Policy

US housing market data have been mixed. In June, the FHFA House Price index unexpectedly declined 0.1% m/m and the NAHB housing market index unexpectedly eased to 39 from a 41 reading. In July, starts and permits both disappointed, contracting 6.8% and 4.0%…

Last week, economists polled by Bloomberg revised their consensus 2024 US GDP forecasts upwards, from 2.3% to 2.5%. Government spending and private investment were both revised 0.3 ppts higher to 3.0% and 3.9%, respectively, while consumption growth forecasts…

The market is currently expecting the Fed to cut rates by 100 bps over the course of 2024 and by another 120 bps throughout the first eight months of 2025. However, our Global Investment strategists expect the extent of 2024 rate cuts to undershoot…

Chinese industrial profits rose by 4.1% y/y (3.6% YTD y/y) in July, from 3.6% (3.5%) in June. Upstream mining industries’ profits contracted 9.5% from January to July 2024, whereas downstream manufacturing sectors’ profits rose 5.0%. The NBS reported that…

During his Jackson Hole speech, Chair Powell dispelled any remaining doubts about a September rate cut. Still, easing monetary policy is unlikely to result in a soft landing. First, recessions have historically started shortly after the Fed began cutting…

The Conference Board’s Consumer Confidence measure surprised to the upside in August, rising from 100.3 to 103.3, above expectations of 100.7. Consumers’ assessment of present economic conditions climbed 0.8 points to 134.4, while their expectations about the…

According to BCA Research’s European Investment Strategy service, Sweden, which acts as a bellwether for the global economy, will offer early insight into whether our base-case late 2024/early 2025 recession scenario will come to fruition. This Nordic country…

The equal-weighted S&P 500 index reached a new all-time high of 7,096.12 on Monday. Chair Powell’s comments at the Jackson Hole Symposium last week dispelled any remaining doubt about a September rate cut and sent smaller stocks higher. The Russell…

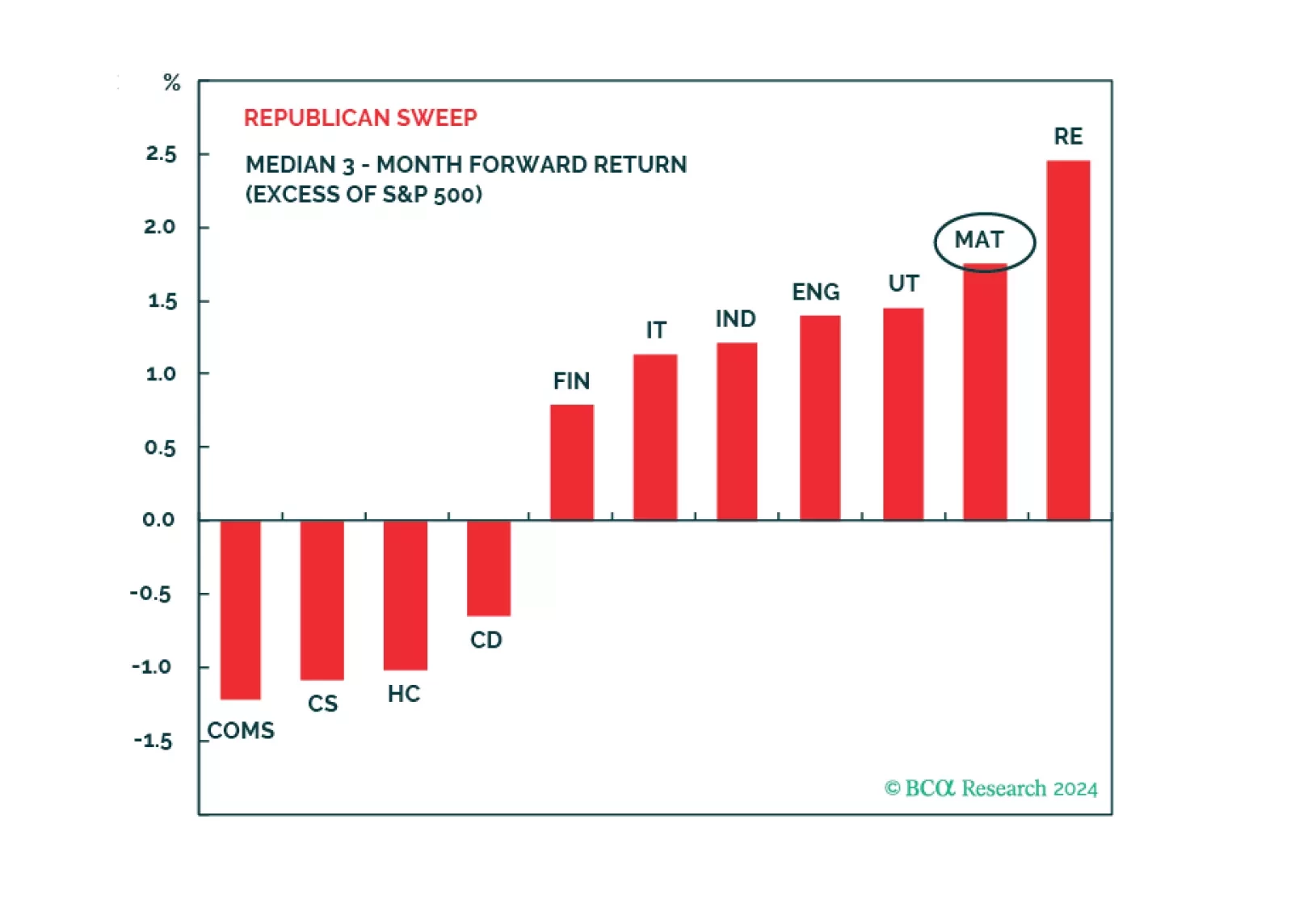

According to BCA Research’s US Political Strategy service, in the final months of an election cycle, equities underperform relative to non-election years. This extends further into Q1 of the following year due to uncertainty. Once the election results are…

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.