Oil

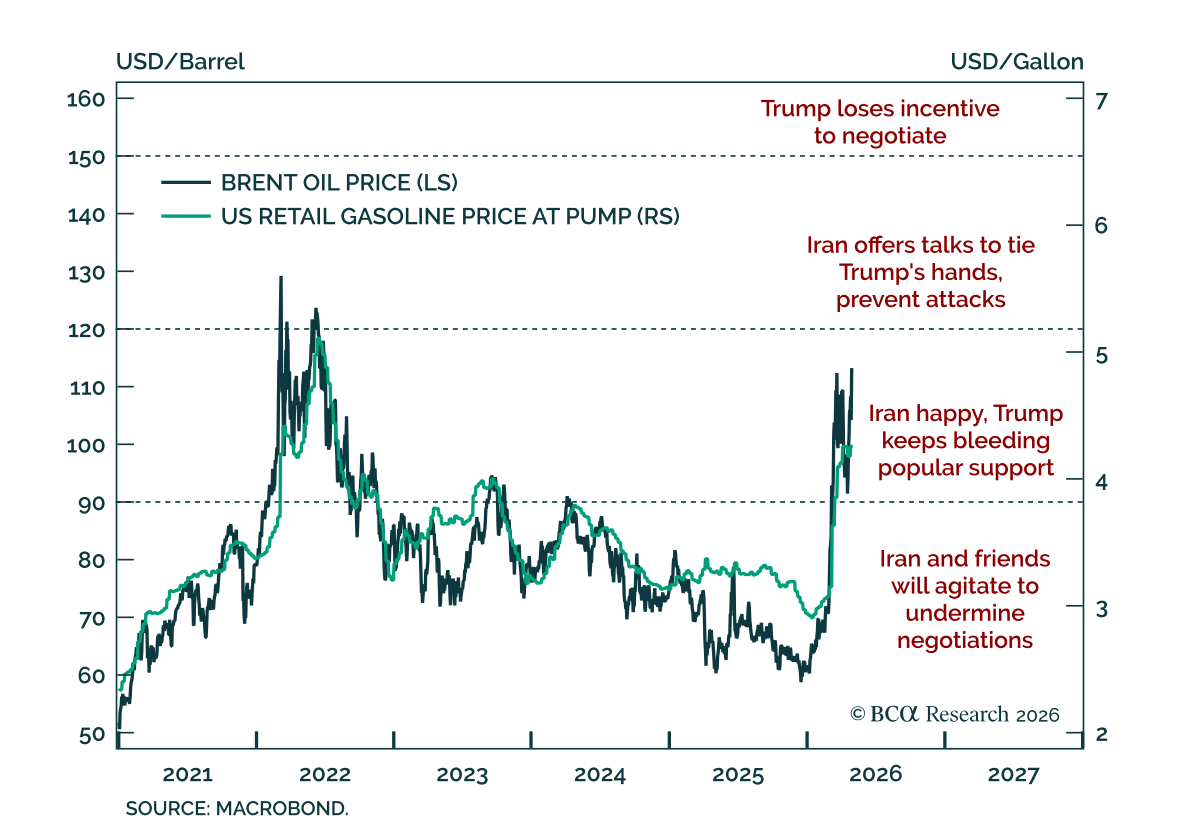

Hopes for an imminent Middle East de-escalation have capped oil prices in recent weeks, but that restraint may soon fade.

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

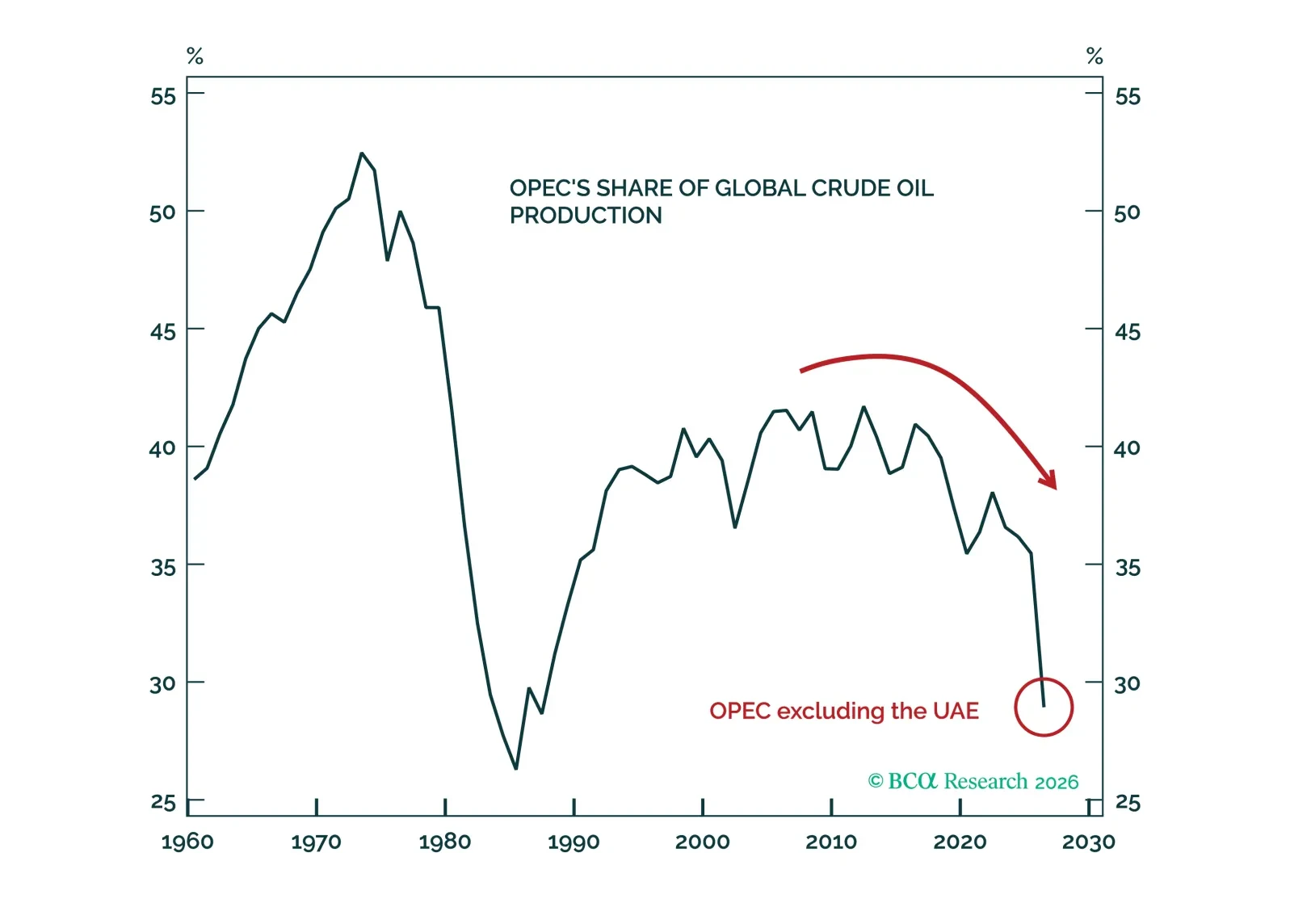

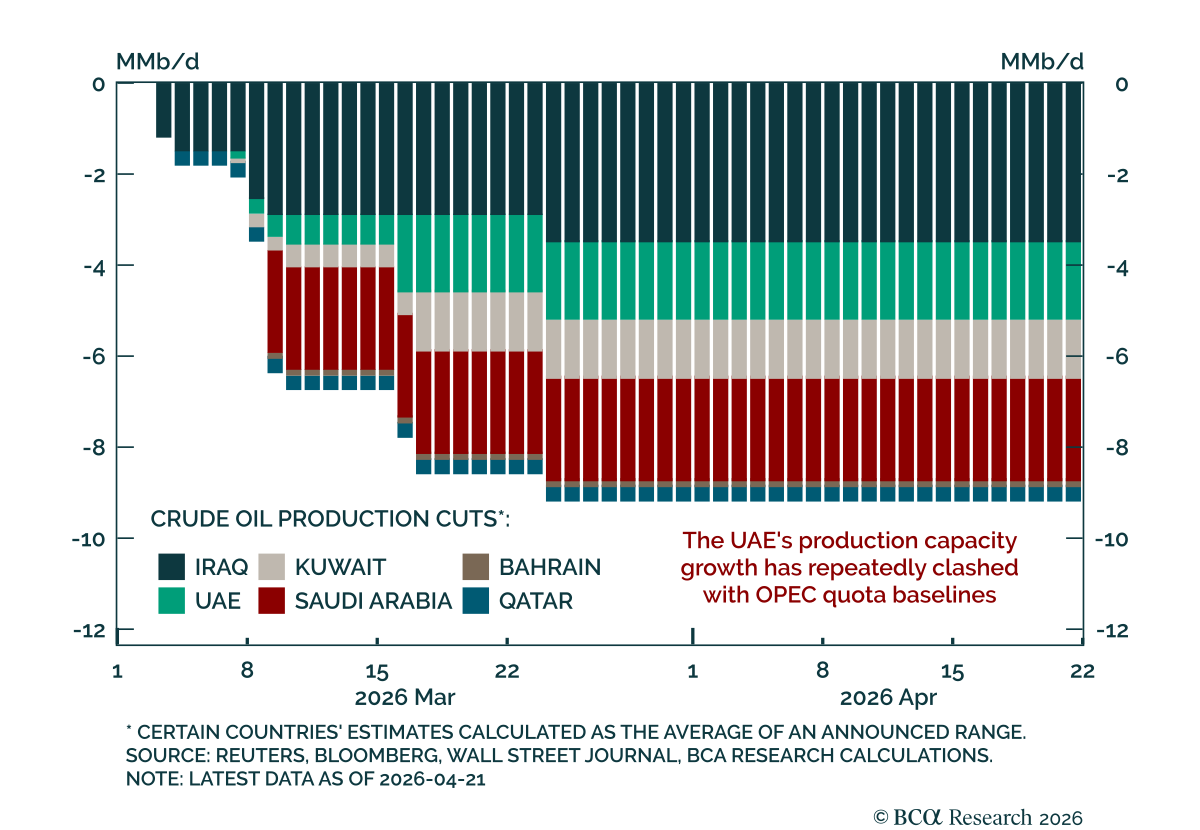

The UAE’s exit from OPEC is unlikely to impact oil markets in 2026. Over the longer term, however, the emergence of an “anti-OPEC club” of producers favoring unconstrained oil output growth would create a headwind to crude prices and weaken the price floor that OPEC seeks to defend.

So far, there is no evidence of second-round effects from the oil price shock showing up in the US economy. Fed rate hikes are off the table unless those effects emerge.

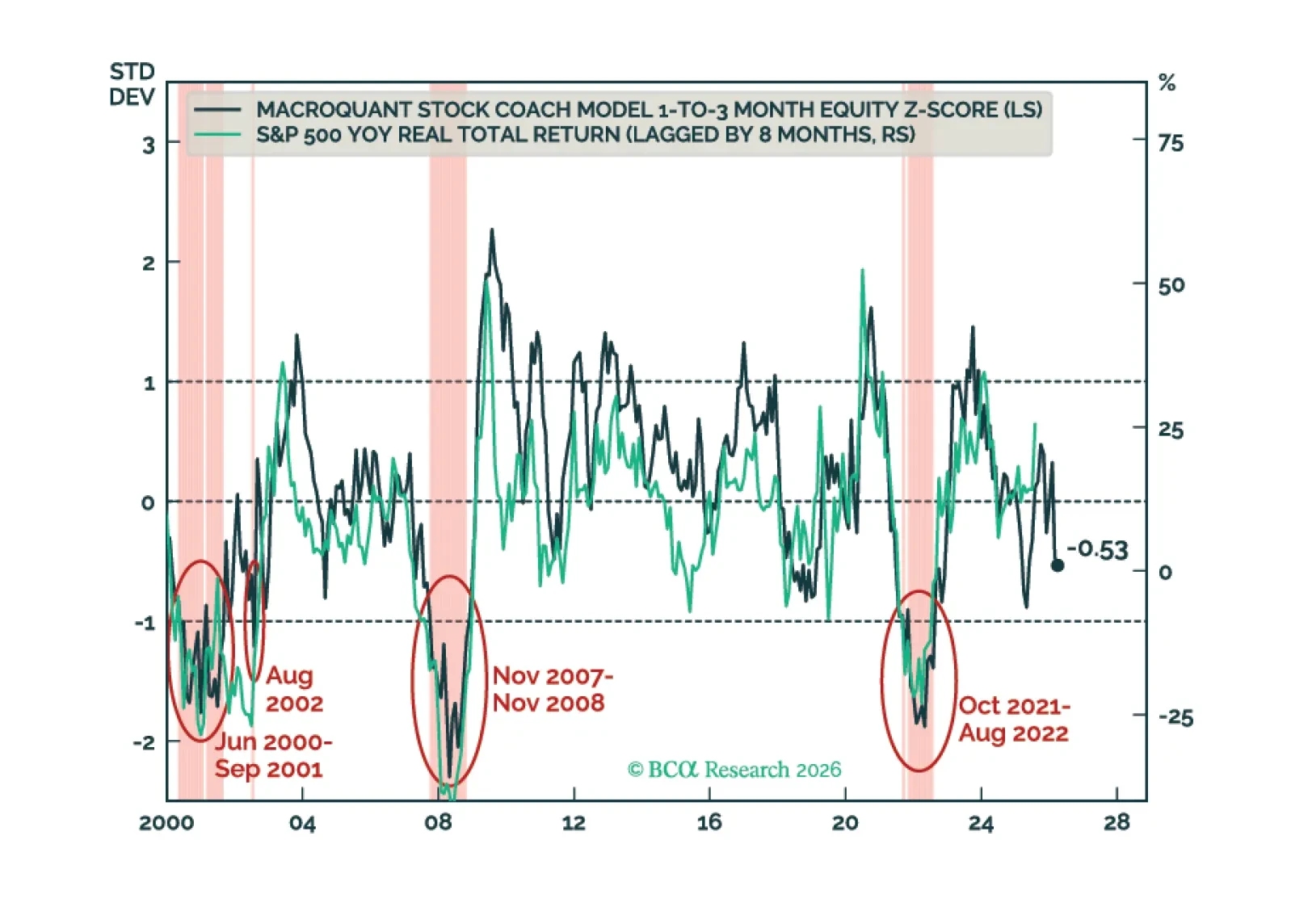

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

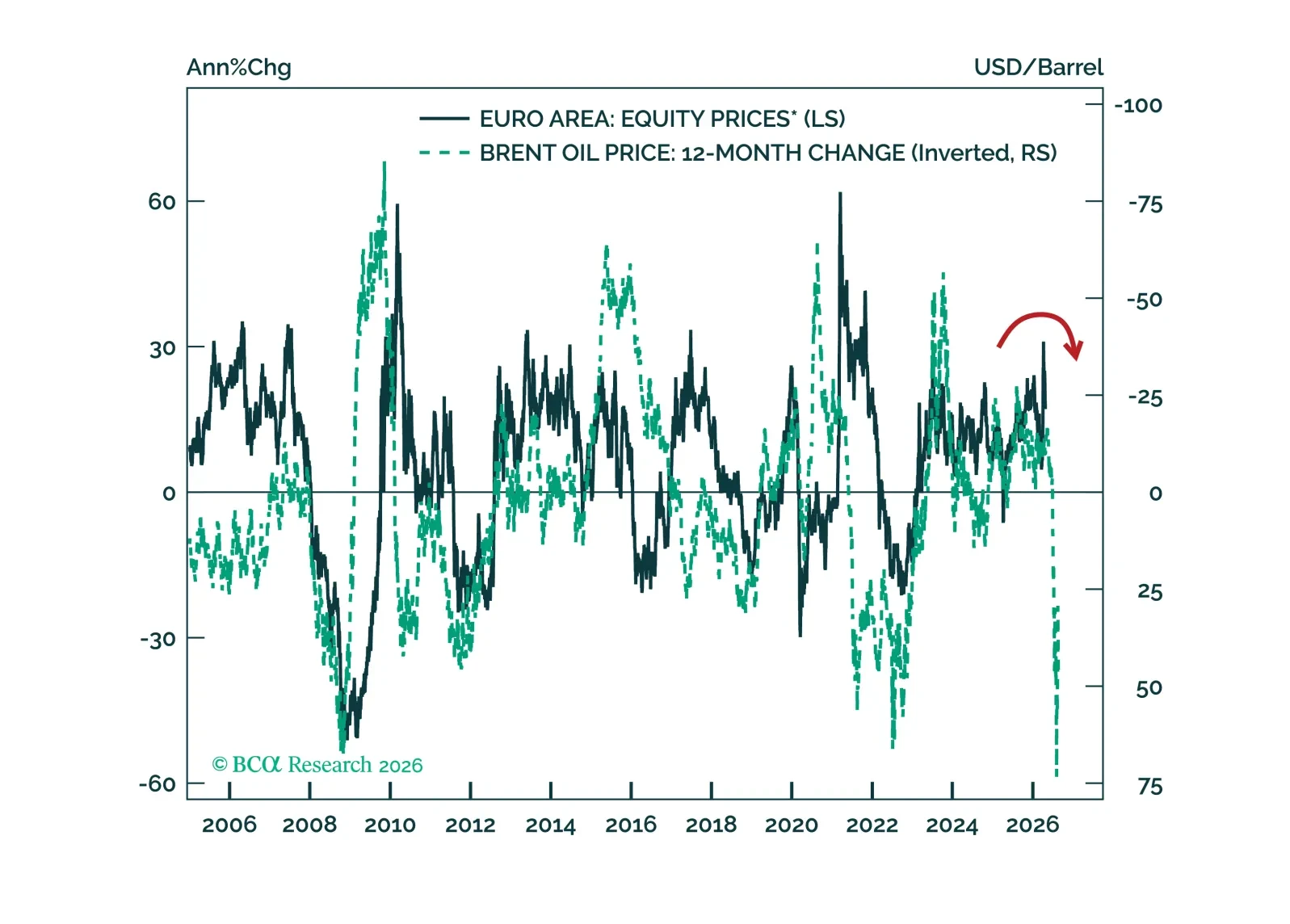

The longer the Strait of Hormuz remains closed, the more likely the Eurozone will experience an economic recession, as higher energy prices, supply chain disruptions, and weaker global demand slowly grind the European economy to a halt. The relief rally is running out of time. Investors should add exposure to the best-performing sectors following past oil supply shocks: Energy, pharma, and utilities.