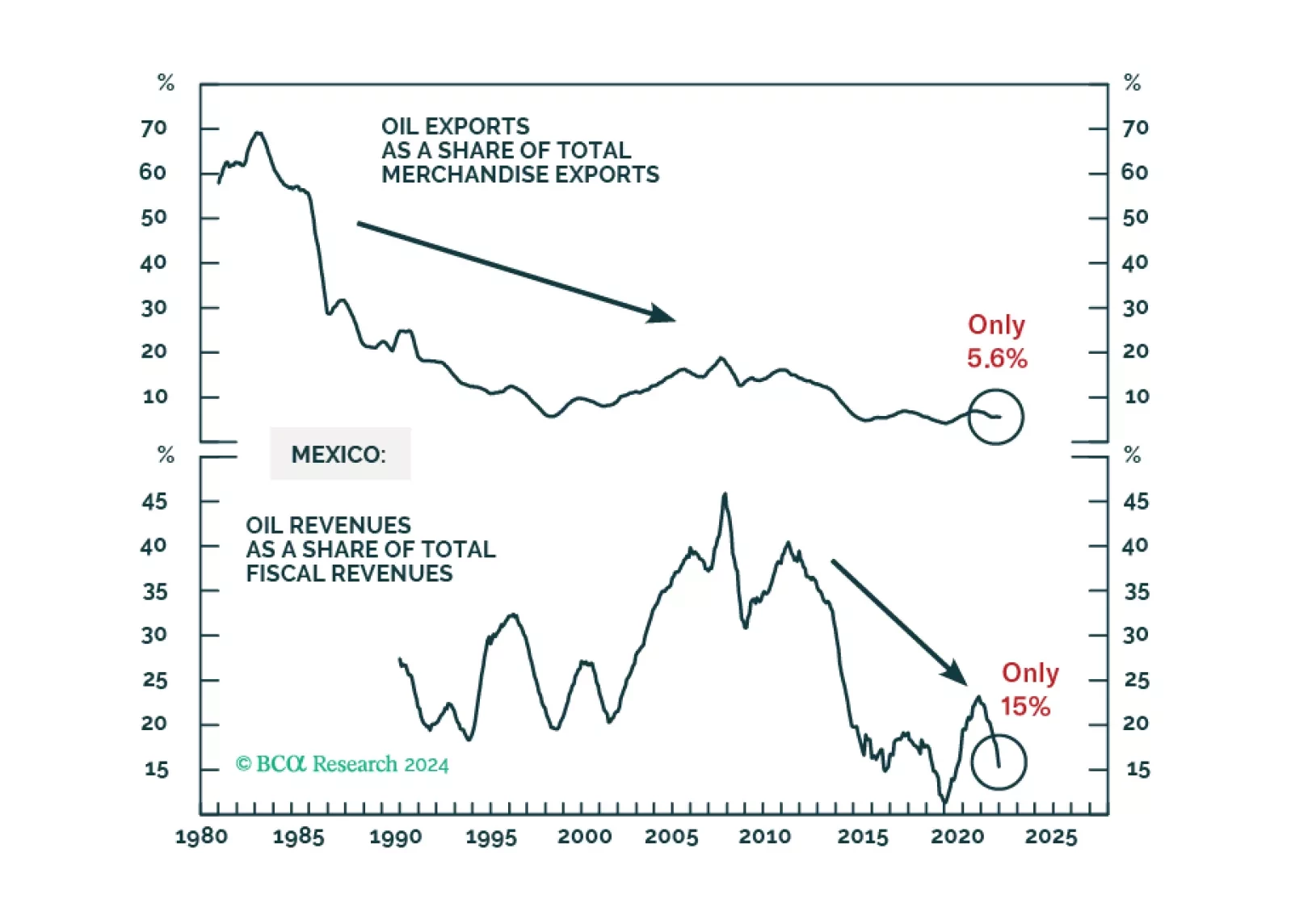

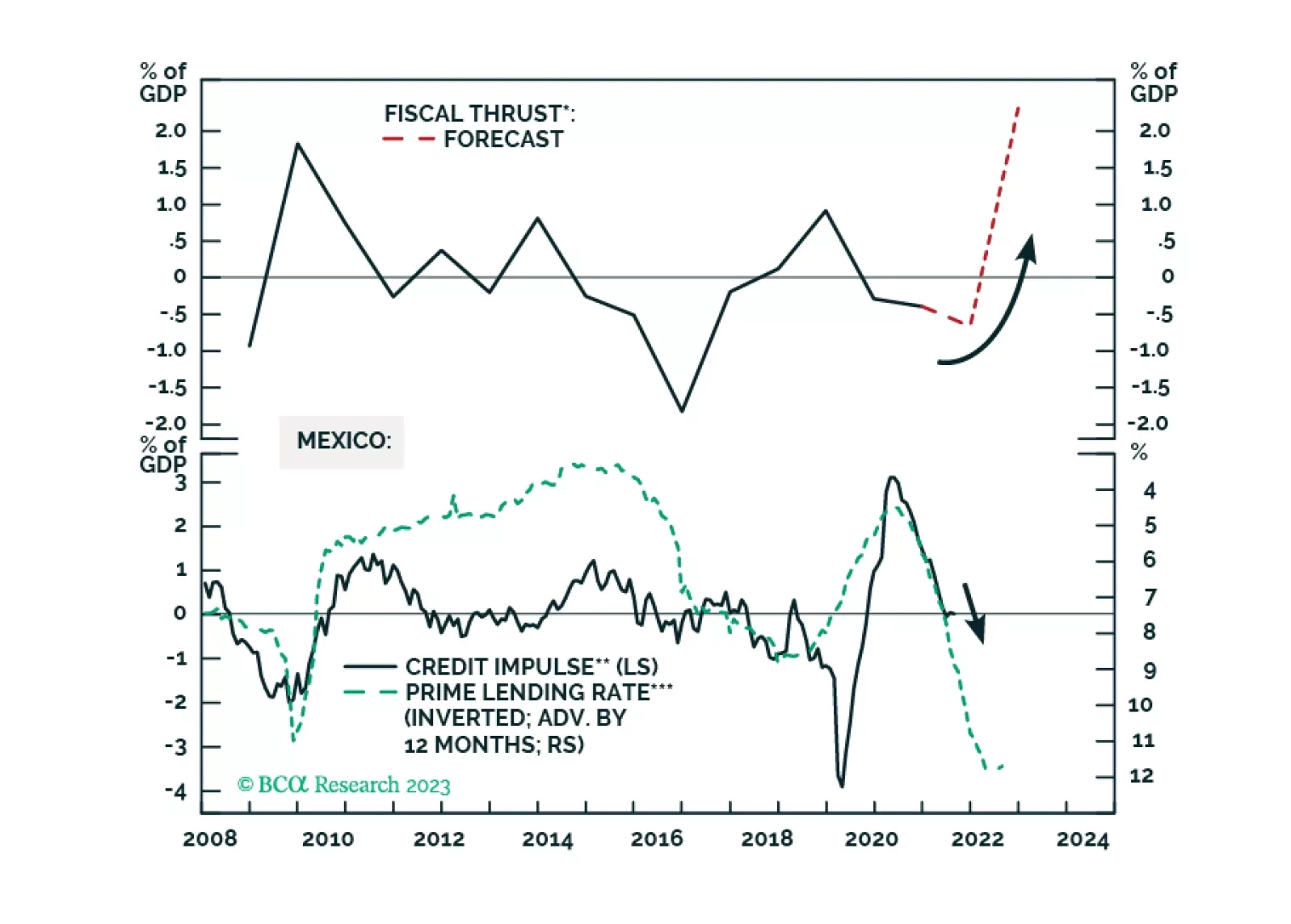

Mexico

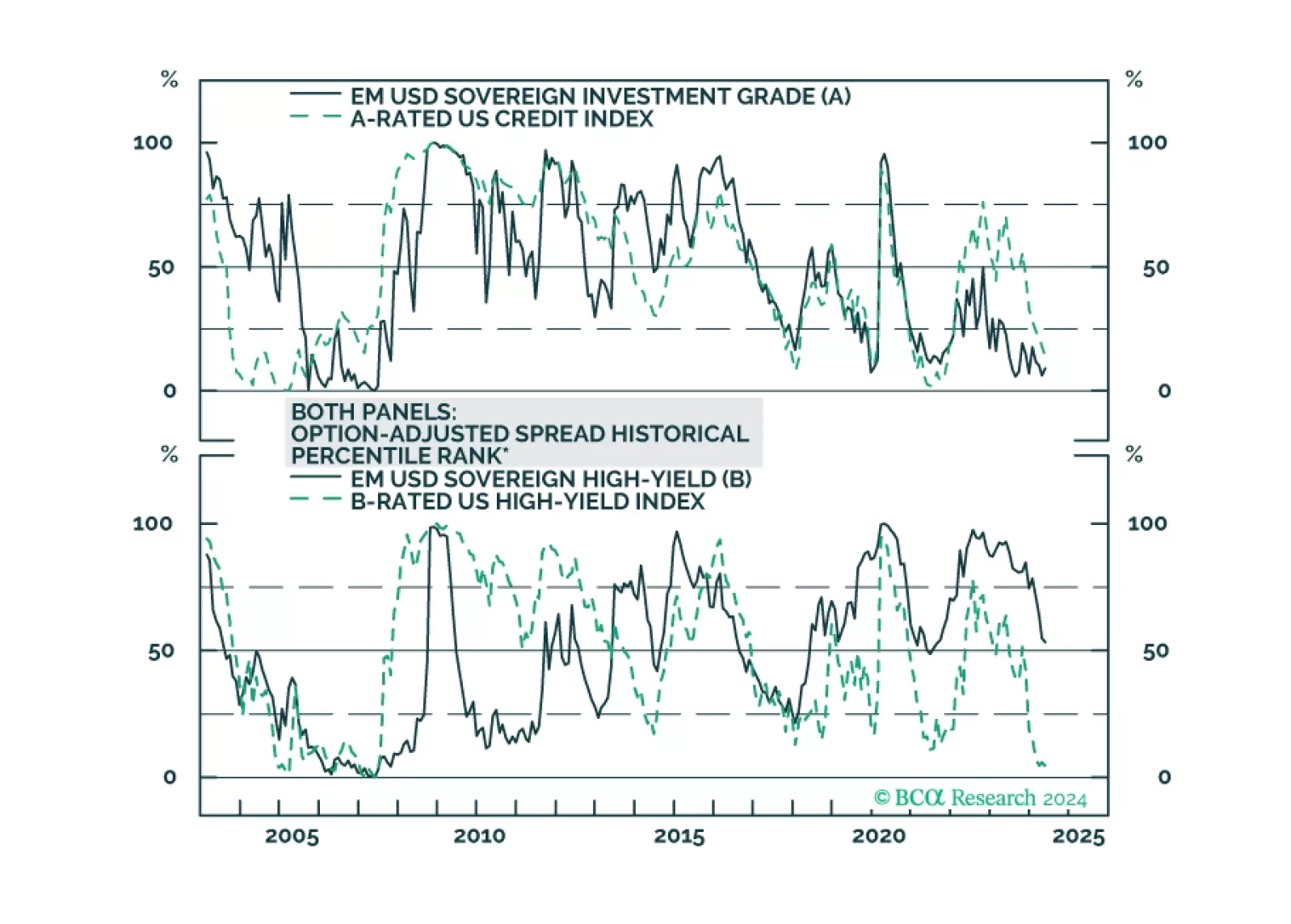

We dig into the USD-denominated Emerging Market Sovereign Index to see which credit tiers and countries offer value relative to US Credit.

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

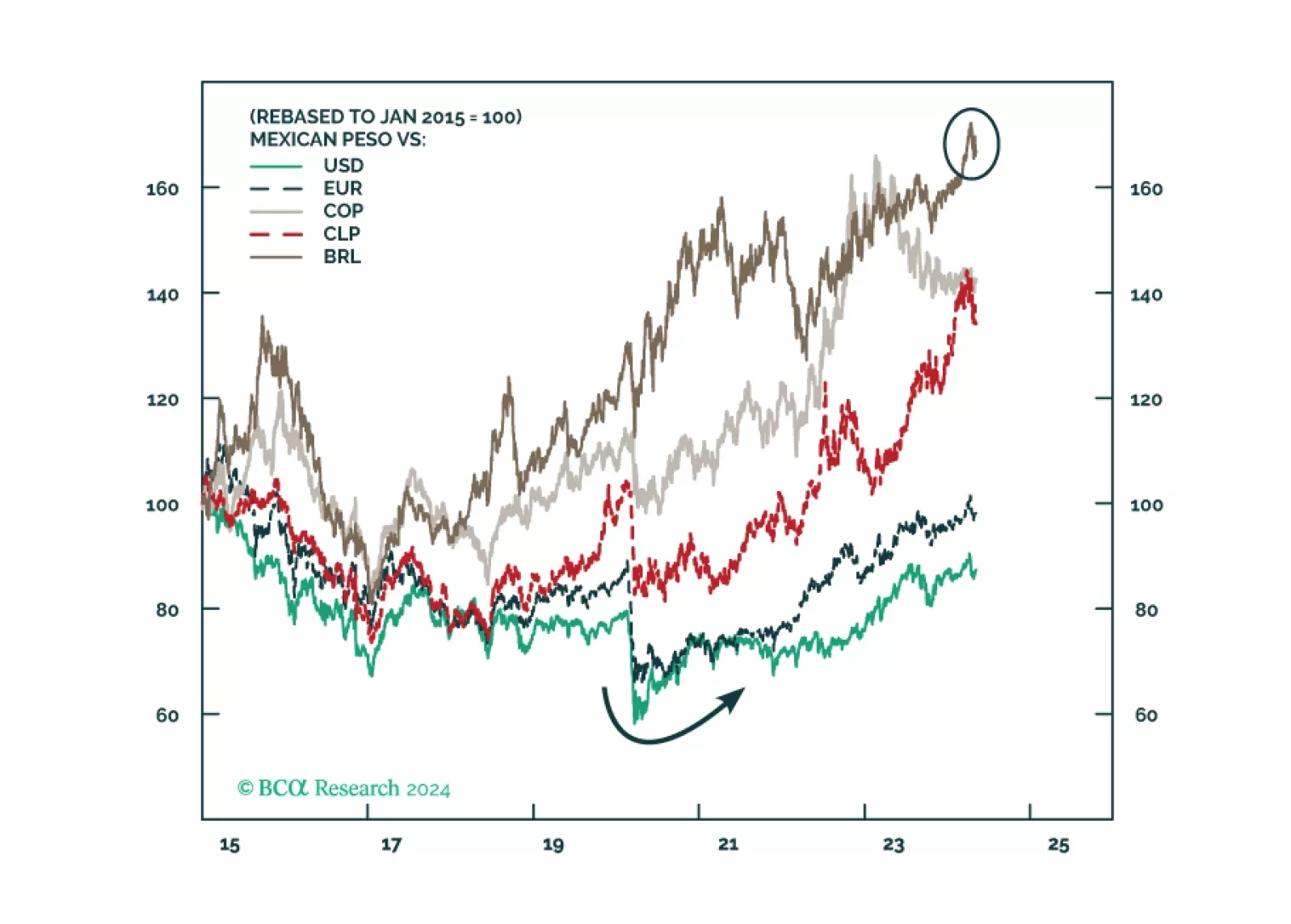

Continue overweighting Mexican stocks, sovereign credit, and local bonds relative to their respective EM benchmarks. That said, the peso is overbought and will correct versus the US dollar. Therefore, we recommend that investors hedge the currency risk for their outright long positions in Mexican equity and local bond markets for the next few months.

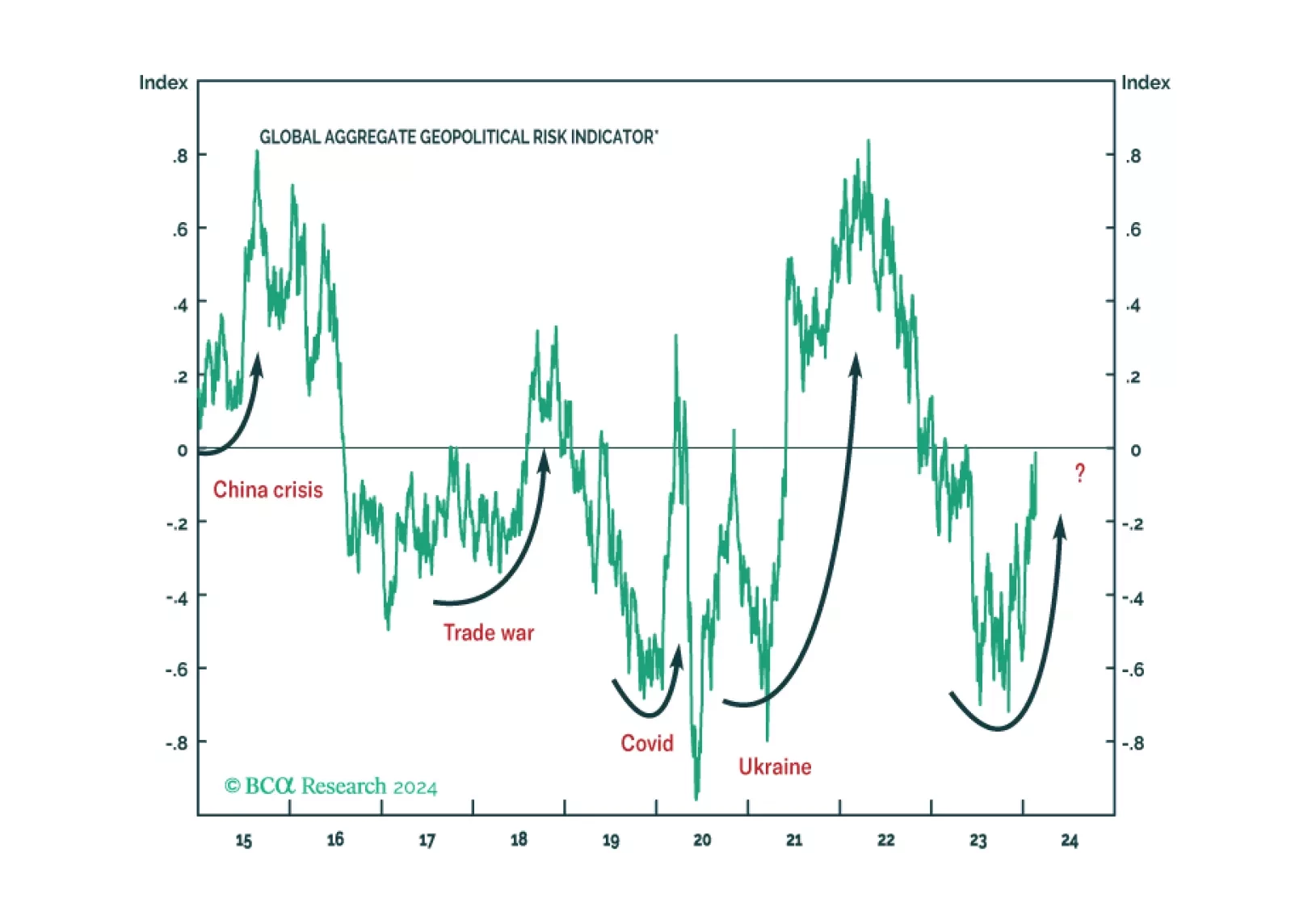

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

While Mexican markets will continue selling off in absolute terms, their recent underperformance versus their EM peers is a temporary setback in a cyclical and structural bull market. Domestic politics are evolving from stable to bullish: the new president will rule in a technocratic manner, respecting private sector interests. The Mexican economy will achieve a soft landing even if the US enters a recession.