Manufacturing

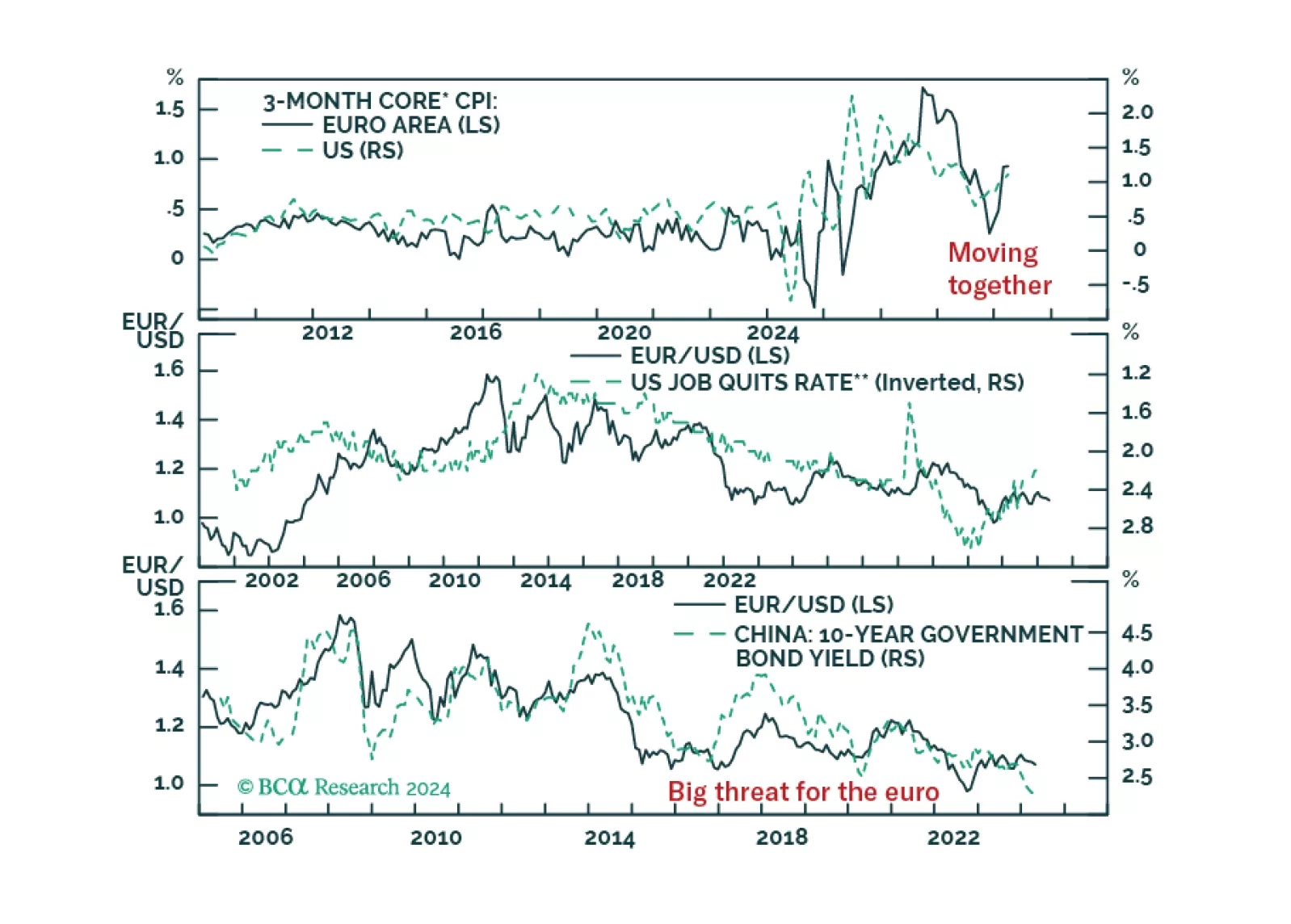

EUR/USD collapsed in the wake of last week’s hotter-than-expected US CPI report. Is this pessimism warranted and will the euro’s trading range that has prevailed since 2023 breakdown?

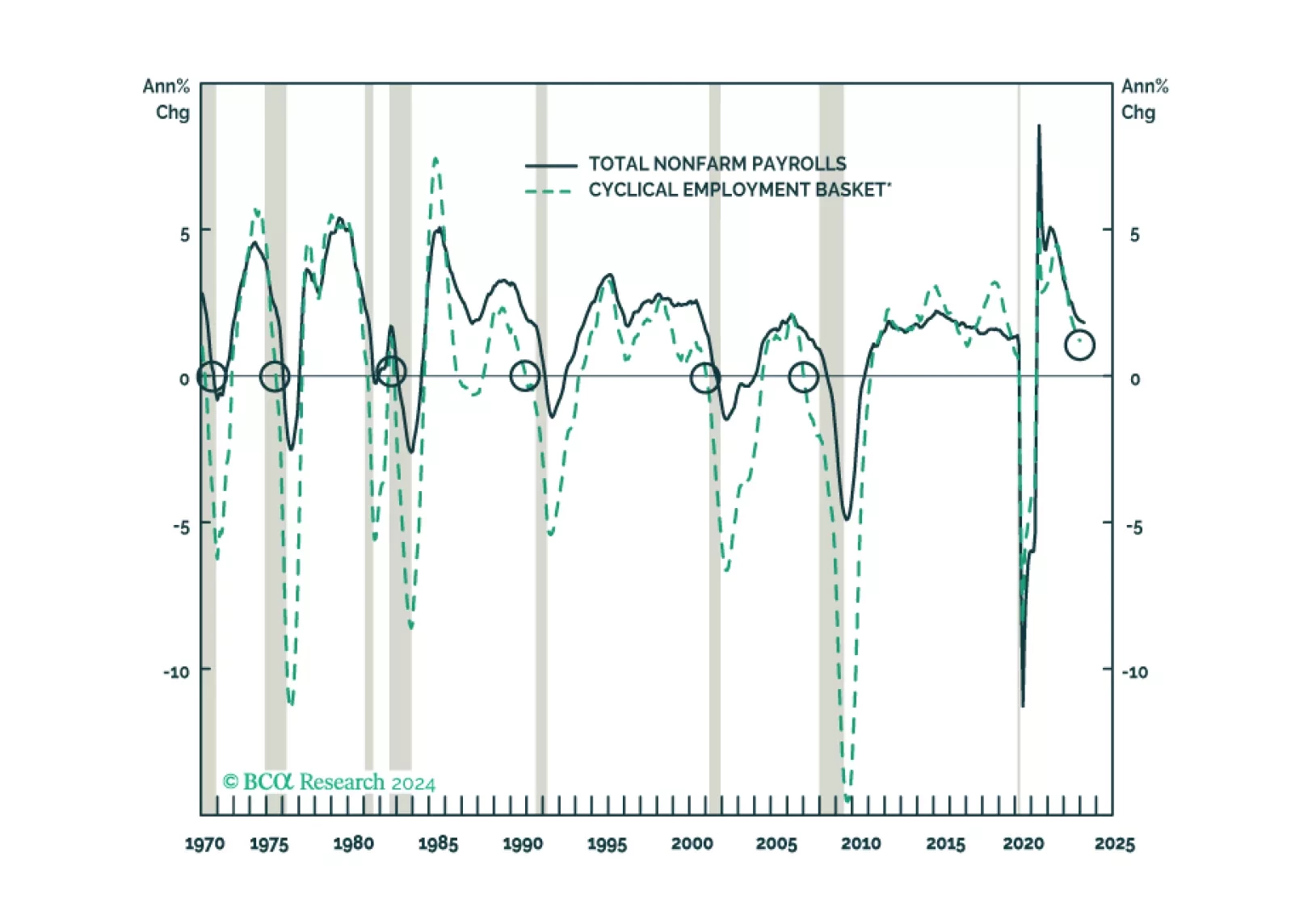

We look beneath headline data to assess the state of the labor market in cyclical goods-producing industries that have previously led overall nonfarm payrolls and in the services segments that have recently been leading the charge. The bottom-up view looks a lot like the top-down view: the labor market is softening, but very slowly, and offers no indications that a recession is at hand.

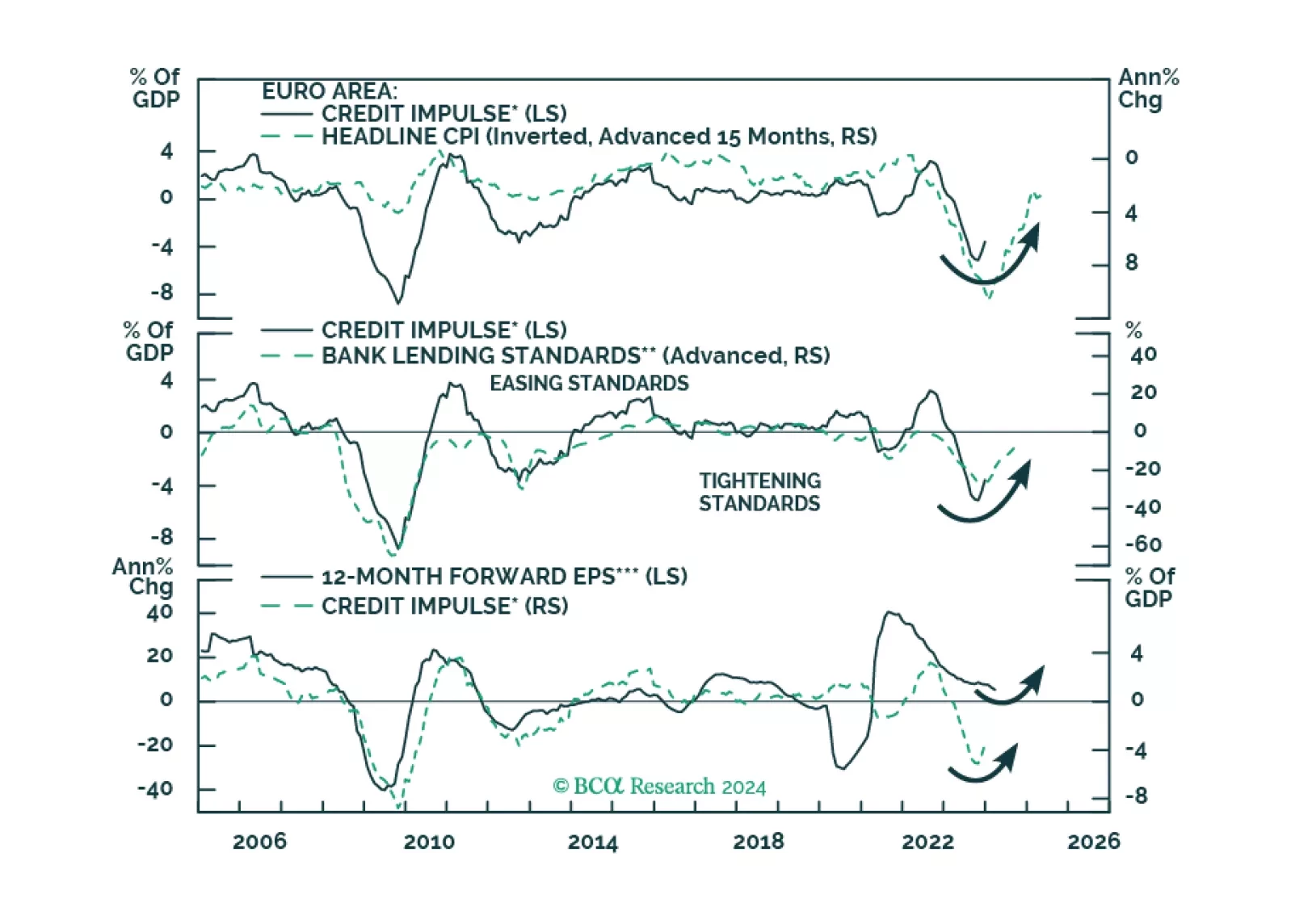

Europe credit flows are stabilizing, hence a major drag on the region’s growth will dissipate. What does this development imply for European equities?

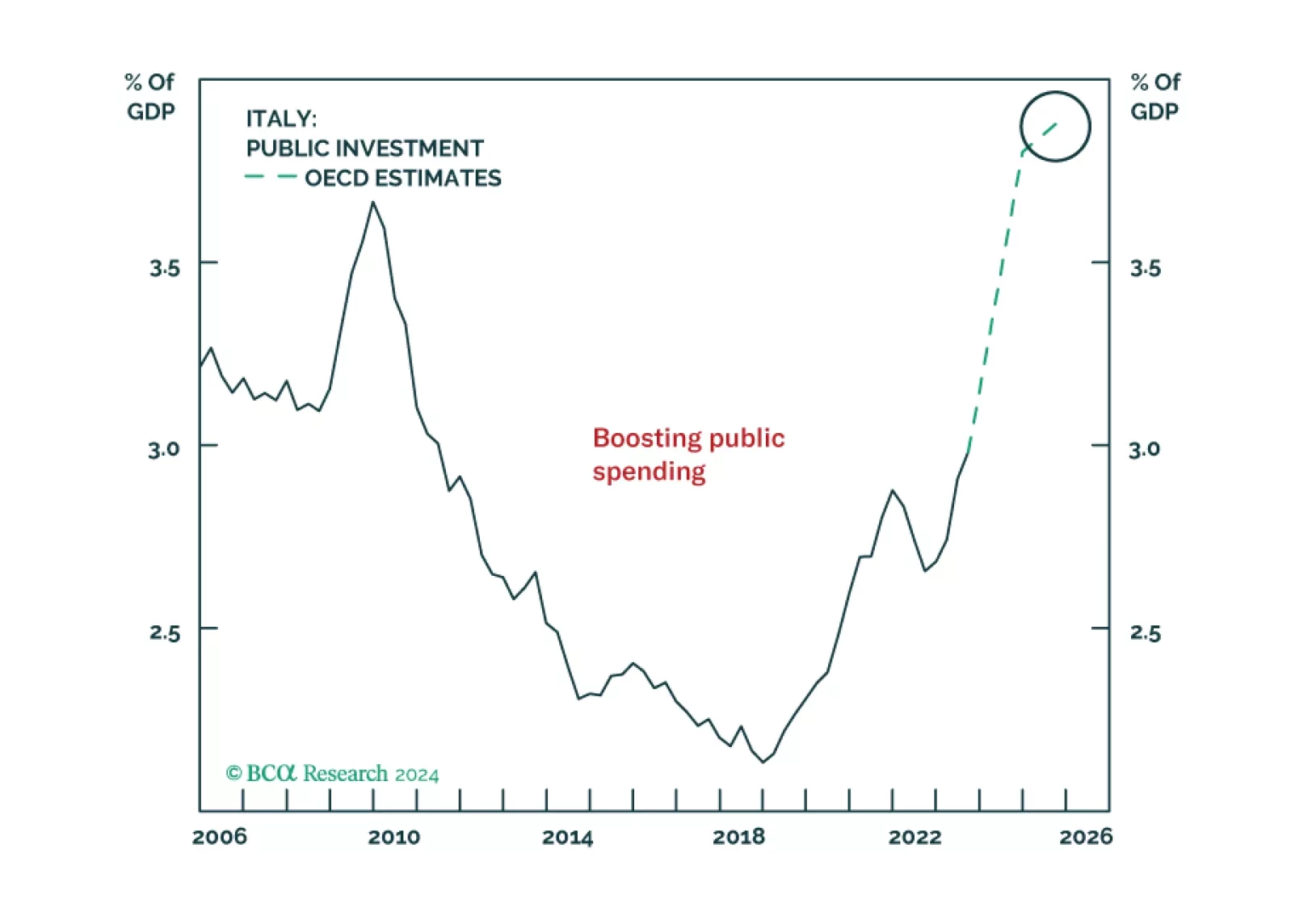

Italy is no longer Europe’s problem child. Investors will be better off reassessing their views of Italian assets, which represent a buying opportunity on a structural time horizon.