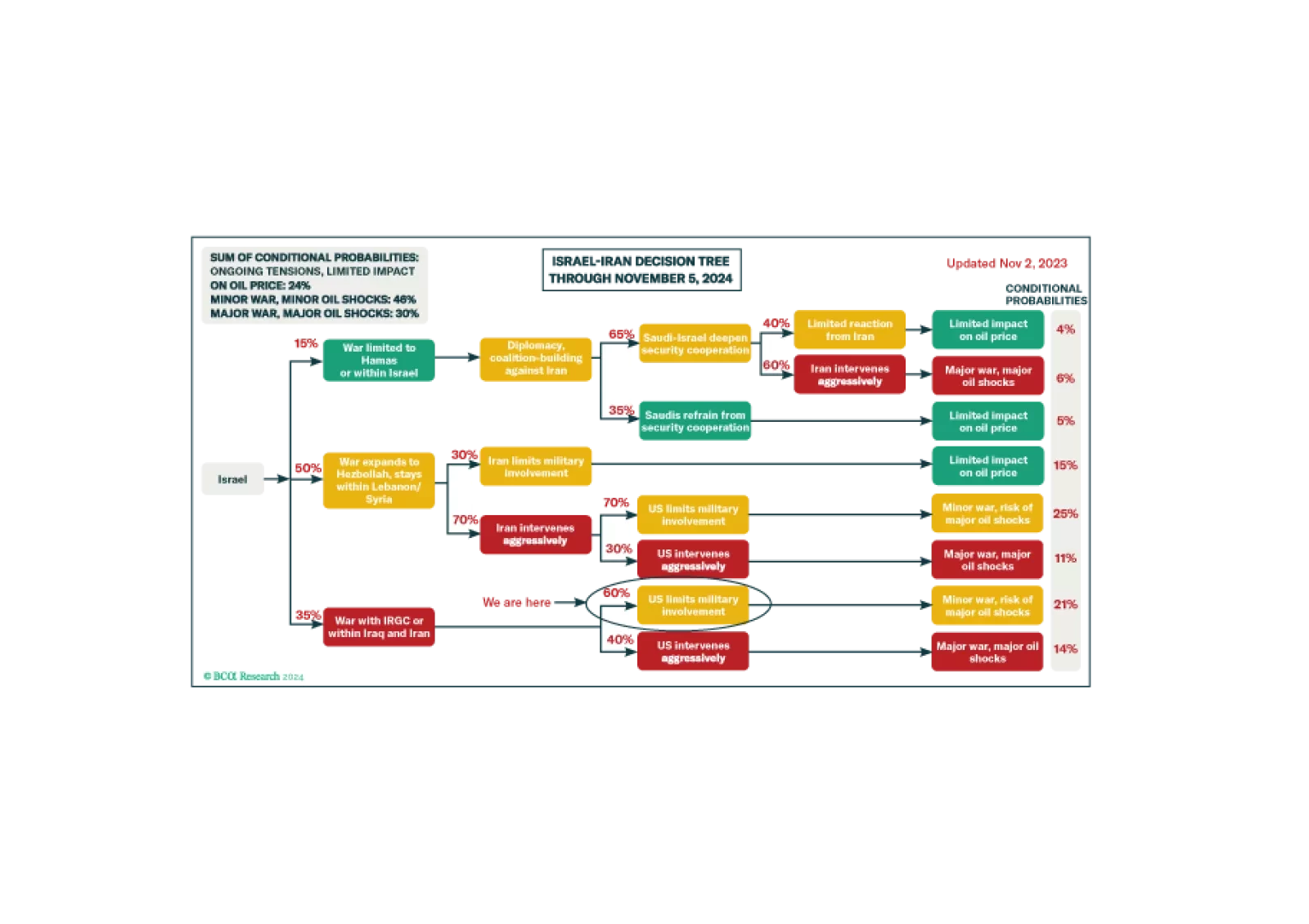

Oil

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability. The US is hobbled by its election. Conflicts with Russia, China, and Iran are all now escalating at the same time, at least marginally. Investors should reduce risk and shift to more defensive assets, markets, and sectors.

The stock market will suffer a setback from the weakening labor market and a rebound in US and global policy uncertainty.

Investors should prepare for economic data to weaken even as policy uncertainty and geopolitical risk skyrocket ahead of the US election.

The implication is that Israel chose not to escalate the risk of direct war with Iran. Hence we remain in our base-case “Minor War, Minor Oil Shock” scenario.