Oil

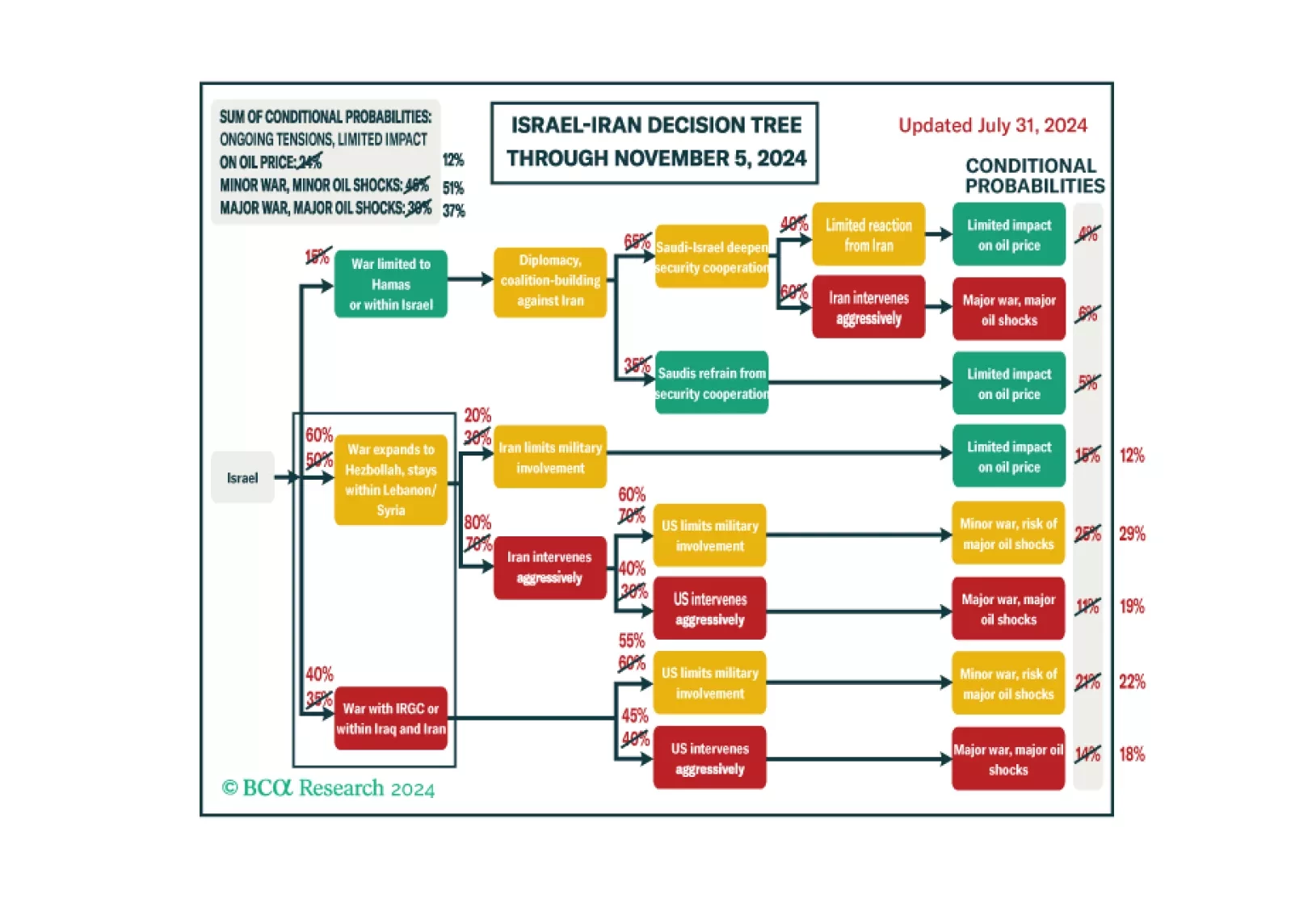

The war in the Middle East is expanding, upgrading our subjective odds of a major oil supply shock to 37% and underscoring our 60% odds of Republican victory in November. Volatility should spike again as investors contemplate the prospect of rising oil prices amid slowing US and global growth. Tactically investors should stay overweight energy stocks relative to other cyclicals and favor oil producers in the Americas rather than Middle East.

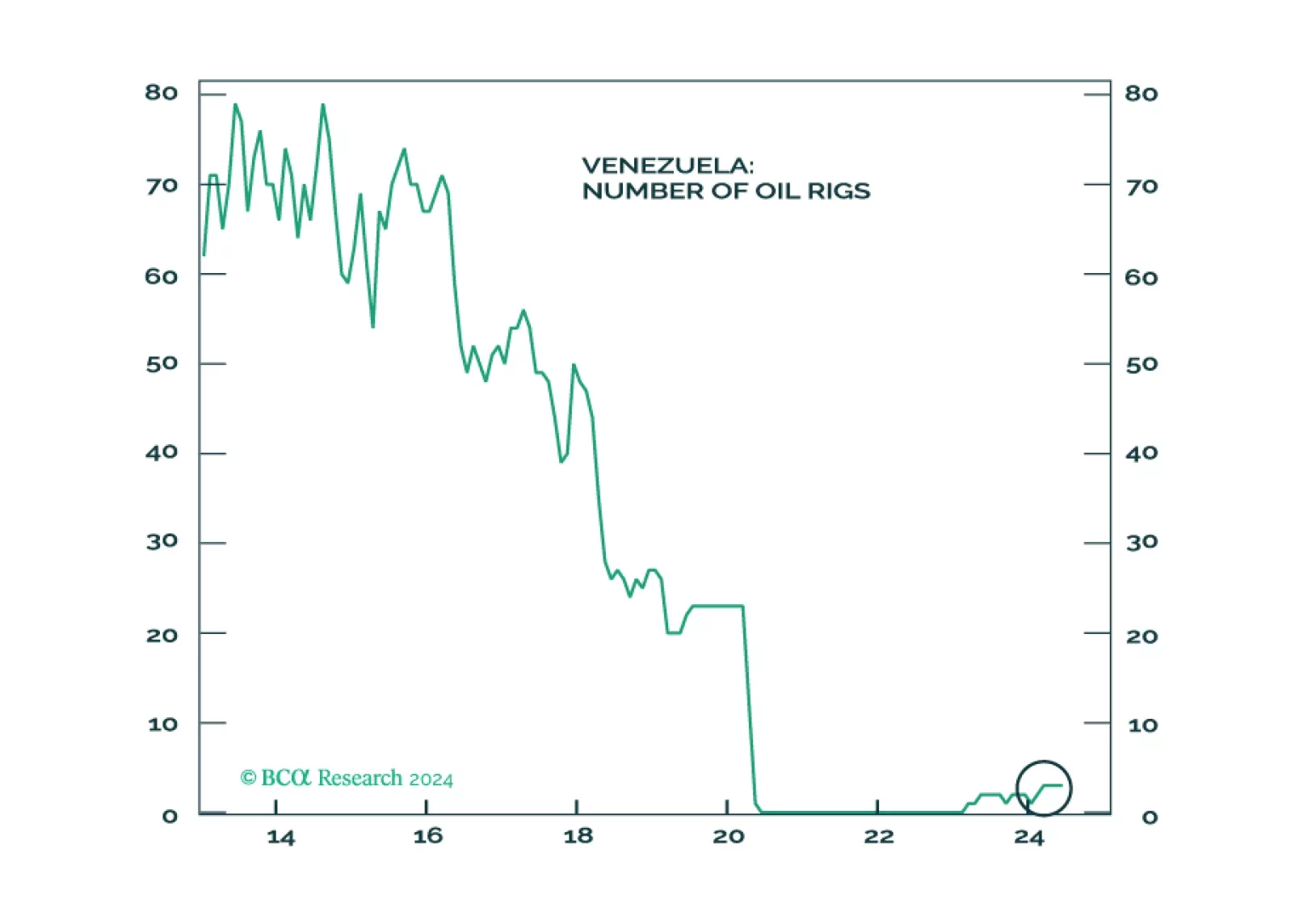

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

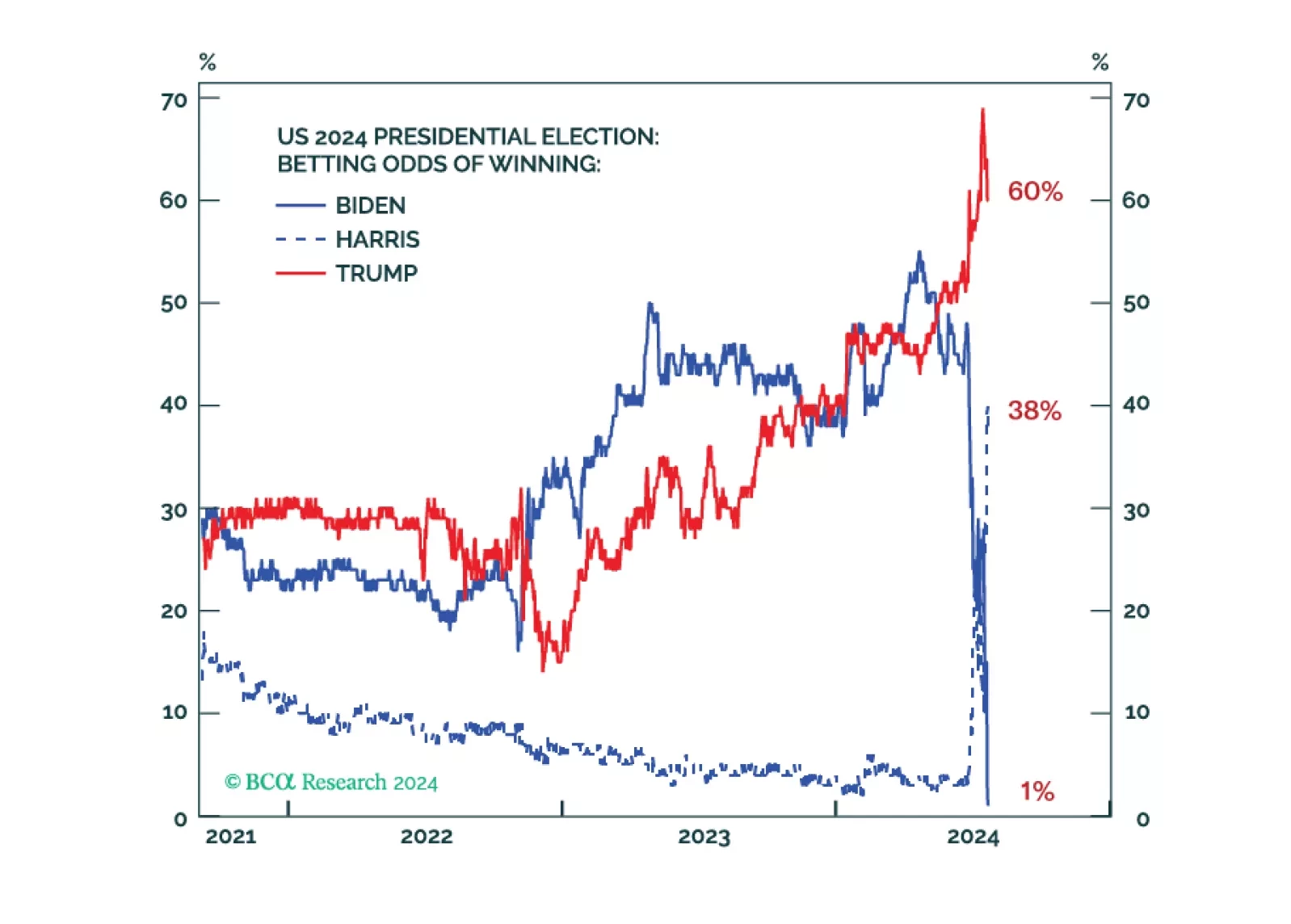

Investors should focus on growth concerns rather than the “Trump trade.” Bond yields will fall in the short run due to cyclically disinflationary economic slowdown, rather than rise in anticipation of a Republican full sweep and inflationary policies, which are likely but not yet a done deal.

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.

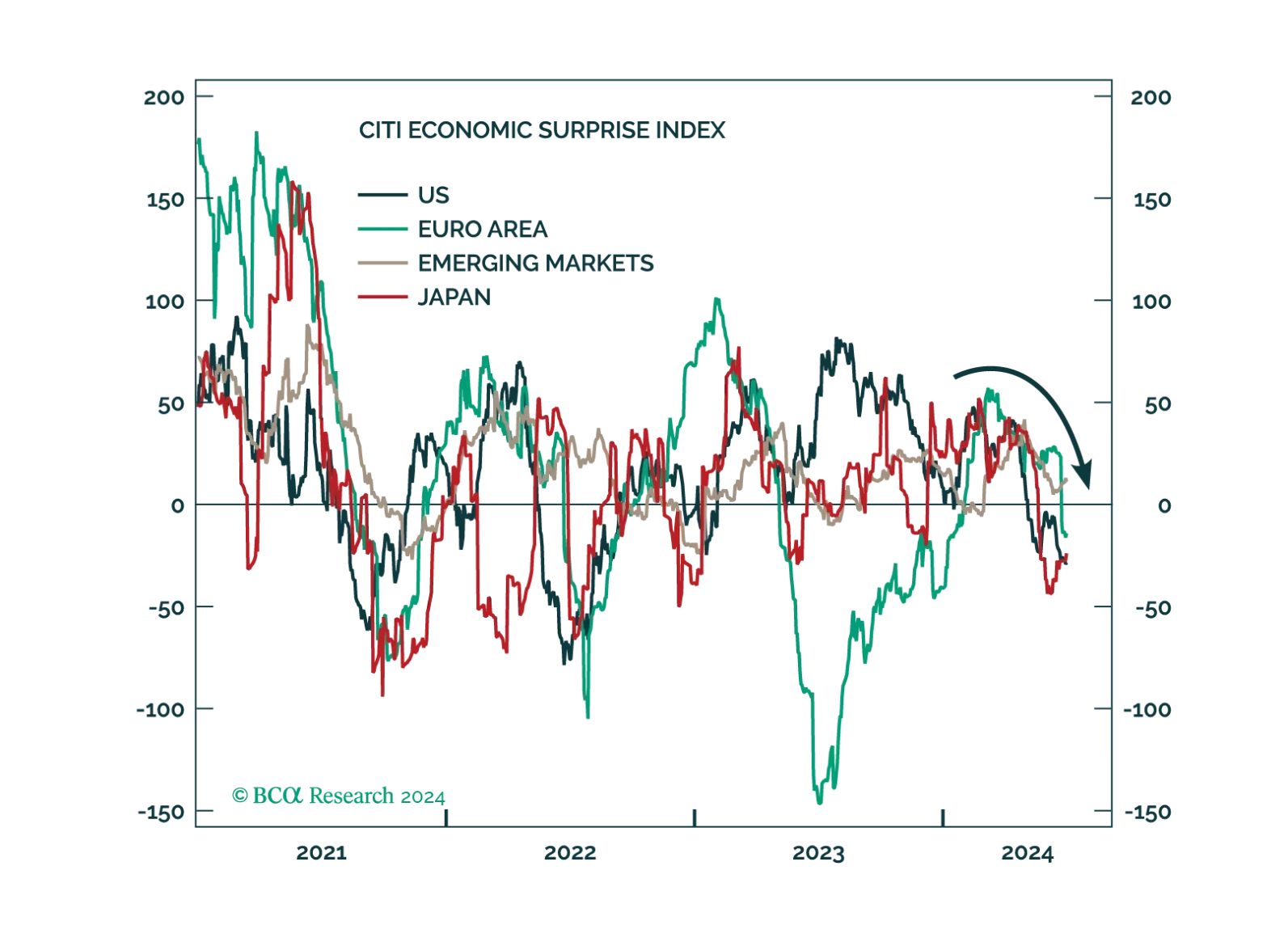

Concerns about the global economy have shifted from sticky inflation to faltering growth. Tight monetary policy is finally starting to bite. We suggest increasing portfolio defensiveness.

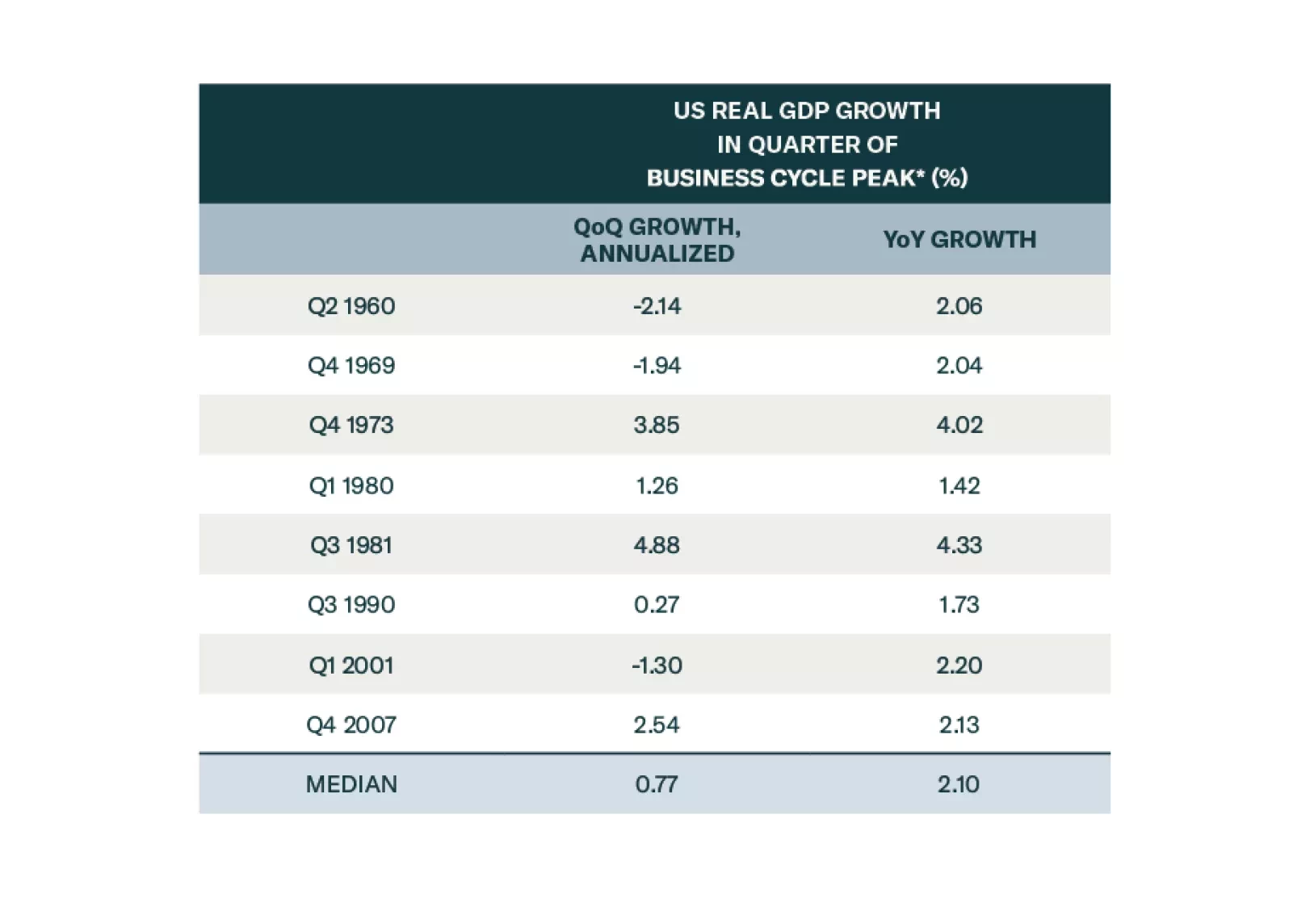

The consensus soft-landing narrative is wrong. The US will fall into a recession in late 2024 or early 2025. We were tactically bullish on stocks most of last year, turned neutral earlier this year, and are going underweight today. We conservatively expect the S&P 500 to drop to 3750 during the coming recession.

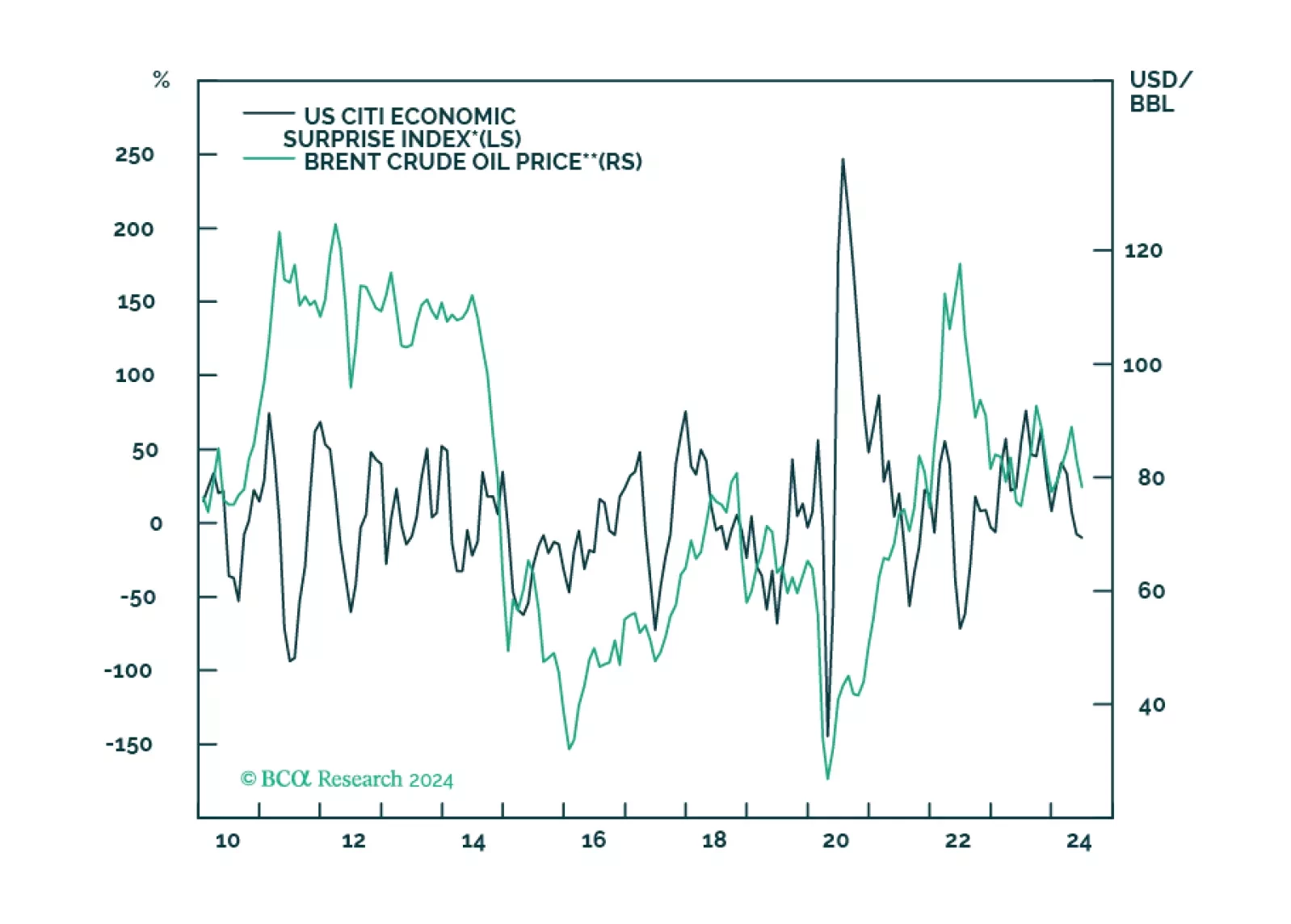

We close our overweights to Energy and Aerospace & Defense. The macroeconomic backdrop is deteriorating for Energy. As for A&D, the good news is already priced in.