 7

In the longer run, rates might even be able to rise further than discounted in swap curves. The real policy rate, calculated as the policy rate minus the BoC’s CPI-trim measure, is negative and a significant distance from the New York Fed’s Q2/2020 estimate of the natural real rate of interest (R-star) for Canada of 1.4%. Admittedly, those estimates have not been updated by the New York Fed for over a year, given the uncertainties over trend growth and output gap measurement created by the pandemic shock. The BoC’s own estimates for the neutral nominal policy interest rate - last updated in April 2021 and therefore inclusive of any structural impacts of the pandemic on potential growth - range from 1.75% to 2.75%.2 The OIS forward curve expects the BoC to only lift rates to 2% in the next hiking cycle, barely in the lower end of the BoC’s neutral range of estimates. After subtracting the mid-point of the BoC’s 1-3% inflation target, presumably a level of inflation consistent with a neutral policy rate, the BoC’s implied real policy rate range is -0.25% to +0.75%. The current level of the real policy rate is near the bottom of that range. Thus, real rates, and the real bond yields that track them over time, have room to rise if the BoC begins to hike rates at a faster pace, and to a higher level, than the market expects. We see this as a likely outcome given the extent of the Canadian inflation overshoot and the robust optimism evident in Canadian business sentiment, thus justifying our current negative view on Canadian government bonds. To think about this mix of rising inflation expectations and increased BoC hawkishness down the road, and its implication for the Canadian inflation-linked bond market, we turn to our Canadian comprehensive breakeven indicator (Chart 8). This indicator combines three measures, on an equal-weighted and standardized basis, to determine the upside potential for 10-year inflation breakevens: the distance from fair value based on our models, the spread between headline inflation and the midpoint of the BoC’s 1-3% target inflation, and the gap between market-based and survey-based measures of inflation expectations. Going forward, we will be using the Canadian Business Outlook Survey measure of inflation expectations, introduced in Chart 5, for this indicator. Chart 8Upgrade Canadian Inflation-Linked Bonds To Neutral

Upgrade Canadian Inflation-Linked Bonds To Neutral

Upgrade Canadian Inflation-Linked Bonds To Neutral

Two out of three measures point towards Canadian breakevens having further upside. Firstly, they are cheap under our fair value model, where the rise in breakevens has lagged the yearly growth in oil prices. Secondly, breakevens are a long distance away from the survey-based business inflation expectations. However, both forces are more than counteracted with Canadian headline inflation nearly two standard deviations from the BoC’s target, which indicates that the central bank must step in to address high realized inflation. Given these diverging signals on the upside potential for breakevens, we see a neutral allocation to Canadian linkers as more appropriate for the time being Bottom Line: Rising inflation, high capacity utilization, and monetary policy constraints will force the Bank of Canada to taper further and move up the timing of its first rate hike to H1/2022. Stay underweight Canadian government bonds in global government bond portfolios. Also, upgrade Canadian real return bonds to neutral within the underweight allocation to better reflect the mixed signals from our suite of Canadian inflation breakeven indicators. Will The BoE Actually Hike By December? Chart 9UK Gilts Have Been Hammered By BoE Hawkishness

UK Gilts Have Been Hammered By BoE Hawkishness

UK Gilts Have Been Hammered By BoE Hawkishness

We downgraded our recommended stance on UK government bonds to underweight on August 11 and, since then, Gilts have severely underperformed their developed market peers (Chart 9).3 We had anticipated that the Bank of England (BoE) would be forced to shift their policy guidance in a less dovish direction because of rising UK inflation expectations. Yet we have been surprised by how quickly the BoE has shifted to an open discussion about the potential for imminent interest rate hikes. The BoE’s new chief economist, Huw Pill, commented in the Financial Times last week that UK inflation will likely hit, or even exceed, 5% by early next year, and that the November 4 Monetary Policy Committee (MPC) was “live” with regards to a potential rate hike.4 This followed BoE Governor Andrew Bailey’s comment that the Bank “will have to act” to contain rising inflation expectations. Mixed signals on economic momentum are not making the BoE’s decisions any easier. The preliminary October Markit PMIs ticked higher for both manufacturing and services, but remain below the peak seen last May. At the same time, UK consumer confidence has fallen since August, thanks in part to rapidly rising inflation that has reduced the perceived real buying power of UK consumers. High Inflation Might Last Longer Chart 10Why The BoE Is More Worried About Inflation

Why The BoE Is More Worried About Inflation

Why The BoE Is More Worried About Inflation

The BoE’s last set of economic forecasts, published in August, called for headline inflation to temporarily climb to 4% by year-end, before gradually returning to the central bank’s 2% target level in 2022. Yet the BoE’s newfound nervousness over inflation is well-founded, for a number of reasons (Chart 10): The domestic economic recovery has led to a robust labor market, with job vacancies relative to unemployment fully recovering to pre-COVID levels. The 3-month moving average of wage growth remains elevated at 6.9%, although the BoE believes some of that increase could be due to compositional issues related to the pandemic. The BoE is projecting that the UK output gap is narrowing rapidly and would be fully closed in the second half of 2022. This suggests growing underlying inflation pressures were already in place before the latest boost to inflation from global supply-chain disruptions. UK energy costs are soaring, particularly for natural gas which remains the main source for UK electricity production. UK natural gas inventories are the lowest within Europe, yet the supply response from major providers has been slow to develop – most notably, Russia, which is seeking regulatory approval to begin shipping gas through the Nord Stream 2 pipeline. While natural gas prices have stopped rising, for now, inadequate supplies during an expected cold UK winter could keep the upward pressure on UK inflation from energy. UK house price inflation remains well supported, even with the recent expiration of the stamp duty reductions initiated as a form of pandemic economic stimulus. According to the Royal Institution of Chartered Surveyors (RICS), the ratio of UK home sales to inventories is still quite elevated (bottom panel). Given a still-favorable demand/supply balance, and low borrowing costs, UK house price inflation will likely not cool as much as the BoE would prefer to see. Stay Defensive On UK Rates Exposure The combination of rising UK inflation and increasingly hawkish BoE comments has resulted in a rapid upward repricing of UK interest rate expectations over the past few months (Chart 11). Markets now expect the BoE to raise Bank Rate to 1%, from the current 0.1%, by late 2022. More interesting is what is discounted after that. The OIS curve is pricing in no additional rate increases in 2023 and a rate cut in 2024. In other words, the market now believes that the BoE is about to embark on a policy mistake with rate hikes that will need to be quickly reversed. Chart 11Markets Are Pricing In A BoE Policy Error

Markets Are Pricing In A BoE Policy Error

Markets Are Pricing In A BoE Policy Error

We think there is a risk of a more aggressive-than-expected BoE tightening cycle. The surge in UK inflation expectations is not trivial nor “transitory”. Looking at survey-based measures of expectations like the YouGov/Citigroup survey, or market-based measures like CPI swaps, inflation is expected to reach at least 4% both in the short-term and over the longer-run (Chart 12). If Bank Rate were to peak at a mere 1%, as indicated in the OIS curve, that would still leave UK real interest rates in deeply negative territory even if there was a pullback in inflation expectations. We expect the votes on whether to hike rates at either the November or December MPC meetings to be close. There will be a new Monetary Policy Report published for the November 4 meeting, which will include a new set of economic and inflation forecasts that will give the BoE a platform to signal, or deliver, a rate hike. In the end, we think that the senior leadership on the MPC has already revealed too much of its hawkish hand, and a rate hike will occur by year-end. Looking beyond liftoff into 2022, we still see markets pricing in too shallow a path for Bank Rate over the next couple of years, leaving us comfortable to maintain our underweight stance on UK Gilts. With regards to positioning along the Gilt yield curve, however, we see the potential for more curve steepening even if after the BoE begins to lift rates. The implied path for UK real interest rates, taken as the gap between the UK OIS forwards and CPI swap forwards, shows that markets expect the BoE to keep policy rates well below expected inflation for well into the next decade (Chart 13). At the same time, the wide current gap between the actual real policy rate (Bank Rate minus headline inflation) and the New York Fed’s most recent estimate of the UK neutral real rate (r-star) suggests that the Gilt curve is far too flat (bottom panel). Chart 12The BoE Cannot Ignore This

The BoE Cannot Ignore This

The BoE Cannot Ignore This

Perversely, this creates a situation where the UK curve steepeners can be an attractive near-term hedge to an underweight stance on UK Gilts.

Chart 13

If the BoE does not deliver on the strongly hinted rate hike in November or December, the Gilt curve can steepen as shorter-maturity Gilt yields fall but longer-dated yields remain boosted by high inflation expectations.However, if the BoE does hike and more tightening is signaled, longer-term yields will likely rise more than shorter-term yields as the market prices in a higher future trajectory for policy rates. Bottom Line: Stay underweight UK Gilts in global bond portfolios, but maintain a curve steepening bias that would win if a hike is delayed to 2022 or, counterintuitively, even if the Bank of England does indeed hike in November or December - longer-term UK yields are still too low relative to the likely peak in Bank Rate. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Shakti Sharma Senior Analyst ShaktiS@bcaresearch.com Ray Park, CFA Research Analyst ray@bcaresearch.com Footnotes 1 For this calculation, we exclude firms that did not provide a response to the BoC Business Outlook Survey. 2 The Bank of Canada’s Staff Analytical Note on neutral rate estimation can be found here: https://www.bankofcanada.ca/2021/04/staff-analytical-note-2021-6/ 3 Please see BCA Research Global Fixed Income Strategy and European Investment Strategy Report, "The UK Leads The Way", dated August 11, 2021, available at gfis.bcaresearch.com. 4https://www.ft.com/content/bce7b1c5-0272-480f-8630-85c477e7d69 Recommendations Duration Regional Allocation Spread Product Tactical Trades GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Image

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Highlights Treasuries: Bond investors should maintain below-benchmark portfolio duration and continue to short the 5-year note versus a duration-matched 2/10 barbell. For those investors who want to take an outright long position in US Treasuries, the 2-year Treasury note looks like the best security to choose. Municipal Bonds: This week we upgrade our recommended allocation to municipal bonds from overweight (4 out of 5) to maximum overweight (5 out of 5). Investors who can take advantage of the muni tax exemption should favor municipal bonds over Treasuries and over corporate bonds with the same credit rating and duration. In particular, we recommend that investors focus on long-maturity municipal bonds. Fed: Given our view that inflation will fall during the next 12 months, we still view December 2022 as the most likely liftoff date. However, we will continue to monitor our Five Factors For Fed Liftoff to see if our forecast needs to be revised. Feature

Chart 1

Our call for a bear-flattening of the US Treasury curve has worked out well during the past few weeks. Long-maturity Treasury yields have almost risen back to their March highs, and the short-end of the curve has also participated in the recent bout of selling (Chart 1). In light of these moves, it makes sense to re-evaluate our nominal Treasury curve positioning. First, we consider whether, at current yield levels, it still makes sense to run below-benchmark portfolio duration. Second, we consider whether our current recommended yield curve trade (short the 5-year note versus a duration-matched 2/10 barbell) remains the best way to extract returns from changes in the yield curve’s shape. The next section of this report answers these questions by looking at forecasted returns for different Treasury maturities across a variety of plausible economic and monetary policy scenarios. Later in the report we look at municipal bond valuation and provide a quick update on last week’s Fedspeak. Forecasting Treasury Returns

Chart 2

Three sources of Treasury bond return need to be considered when creating a forecast. Income Return: The return earned from the bond’s coupon payments. Rolldown Return: The return that a bond accrues simply by moving closer to its maturity date in an unchanged yield curve environment. Capital Gains/Losses: The return earned by a bond due to changes in the level and slope of the yield curve. We like to combine the income and rolldown return into one measure called “carry”. The carry can be thought of as the return an investor will earn in a specific bond if the yield curve remains unchanged throughout the investment horizon. Though carry is not the be all and end all of bond returns, it can be illuminating to look at the yield curve in terms of carry instead of the typical yield-to-maturity. Chart 2 shows the usual par coupon yield curve alongside the 12-month carry for each Treasury security. At present, the steepness of the 3-7 year part of the curve means that bonds of those maturities benefit a lot from rolldown. In fact, we see that a 7-year Treasury note will earn more than a 10-year Treasury note during the next 12 months if the curve remains unchanged. After calculating carry, the next step is to calculate capital gains/losses for each bond. To do this, we create some possible scenarios for future changes in the fed funds rate and assume that the yield curve moves to fully price-in that funds rate path over the course of a 12-month investment horizon.1 Next, we calculate the capital gains/losses for each bond based on the new shape of the yield curve in each scenario. Tables 1A-1D show the results from four different scenarios where the Fed starts to lift rates in December 2022. We then assume that the Fed will lift rates at a pace of 75-100 bps per year and that the funds rate will level-off at a terminal rate of either 2.08% or 2.58%. The 2.08% terminal rate corresponds to the median estimate of the long-run neutral fed funds rate from the New York Fed’s Survey of Market Participants. The 2.58% terminal rate corresponds to the median forecast from the Fed’s Summary of Economic Projections.2

Chart

Chart

Chart

Chart

The scenario shown in Table 1B is the closest to our base case. In this scenario, some short-maturity bonds deliver positive returns, but returns are negative for the 5-year maturity and beyond. Also, the 5-year note delivers the worst total return of all the maturities we examine. Unsurprisingly, expected returns for the longer maturities drop significantly if we raise our terminal rate assumption to 2.58% (Tables 1C & 1D). Therefore, any call to short the 5-year note versus the long-end relies on an assumption that the market will trade as though the terminal rate is closer to 2% than to 2.5% during the next 12 months. This is in line with our expectation. Finally, we observe that slowing our pace assumption from 100 bps per year to 75 bps raises expected returns across the board, but the 5-year still performs worse than the other maturities (Table 1A). Due to our expectation that inflation will fall during the next 12 months, a December 2022 liftoff remains our base case.3 However, the market has recently moved to price-in an earlier start to rate hikes. As of last Friday’s close, the fed funds futures curve was priced for liftoff in September 2022 and for a total of 49 bps of tightening by the end of 2022 (Chart 3). Chart 3Market Priced For September 2022 Liftoff

Market Priced For September 2022 Liftoff

Market Priced For September 2022 Liftoff

Tables 2A-2D incorporate these recent market moves into our forecast by looking at the same scenarios as in Tables 1A-1D but assuming a September 2022 liftoff instead of December. The results are not all that different. Expected returns are worse across the board, but the 5-year still looks like the worst spot on the curve unless the market starts to price-in a higher terminal rate.

Chart

Chart

Chart

Chart

Investment Conclusions Most of the scenarios we examined had negative expected returns for most maturities. We therefore still think it makes sense to keep portfolio duration low. Further, in every scenario the best expected returns can be found in the shorter maturities. In fact, the 2-year Treasury note offers positive returns in every scenario we examined. An outright long position in the 2-year Treasury note looks like a decent trade for investors forced to hold bonds. As for the yield curve, our results suggest that we should continue with our current positioning: short the 5-year note versus a duration-matched 2/10 barbell. The 5-year note performs worst in every scenario that assumes a 2.08% terminal rate. While it’s conceivable that investors will eventually push their terminal rate expectations higher, we think this is more likely to occur once the Fed has already lifted rates a few times. Bottom Line: Bond investors should maintain below-benchmark portfolio duration and continue to short the 5-year note versus a duration-matched 2/10 barbell. For those investors who want to take an outright long position in US Treasuries, the 2-year Treasury note looks like the best security to choose. The Duration Drift In Municipal Bond Valuations One under-discussed aspect of municipal bonds is that the securities tend to pay higher coupons than other bonds. That is, the bonds will often be issued with coupon rates well above prevailing yields. Investors therefore must pay a higher price to purchase the bonds, but they receive more return in the form of coupon payments. This feature of municipal bonds has important implications for how we should value them. For example, while the average maturity of the Municipal Bond index is much higher than the average maturity of the Treasury index, the muni index’s higher coupon rate makes its average duration significantly lower (Chart 4). This means that any valuation measure that compares a municipal bond’s yield with the yield of another bond with the same maturity will be unflattering for the muni. Chart 4Munis Pay High Coupons, Have Low Durations

Munis Pay High Coupons, Have Low Durations

Munis Pay High Coupons, Have Low Durations

Further, since Treasury securities and corporate bonds tend to issue at par, the coupon rates paid by those securities have fallen alongside yields during the past few decades. Meanwhile, municipal bond coupons have been relatively stable (Chart 4, panel 3). This means that, over time, municipal bond durations have fallen significantly compared to the durations of other US bond sectors. A fair valuation measure would compare municipal bond yields with equivalent-duration Treasury yields and that is exactly what we’ve done. Chart 5A shows the spread between General Obligation (GO) muni bond yields and equivalent-duration Treasury yields. Chart 5B shows the spreads expressed as percentile ranks. For example, a percentile rank of 50% means that the spread is at its historical median, a percentile rank of 10% means the spread has only been tighter 10% of the time. Chart 5AGO Muni/Treasury Spreads I

GO Muni/Treasury Spreads I

GO Muni/Treasury Spreads I

Chart 5BGO Muni/Treasury Spreads II

GO Muni/Treasury Spreads II

GO Muni/Treasury Spreads II

The first thing that jumps out from our analysis is that municipal bonds are not that expensive. Shorter-maturity spreads were tighter than current levels as recently as 2019/20 and the long-maturity (17-year+) spread is positive, despite the muni tax exemption. In terms of percentile rank, spreads for all GO maturity buckets are only just below the historical median. However, spreads traded much tighter prior to the 2008 financial crisis and it may not be reasonable to expect munis to return to those tight mid-2000 valuations. Charts 6A and 6B repeat the exercise from Charts 5A and 5B but for Revenue bonds instead of GOs. The message is similar. Muni valuations are not that stretched compared to history, and investors can earn a before-tax spread pick-up in munis versus Treasuries if they focus on the long maturities. Chart 6ARevenue Muni/Treasury Spreads I

Revenue Muni/Treasury Spreads I

Revenue Muni/Treasury Spreads I

Chart 6BRevenue Muni/Treasury Spreads II

Revenue Muni/Treasury Spreads II

Revenue Muni/Treasury Spreads II

In fact, municipal bonds offer a before-tax yield advantage versus Treasuries for Revenue bonds beyond the 12-year maturity point and for GO bonds beyond the 17-year maturity point. Further, the breakeven tax rate for 12-17 year GOs versus Treasuries is a mere 1% and the breakeven tax rate for 8-12 year Revenue bonds is only 8%. Investors facing a tax rate above the breakeven rate will earn an after-tax yield pick-up in munis versus duration-matched Treasuries (Table 3). Table 3Muni/Treasury And Muni/Credit Yield Ratios

The Best & Worst Spots On The Yield Curve

The Best & Worst Spots On The Yield Curve

Of course, municipal bonds also carry a small credit risk premium relative to duration-matched Treasuries. The GO and Revenue indexes have average credit ratings of Aa1/Aa2 and Aa3/A1, respectively, compared to a Aaa rating for US Treasuries. But we can control for credit risk as well by comparing municipal bonds to the US Credit Index and matching both the duration and credit rating. Even this comparison looks favorable for municipal bonds. Once again, long-maturity munis offer a before-tax yield advantage compared to credit rating and duration-matched US Credit. Meanwhile, breakeven tax rates for other maturities are low enough to attract most investors. Bottom Line: This week we upgrade our recommended allocation to municipal bonds from overweight (4 out of 5) to maximum overweight (5 out of 5). Investors who can take advantage of the muni tax exemption should favor municipal bonds over Treasuries and over corporate bonds with the same credit rating and duration. In particular, we recommend that investors focus on long-maturity municipal bonds, noting that the relatively low duration of these bonds makes them attractive relative to other bonds with similar risk profiles. Five Fed Factors A lot of Fedspeak hit the tape last week. Of particular interest were an interview with Chair Jay Powell on Friday and speeches by Fed Governors Randy Quarles and Chris Waller on Wednesday and Tuesday. One takeaway from their remarks is that a tapering announcement at the next FOMC meeting is very likely, with net asset purchases expected to hit zero by the middle of next year. The market, however, seems to have already taken the taper announcement on board. The more interesting aspects of the speeches were the discussions about how the Fed will decide when to lift rates and how elevated inflation readings may or may not influence that decision. We’ve noted in prior reports that five factors will determine when the Fed finally decides to lift rates, and last week’s comments gave us confidence that we’re on the right track. We run through our Five Factors For Fed Liftoff below, with some additional comments on why each factor is important (Table 4). Table 4Five Factors For Fed Liftoff

The Best & Worst Spots On The Yield Curve

The Best & Worst Spots On The Yield Curve

1. The Unemployment Rate The Fed has officially pledged through its forward guidance not to lift rates until “maximum employment” is reached. While the exact definition of “maximum employment” can be debated, there is widespread agreement that it includes an unemployment rate below its current adjusted level of 4.9%.4 More specifically, we inferred from the September Summary of Economic Projections that most FOMC participants view an unemployment rate of around 3.8% as consistent with “maximum employment” (Chart 7).5 Chart 7Defining "Maximum Employment"

Defining "Maximum Employment"

Defining "Maximum Employment"

We expect that the Fed will refrain from lifting rates until the unemployment rate reaches 3.8%. 2. Labor Force Participation We explored the debate about labor force participation in a recent report.6 In short, there are some policymakers who believe that “maximum employment” cannot be achieved until the labor force participation rate has returned to pre-COVID levels. There are others, however, who think that an aging population and the recent uptick in retirements make such a return impossible. Randy Quarles, for example: I expect that as conditions normalize, [the labor force participation rate] will pick up, but it is unlikely to return to its February 2020 level. One reason is that a disproportionate number of older workers responded to the initial shock of the COVID event by retiring, which may be an area where participation and employment struggle to retrace lost ground.7 In his speech, Governor Waller also mentioned “2 million jobs” that will be lost forever due to retirements.8 While many policymakers cite increased retirements as a reason why the overall labor force participation rate will remain permanently lower, there is much broader agreement that a reasonable definition of “maximum employment” should include the prime-age (25-54) labor force participation rate being much closer to its February 2020 level (Chart 7, bottom panel). We think the Fed will refrain from lifting rates until the prime-age (25-54) labor force participation rate is close to its February 2020 level. 3. Wage Growth Accelerating wages are a tried-and-true signal that the labor market is running hot. While wage growth is rising quickly right now (Chart 8), there is a strong sense that this is due to pandemic-related labor supply shortages and that wage growth will moderate as pandemic fears (and labor shortages) wane. Chart 8Wage Growth

Wage Growth

Wage Growth

What will be more important is what wage growth looks like when the unemployment rate is close to the Fed’s target of 3.8%. At that point, accelerating wages will give the Fed a strong signal that a 3.8% unemployment rate really does constitute “maximum employment”. 4. Non-Transitory Inflation Of our five factors, this is admittedly the most difficult to pin down. However, Governor Quarles did a good job of explaining non-transitory inflation in last week’s speech: The fundamental dilemma that we face at the Fed now is this: Demand, augmented by unprecedented fiscal stimulus, has been outstripping a temporarily disrupted supply, leading to high inflation. But the fundamental productive capacity of our economy as it existed just before COVID – and, thus, the ability to satisfy that demand without inflation – remains largely as it was, constraining demand now, to bring it into line with a transiently interrupted supply, would be premature. Essentially, Quarles is saying that the Fed does not want to respond to a pandemic-related supply shock by lifting rates and curtailing aggregate demand. The Fed only wants to tighten policy if it sees an increase in broad-based inflationary pressures that will not be contained naturally by a return to more normal aggregate supply conditions. Accelerating wages would be one signal of such broad-based inflationary pressures, as would be measures of core inflation excluding those sectors that have been most impacted by the pandemic supply disruptions (Chart 9). Lastly, we could also look at indicators of inflation’s breadth across its different components, which have recently spiked to concerning levels (Chart 10). Chart 9Non-Covid Inflation

Non-Covid Inflation

Non-Covid Inflation

Chart 10CPI Breadth Has Spiked

CPI Breadth Has Spiked

CPI Breadth Has Spiked

5. Inflation Expectations Inflation expectations are also critical to monitor. While all Fed participants seem to agree that inflation will fall during the next year, there is also widespread agreement that if high inflation causes inflation expectations to rise to uncomfortably high levels, then the Fed will be forced to act. Chris Waller: A critical aspect of our new framework is to allow inflation to run above our 2 percent target (so that it averages 2 percent), but we should do this only if inflation expectations are consistent with our 2 percent target. If inflation expectations become unanchored, the credibility of our inflation target is at risk, and we likely would need to take action to re-anchor expectations at our 2 percent target. At present, inflation expectations remain well-anchored near levels consistent with the Fed’s target (Chart 11). In particular, we like to track the 5-year/5-year forward TIPS breakeven inflation rate targeting a range of 2.3% to 2.5% as consistent with the Fed’s target. Incidentally, Governor Waller also flagged TIPS breakeven inflation rates as his “preferred” measure of inflation expectations in last week’s speech. Chart 11Inflation Expectations Remain Well-Anchored

Inflation Expectations Remain Well-Anchored

Inflation Expectations Remain Well-Anchored

The Fed will move much more quickly toward rate hikes if the 5-year/5-year forward TIPS breakeven inflation rate moves above 2.5%. Bottom Line: Given our view that inflation will fall during the next 12 months, we still view December 2022 as the most likely liftoff date. However, we will continue to monitor our Five Factors For Fed Liftoff to see if our forecast needs to be revised. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 All of our scenarios use a 12-month investment horizon and assume a term premium of 0 bps. 2 In both cases we assume that the fed funds rate trades 8 bps above its lower-bound, as is currently the case. 3 Please see US Bond Strategy Weekly Report, “Right Price, Wrong Reason”, dated October 19, 2021. 4 We adjust the unemployment rate for distortions in the number of people employed but absent from work. Please see US Bond Strategy Weekly Report, “Overreaction”, dated July 13, 2021 for further details. 5 Please see US Bond Strategy Weekly Report, “Damage Assessment”, dated September 28, 2021. 6 Please see US Bond Strategy Weekly Report, “2022 Will Be All About Inflation”, dated September 14, 2021. 7 https://www.federalreserve.gov/newsevents/speech/quarles20211020a.htm 8 https://www.federalreserve.gov/newsevents/speech/waller20211019a.htm Recommended Portfolio Specification Other Recommendations Treasury Index Returns Spread Product Returns

Highlights Inflation in the US and many other countries is likely to follow a “two steps up, one step down” trajectory of higher highs and higher lows over the remainder of the decade. Goods inflation will ease in 2022, while energy price pressures will abate. This suggests that we are currently near the top of those two steps. Any decline in inflation will be short-lived, however. Tight labor markets will bolster wages. Rent inflation is also poised to pick up, especially in the US. The Fed and other central banks will face political pressure to keep interest rates low in order to suppress debt-servicing costs. This could lead to overheating. While we are not as bullish on stocks as we were at the start of the year, the combination of low interest rates and above-trend growth over the next 12 months will support equities. Investors should favor cyclicals, value stocks, small caps, and non-US markets. The Stairway To Higher Inflation In past reports, we argued that global inflation had reached a secular bottom and would begin to reaccelerate (see here, here, and more recently here). While it is still too early to be certain, recent developments appear to have vindicated that view. The path to structurally higher inflation is likely to be a bumpy one. We have generally contended that the shift to a more inflationary regime would follow a “two steps up, one step down” pattern, characterized by a series of higher highs and higher lows for inflation. In thinking about the inflation process, it is useful to distinguish between transitory shocks and structural forces. Unfortunately, much of the recent discussion about inflation has been politically charged, with one camp arguing that high inflation is entirely transitory (mainly due to pandemic disruptions) and another camp arguing that it is entirely structural in nature (big budget deficits, QE, and “dollar debasement” are often cited). The idea that both transitory shocks and structural forces may be driving inflation seems to generate a lot of cognitive dissonance in peoples’ minds. Our view is that transitory shocks have pushed up inflation, but that structural forces (both policy and non-policy related) are playing an important role too. In other words, we think that we are near the top of those metaphorical two steps. The next step for inflation is likely down, even though the longer-term trend is to the upside. Team Transitory Is Right About One Thing During most recessions, cyclically-sensitive durable goods spending falls, while the service sector serves as a ballast for the economy. The pandemic flipped this pattern on its head (Chart 1). While durable goods spending did dip briefly, it came roaring back due to generous stimulus payments and stay-at-home restrictions which cut many households off from the services they normally purchase. In March of this year, US real consumer durable spending was 27% above its pre-pandemic trend (Chart 2A and 2B). Chart 1Unlike During Most Recessions, Durable Goods Spending Spiked Due To Stimulus Checks And Stay-At-Home Restrictions

Unlike During Most Recessions, Durable Goods Spending Spiked Due To Stimulus Checks And Stay-At-Home Restrictions

Unlike During Most Recessions, Durable Goods Spending Spiked Due To Stimulus Checks And Stay-At-Home Restrictions

Chart 2ADurable Goods Spending Has Begun To Normalize, But Durable Goods Prices Keep Rising Due To Supply Bottlenecks (I)

Durable Goods Spending Has Begun To Normalize, But Durable Goods Prices Keep Rising Due To Supply Bottlenecks (I)

Durable Goods Spending Has Begun To Normalize, But Durable Goods Prices Keep Rising Due To Supply Bottlenecks (I)

Chart 2BDurable Goods Spending Has Begun To Normalize, But Durable Goods Prices Keep Rising Due To Supply Bottlenecks (II)

Durable Goods Spending Has Begun To Normalize, But Durable Goods Prices Keep Rising Due To Supply Bottlenecks (II)

Durable Goods Spending Has Begun To Normalize, But Durable Goods Prices Keep Rising Due To Supply Bottlenecks (II)

Durable goods spending has retreated since then, however. As of August, it was only 8% above its trendline. Supply-chain bottlenecks have curbed durable goods spending over the past eight months. A tell-tale sign of a supply shock is when spending declines and prices nonetheless rise. Between January 2020 and March 2021, durable goods spending increased at an annualized rate of 29% while prices rose at an annualized pace of 2%. Since March 2021, durable goods spending has fallen at an annualized pace of 28%, but price inflation has accelerated to 15% (Chart 3).

Chart 3

Even more than other categories of durable goods, vehicle production has been stymied by supply-chain disruptions. Motor vehicles and auto parts represent about 40% of the durable goods sold in the US and accounted for nearly two-thirds of the decline in real durable goods spending between March and August. The downward trend in vehicle sales continued in September, with unit sales declining by 7.2% on the month. In the US, vehicle sales are now back to where they were in 2011 when the unemployment rate was 9%. In the euro area, they are below their sovereign debt crisis lows (Chart 4). The chip shortage hampering vehicle production will abate in 2022. However, vehicle prices are likely to come down only slowly. Auto inventories in the US are only a third of what they were prior to the pandemic (Chart 5). Until dealers are able to rebuild inventories, they will have little incentive to cut prices. Chart 4The Chip Shortage Has Caused Auto Sales To Tumble

The Chip Shortage Has Caused Auto Sales To Tumble

The Chip Shortage Has Caused Auto Sales To Tumble

Chart 5Dealer Inventories Have Collapsed

Dealer Inventories Have Collapsed

Dealer Inventories Have Collapsed

Energy Price Pressures Should Abate, But Probably Not As Fast As Investors Expect Investors believe the recent surge in energy prices will reverse. The futures curves for oil, natural gas, and coal are all in steep backwardation (Chart 6). We agree that energy price pressures are likely to abate in 2022. However, as we discussed last week, the odds are that prices do not fall as quickly as anticipated. This concern is especially acute in Europe, where La Niña could lead to another cold winter and uncertainty abounds over the status of the Nord Stream 2 pipeline. Looking beyond the next 12 months, the risk is that years of declining investment in the oil and gas sector lead to continued energy shortages during the remainder of the decade. In 2020, 12% of global energy production came from renewable sources such as solar, wind, and hydro. The IEA estimates that this share will rise to 20% in 2030. However, the IEA also reckons that the global economy will still need about 5% more oil and natural gas than it consumes now (Table 1). Given the reluctance of many countries to invest in nuclear power generation, the phase-out of carbon-based fuels may take longer than expected.

Chart 6

Table 1Oil And Gas Consumption Will Not Peak Until The Next Decade

The Inflation Outlook: Two Steps Up, One Step Down

The Inflation Outlook: Two Steps Up, One Step Down

Near-Term Upside For Rents Despite increasing home prices in most economies, rent inflation decelerated in the first year of the pandemic (Chart 7). More recently, however, the rental market has begun to heat up. US rents rose by 0.5% in September, the fastest monthly growth since the 2006 housing boom (Chart 8). The Zillow rent index, which looks only at units turning over, has spiked (Chart 9). Chart 7Rent Inflation Is Bouncing Back After Falling During The Pandemic

Rent Inflation Is Bouncing Back After Falling During The Pandemic

Rent Inflation Is Bouncing Back After Falling During The Pandemic

Chart 8More Upside To Rent Inflation

More Upside To Rent Inflation

More Upside To Rent Inflation

Strong job growth, the end of the nationwide eviction moratorium, and the loosening of regulations freezing rents in a number of US cities and states are all contributing to higher rent inflation. A shortage of homes is also putting upward pressure on home prices and rents. After having surged during the Great Recession, the homeowner vacancy rate has fallen to record low levels (Chart 10). Chart 9Newly Listed Apartments Are Being Marked Up Sharply

Newly Listed Apartments Are Being Marked Up Sharply

Newly Listed Apartments Are Being Marked Up Sharply

Chart 10The Home Vacancy Rate Is Very Low

The Home Vacancy Rate Is Very Low

The Home Vacancy Rate Is Very Low

In addition to encouraging more construction, higher home prices could indirectly boost inflation through the wealth effect. According to the Federal Reserve, homeowner equity increased by $4.1 trillion, or 21%, between 2019Q4 and 2021Q2. Empirical estimates of the wealth effect suggest that consumption rises between 5 and 8 cents for every additional dollar in housing wealth. For the US, this would translate into 0.9%-to-1.4% of GDP in incremental annual consumption since the start of the pandemic. Higher Nominal Income Growth Would Make Housing More Affordable Chart 11Many Developed Economies Feature Overheated Housing Markets

Many Developed Economies Feature Overheated Housing Markets

Many Developed Economies Feature Overheated Housing Markets

The housing wealth effect would turn negative if home prices were to fall. While this is less of a risk in the US where housing is still reasonably affordable in many states, it is more of a risk in countries such as Canada, Australia, New Zealand, and Sweden where home prices have reached stratospheric levels in relation to incomes and rents (Chart 11). Not only would a decline in nominal home prices curb construction and consumer spending, but it would also potentially undermine the financial system by reducing the value of the collateral backing mortgage loans. To support spending and preclude an outright fall in home prices, central banks would likely keep interest rates at fairly low levels. Low rates, in turn, would incentivize governments to maintain accommodative fiscal policies. The IMF expects the cyclically-adjusted primary budget deficit to be 2% of GDP larger in advanced economies in 2022-26 compared to 2014-19 (Chart 12).

Chart 12

The combination of low interest rates and loose fiscal policies will help drive nominal income growth, thus allowing for improved home affordability without the need for a disruptive decline in home prices. As Japan’s experience demonstrates, a deflationary environment is toxic for the property market and the financial system. Labor Markets Getting Tighter There is little doubt that the US labor market is heating up. Even though there are 5 million fewer people employed now than at the start of the pandemic, the job vacancy rate is near record high levels and workers are displaying few misgivings about quitting their jobs (Chart 13). Part of the apparent tightness in the US labor market stems from pandemic-related factors. Although enhanced federal unemployment benefits have expired, households are still sitting on $2.4 trillion in excess savings (Chart 14). This cash cushion has allowed workers to be choosy in entertaining job offers. In addition, decreased immigration flows and a spate of early retirements have decreased labor supply.

Chart 13

Chart 14

More recently, the introduction of vaccine mandates has caused some disruptions to the labor market. About 100 million US workers are currently subject to the mandates. According to the Census Household Pulse Survey, about 8 million of them are unvaccinated and attest that “they will definitely not get the vaccine.” Although many of them will reconsider, the anecdotal evidence suggests that some will not. In one glaring example, 4.6% of workers resigned from a rural hospital in upstate New York, causing the maternity ward to temporarily suspend operations. Prospects For A Wage-Price Spiral Chart 15Wages At The Bottom End Of The Income Distribution Are Rising Briskly

Wages At The Bottom End Of The Income Distribution Are Rising Briskly

Wages At The Bottom End Of The Income Distribution Are Rising Briskly

So far, much of the pick-up in wage growth has been confined to the bottom end of the income distribution (Chart 15). Wage pressures are likely to become more broad-based over time as the unemployment rate continues to decline. A full-blown wage-price spiral would worry the Fed. However, such a spiral does not appear imminent. While respondents to the University of Michigan survey in October expected inflation to reach 4.8% over the next 12 months, they anticipated inflation of only 2.8% over a 5-to-10-year horizon (Chart 16). This is not much higher than their pre-pandemic expectations and is lower than the 3.0% figure reported for September. Chart 16Long-Term Inflation Expectations Have Risen But Remain At Historically Low Levels

Long-Term Inflation Expectations Have Risen But Remain At Historically Low Levels

Long-Term Inflation Expectations Have Risen But Remain At Historically Low Levels

It is easy to dismiss households’ beliefs about future inflation as being largely irrelevant. However, these beliefs do influence spending decisions. For example, a record share of households say that this is a bad time to buy a car (Chart 17). The top reason given is that prices are too high. In other words, many households are deferring the purchase of a vehicle in the hopes of getting a better deal. Automobile demand would be a lot higher now if households thought that prices would keep rising, as this would incentivize them to buy a car before prices rose even more. Chart 17Households Think That This Is The Worst Time Ever To Buy A Car

Households Think That This Is The Worst Time Ever To Buy A Car

Households Think That This Is The Worst Time Ever To Buy A Car

Chart 18Inflation Started Accelerating Quickly Only When Unemployment Reached Very Low Levels In The 1960s

Inflation Started Accelerating Quickly Only When Unemployment Reached Very Low Levels In The 1960s

Inflation Started Accelerating Quickly Only When Unemployment Reached Very Low Levels In The 1960s

What should be acknowledged is that inflation expectations tend to be governed by complex social feedback loops, which makes the relationship between slack and inflation highly non-linear. The experience of the 1960s provides a pertinent example. The US unemployment rate reached NAIRU in 1962. However, it was not until 1966, when the unemployment rate was two percentage points below NAIRU, that inflation expectations became unhinged. Within the span of ten months, both wage growth and CPI inflation doubled, with the latter reaching 6% by the end of the decade (Chart 18). The lesson is clear: While long-term inflation expectations are well anchored today, there is no guarantee they will stay that way indefinitely. Is this a lesson that the Fed will heed? Like Larry Summers, we have our doubts, suggesting that the long-term risks to inflation are to the upside. Fighting The Last War Just as military generals are prone to fighting the last war, the same is true of economic policymakers. Central bankers have been staring down the barrel of the deflationary gun for over two decades. In the 1960s, policymakers prioritized high employment over low inflation. With memories of the Great Depression still fresh in their minds, they kept policy rates too low for too long. This time around, policymakers have an additional reason to drag their heels in raising rates: government debt is very high. Higher borrowing costs would force governments to shift spending from social programs to pay off bondholders. Needless to say, that would not be very popular with most voters. Reducing debt-to-GDP ratios via higher nominal income growth will prove to be more politically palatable than fiscal austerity. Investment Conclusions The path to high interest rates is lined with low interest rates. Structurally higher inflation will eventually lead to higher nominal interest rates, but not before an extended period of negative real rates. Chart 19Neither The Fed Nor The Markets Think The Neutral Rate Of Interest Is All That High

Neither The Fed Nor The Markets Think The Neutral Rate Of Interest Is All That High

Neither The Fed Nor The Markets Think The Neutral Rate Of Interest Is All That High

Neither the Fed nor the markets think the neutral rate of interest is all that high (Chart 19). We think the neutral rate is higher than widely believed. However, this will not become apparent until the unemployment rate falls well below its full employment level. For now, the Fed’s leadership will want to avoid rocking the boat by turning more hawkish. While the US 10-year Treasury yield will trend higher over time, it will pause at around 1.8% in the first half of next year as the unwinding of pandemic-related bottlenecks leads to a “one step down” for inflation. The ECB and the Bank of Japan are even more reluctant to tighten monetary policy than the Fed. Some developed economy central banks like those of the UK, Norway, Sweden, Canada, and New Zealand are more inclined to normalize monetary conditions. That said, they too will be constrained by the fear that going it alone in raising rates will put undue upward pressure on their currencies. While we are not as bullish on stocks as we were at the start of the year, the combination of low interest rates and above-trend growth over the next 12 months will support equities. As we discussed in our recent strategy outlook, investors should favor cyclicals, value stocks, small caps, and non-US markets. Bitcoin Trade Update After being up as much as 50%, our short Bitcoin trade got stopped out for a loss. We remain bearish on Bitcoin and have decided to reinstate the trade. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com View Matrix

Image

Special Trade Recommendations

Image

Current MacroQuant Model Scores

Image

Highlights Liquidity conditions in Bangladesh are easy and growth has revived. Exports are set to recover as well. Foreign reserve accumulation will continue, which will have positive implications for the economy and stock prices. Steadily rising capital expenditure has improved the economy’s productivity and competitiveness. Progress towards gender and income equality has also been impressive. Growth will stay strong and steady, which warrants higher equity multiples. Bangladeshi stocks also have low correlation with their EM and Emerging Asian counterparts, providing diversification benefits. Absolute return investors should buy this market on dips. Dedicated EM/Frontier market equity portfolios should consider overweighting Bangladeshi stocks. Feature A new business cycle appears to be unfolding in Bangladesh. Domestic demand has picked up. Exports are slated to rise as well. The country’s structural progress also continues to be impressive. Not surprisingly, stocks have gone up in tandem. Yet, high and rising oil prices may lead to a pause in the rally. Absolute-return investors with a time horizon of more than one year should therefore consider accumulating equities on dips. Dedicated equity investors should consider adding the very ‘low-correlation’ Bangladeshi equity market to an EM Asia/EM equity portfolio (Chart 1). External Tailwinds Bangladesh’s foreign reserves have surged to a new high. This has been a very positive development for both the economy and stock prices (Chart 2). Chart 1Bangladeshi Stocks Will Benefit From Liquidity Tailwinds

Bangladeshi Stocks Will Benefit From Liquidity Tailwinds

Bangladeshi Stocks Will Benefit From Liquidity Tailwinds

Chart 2Foreign Reserves, M1 And Stock Prices

Foreign Reserves, M1 And Stock Prices

Foreign Reserves, M1 And Stock Prices

Chart 3Both Current And Capital Account Balances Have Improved

Both Current And Capital Account Balances Have Improved

Both Current And Capital Account Balances Have Improved

The country’s balance of payments (BoP) has improved substantially in the last couple of years. The improvement can be attributed to both current and capital accounts: The current account deficit has narrowed significantly since 2018. The improvement will likely persist as the outlook of its two main components are both promising: Remittances have surged to an all-time high of $25 billion over the past 12-months. In the coming year too, it will likely stay buoyant thanks to a 2% incentive scheme that the government introduced on inward remittances (Chart 3, top panel). The second major component, the trade deficit, will likely stabilize. This is because exports are set to pick up, in part due to rising orders from the EU, Bangladesh’s prime export destination (Chart 4). The recent surge in trade credit inflows also implies a significant rise in export revenues in the coming months (Chart 5). That said, high oil prices, if they remain as such, will lead to higher import bills. Crude and petroproducts make up about 10% of Bangladesh’s import costs and can be a headwind to the trade balance, and by extension, stock prices. Chart 6 shows that stock prices accelerate when oil prices are low, but struggle when oil prices rise. Chart 4Strong EU Orders Means Exports Are Set To Accelerate Further

Strong EU Orders Means Exports Are Set To Accelerate Further

Strong EU Orders Means Exports Are Set To Accelerate Further

Chart 5A Surge In Trade Credit Also Implies Strong Export Numbers Ahead

A Surge In Trade Credit Also Implies Strong Export Numbers Ahead

A Surge In Trade Credit Also Implies Strong Export Numbers Ahead

Capital account inflows have risen sharply too. The rise is due mainly to surging trade financing inflows (as mentioned above), and elevated government foreign borrowing (Chart 3, bottom panel). Going forward, trade financing inflows can remain at a high level if the country continues to obtain the same volume of export orders. The government’s foreign borrowing may also persist. Notably, this long-term financing is mostly used to import capital goods – something that the country needs for its investment and infrastructure projects (Chart 7). With Bangladesh’s ever-rising capital expenditure, such long-term capital inflows – either in the form of government borrowing, or FDI, or a combination of two – will likely continue. If so, this will not only help boost the country’s BoP in the short-term, but it will also be a long-term positive for Bangladesh since capital spending will help improve productivity. Chart 6Stocks Struggle Whenever Oil Prices Rise Too Much

Stocks Struggle Whenever Oil Prices Rise Too Much