Policy

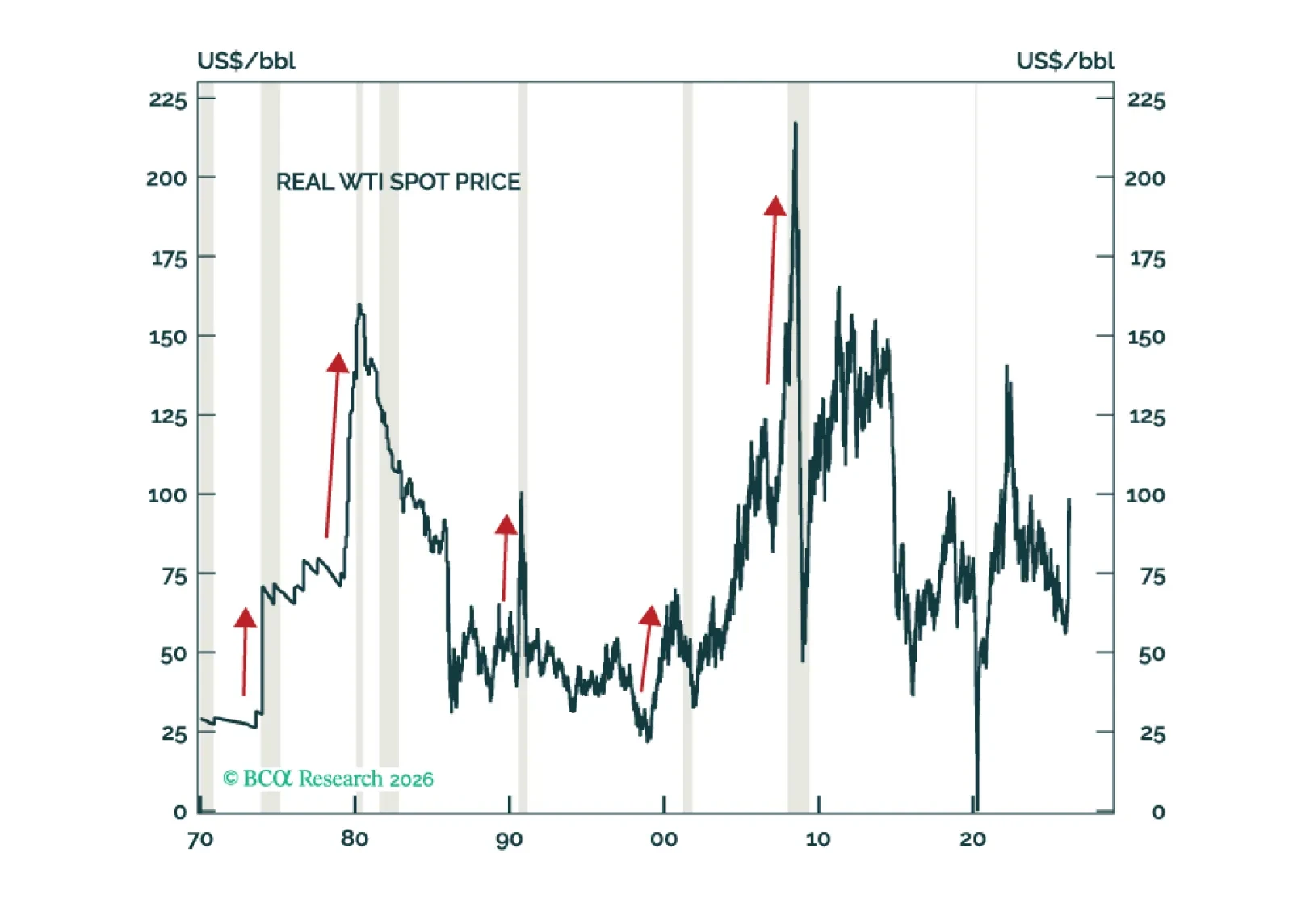

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

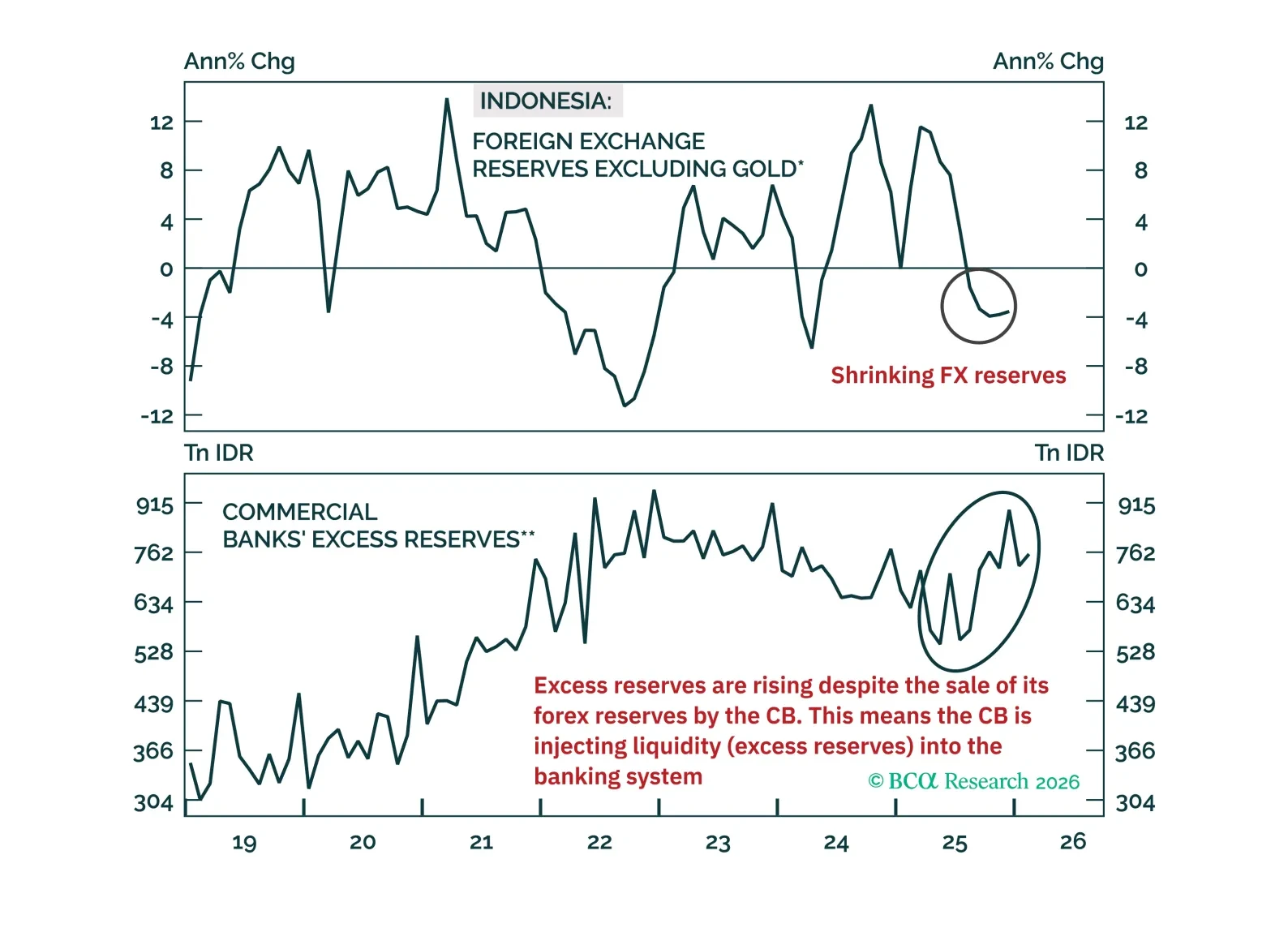

Indonesian rupiah will continue to plunge, and its local-currency bond yields will rise materially. Investors should short domestic bonds, currency unhedged.

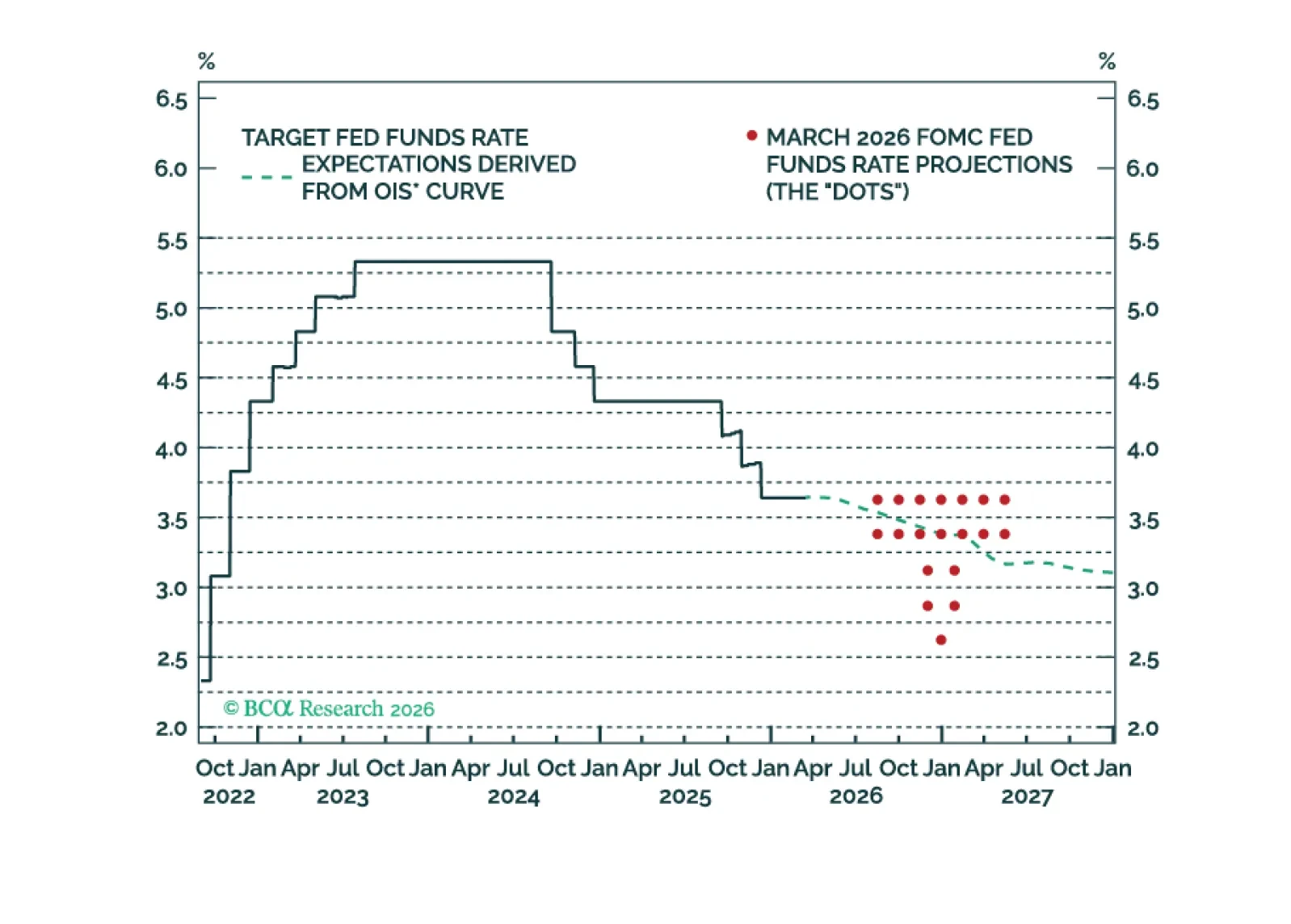

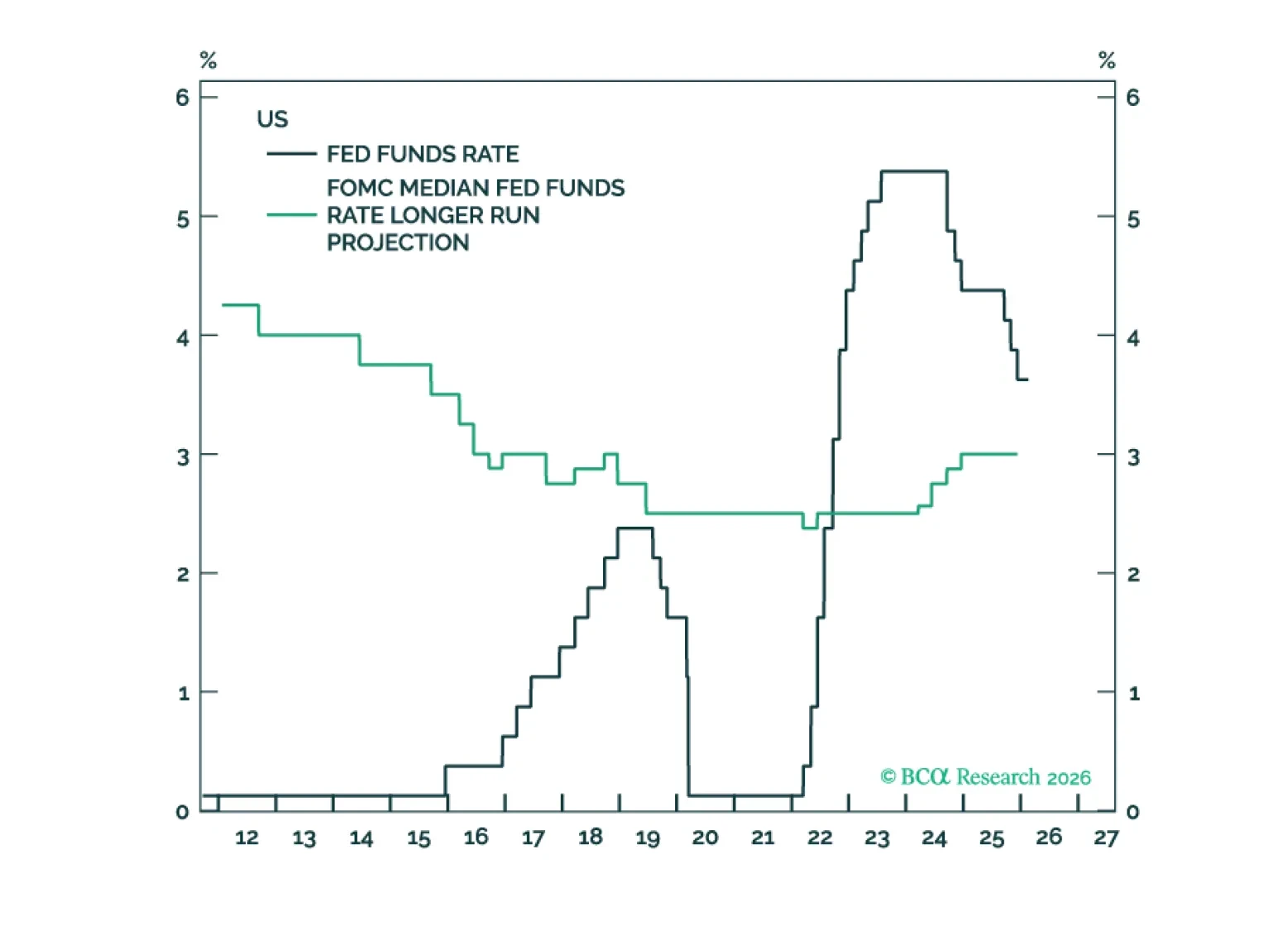

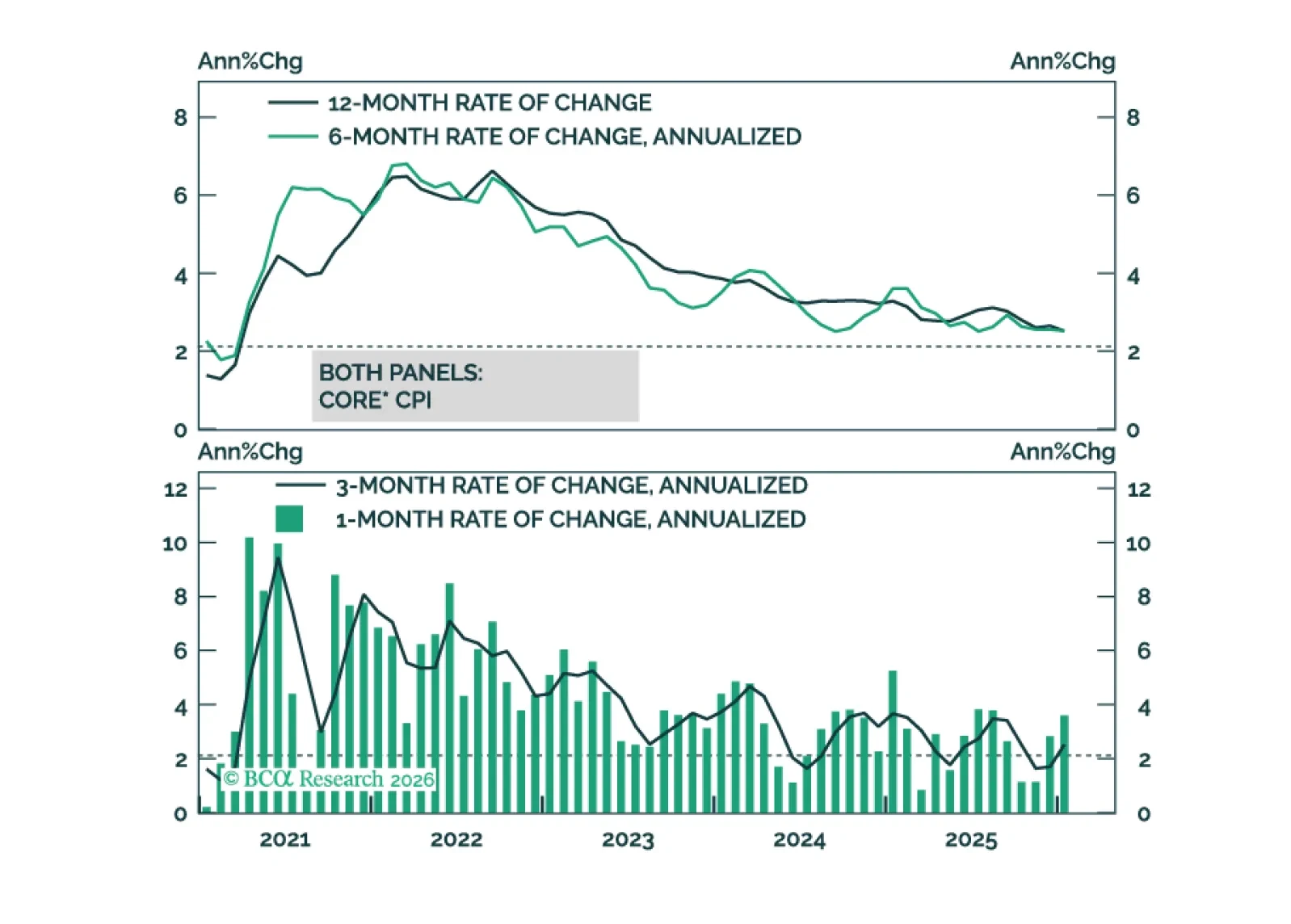

The Fed will not cut rates again until core inflation trends lower. This remains likely as the tariff impact on goods inflation wanes, but the recent energy price shock could delay any meaningful downtrend.

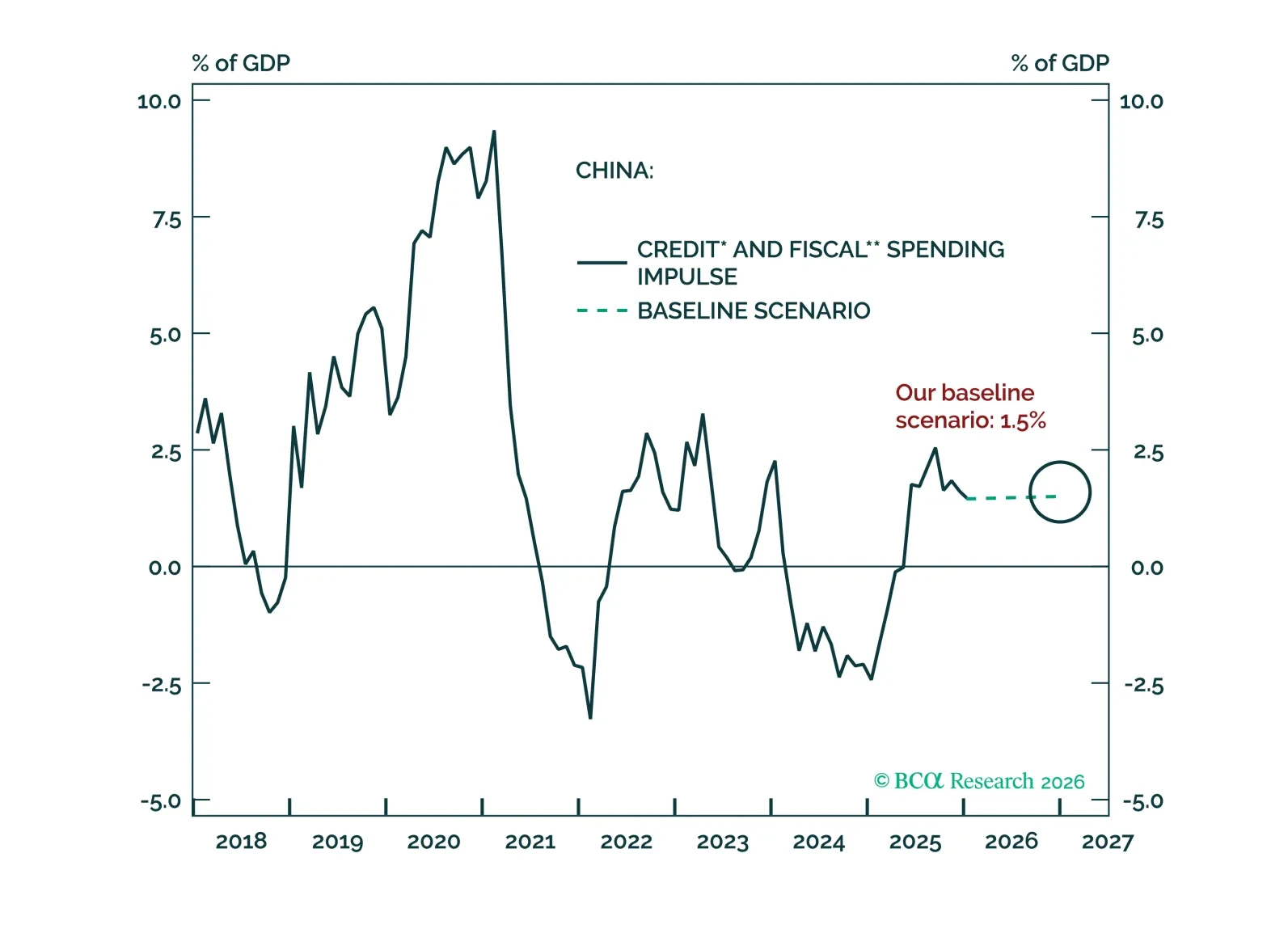

This report unpacks this year’s uneventful NPC, reading the tea leaves of key messages and offering insights on the impact of rising oil prices on China.

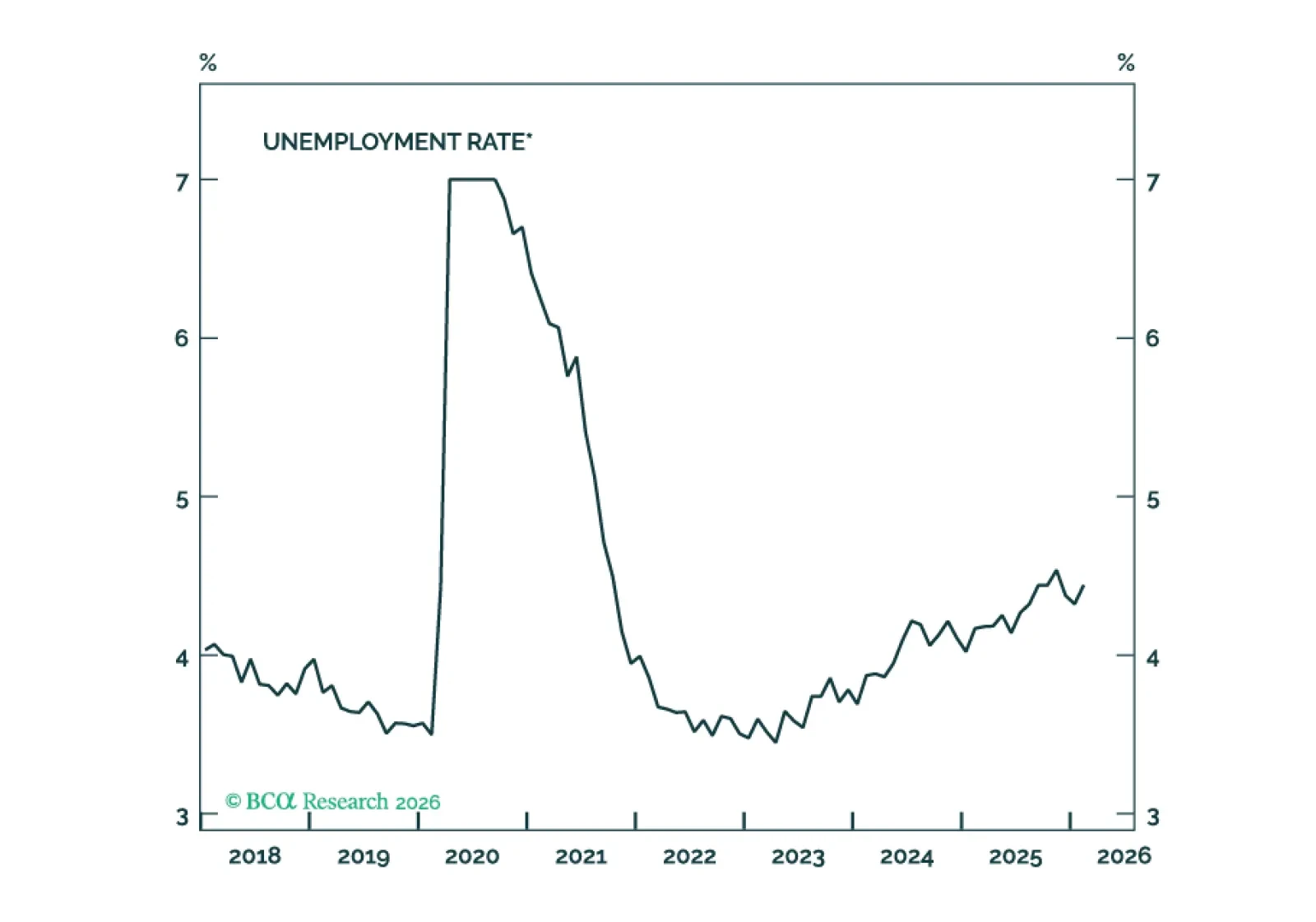

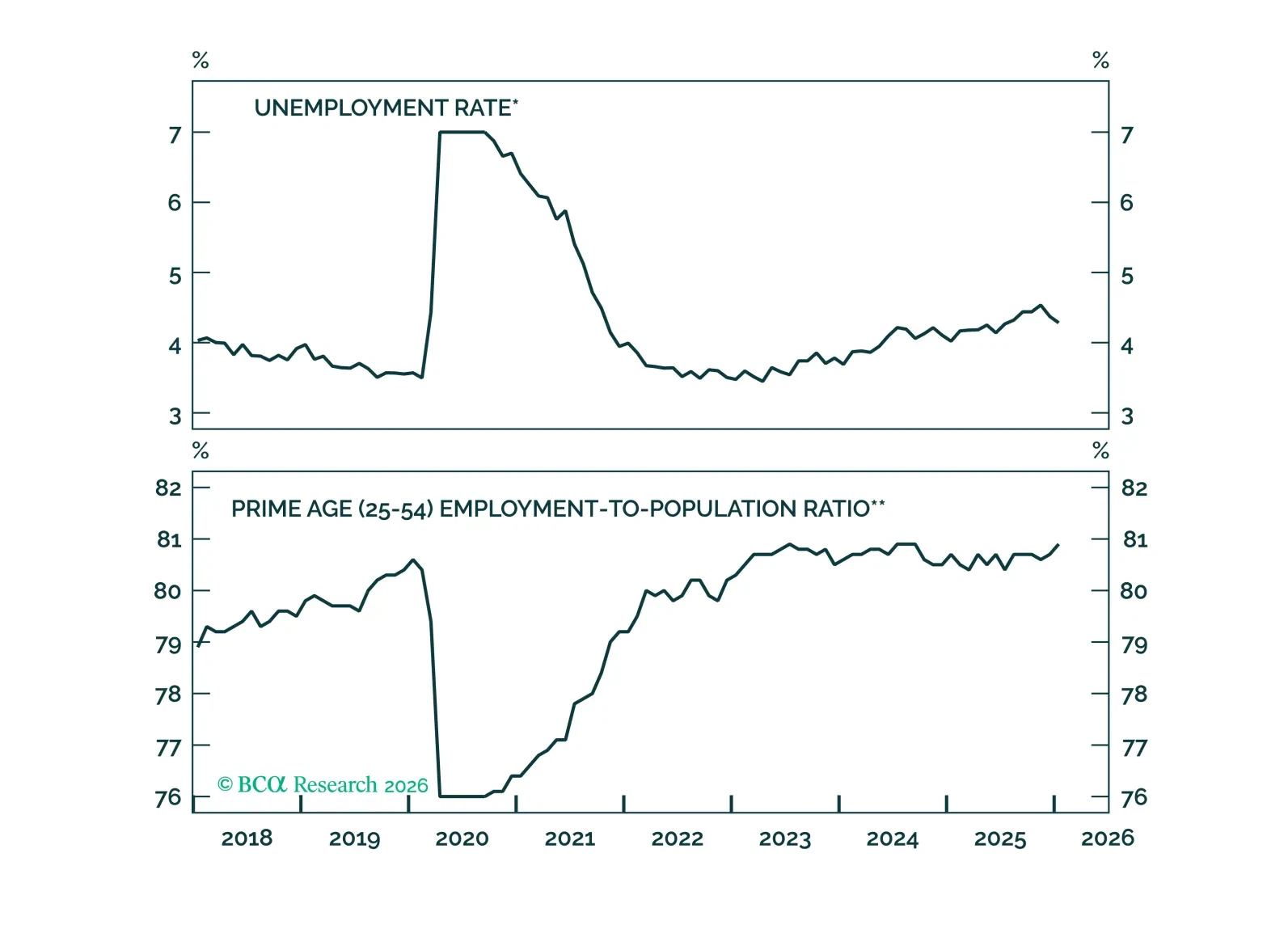

Looking through month-to-month volatility, job growth’s underlying trend is stable and consistent with a flat-to-slightly higher unemployment rate.

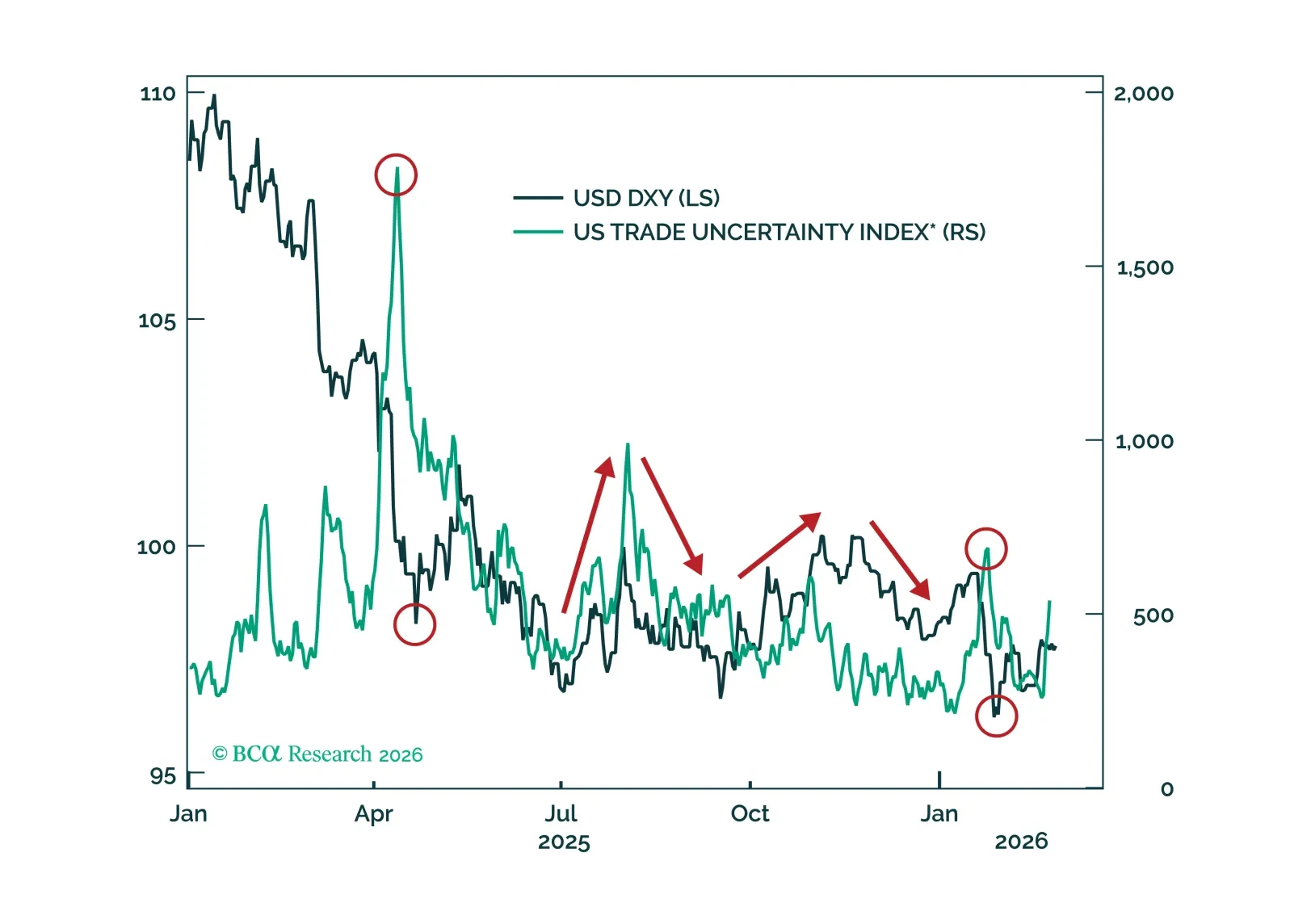

Policy risks are set to fade just as markets underestimate hawkish Fed repricing and crowd into short-USD positions, setting the stage for a tactical dollar rebound into the election cycle. Go long USD/CHF to capture the rate differential and receding policy uncertainty.

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.

Core inflation will get close to the Fed’s 2% target by the end of this year.

The labor market tightened in January, significantly lowering the odds of a H1 2026 rate cut. Rate cuts driven by lower inflation are still likely in H2 2026.

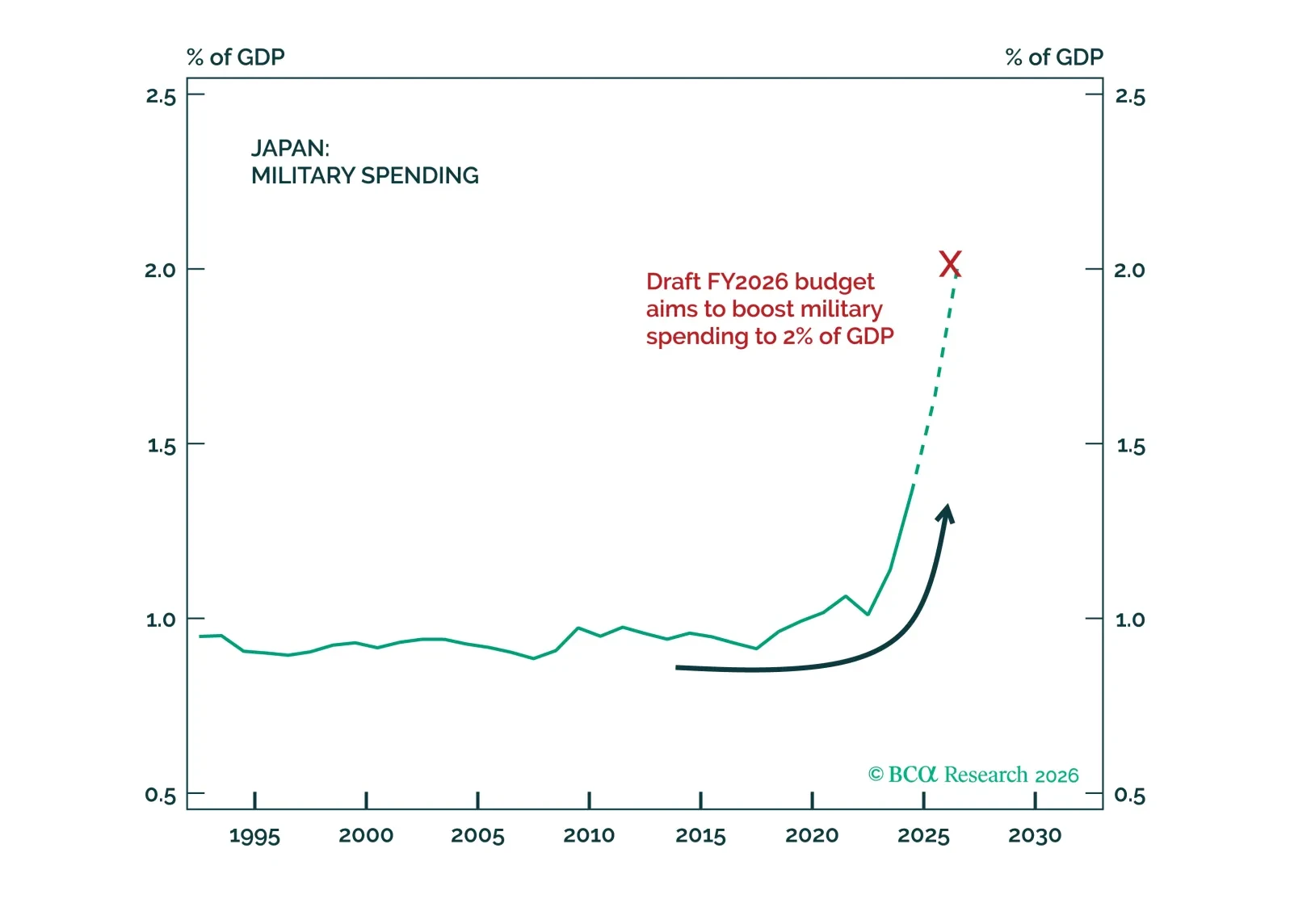

Ignore Japan's constitutional debate. Rearmament will accelerate anyway. Tech, defense stocks, and industrials will benefit. The threat to JGBs is real but will probably be contained.