Recession-Hard/Soft Landing

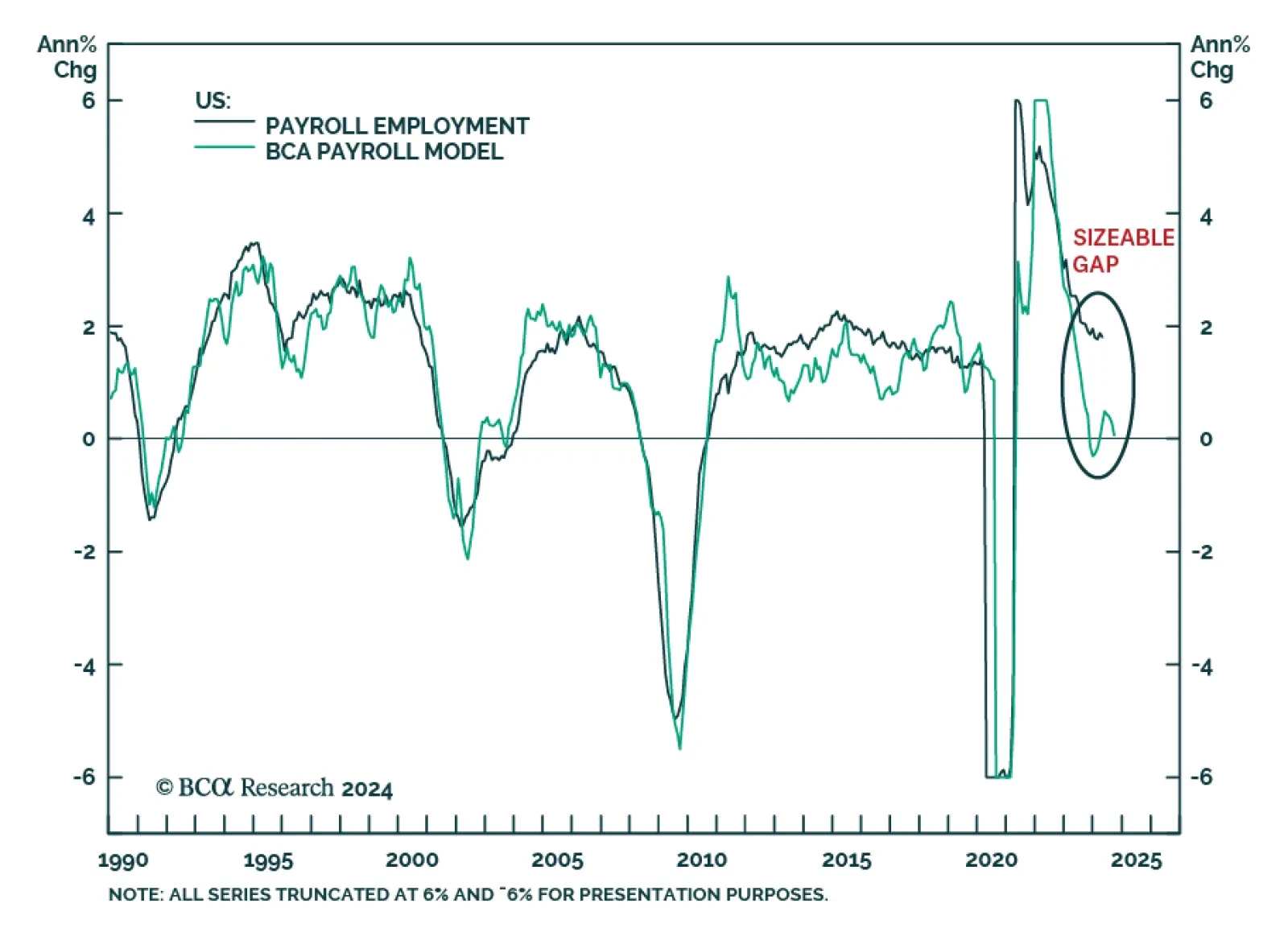

At BCA Research, fundamentals drive our analysis and we use indicators and quantitative metrics as guides to inform our views further. It is our fundamental assessment of the US labor market that underpins our view that softer labor demand and decelerating…

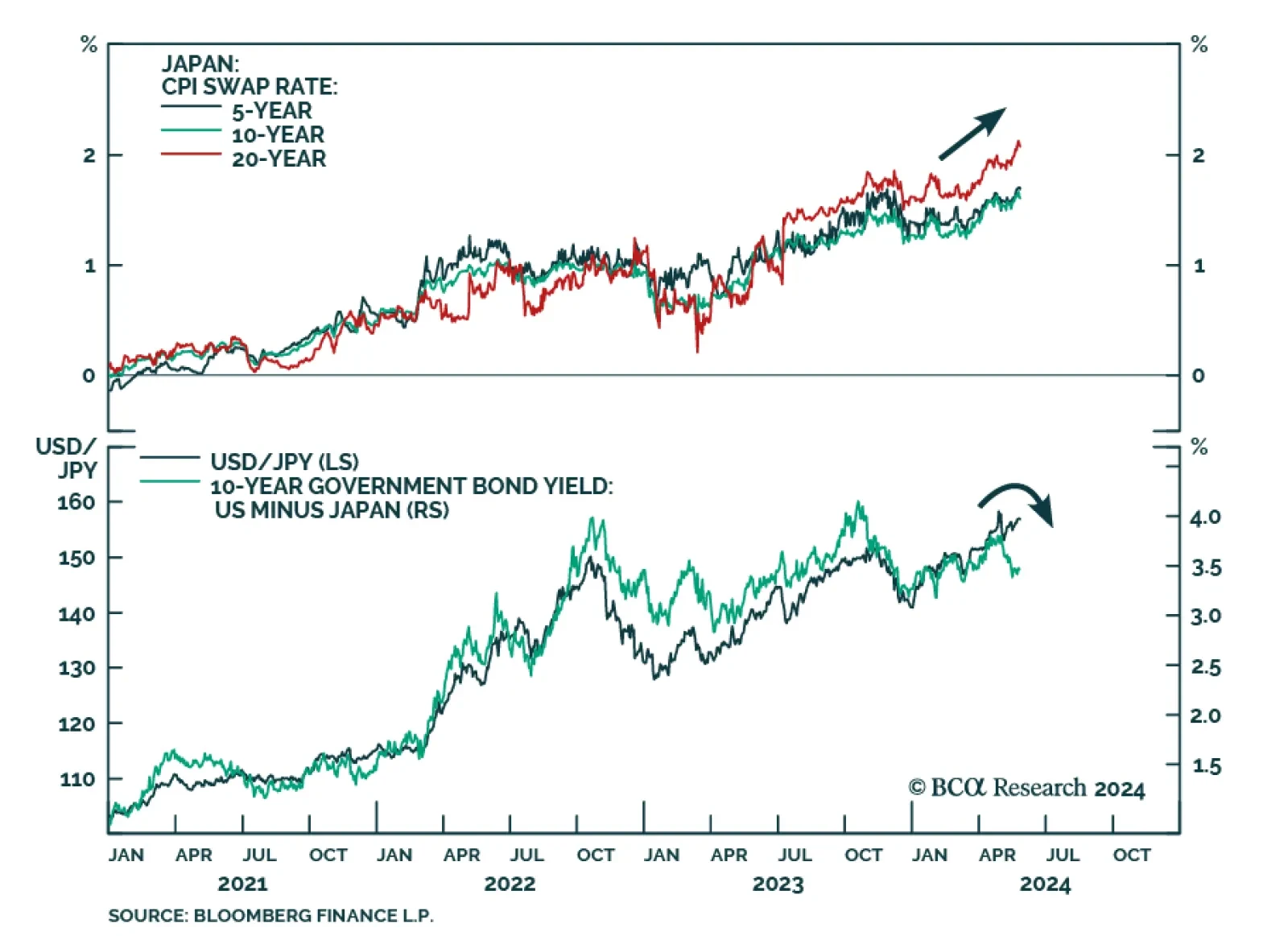

Our Global Investment strategists highlighted back in November 2022 that structural deflationary forces in Japan were weakening, thus setting the stage for inflation to make a historic comeback in Japan. About a year later, they highlighted that 2024…

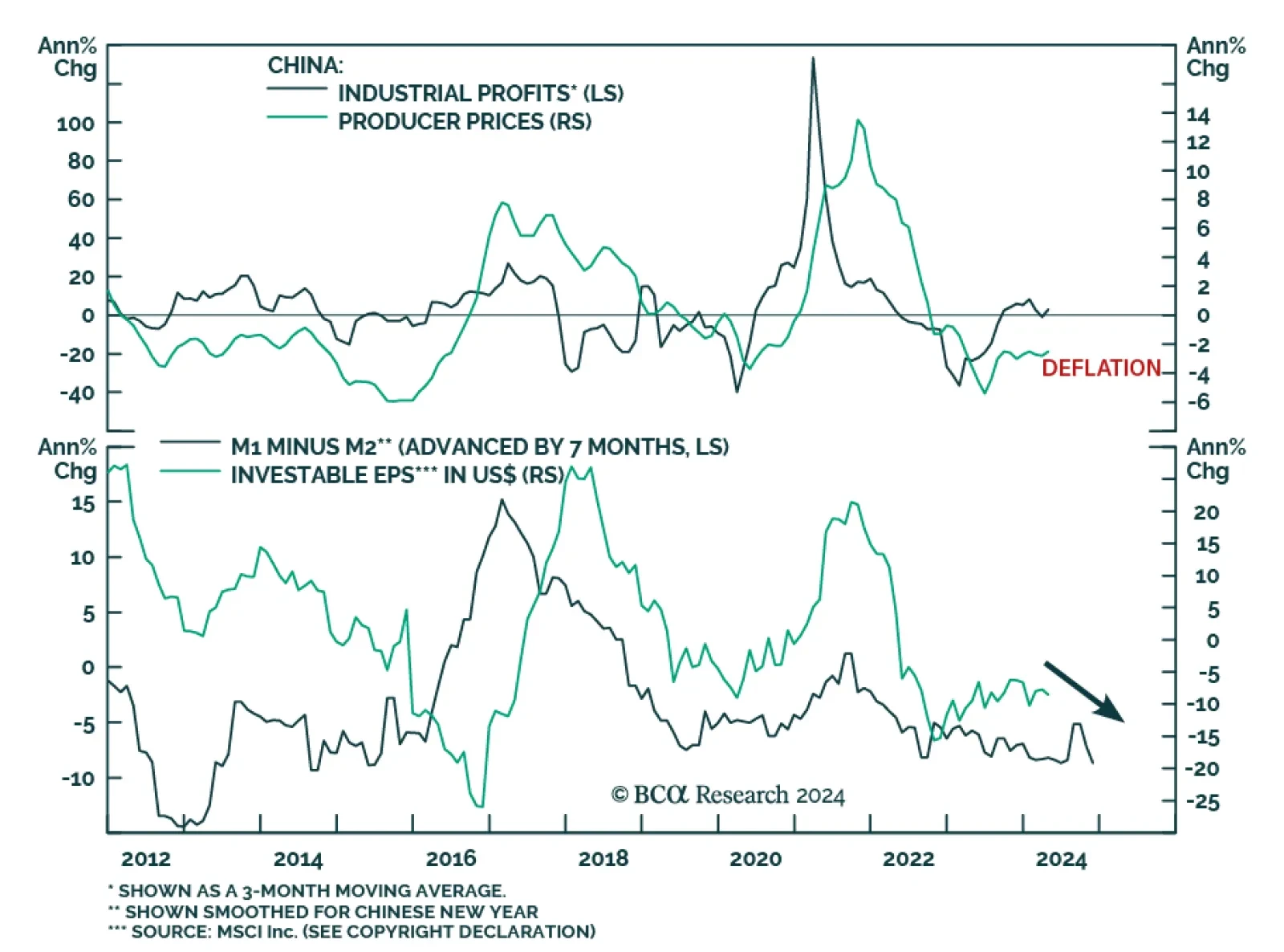

Chinese industrial profits rose by 4.0% y/y in April, from a 3.5% y/y contraction in March. They grew by 4.3% in the first four months of the year, compared to the same period in 2023. In March, the central government pledged funds to incentivize…

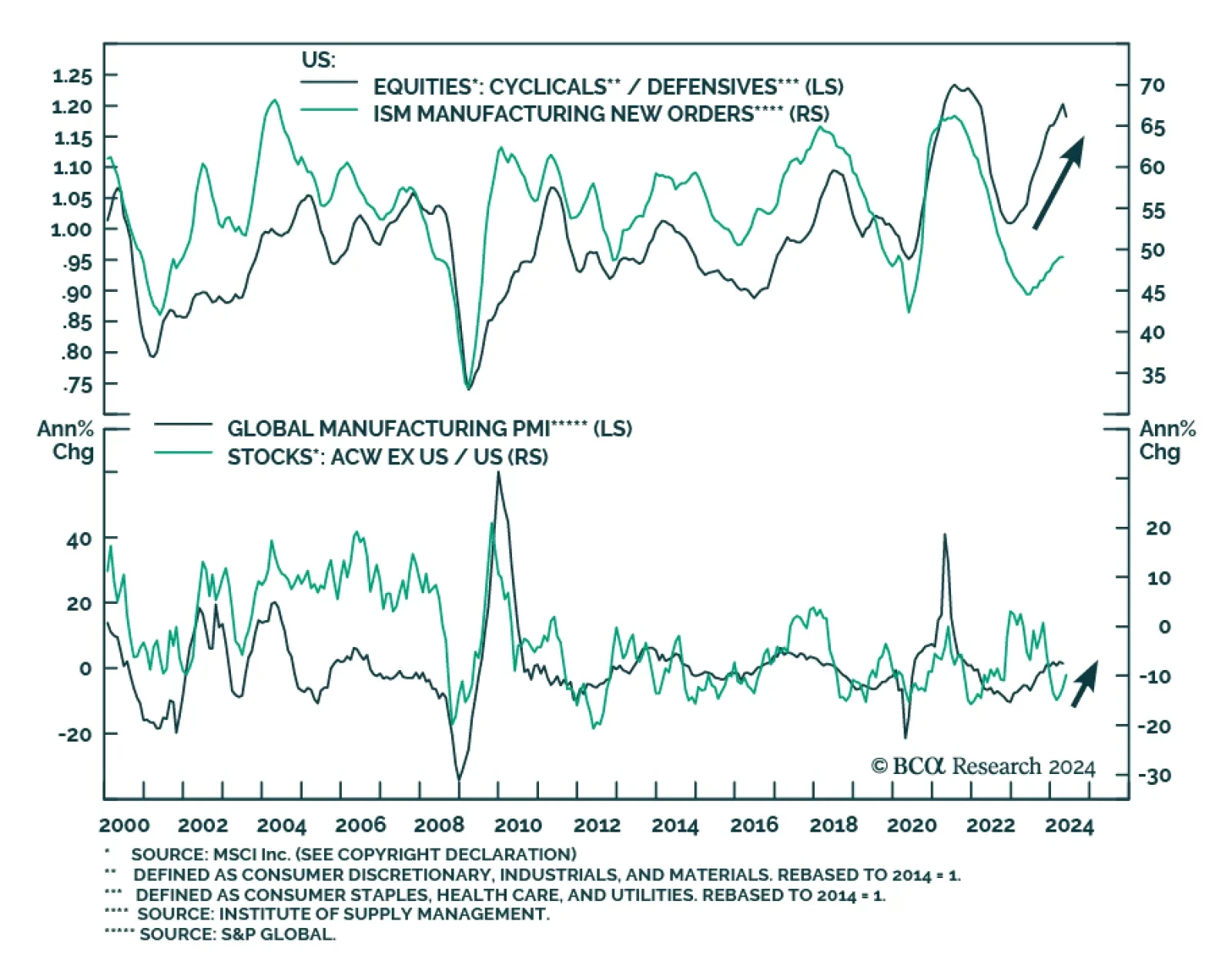

The US manufacturing cycle has followed a surprisingly stable pattern for over seven decades. History suggests that this cycle tends to last for about 36 months, with a down leg spanning 18 months, followed by an up leg approximately spanning another 18…

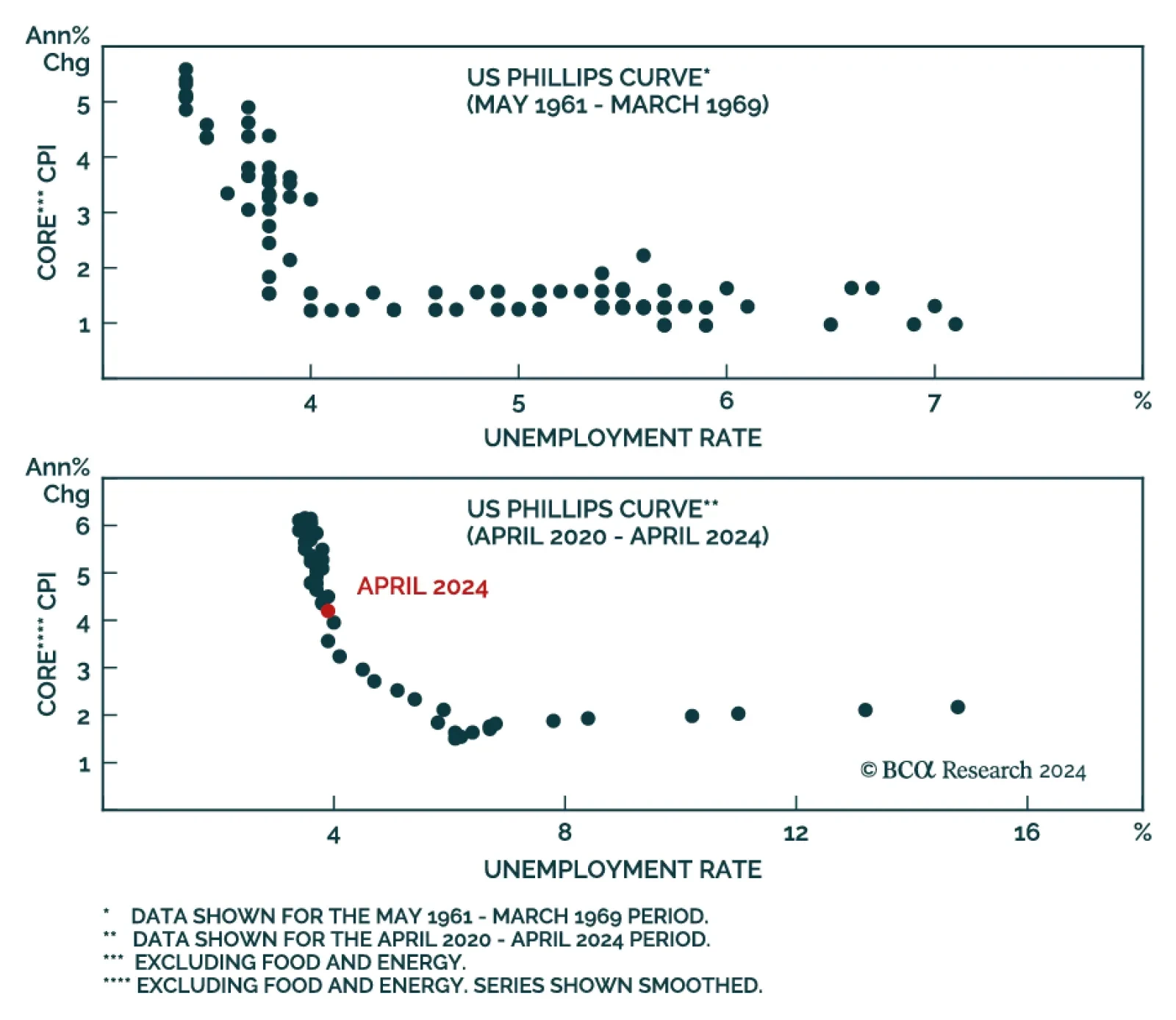

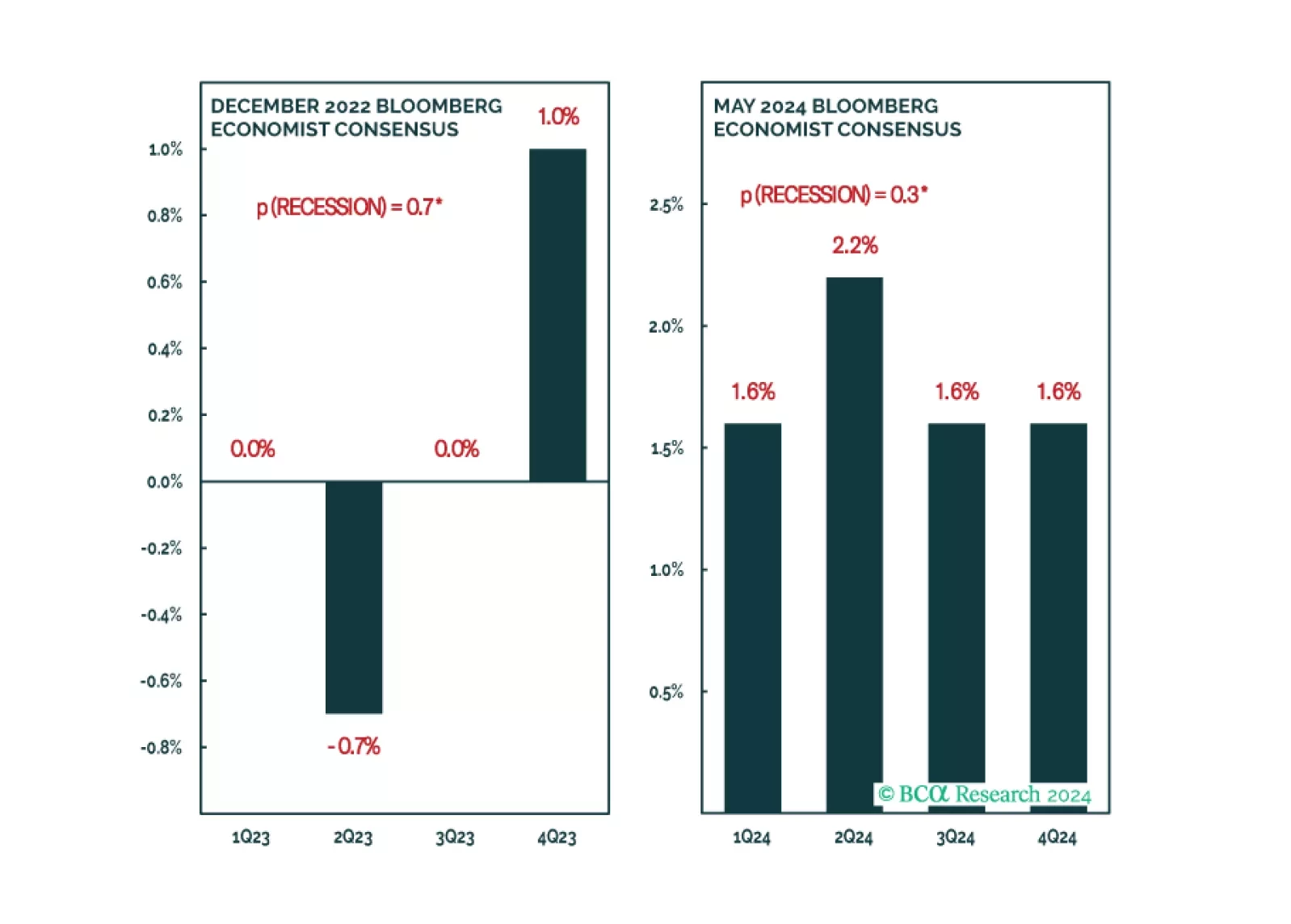

According to BCA Research’s Global Investment Strategy service, there is only a narrow path to a soft landing. Our colleagues estimate a mere 20% chance that the US will avoid a recession before the end of 2025. The US unemployment rate is a highly…

The signs of an approaching recession are starting to emerge. We will turn tactically defensive once they all fall into place.

There is a path to a soft landing, but it is a narrow one. We estimate that there is only a 20% chance that the US will avoid a recession before the end of 2025. We are currently neutral on global equities, but expect to downgrade stocks to underweight during the summer.

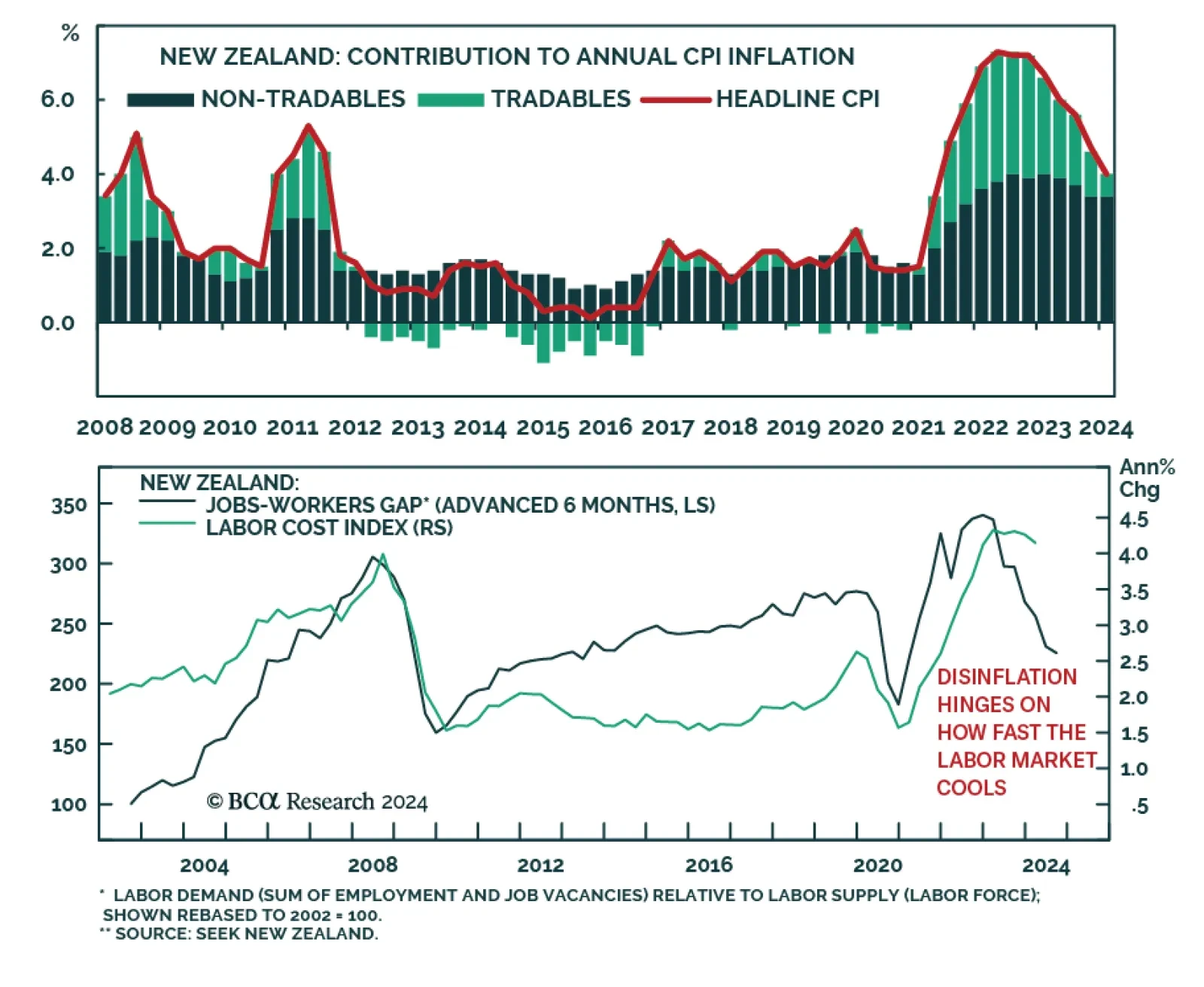

The Reserve Bank of New Zealand (RBNZ) kept interest rates on hold at this week’s monetary policy meeting, in line with expectations. However, there were three new notes from its monetary policy statement that will likely affect how it approaches future…

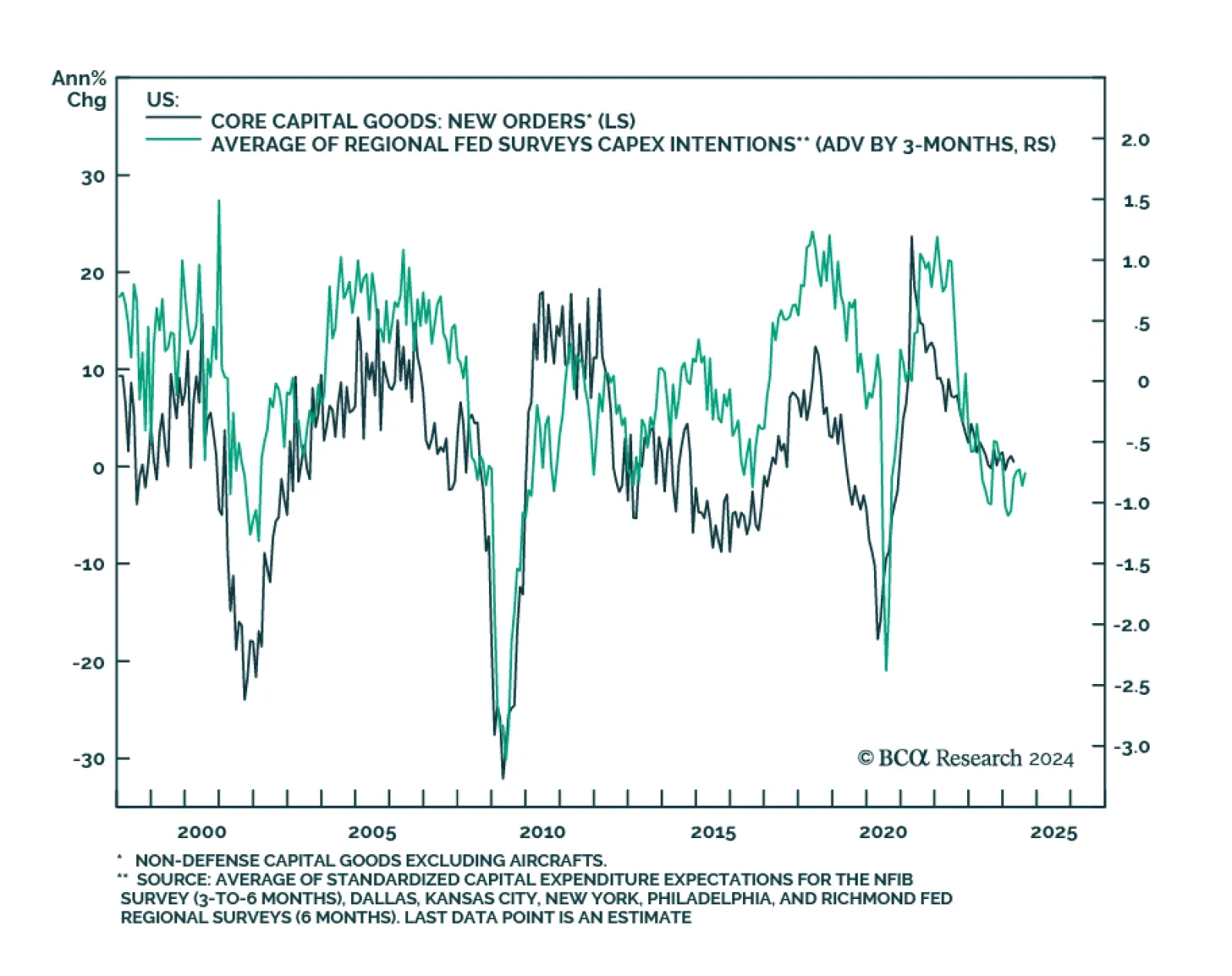

US durable goods orders surprised to the upside in April, growing 0.7% m/m against expectations they would decline. The March growth rate was nevertheless revised significantly lower, from 2.6% m/m to 0.8% m/m. Core capital goods shipments (an input into…

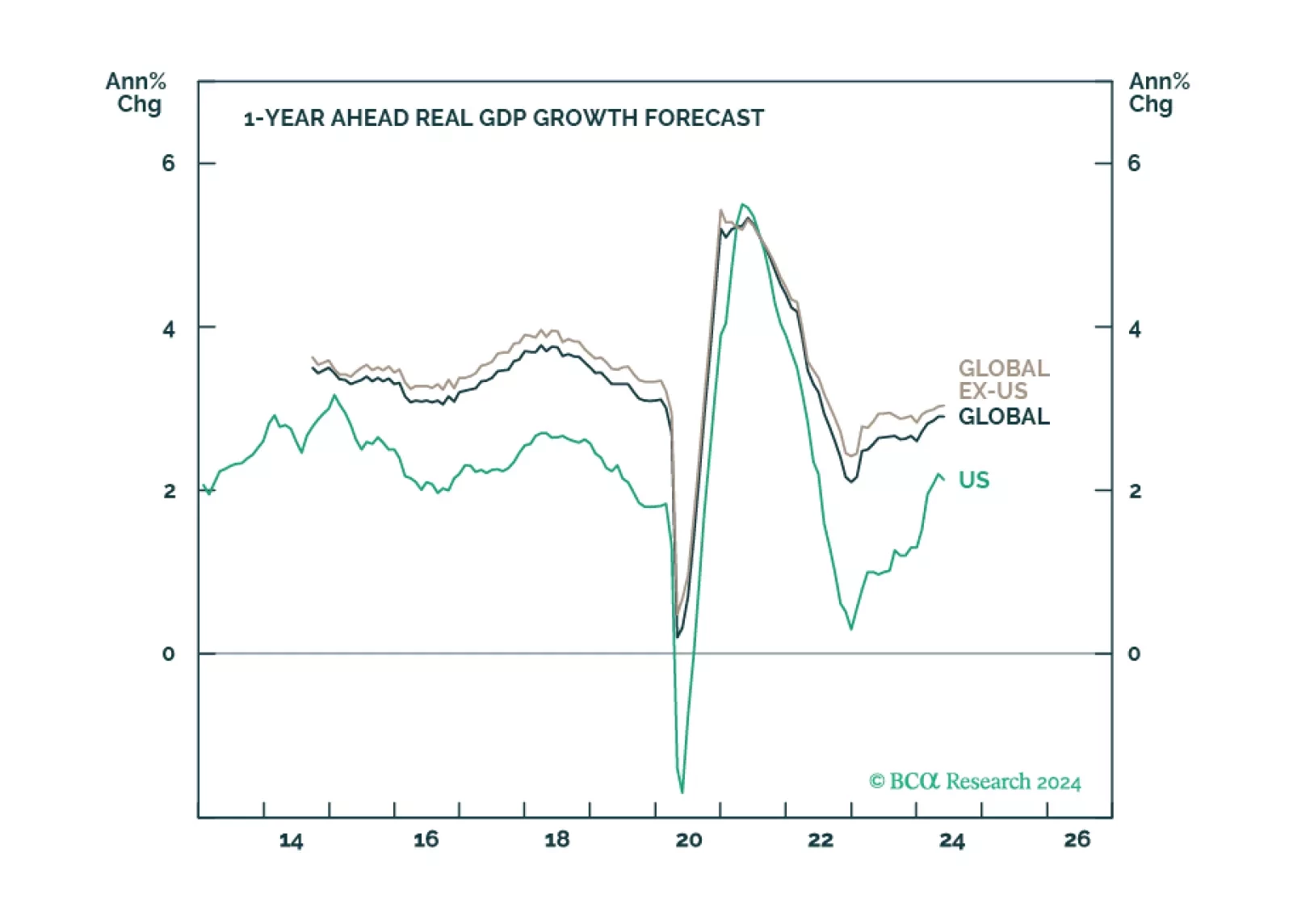

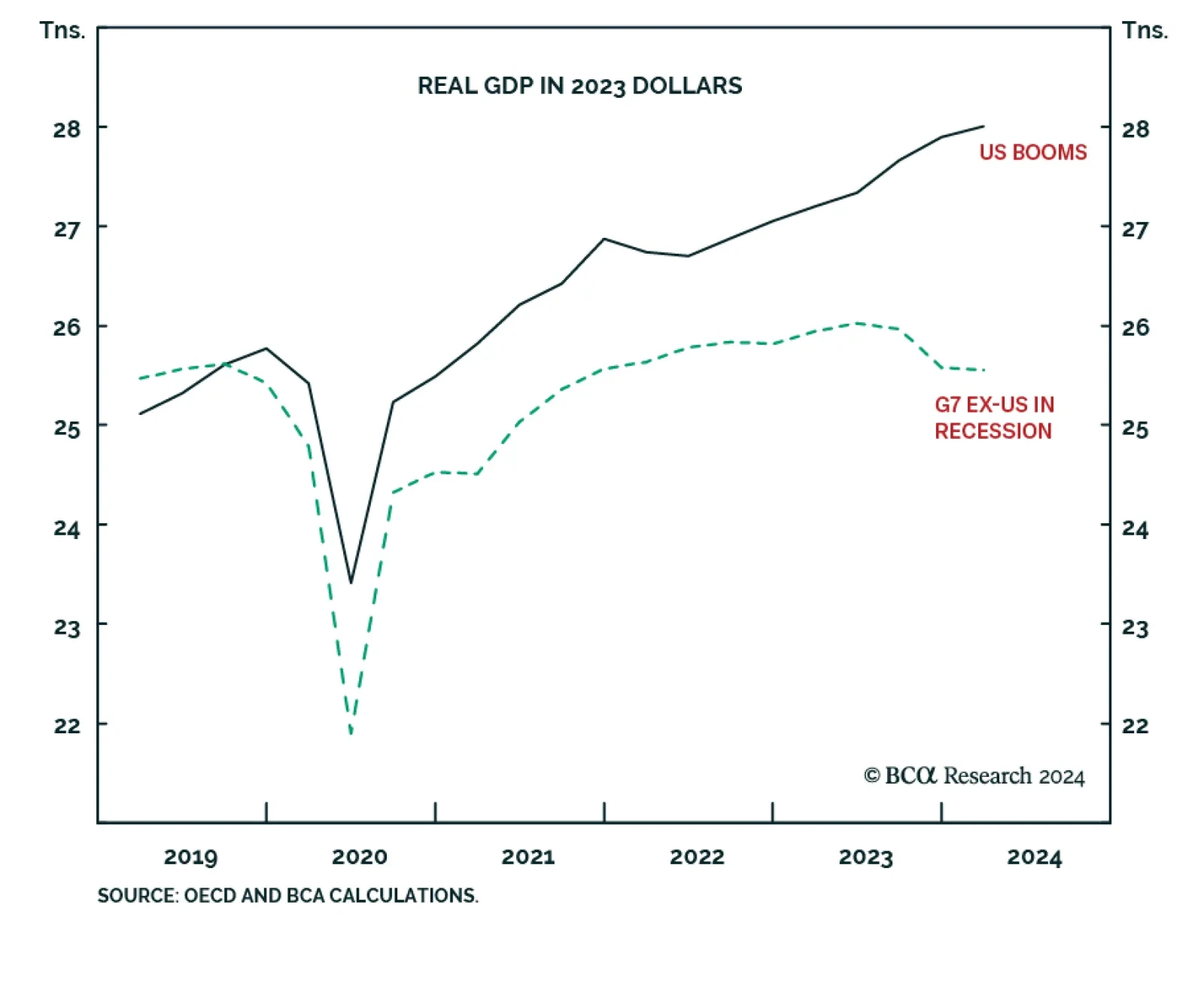

According to BCA Research’s Counterpoint service, the non-US developed economy is “demand-constrained” whereas the US economy is “supply-constrained”. This schism will continue but in reverse. The team has highlighted that following the surge in…