Recession-Hard/Soft Landing

Our Emerging Markets team believes that the risk-reward profile of the US dollar remains very attractive. First, if US growth stays robust, US interest rate expectations will rise because rate cuts priced in will not be realized. Rising interest rates will…

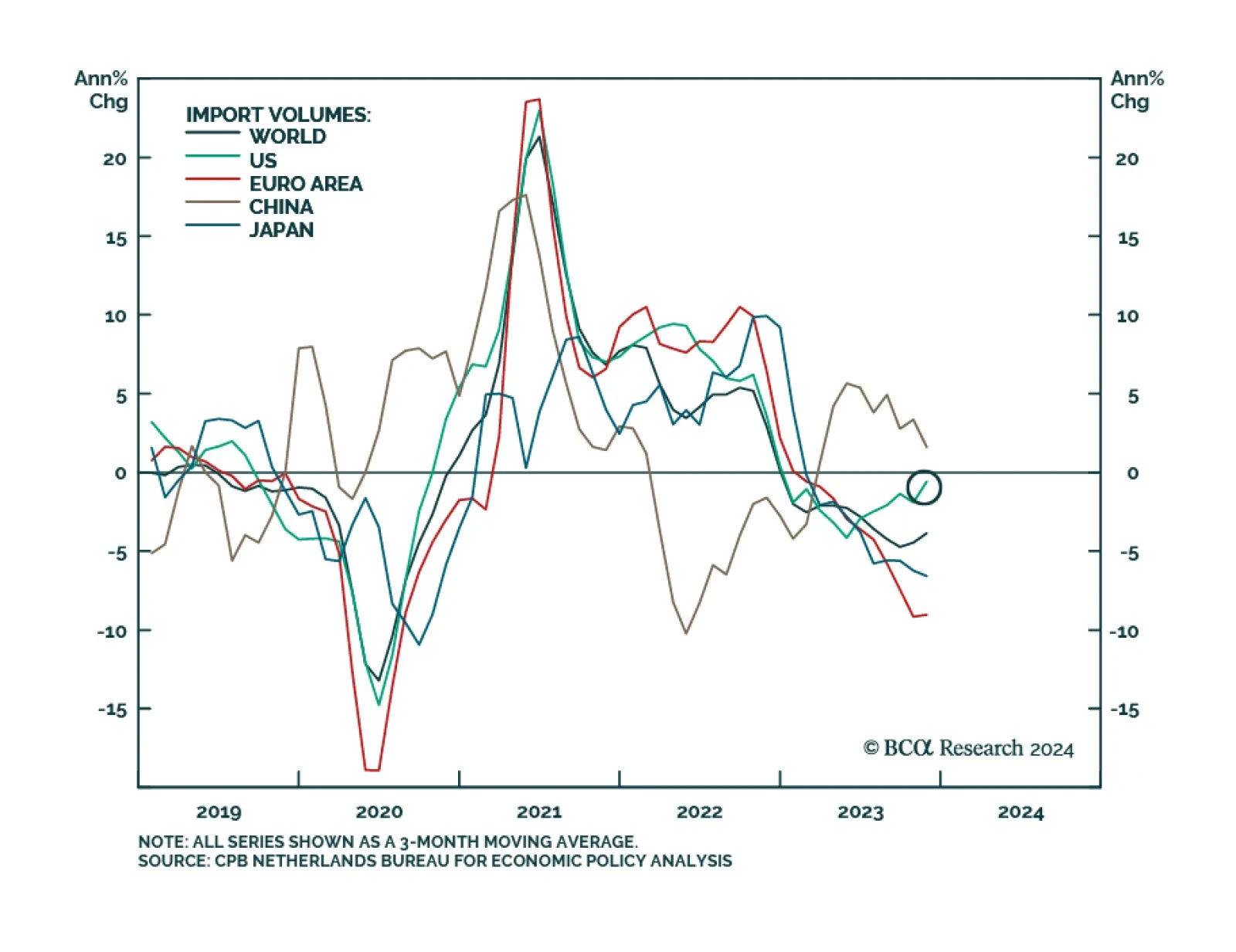

Over the past few months we have been highlighting that there are some budding signs of a recovery in global manufacturing activity. Most notably, the new orders-to-inventories ratio of Sweden’s manufacturing PMI has been rebounding. To the extent that Sweden…

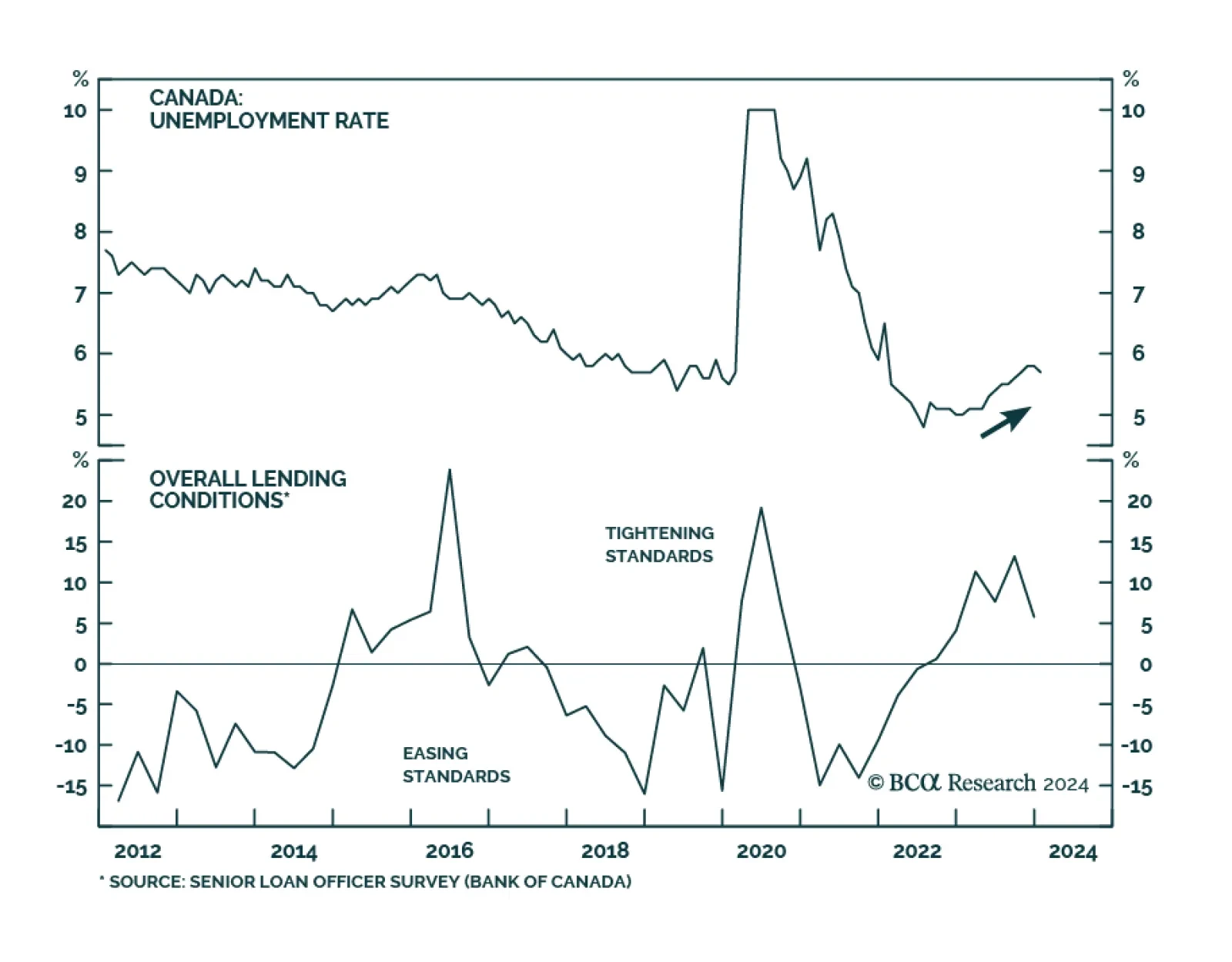

The latest Canadian data suggest that although demand is cooling down, the Canadian economy is not in freefall. The unemployment rate fell for the first time since December 2022, declining by 0.1 percentage points to 5.7%, compared to consensus…

Easier financial conditions, rising home prices, rebounding consumer sentiment, and a stabilization in manufacturing activity all augur well for near-term US growth prospects. An unsustainably low savings rate is a key risk to the US economic outlook. Our revised forecast is centered on a recession starting in late 2024 or early 2025.

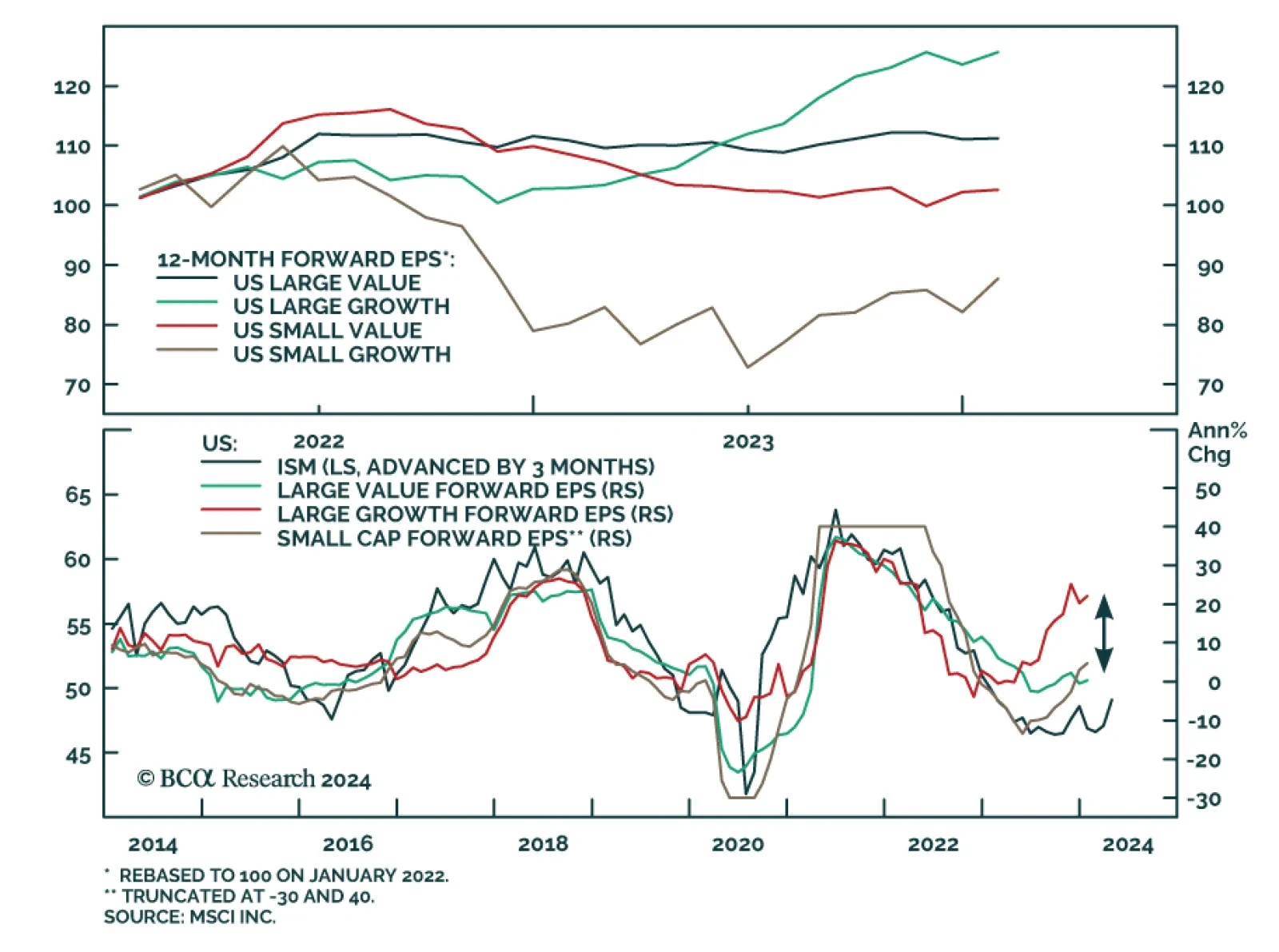

The dominance of large tech companies in the S&P 500 has caused concern amongst investors. The Magnificent Seven now represent 30% of the index. These companies have more than doubled in value over the past year, in contrast to just over 10% for the rest…

Last Friday’s blockbuster US employment report is among the recent data releases that have focused investors’ attention on the possibility that resilient economic conditions will reduce the magnitude of Fed easing this year. Markets are now priced for roughly…

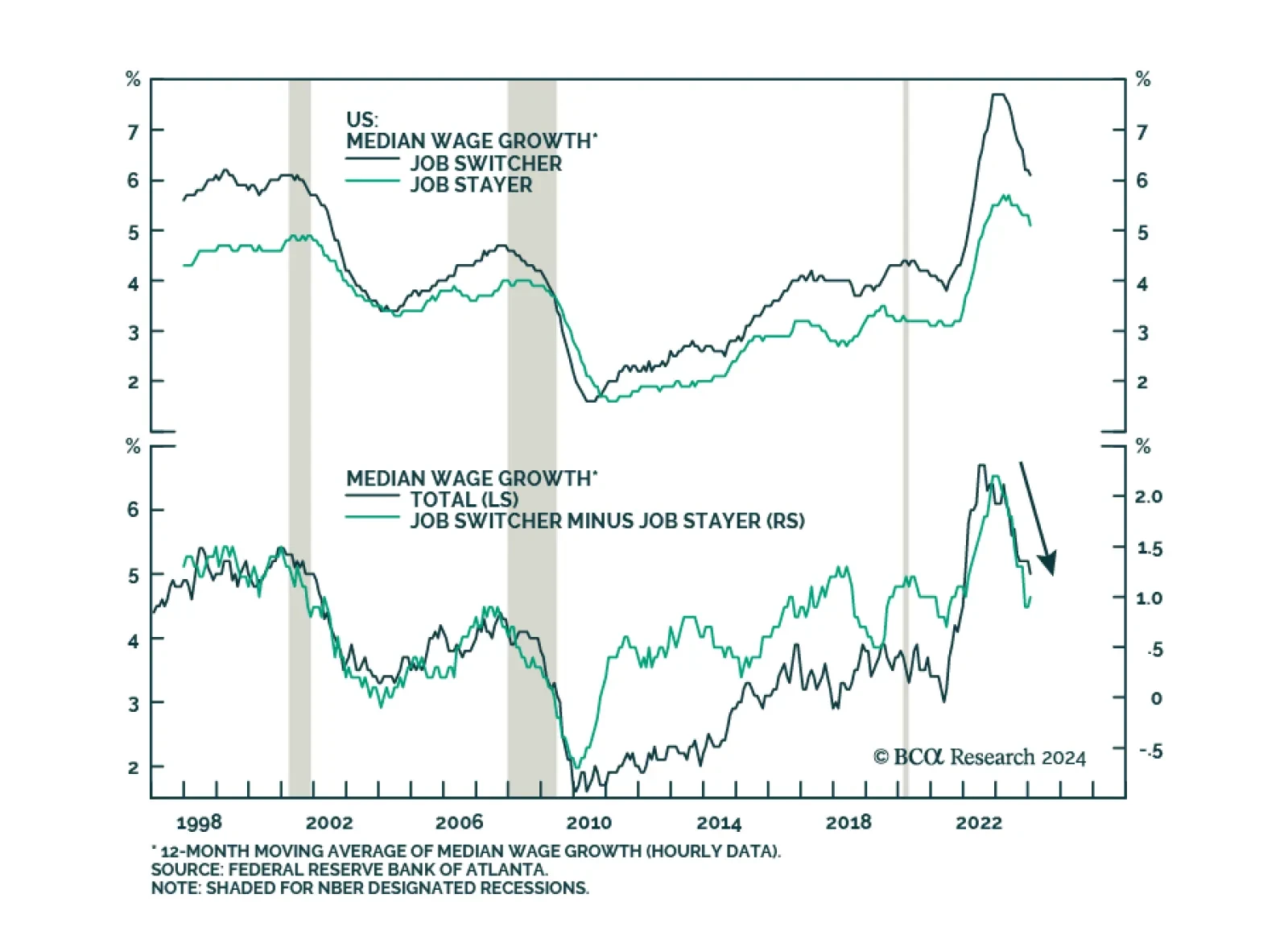

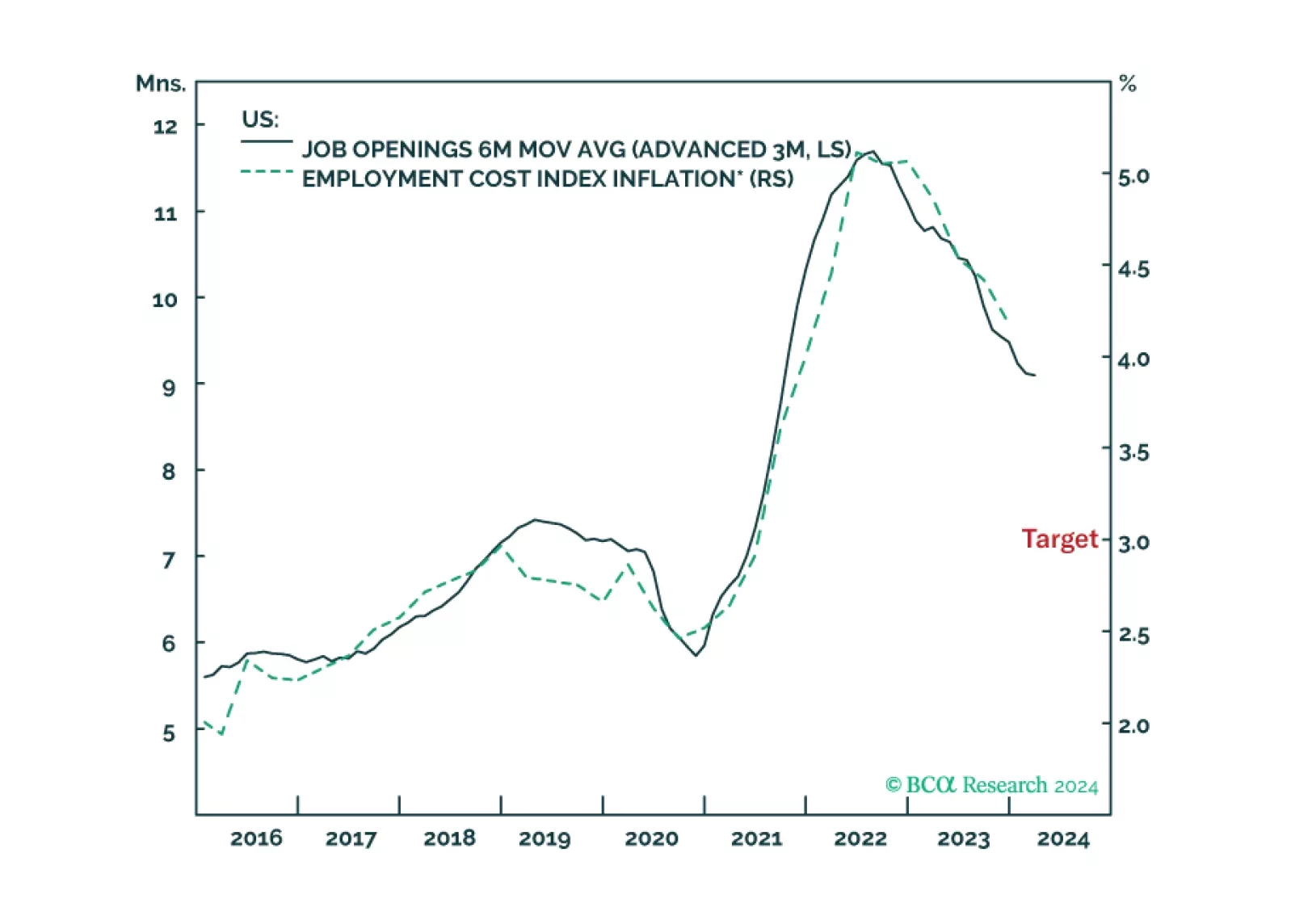

After having surged in the second half of 2021 and early 2022, the Atlanta Fed’s Wage Growth Tracker peaked in mid-2022 and has since been on a general downtrend. The latest reading of 5.0% in January is a continuation of this process, marking the lowest pace…

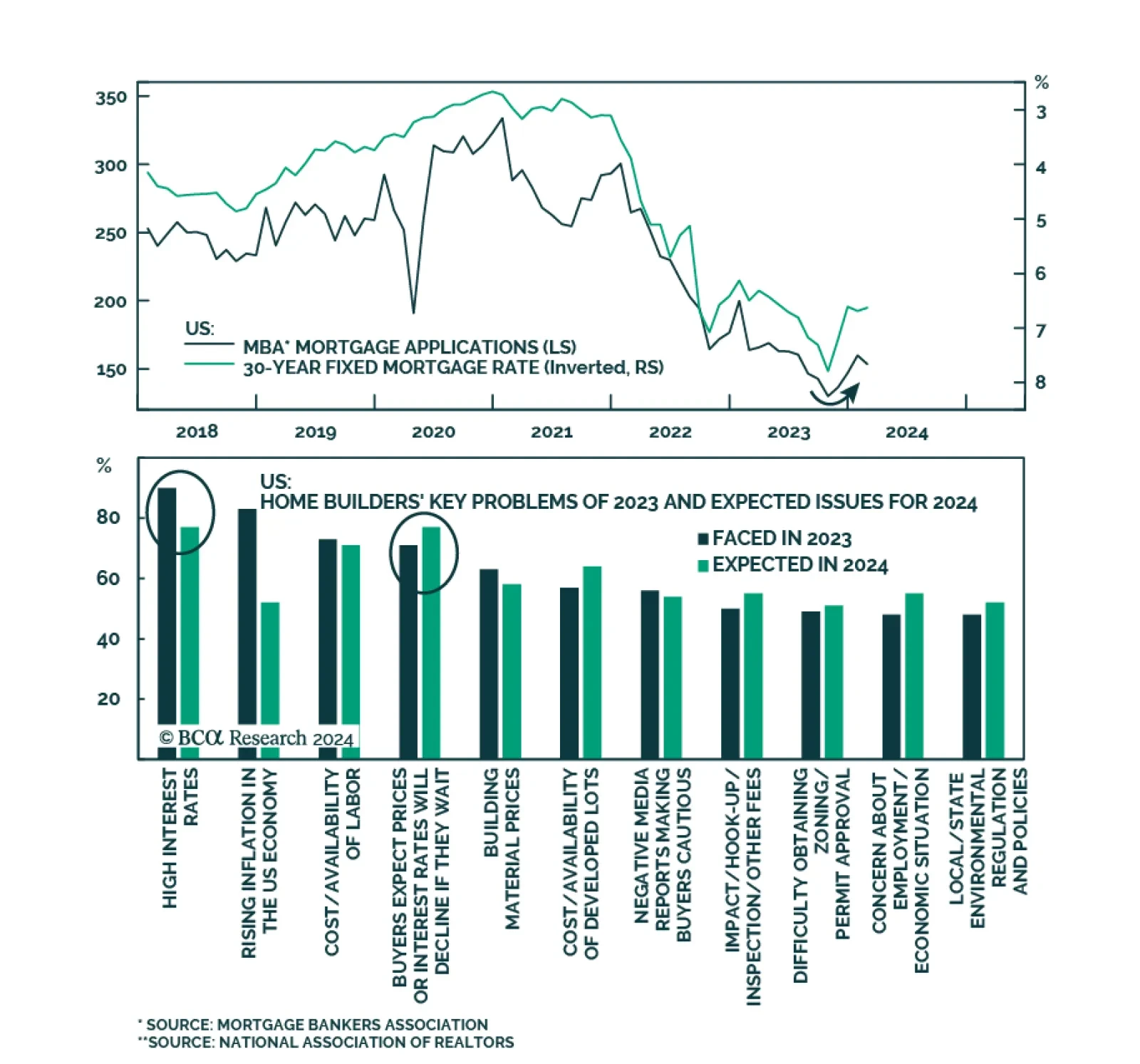

According to the latest MBA weekly survey, mortgage applications increased 3.7% in the week ending February 2. The contents of the report were mixed. A 12.3% jump in the refinance index drove the increase while mortgage applications to purchase a home fell by…

The disinflation to date has been benign because it has come almost entirely from improving supply. But the supply-side tailwind has exhausted, so the last mile of the journey to 2 percent inflation will be the hardest, especially in the US and the UK. We discuss the investment implications. Plus, we highlight an interesting sector pair-trade.

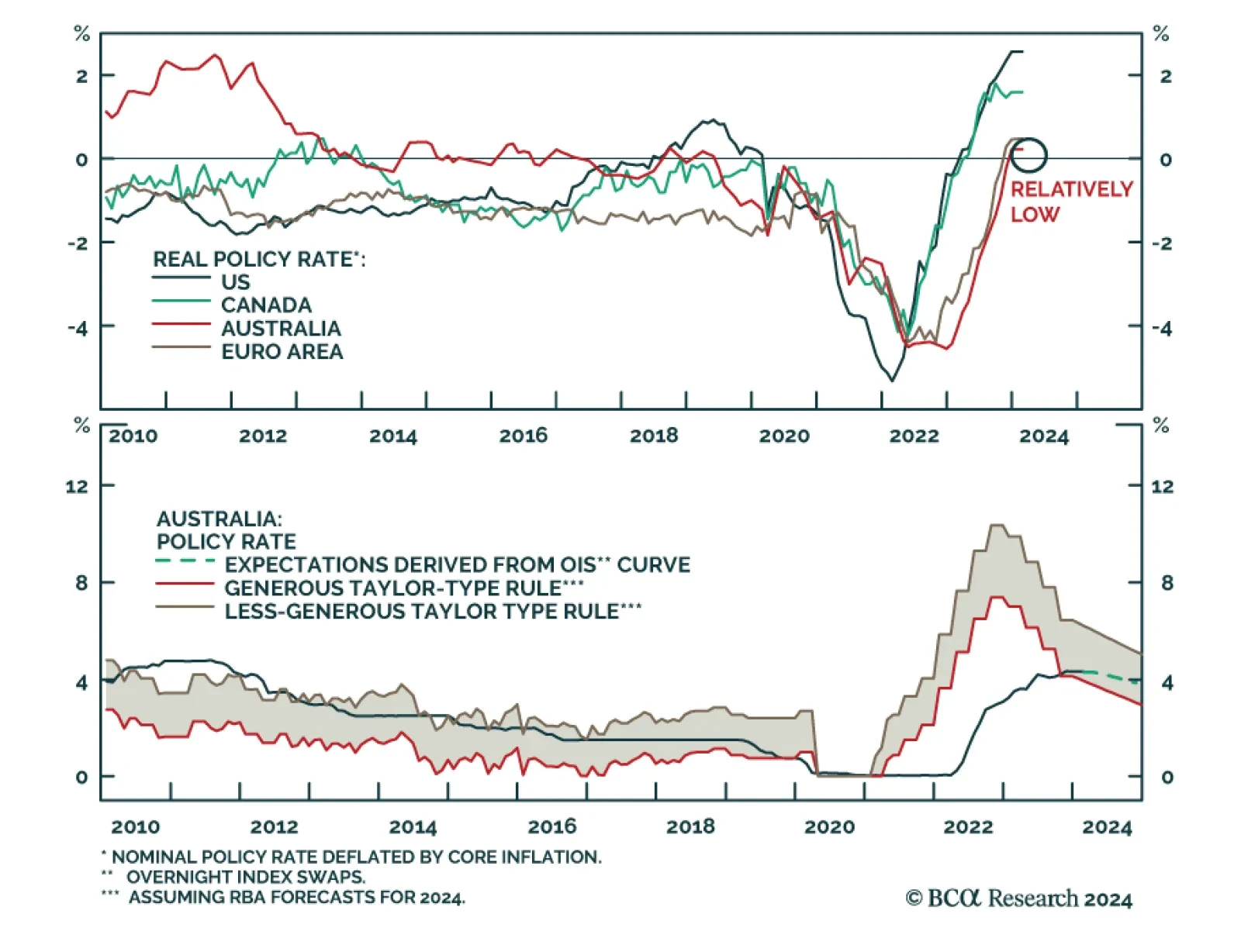

As expected, the Reserve Bank of Australia kept the policy rate unchanged at 4.35% on Tuesday. The updated economic forecasts show a downward revision to the growth outlook for this year versus the previous round of projections released in November. The…