Policy

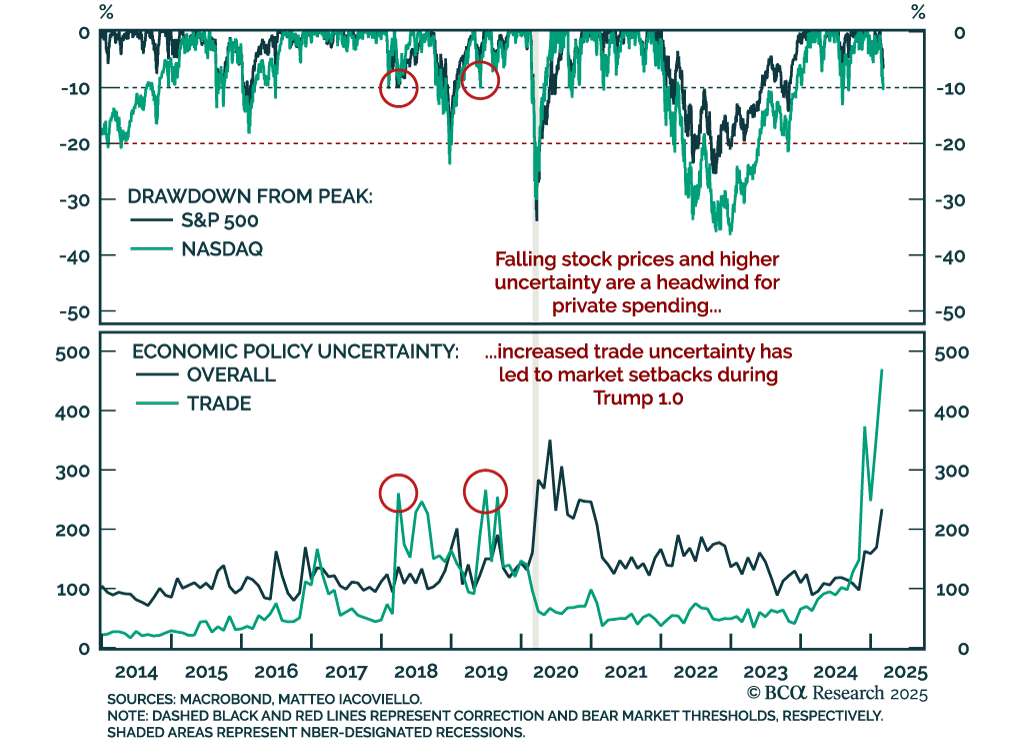

Despite our Global Investment strategists’ bearish stance, their latest report reviews scenarios that could be bullish for equities. Our colleagues remain bearish on equities, expecting a US recession this year. However, several upside scenarios could…

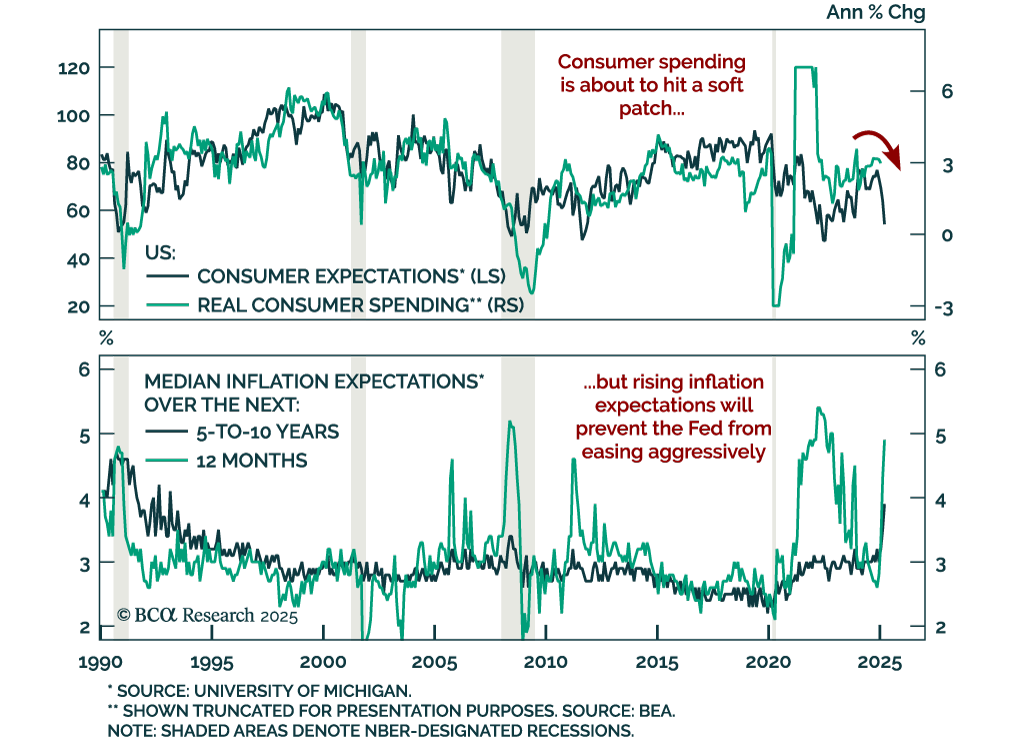

The preliminary March University of Michigan Consumer Sentiment Index missed estimates, falling to 57.9 from 64.7. The decrease came from both the assessment of current conditions and expectations, with the latter falling almost 10 points. Measures of 1-year…

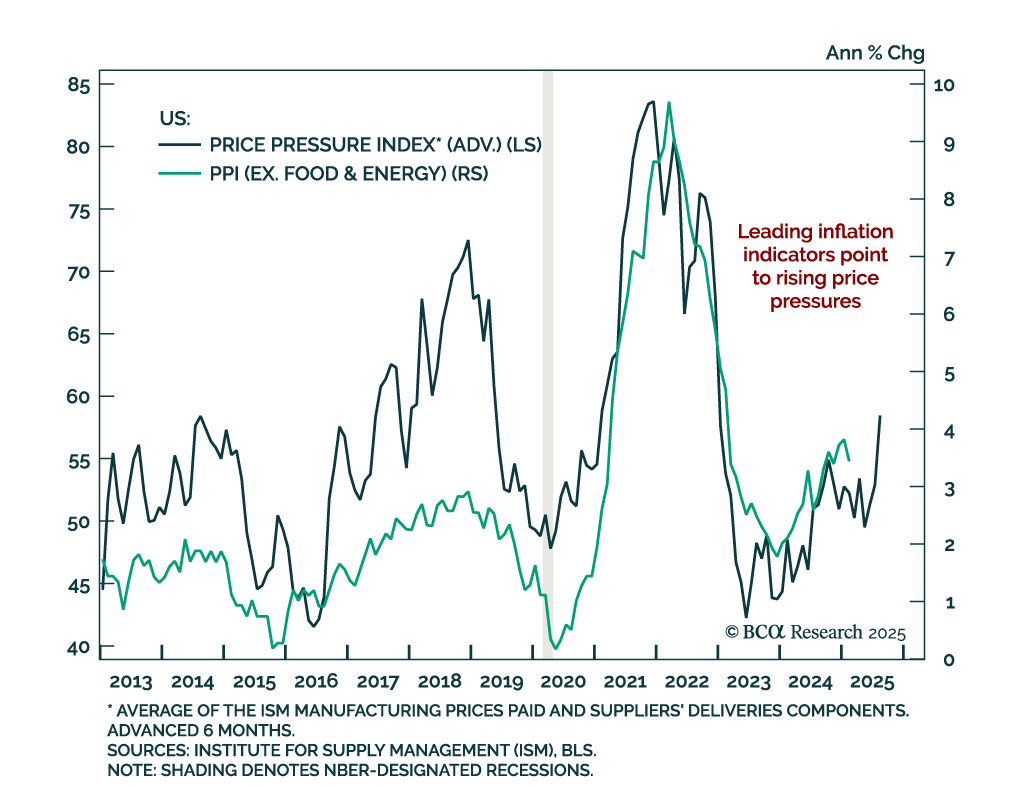

The February US Producer Price Index came in below estimates, with the headline measure showing no monthly change and standing at 3.2% y/y. Core PPI (excluding food, energy, and trade services) was also cooler than expected, coming in at 0.2% m/m (3.3%…

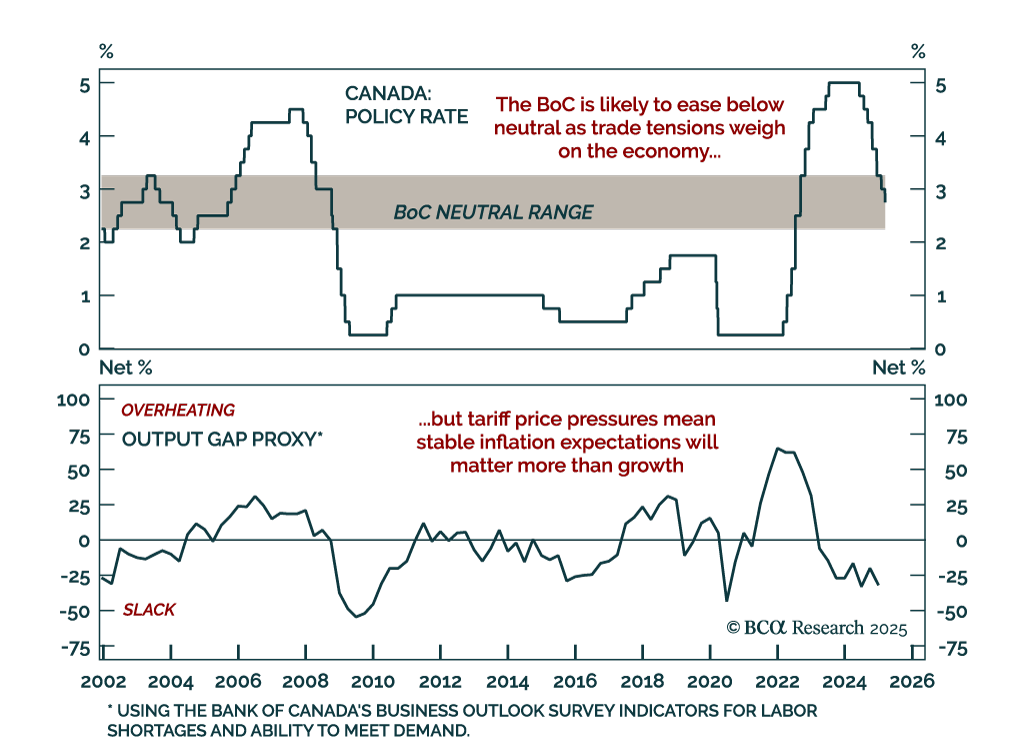

The Bank of Canada cut by 25 bps to 2.75% as expected. This seventh consecutive cut brings the policy rate further into neutral territory, estimated to be in the 2.25%-to-3.25% range. The BoC is in a tough place. The trade war will ultimately be…

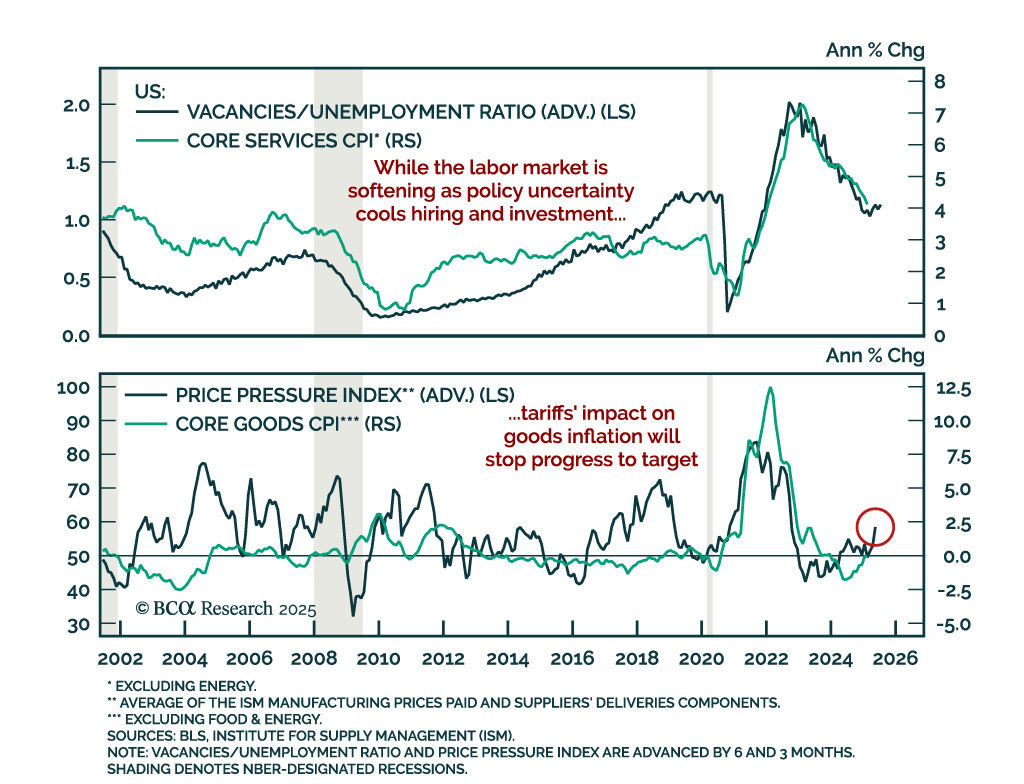

The February US CPI came in cooler than expected. Headline inflation decelerated to 0.2% m/m (2.8% y/y), as did core which now stands at 3.1% y/y. Core services inflation declined while core goods inflation was roughly unchanged. Inflation is headed…

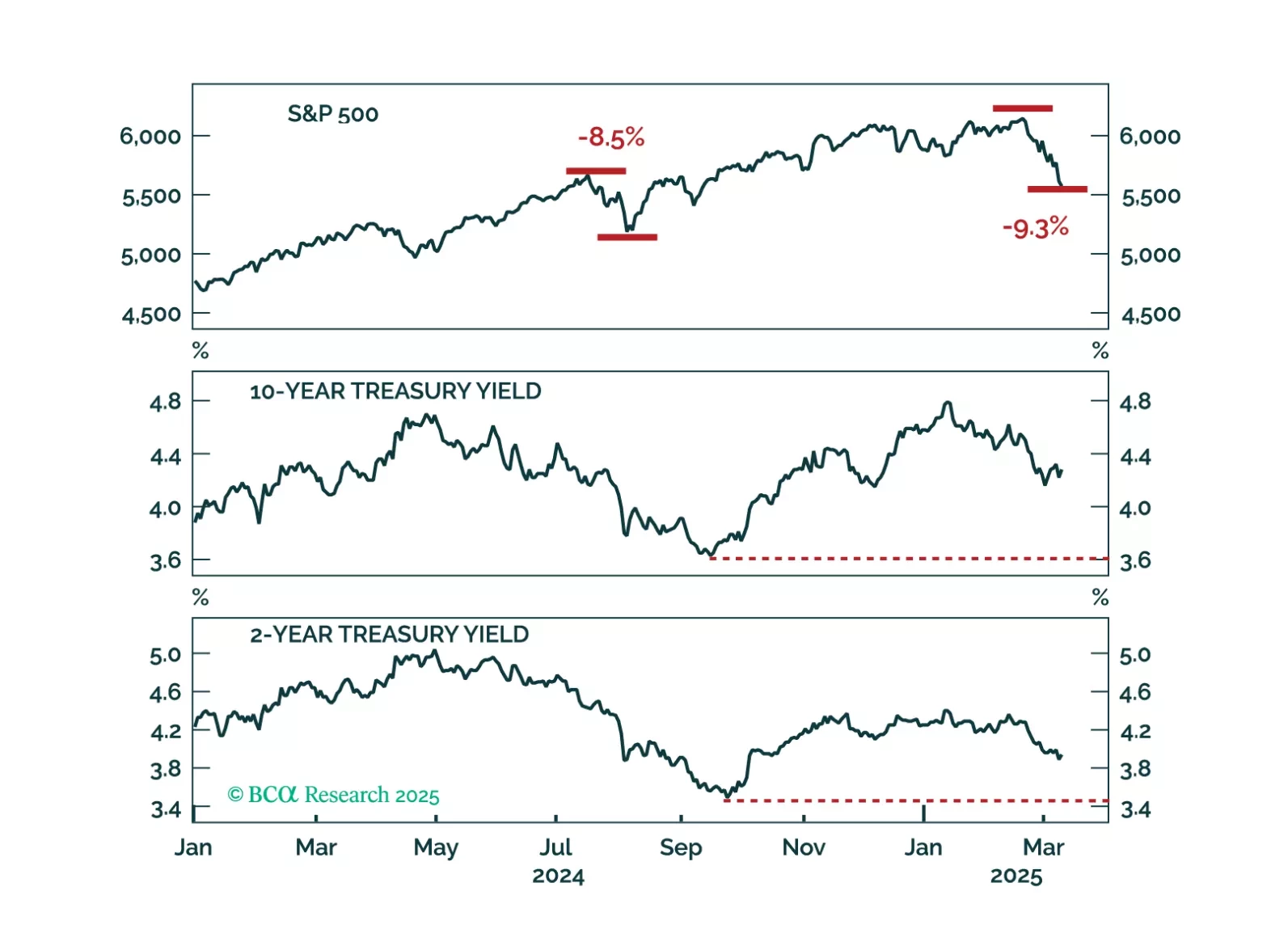

A falling stock market and sticky bond yields represent the worst of both worlds for investors. We interrogate why bond yields haven’t dropped more given the large selloff seen in equities.

开年以来,中国经济与股市走势日益分化,高科技行业和科技股持续领跑,而整体经济仍深陷通缩压力。同时,特朗普政府已两度上调对华关税,加剧了外部不确定性。在此背景下,2025 年中国经济将如何演变?两会上推出的刺激政策能否有效对冲经济下行风险?投资者又该如何适应不断变化的市场环境?

After affirming he does not look at the stock market, President Trump said he cannot exclude the possibility of a recession as he rushes to implement his agenda before the 2026 midterms. Could a President willingly start a recession? A President’s…

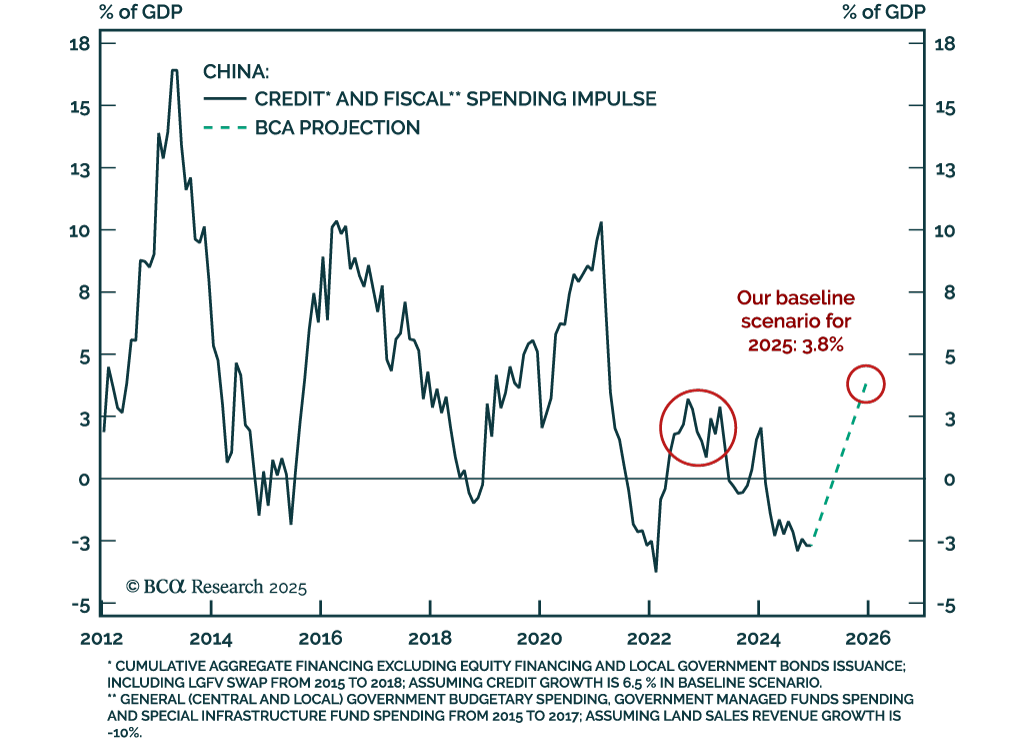

Our China and Emerging Markets strategists assessed China’s outlook after the National People’s Congress concluded last week. China’s latest fiscal stimulus is only marginally larger than last year’s, with a combined credit and fiscal impulse of 3.8% of…

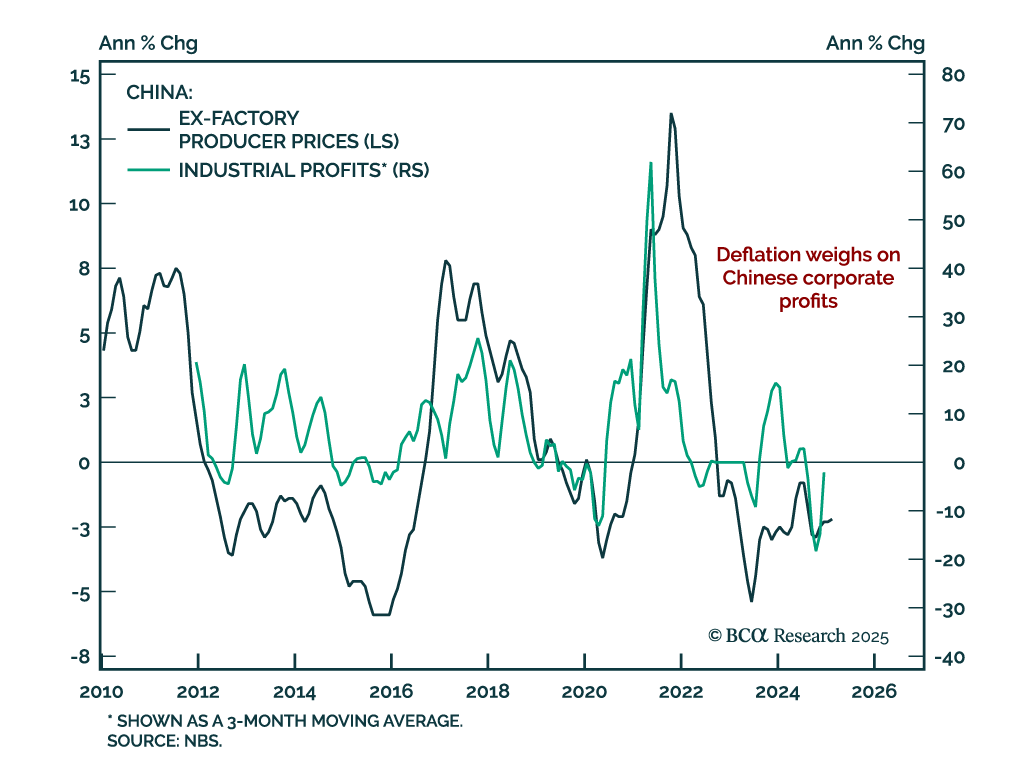

China’s February consumer prices fell 0.7% y/y after expanding on an annual basis in January. Producer price deflation stood at -2.2% y/y, roughly unchanged from a month prior. China’s first quarter data is heavily influenced by seasonality, as the shifting…