Policy

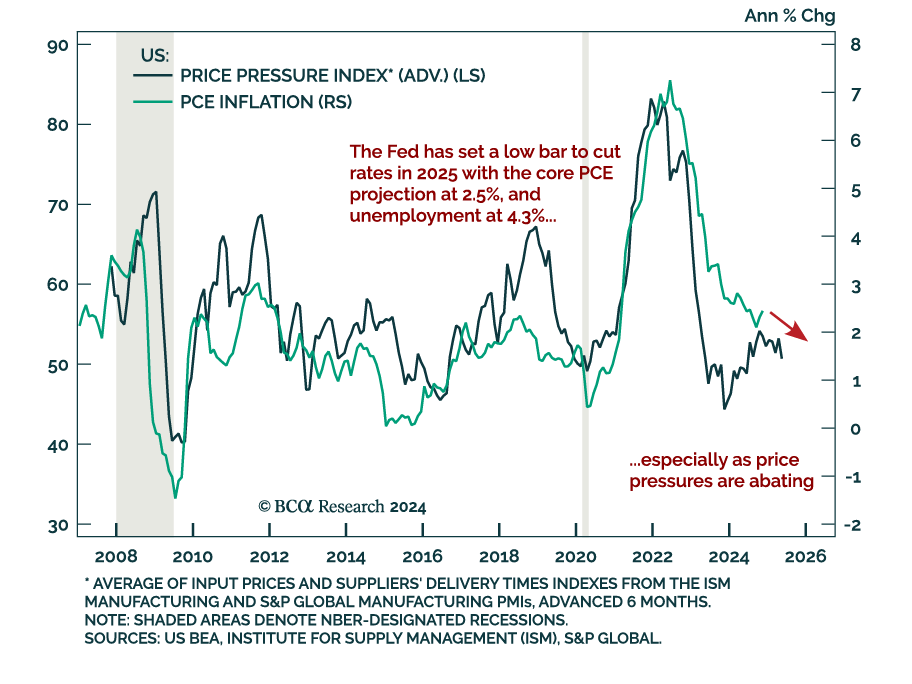

The Fed’s preferred measure of inflation, core PCE, came in below expectations at 0.1% m/m in November, remaining steady at 2.8% y/y. The monthly advance was the lowest since May. The inflation deceleration was broad-based. Core services inflation increased…

The November UK CPI, in line with estimates, hit an eight-month high, accelerating from 2.3% y/y to 2.6%. Core and services inflation were also strong at 3.5% (vs. 3.3% in October) and 5.0% (flat from October), respectively. Services inflation…

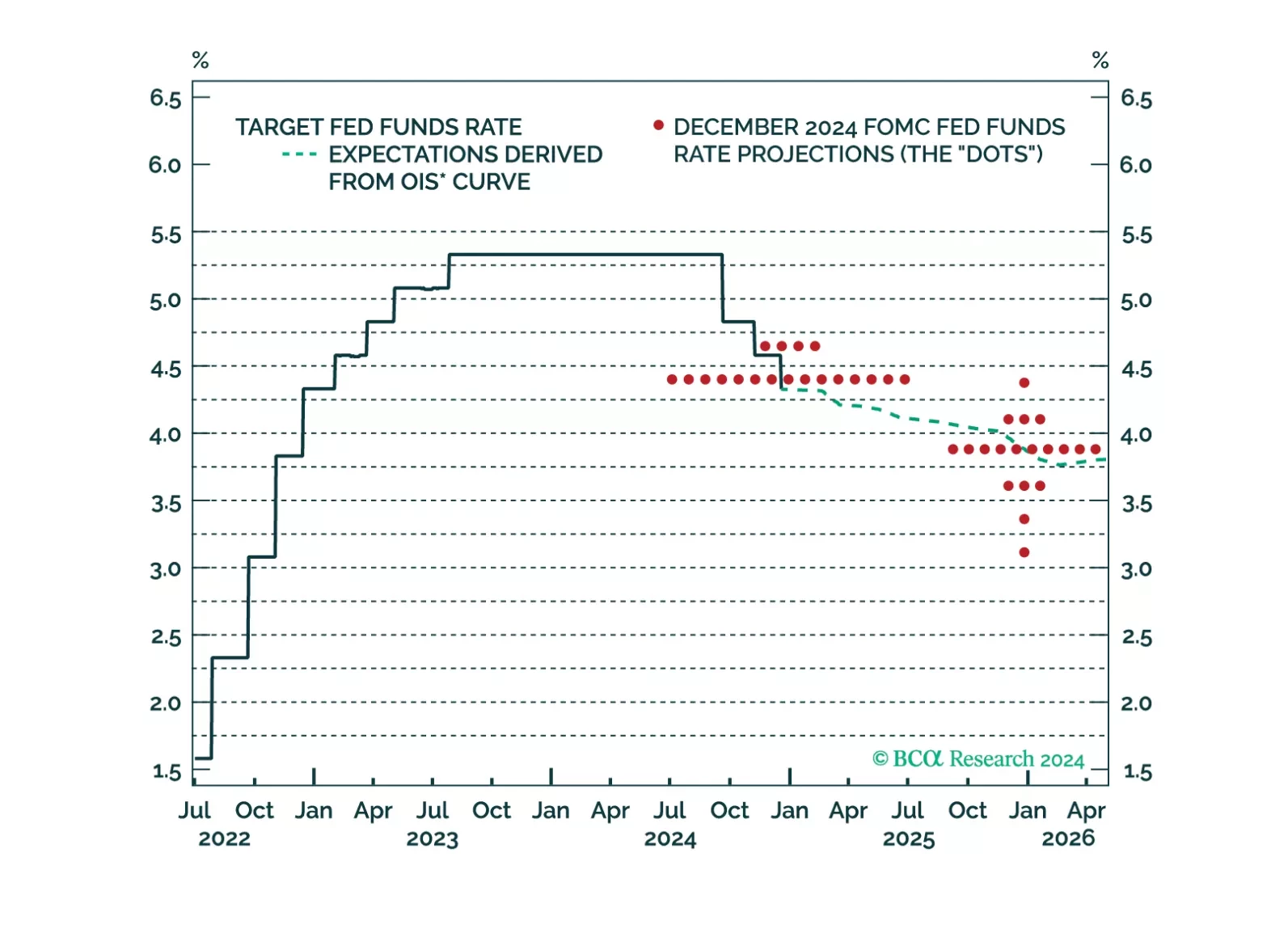

The Federal Reserve cut the fed funds rate by 25 bps to a 4.25%-4.5% range, as expected. However, it was a “hawkish cut”; the FOMC signaled a slower pace of easing ahead. The statement signalled less urgency, saying the “extent and timing” for further cuts…

Our Global Fixed Income and FX strategists published their 2025 outlook, and provide five key views for the year ahead. Duration revival: After three years of underperformance versus cash, government bonds will outperform in either a soft-landing…

Our thoughts on this afternoon’s Fed decision and the bond market reaction.

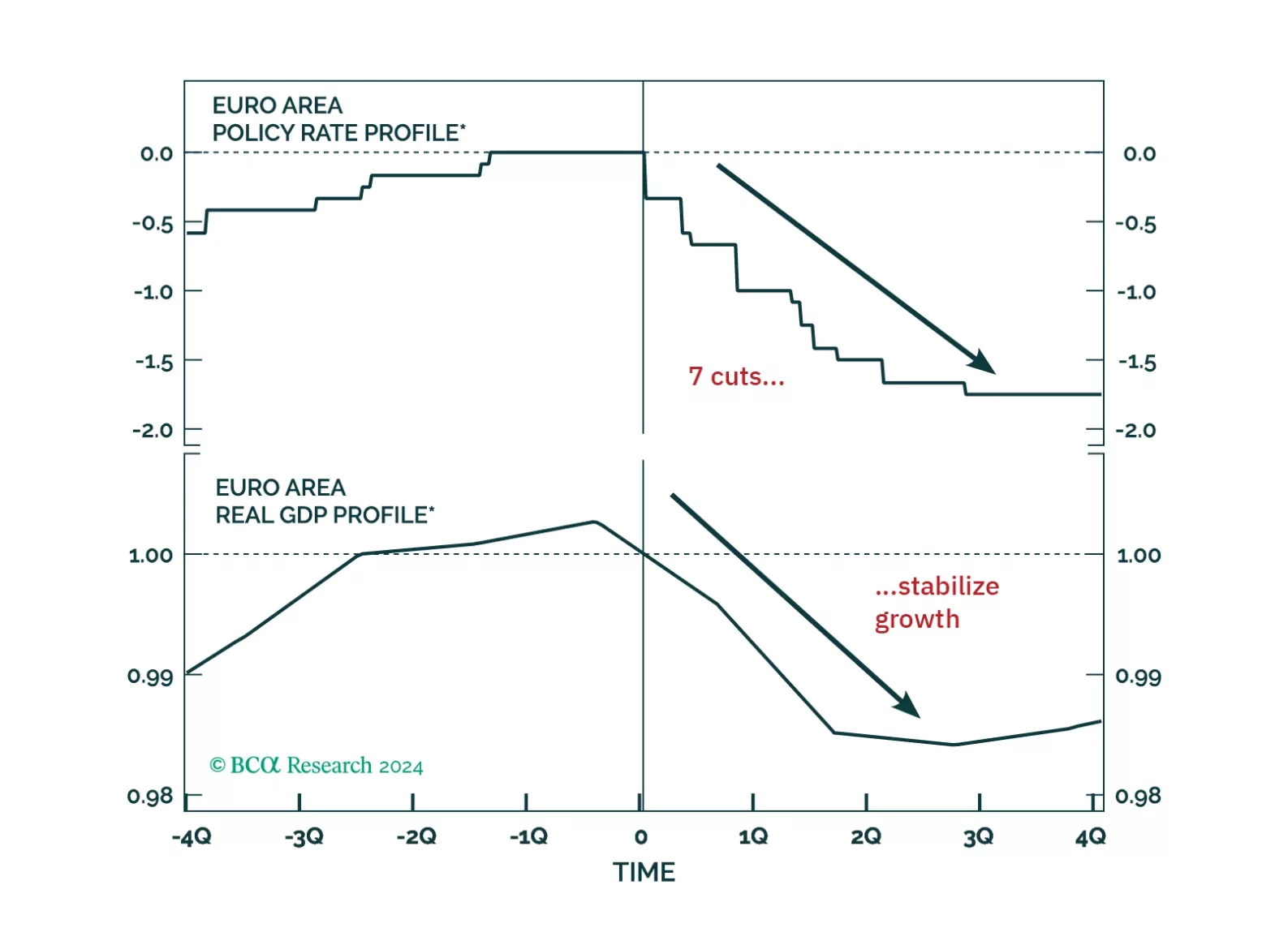

Our European Investment Strategy team published their annual outlook, outlining five key themes that will shape Europe’s economy and markets in 2025. Europe will enter a mild recession in H1 2025, but growth is expected to rebound quickly in the…

European sentiment data was mixed. The December Ifo Business Climate index for Germany missed estimates and was down 1 point to 84.7 from November. The decrease came from its expectations component, which fell to 84.4 from 87.2. Meanwhile, the December ZEW…

The November Canadian CPI was slightly below estimates, declining to 1.9% y/y from 2.0%, below the BoC’s 2% target but within the 1%-to-3% range. The BoC’s favored core measures, median and trim, were flat at 2.6% and 2.7% respectively after revisions. CPI…

For our last publication of the year, we explore five key themes that will dominate the European macro landscape and markets next year. While the start of 2025 will be challenging for European assets, the latter part will offer some much-needed relief.

The November CPI came in line with expectations, accelerating to 0.3% m/m (2.7% y/y) from 0.2% (2.6% y/y) in October. Core also printed at 0.3% m/m, the same as October and remaining at 3.3% y/y. The acceleration was mainly driven by food and used cars. …