Policy

The Canadian economy added 90.4 thousand jobs in April, up from a new loss of 2.2 thousand jobs in March. The April reading beat expectations of a more moderate increase of 20 thousand. The services sector entirely explains April’s employment growth; services…

Preliminary GDP estimates suggest that the UK economy started growing again in Q1, thus exiting a technical recession in the past two quarters. Q1 growth came in at 0.6%, improving from a 0.3% contraction last quarter, surpassing expectations of 0.4%. On a…

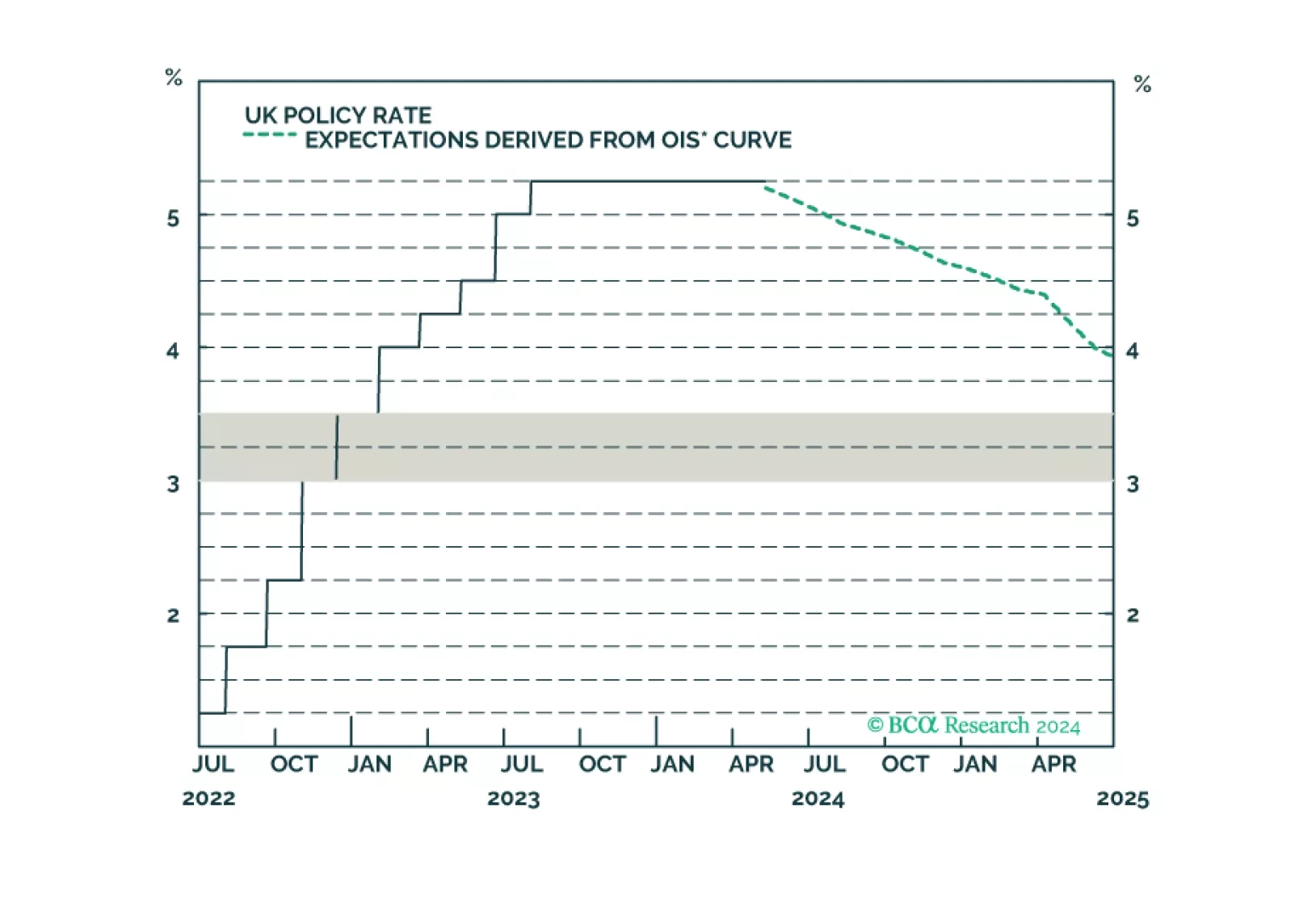

In a widely expected move, the Bank of England (BoE) maintained its policy rate at 5.25% in May. Nevertheless, two Committee Members voted in favor of cutting rates, one more than was anticipated. The tone of the report was overall dovish. The BoE…

An update to our views on UK rates and currency following today’s Bank of England meeting.

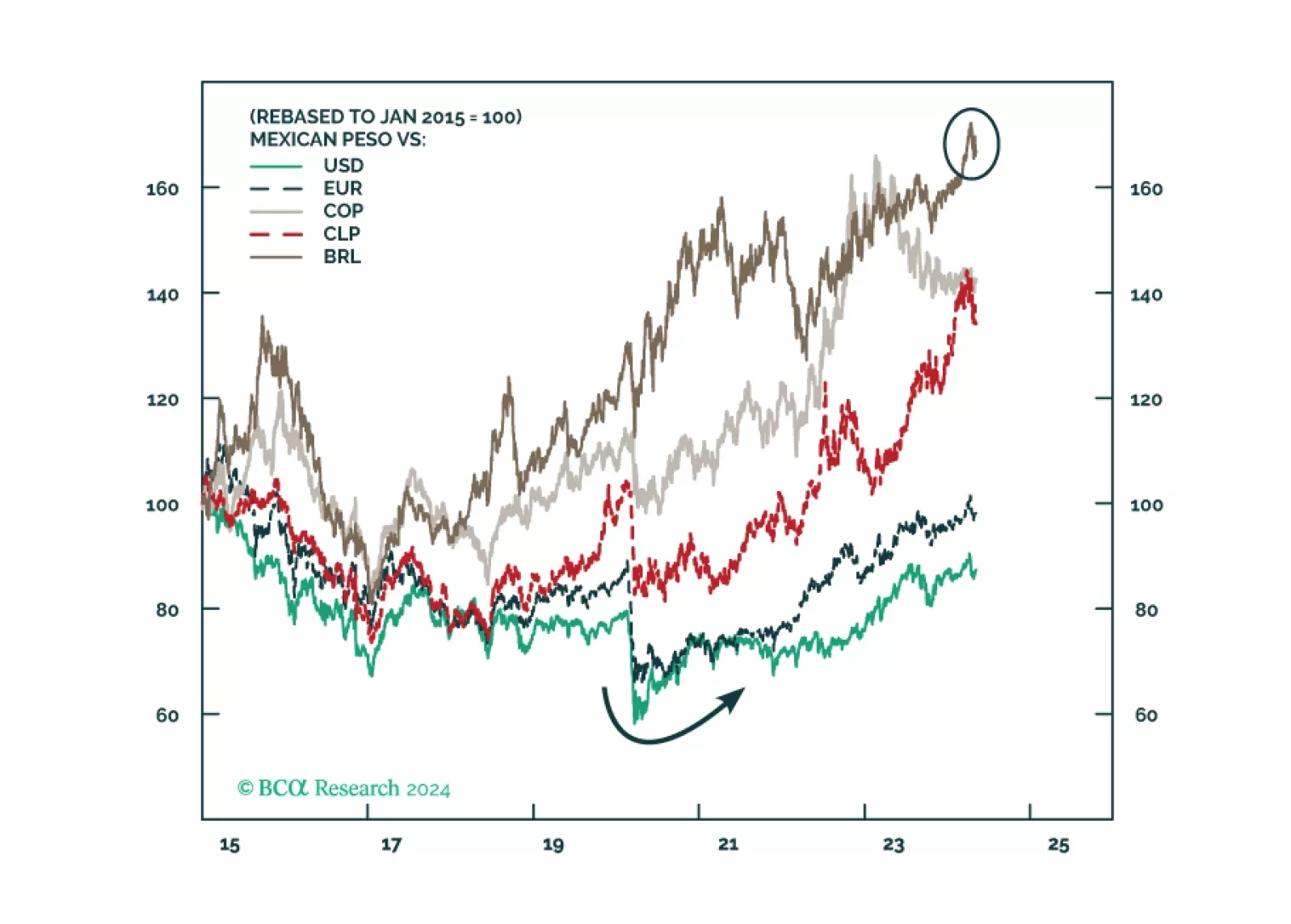

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

In a widely expected move, the Riksbank cut its policy rate by 25 basis points on Wednesday from 4% to 3.75%. The policy statement highlighted that inflation is approaching its 2% target, that leading indicators are pointing to further downside in prices and…

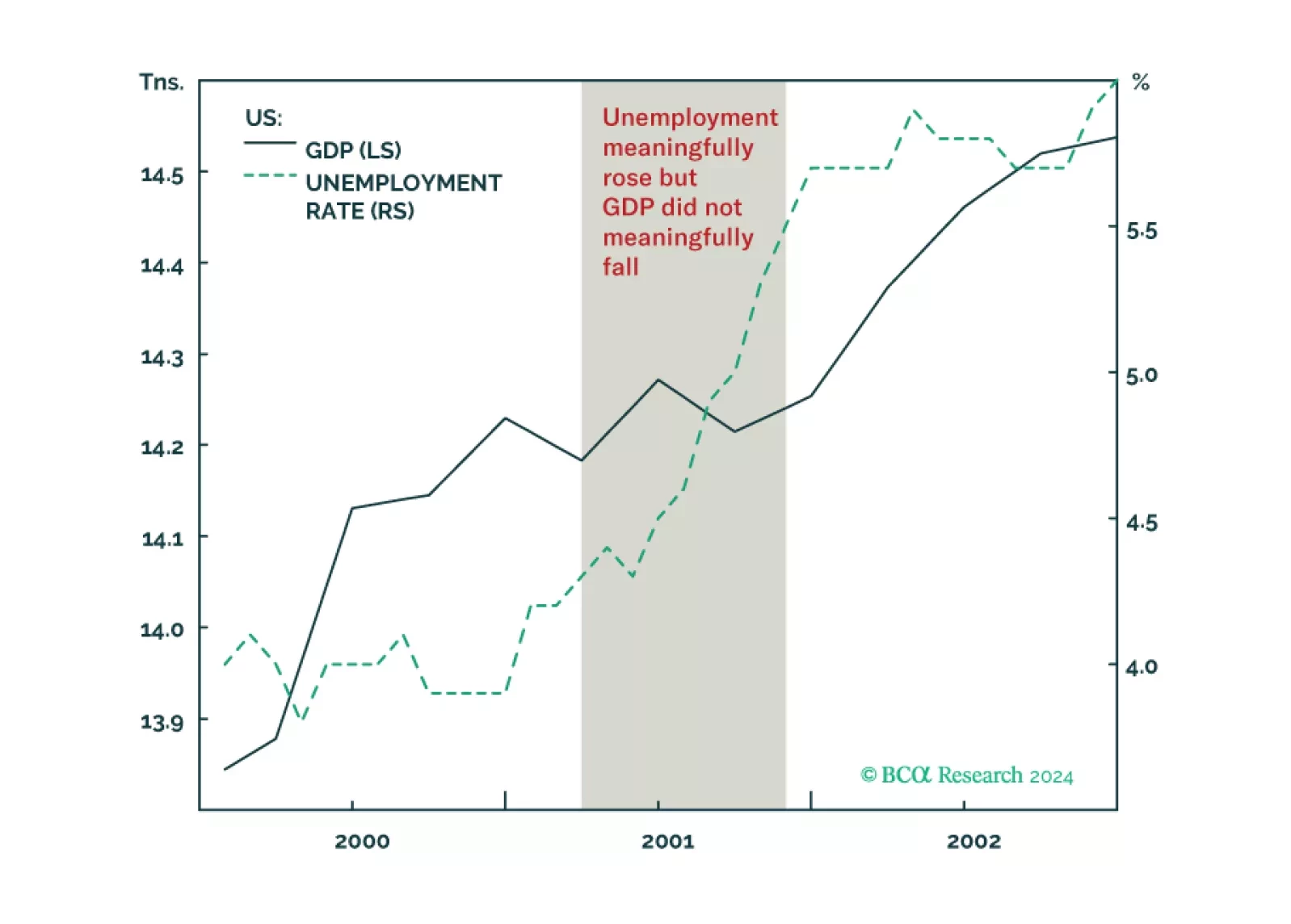

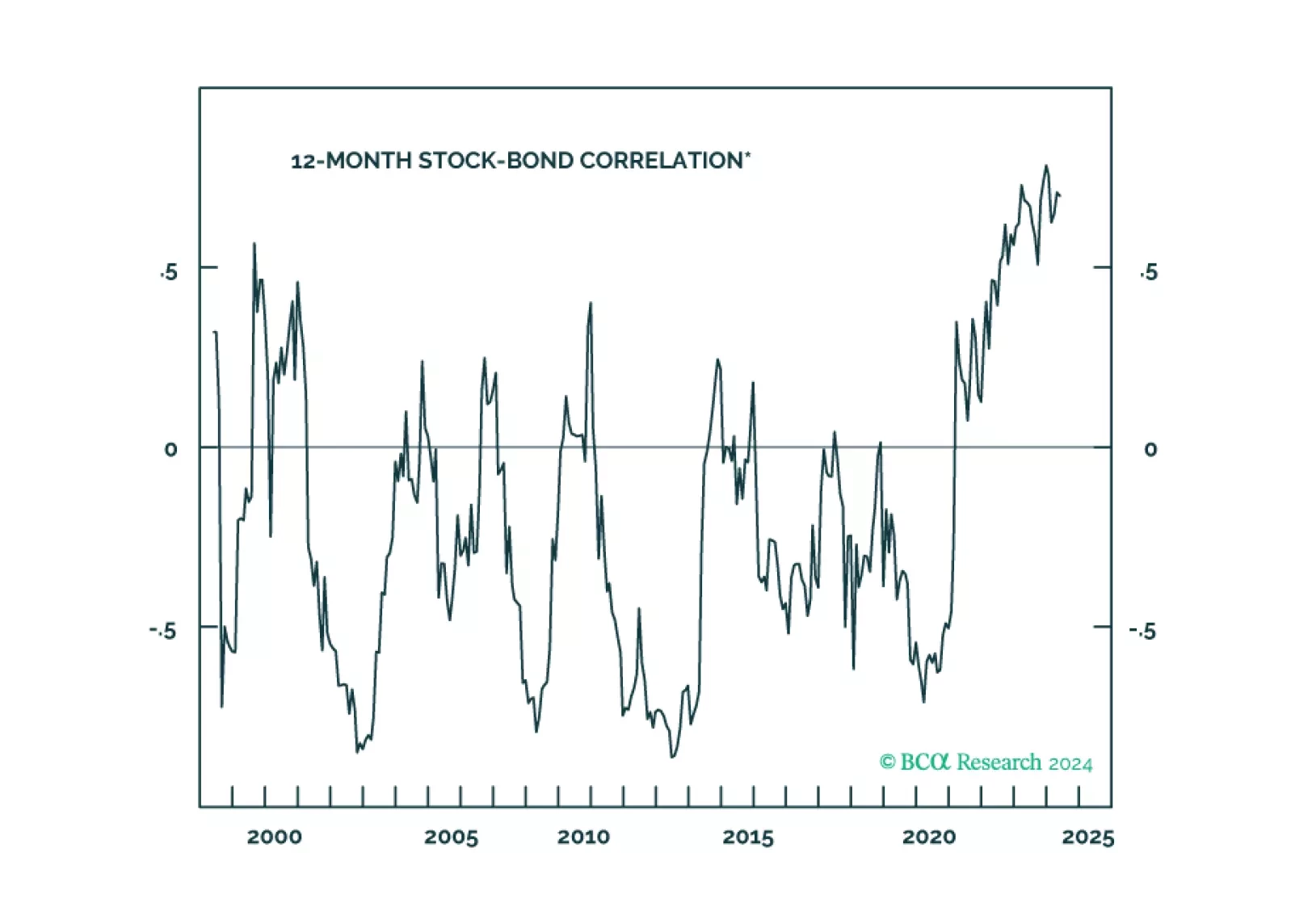

Why the US could get a jobs recession without a GDP recession, as happened in 2001, and what it means for stocks and bonds. Plus, an update on the Joshi rule.

The Reserve Bank of Australia (RBA) left its policy rate unchanged at 4.35% at its May meeting, in line with expectations. The statement highlighted that inflation continues to moderate, though at a slower-than-expected pace. Board members also pointed out…

Transit through the Suez Canal has hit a new low. The 7-day moving average of daily ship transit calls is currently at 30, less than half of what it was at the end of 2023. The decline in volume has been even more severe, with metric tons passing through the…

Our Portfolio Allocation Summary for May 2024.