Recession-Hard/Soft Landing

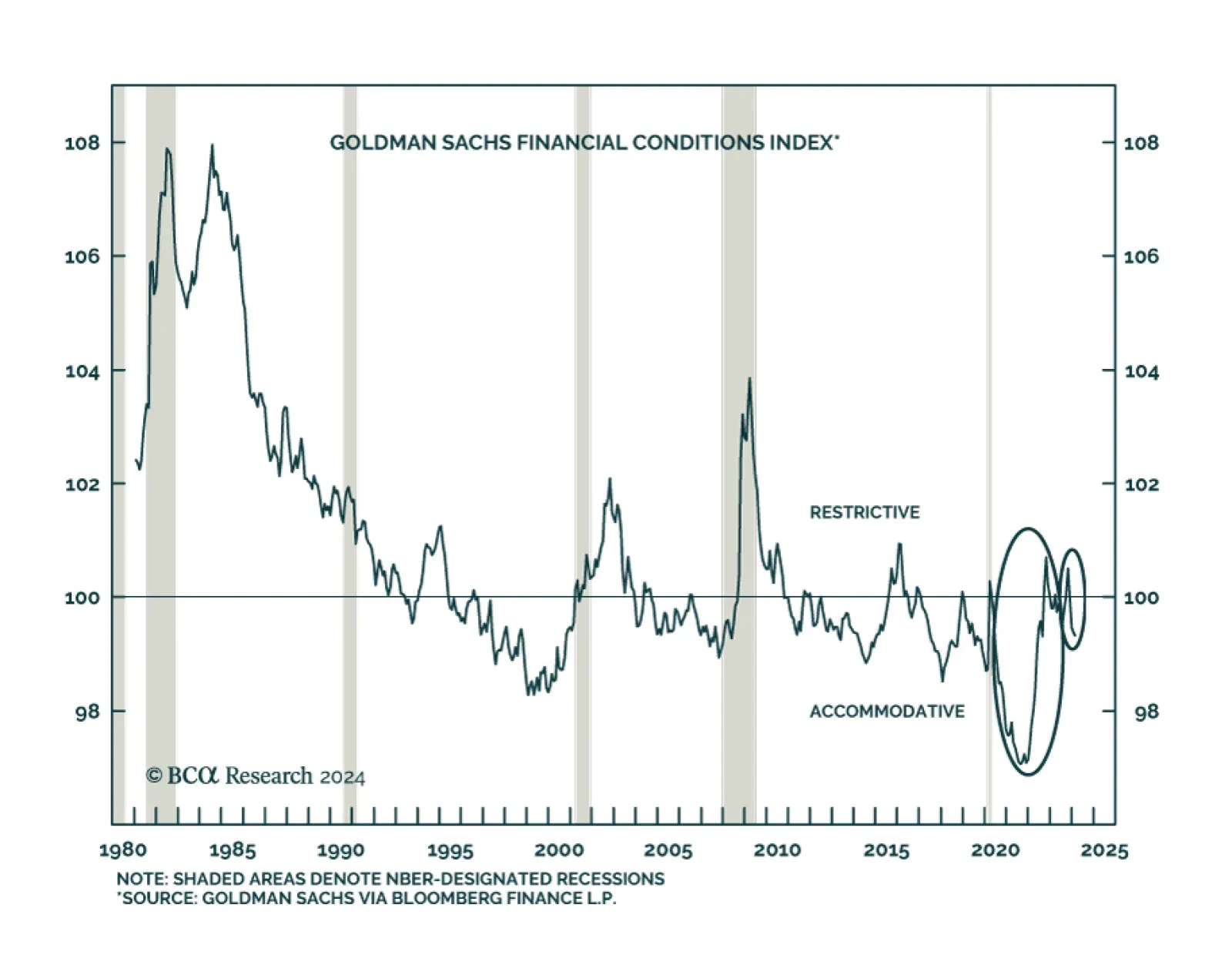

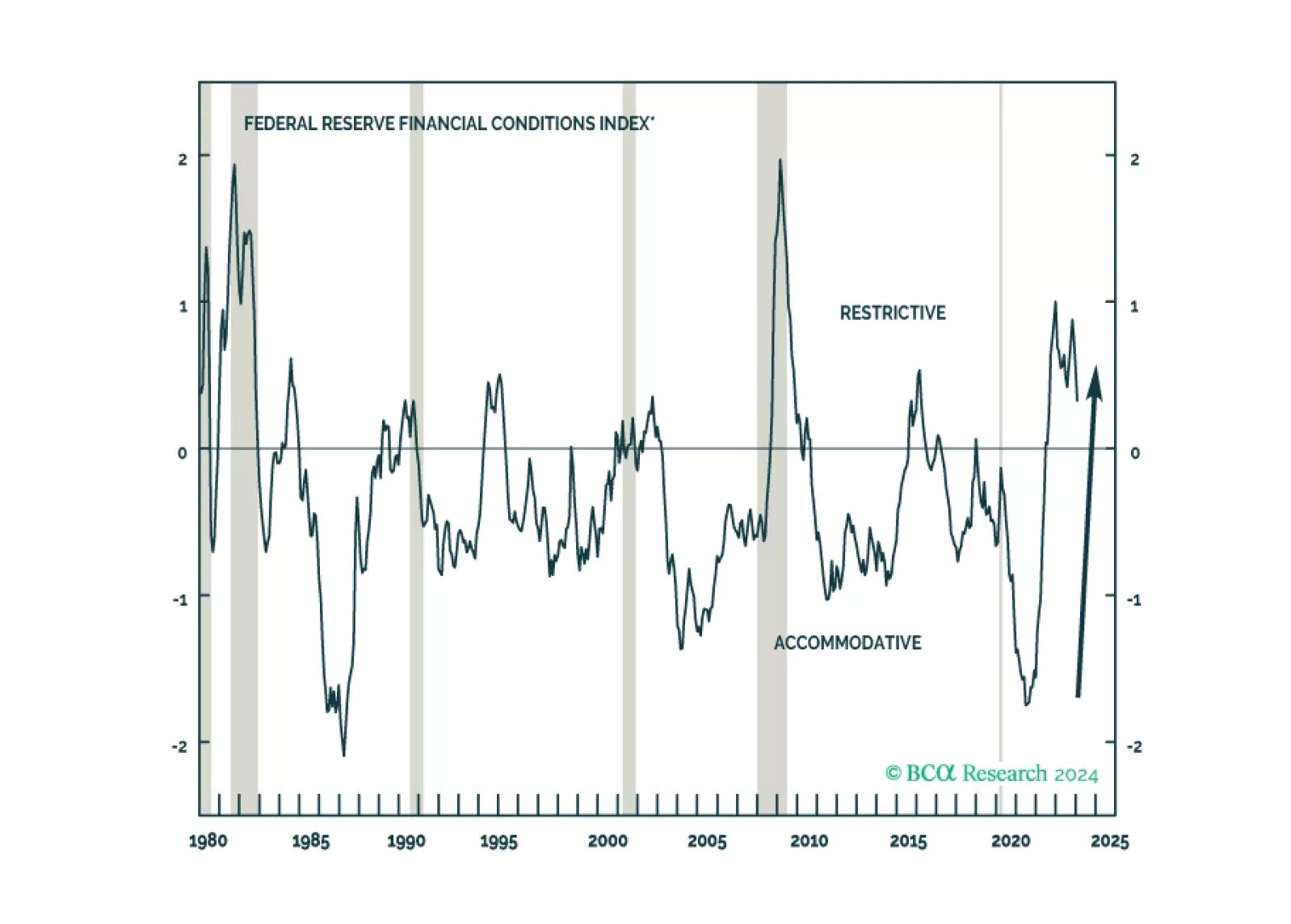

According to BCA Research’s US Investment Strategy service, investors should take care not to read too much into the recent easing in financial conditions. According to Goldman Sachs’ Financial Conditions Index (FCI) financial conditions have become…

Clients have been pushing back on our recession call on the grounds that it is incompatible with the economy’s second-half acceleration and the more recent easing in financial conditions. We examine both of those points in the course of doing some pushing back of our own.

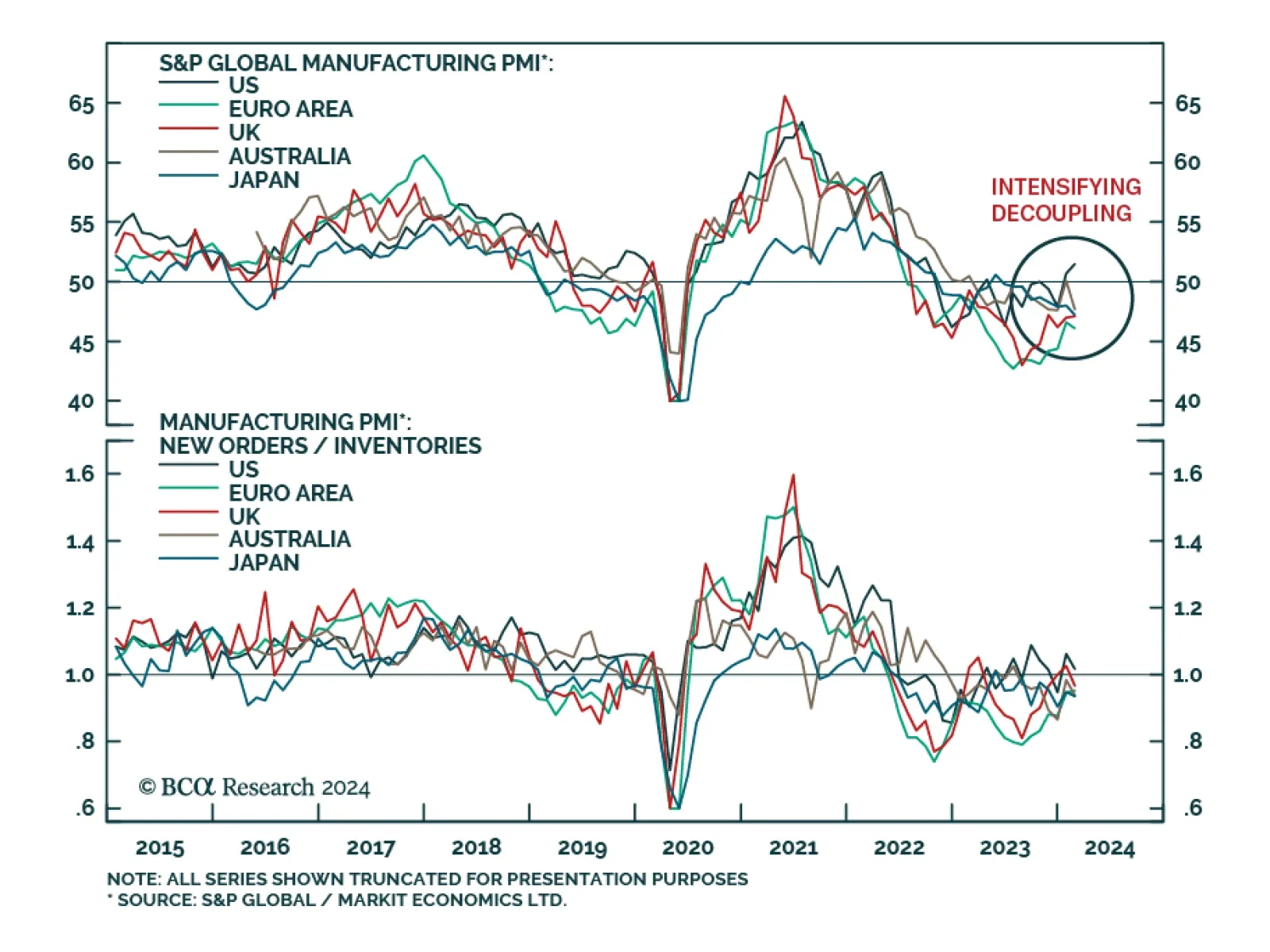

Preliminary PMI estimates suggest that service sector activity is expanding across DM economies in February. Most notably, services PMIs are back at or above 50 in Australia and the Eurozone from previously contracting levels. Meanwhile, the services sectors…

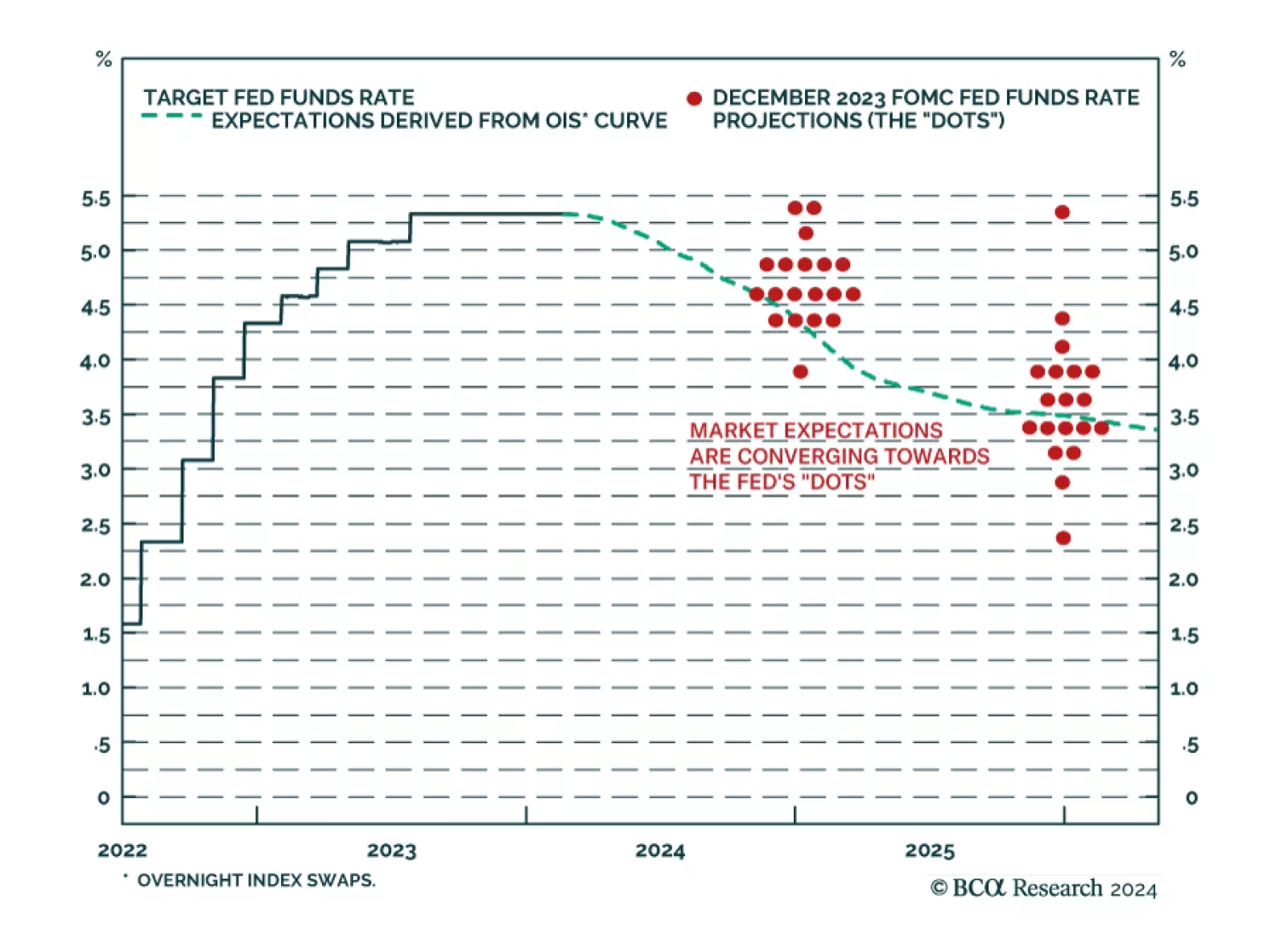

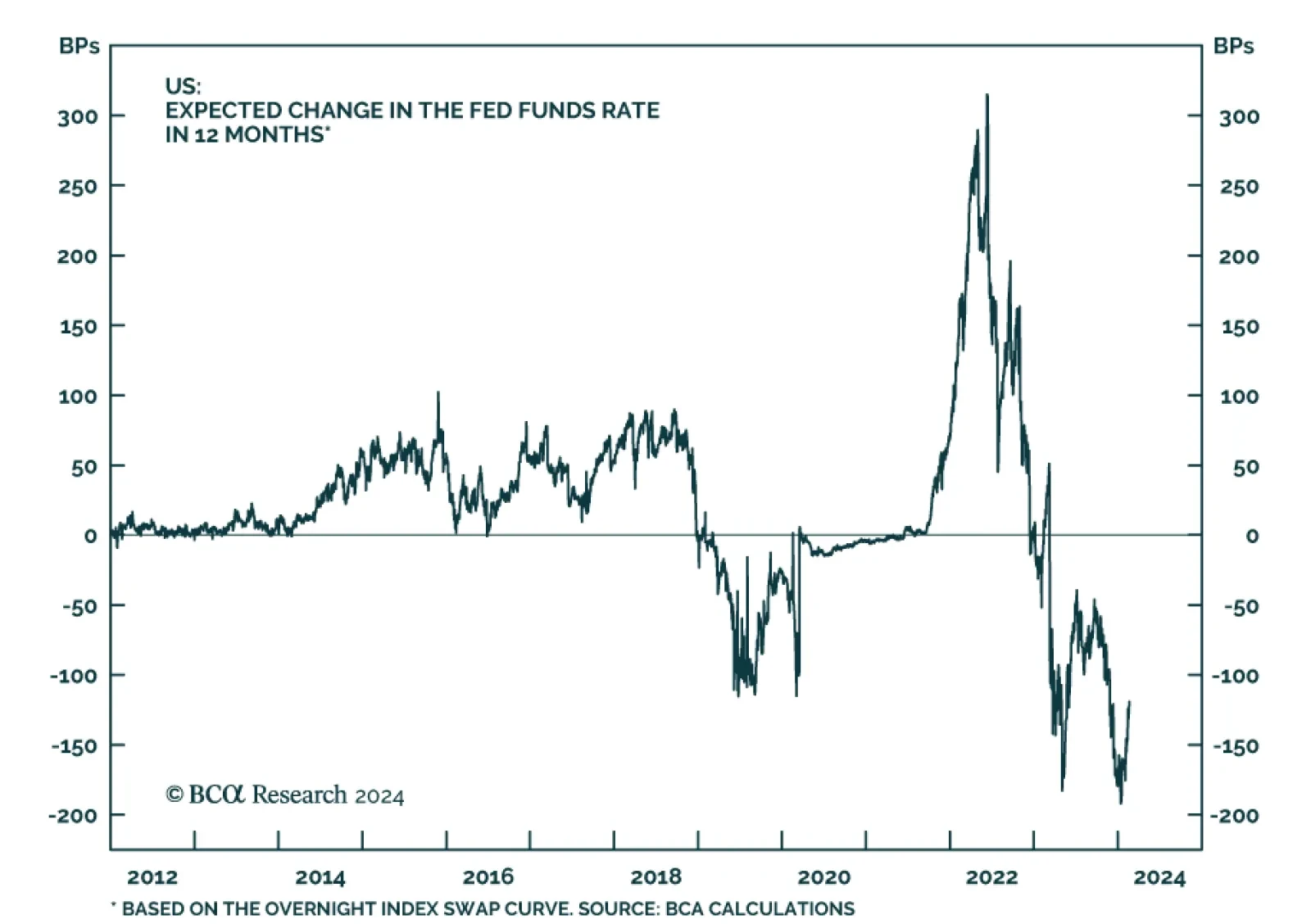

The minutes of the January FOMC meeting underscore that policymakers are adopting a cautious approach in timing the pivot to policy easing. Although Fed officials acknowledged that inflation and employment risks are “moving into better balance,” and that…

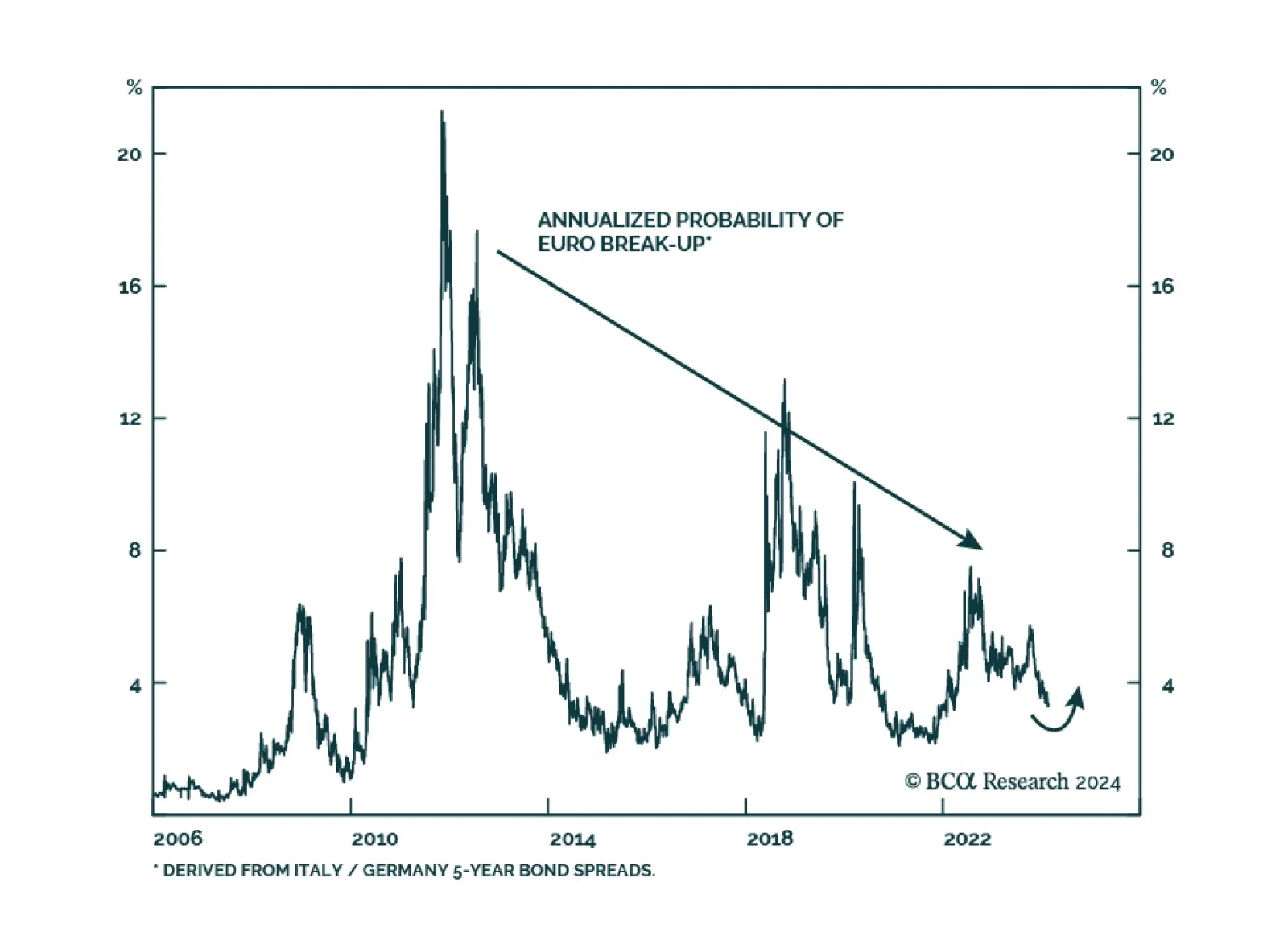

According to BCA Research’s Geopolitical Strategy service, European political risk is turning up again. Increased European political risk is not because of the European parliamentary elections, which will see right-wing populist parties perform well but…

We rank the US spread sectors in terms of risk versus reward.

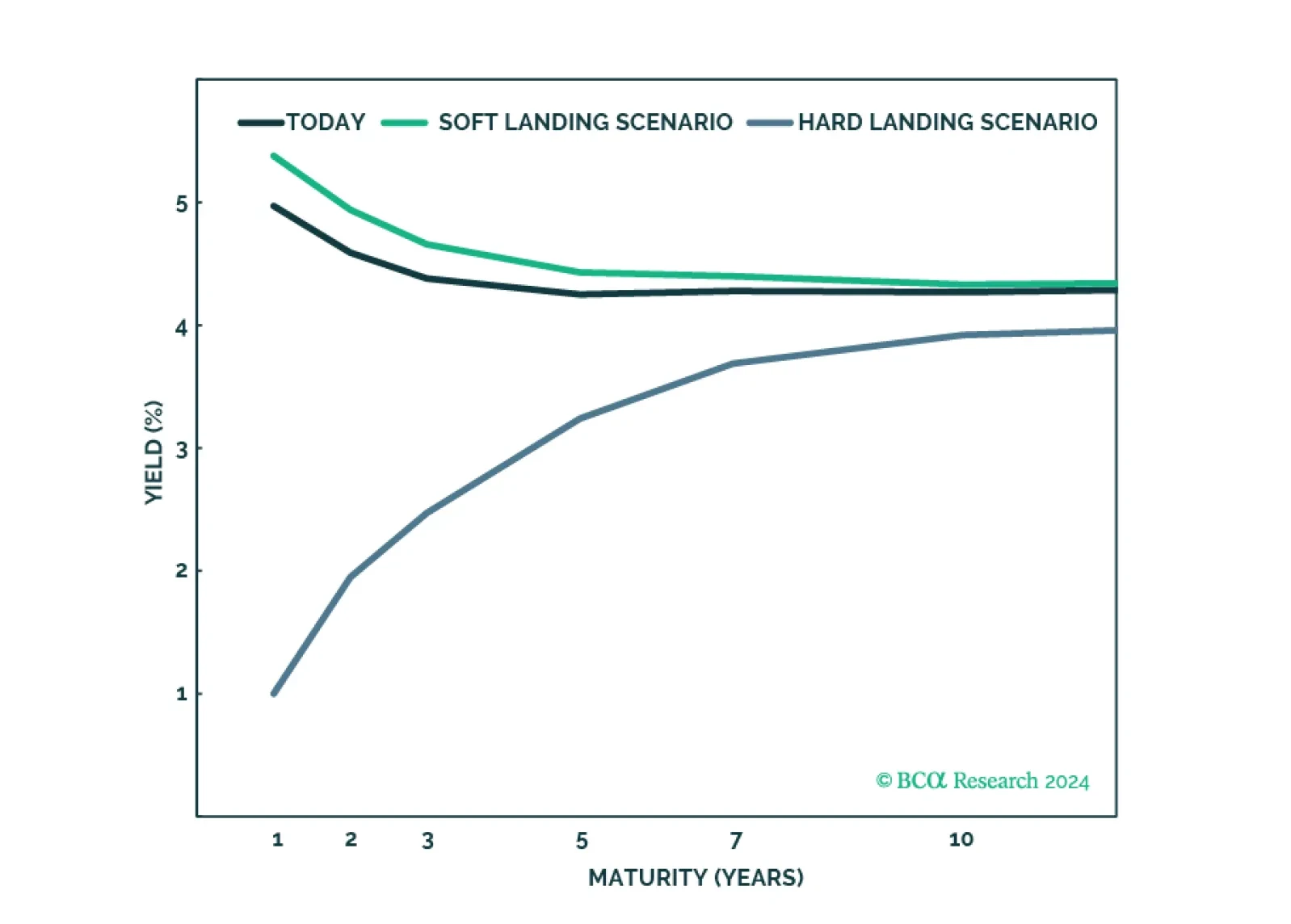

US Treasuries have been selling off over the past two months as investors downgrade the odds of an imminent start to the Fed’s easing cycle. Naturally, a question facing investors is whether current levels constitute a good opportunity to increase duration…

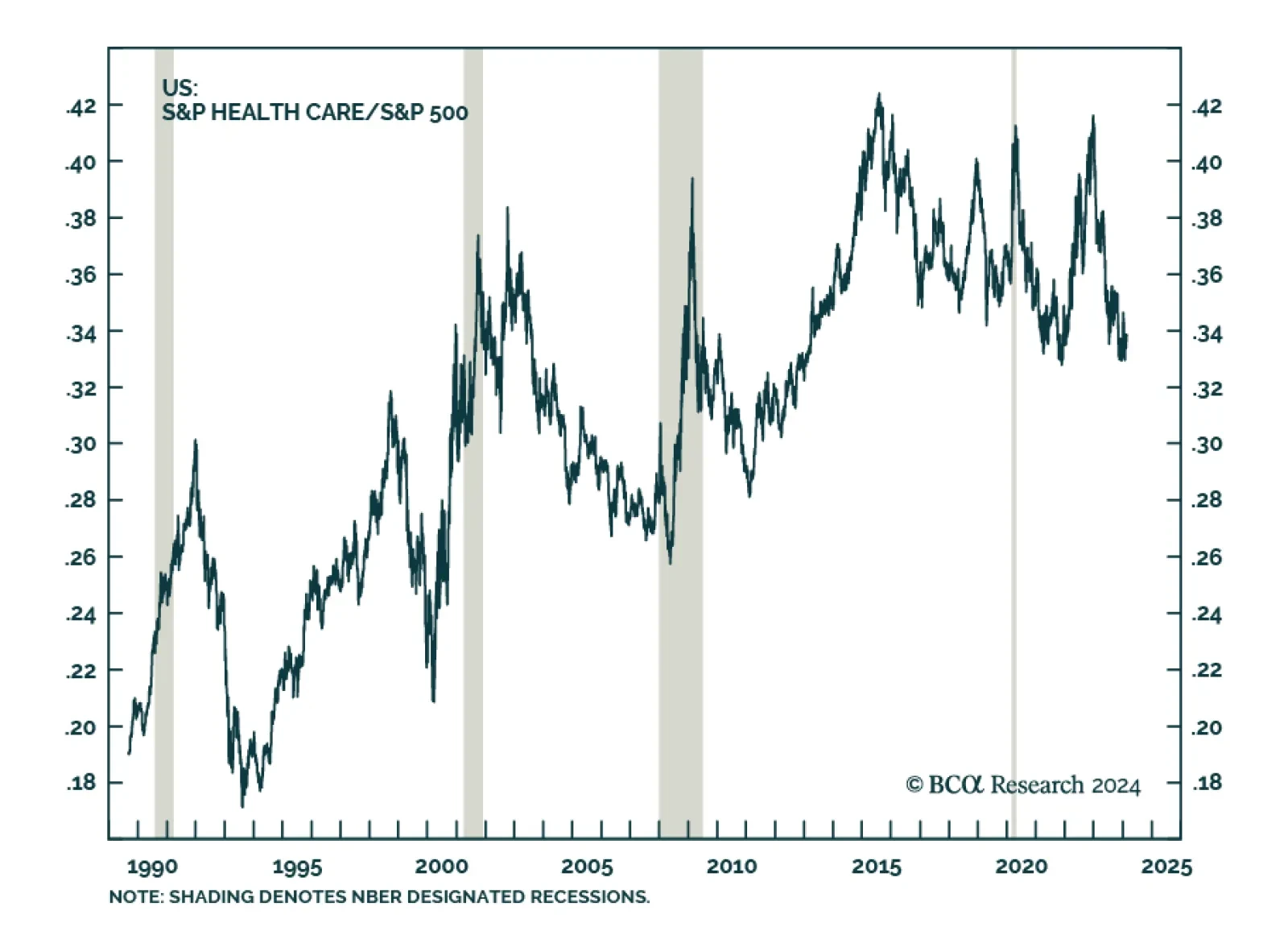

The Health Care sector is among the best performing US equity sectors so far this year. Its 6.2% year-to-date price gain exceeds the S&P 500’s 4.3% increase and is second only to Communication Services. This marks a shift in dynamics from the earlier part…

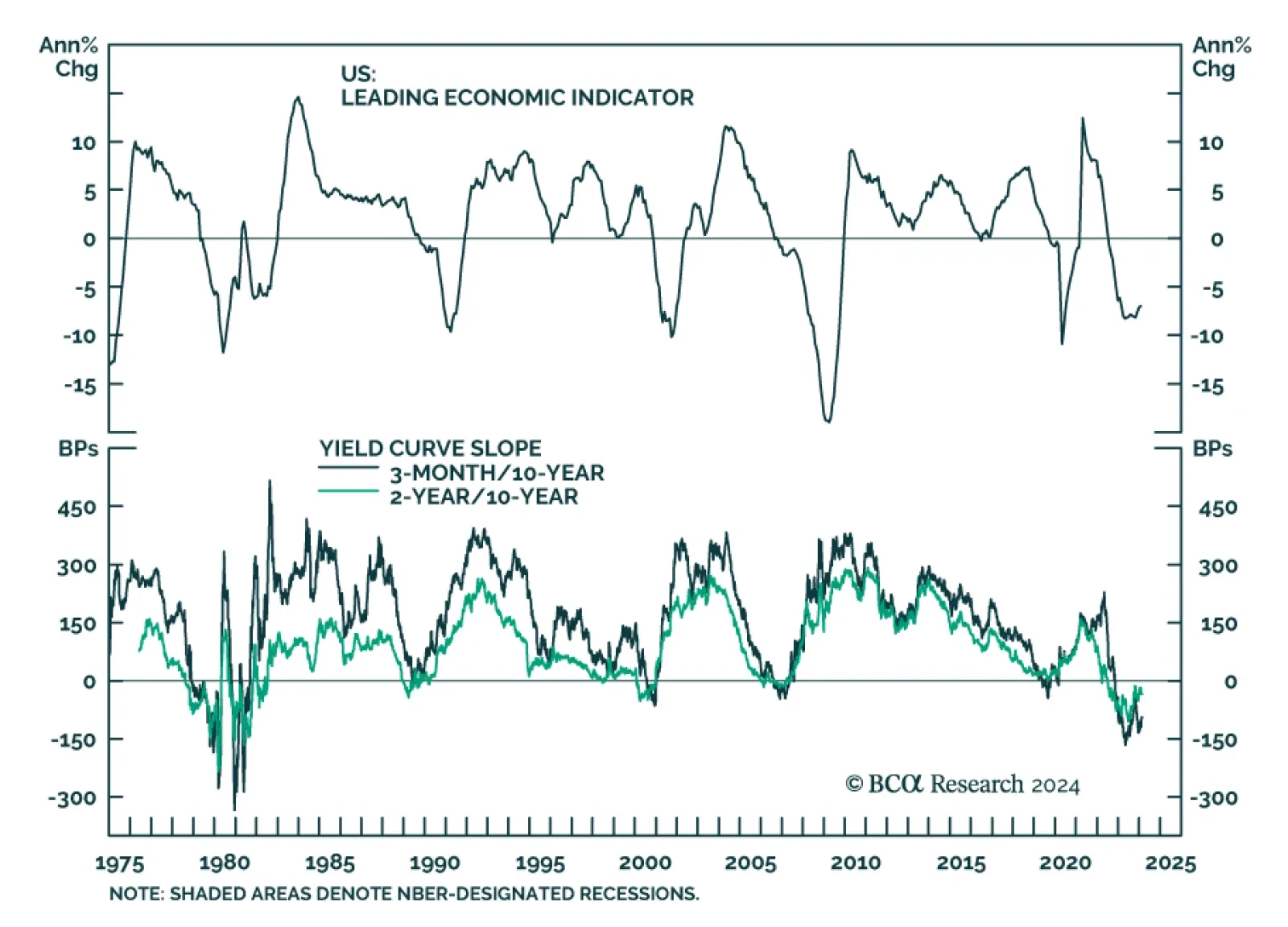

The US Conference Board’s Leading Economic Index (LEI) fell by 0.4% m/m in January, following a 0.1% m/m drop in December – disappointing expectations of a milder decline. This marks the 23rd consecutive monthly decrease and has pushed down the index to its…

Democrats remain favored for reelection in 2024, which implies gridlock and policy status quo in 2025. That is not negative for stocks in the near term. However, economic, political, and geopolitical risks will escalate from here, causing volatility.