Recession-Hard/Soft Landing

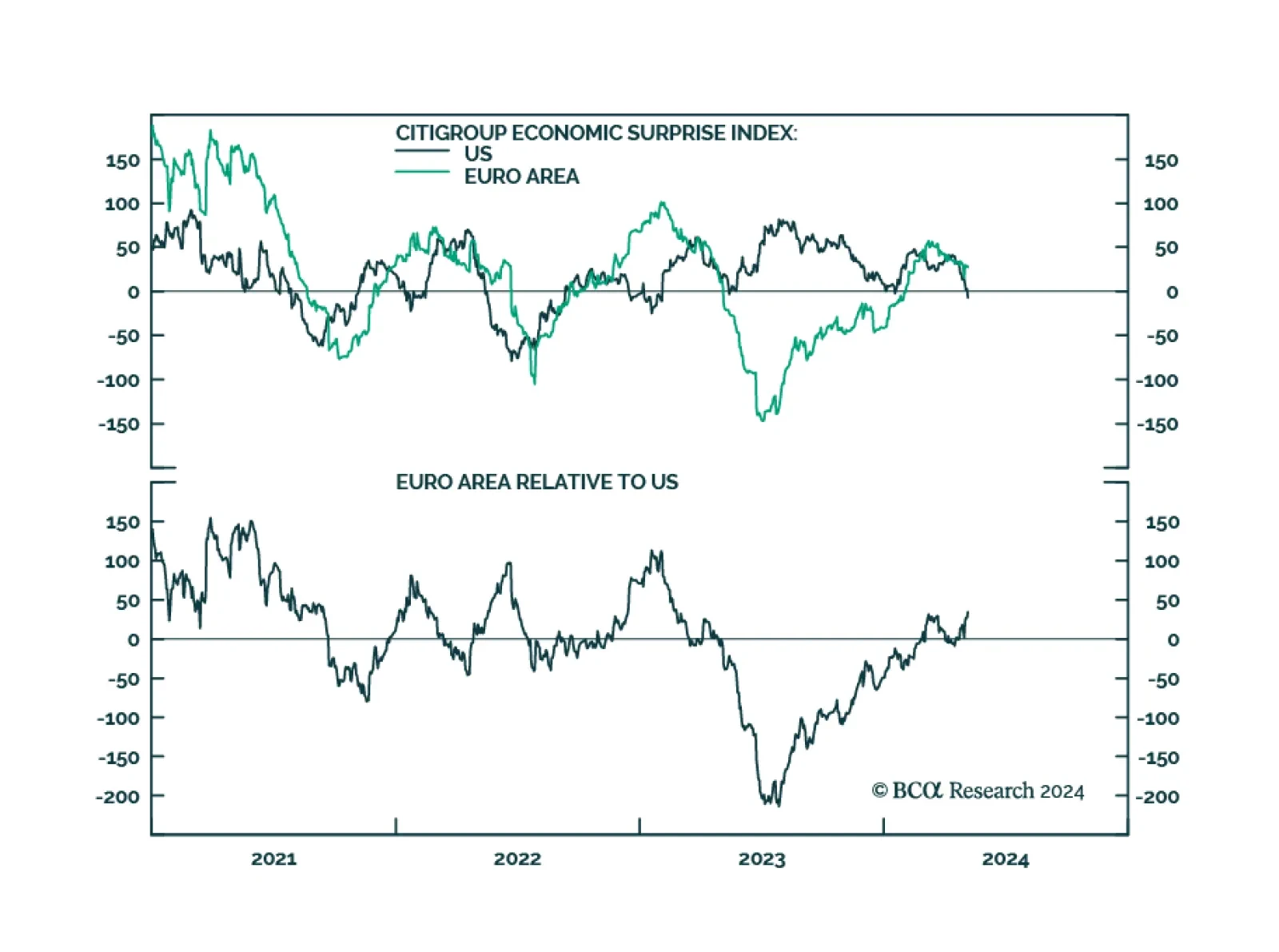

The final estimates of Spain's and France’s services PMIs were revised upwards of expectations in April, increasing from 56.1 to 56.2 and from 50.5 to 51.3 respectively. The services European harmonized PMI also increased from 52.9 to a higher-than-expected…

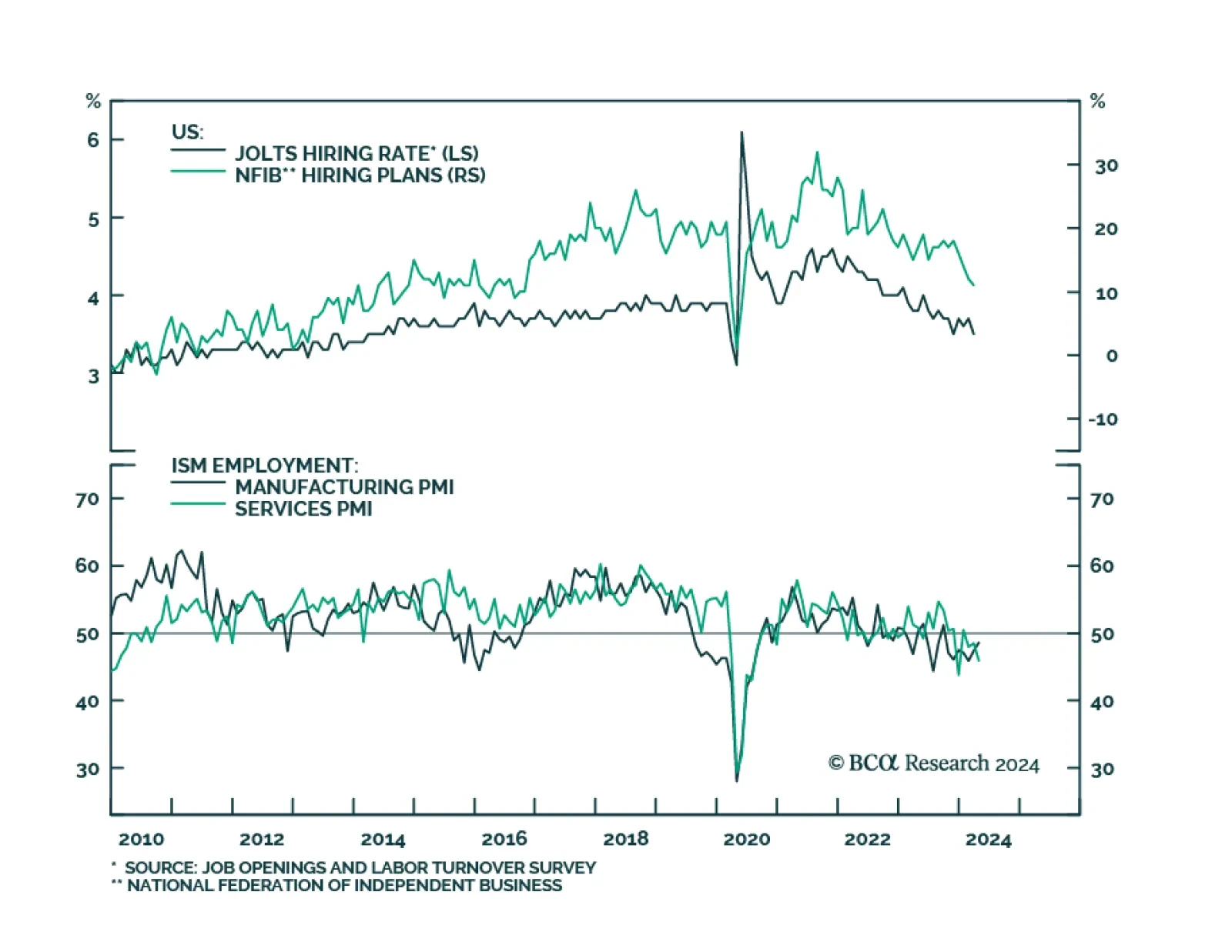

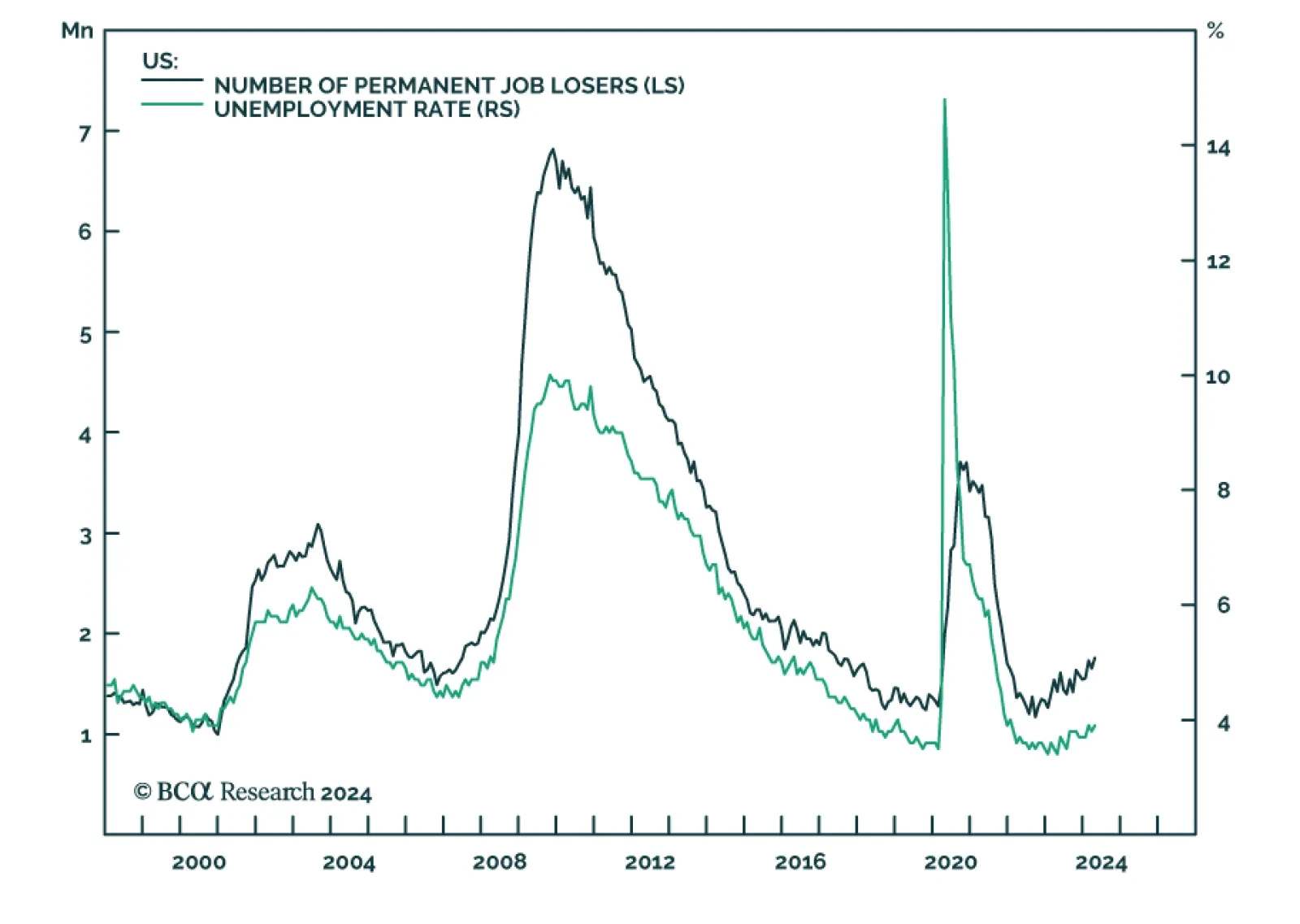

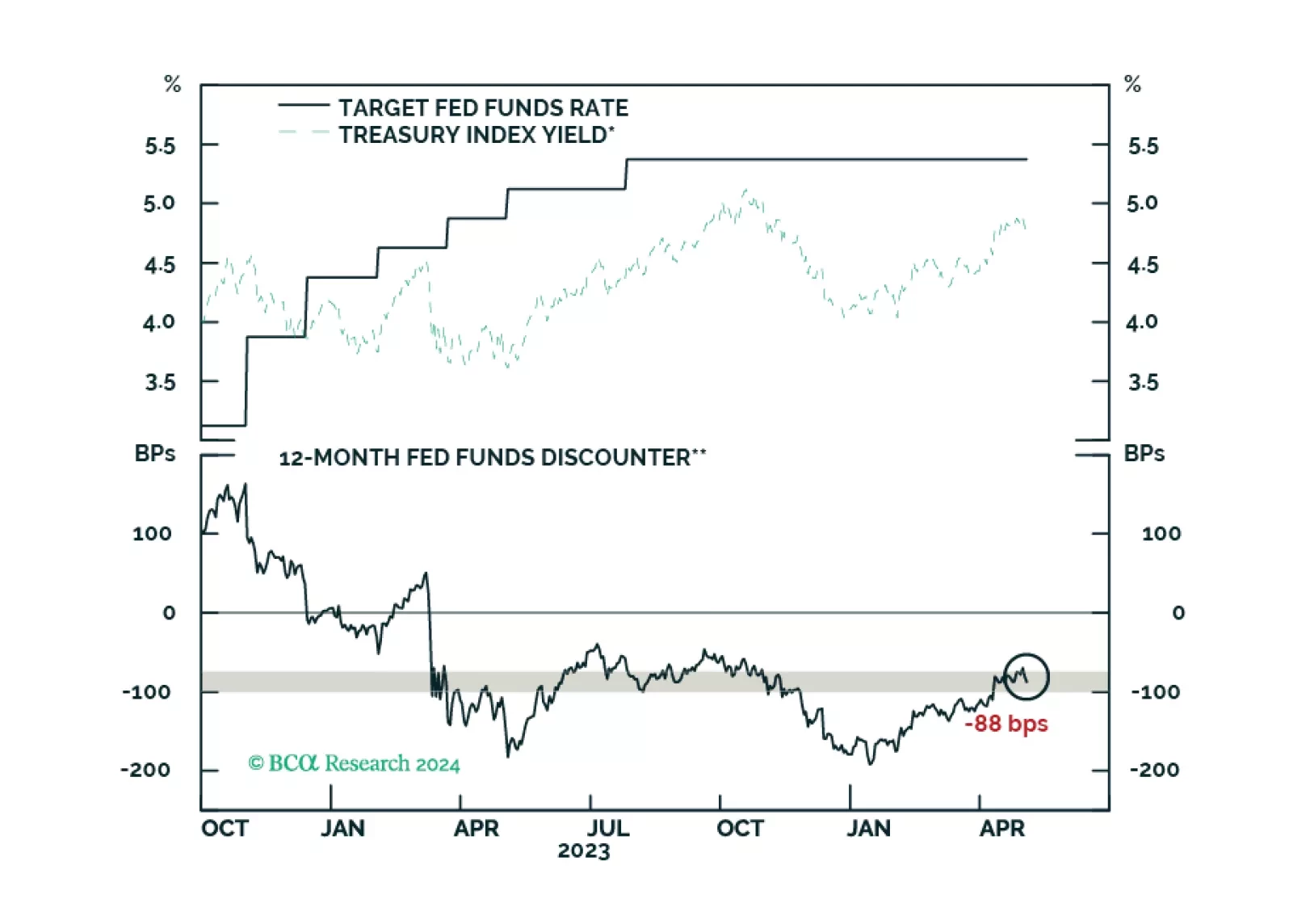

According to BCA Research’s US Bond Strategy service, while US economic data clearly show that labor demand has slowed from its peak two years ago, it isn’t yet clear whether this slowing represents a re-normalization to pre-pandemic levels or the start of a…

Average hourly earnings growth slowed to 0.2% m/m in April from 0.3% m/m in March and came in below expectations. On a year-on-year basis, they decelerated from 4.1% to 3.9%, the lowest since June 2021 and below expectations of 4%. Nonfarm payrolls growth…

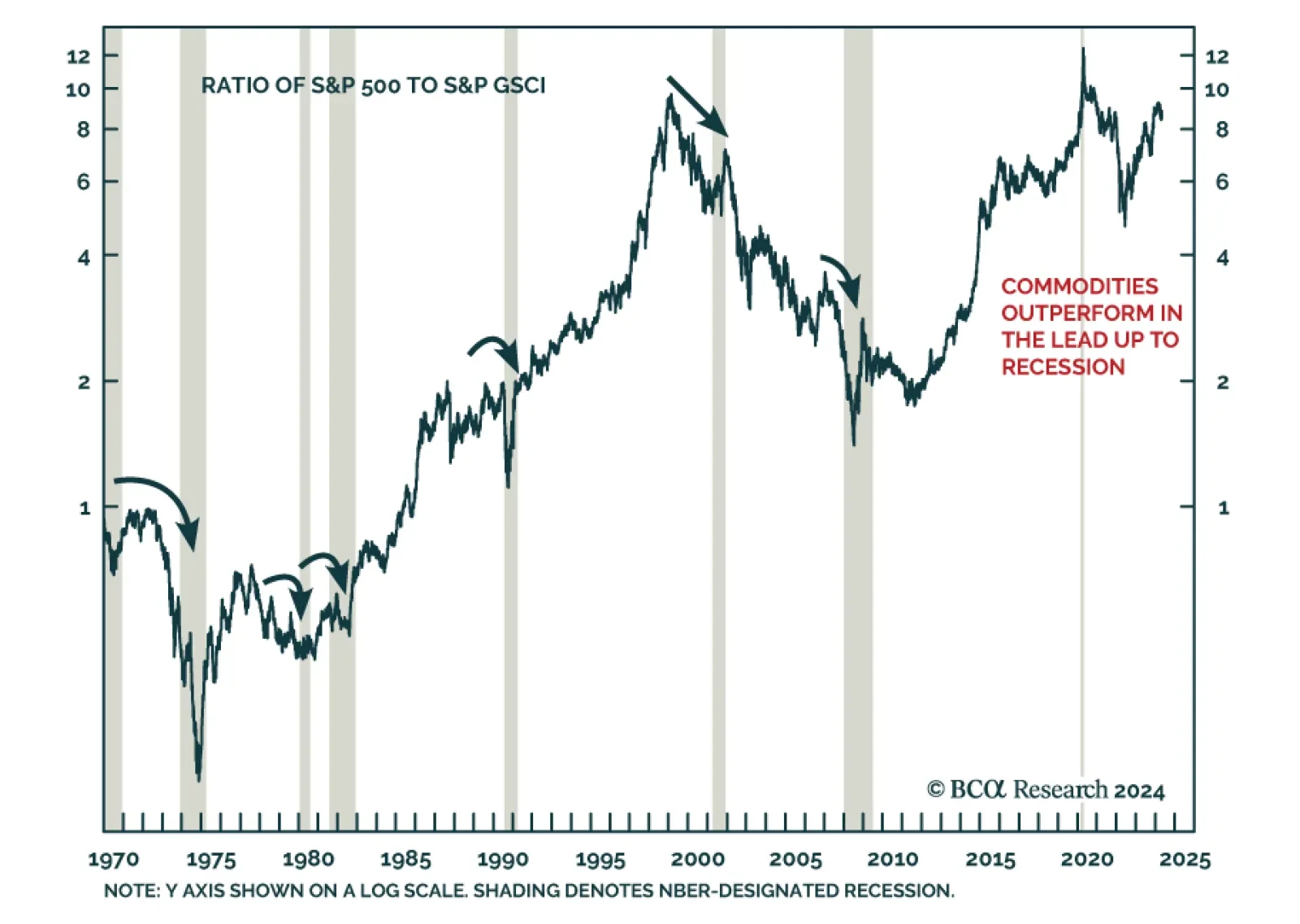

According to BCA Research’s Commodity & Energy Strategy service, commodity prices typically rally toward the end of the business cycle. In the past six recessions, the S&P 500 peaked before commodity prices. While there is significant variability…

Some thoughts on this morning’s employment report and recent trends in US economic data.

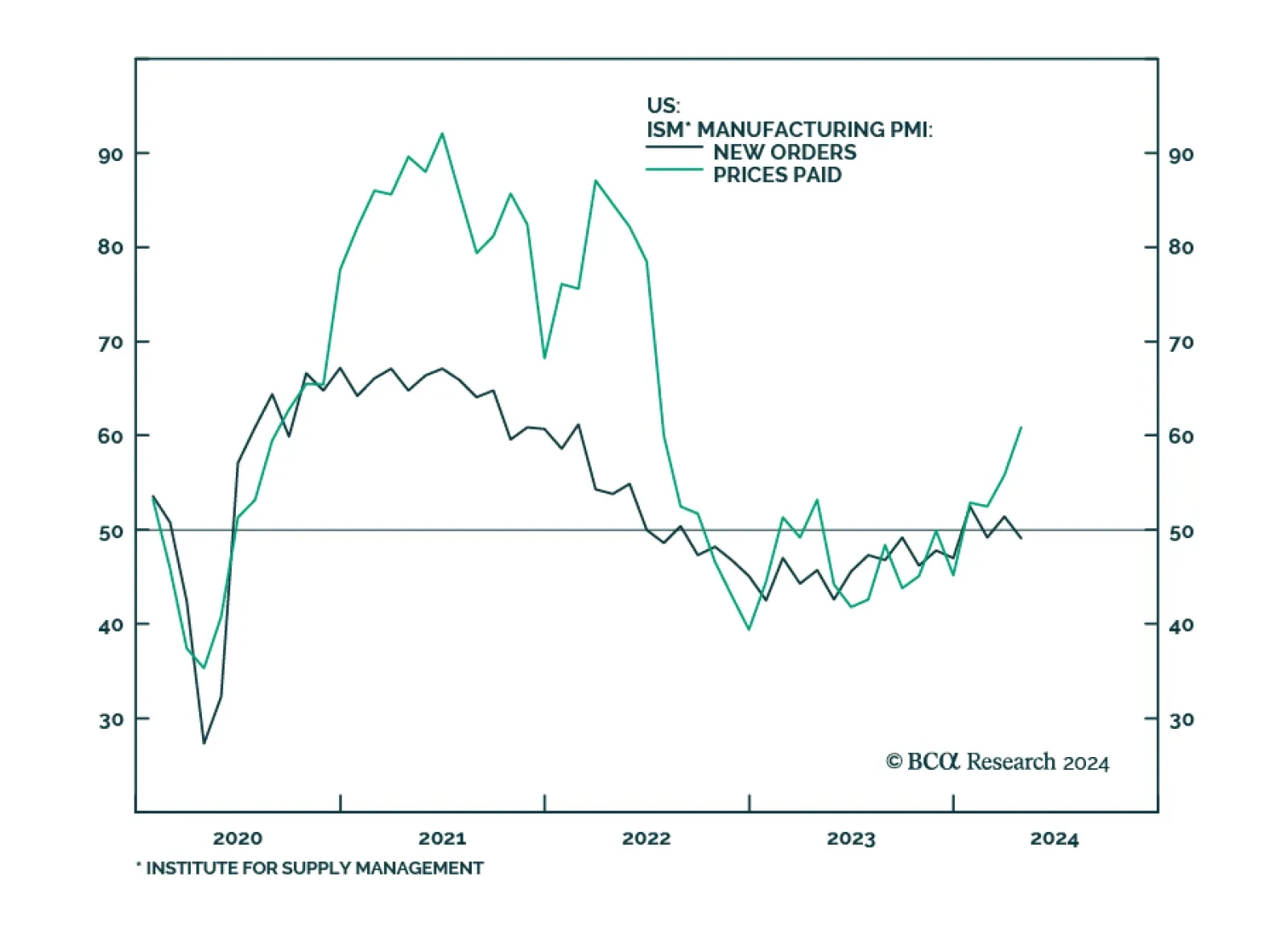

After briefly breaking a 16-month contraction streak, the ISM Manufacturing PMI dipped back below the 50.0 boom-bust line in April. It decreased from 50.3 to 49.2, disappointing expectations of 50.0. Notably, measures of domestic and foreign demand both…

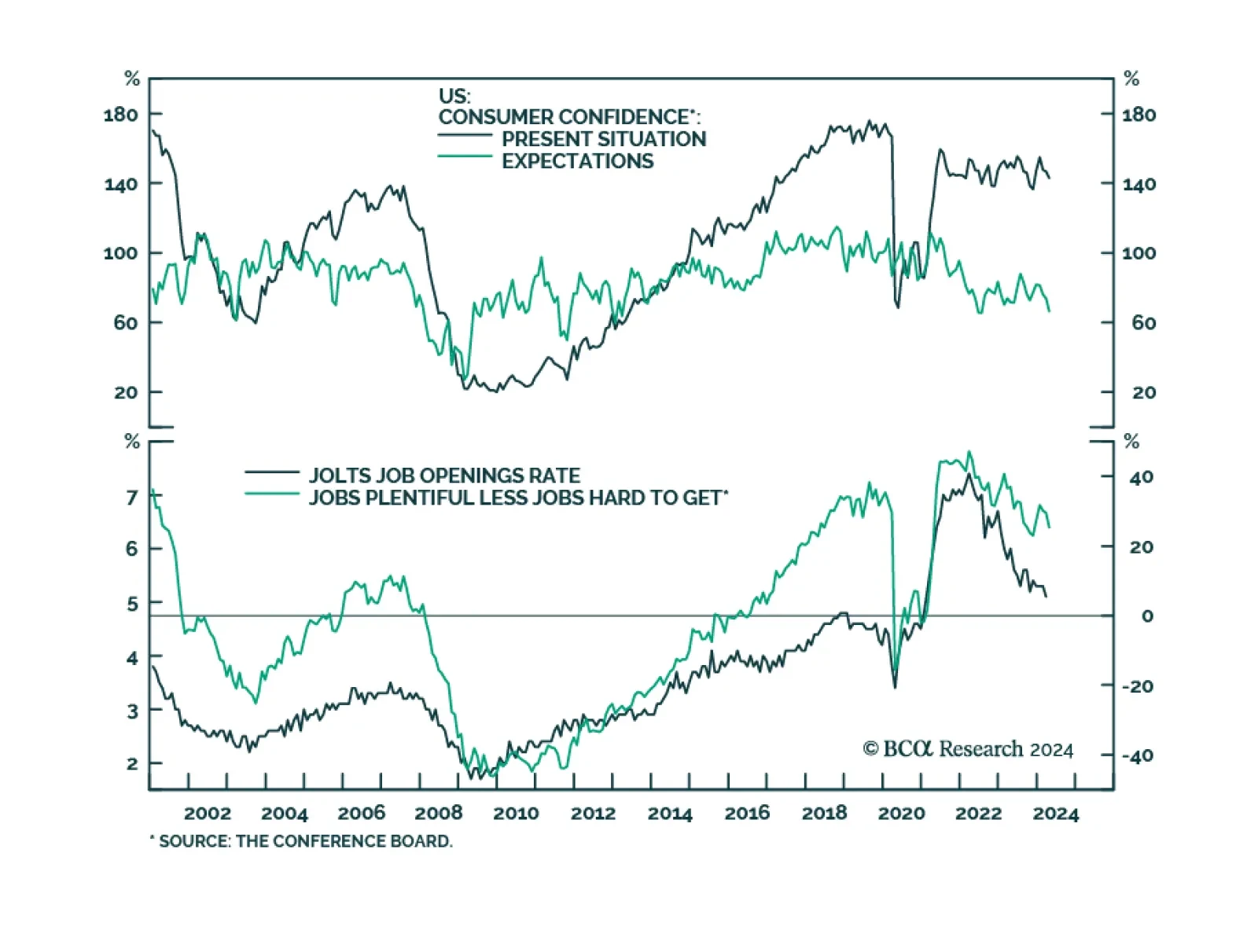

The Conference Board’s gauge of consumer confidence largely disappointed in April. 3.9- and 7.6-point decreases in the Present Situation and Expectations subcomponents, respectively, drove the overall index to a 22-month low of 97.0 in April. This third…

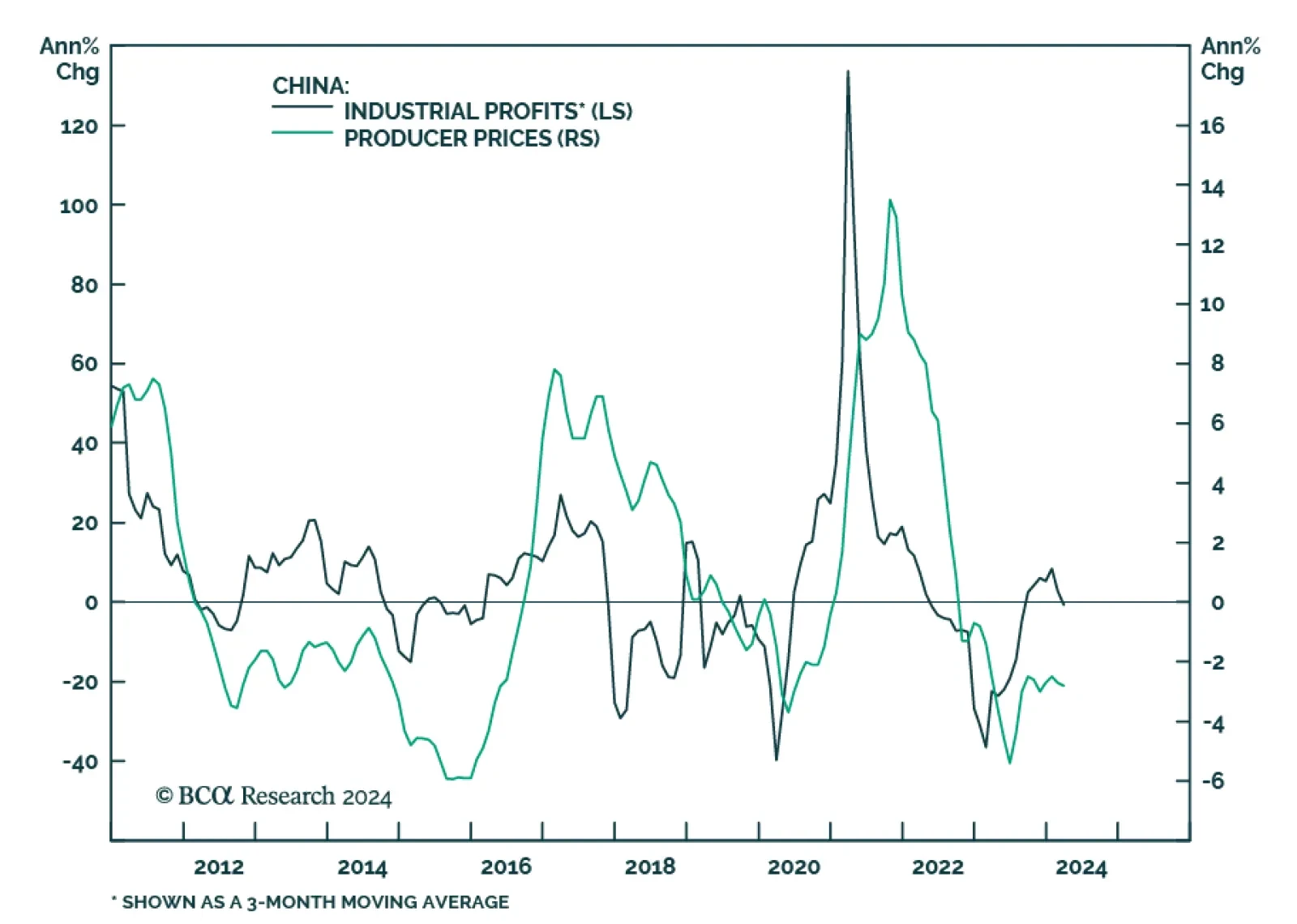

Chinese industrial profit growth slowed in the first three months of the year to 4.3% YTD y/y, from 10.2% y/y in January and February. The March slowdown is meaningful since industrial profits outright contracted by 3.5% relative to March 2023. Weak…

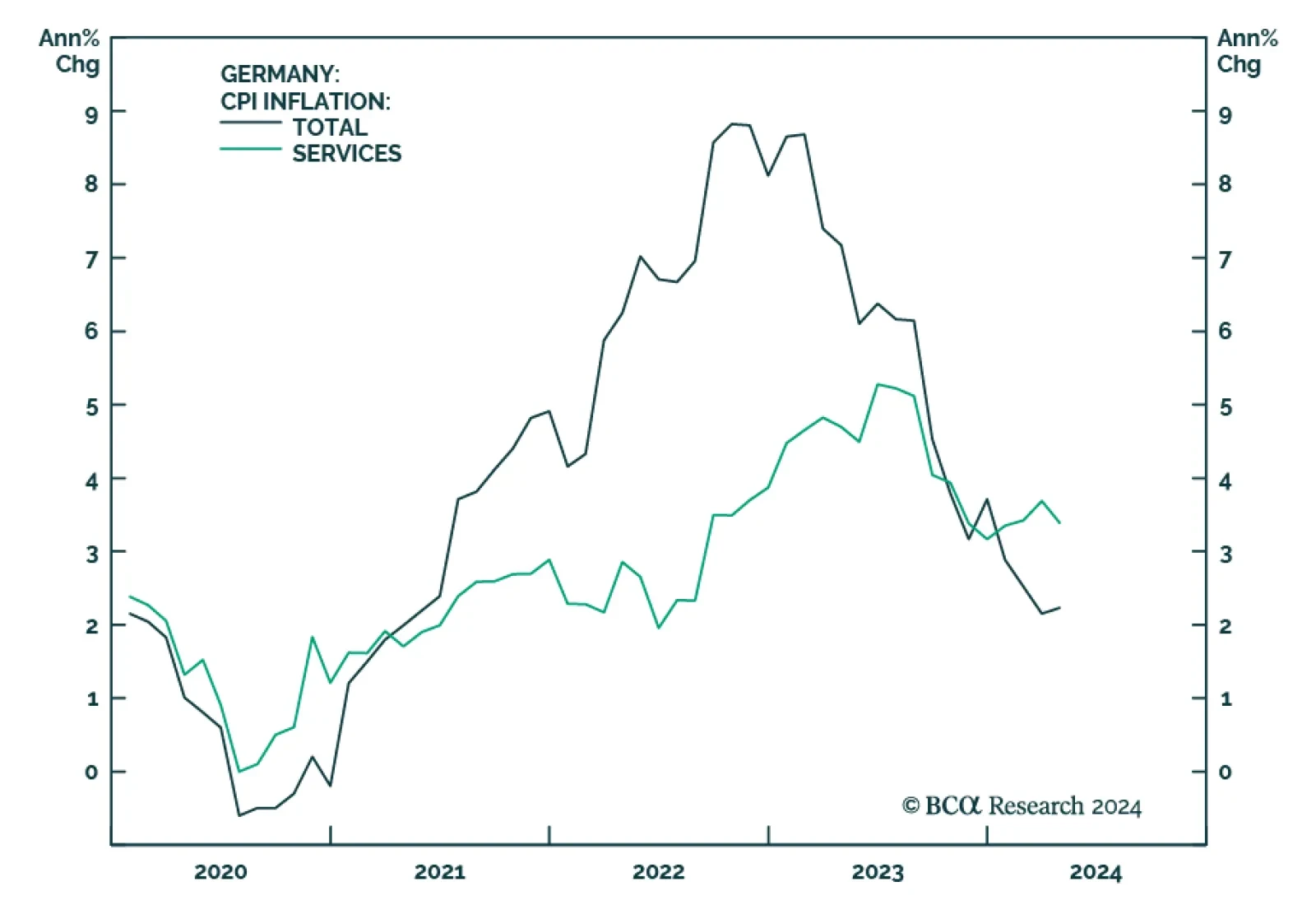

A few preliminary measures of German inflation for April were released on Monday. The month-on-month headline inflation measure came in at 0.5% an increase from last month’s reading of 0.4% but below expectations of 0.6%. Meanwhile the year-on-year version…

The latest edition of our Big Bank Beige Book suggests the expansion remains intact, though weakness in C’s private-label credit card portfolio could be a harbinger of distress among lower-income consumers. We remain tactically neutral with a bias to turn defensive once clearer signs of a recession emerge.