Recession-Hard/Soft Landing

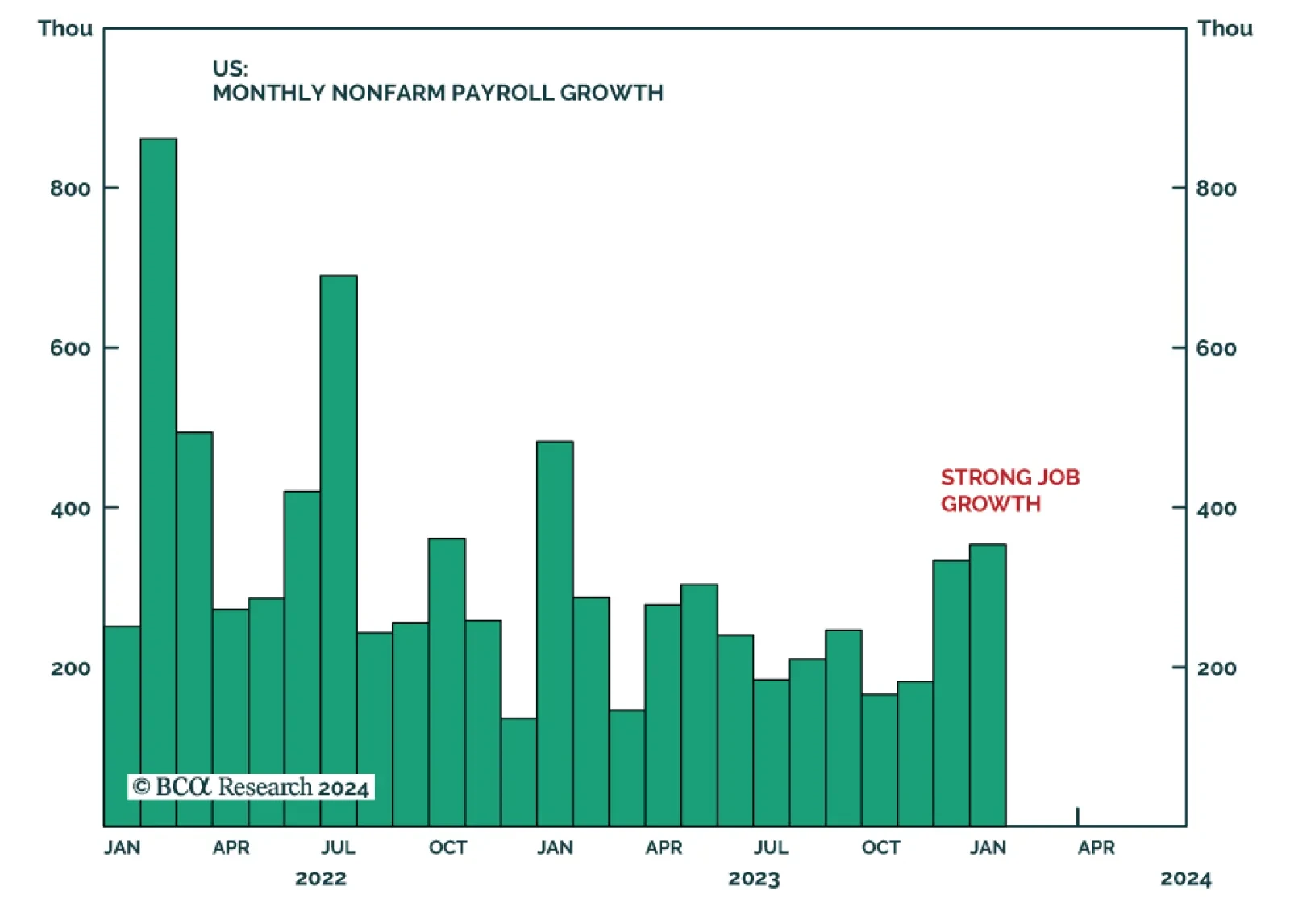

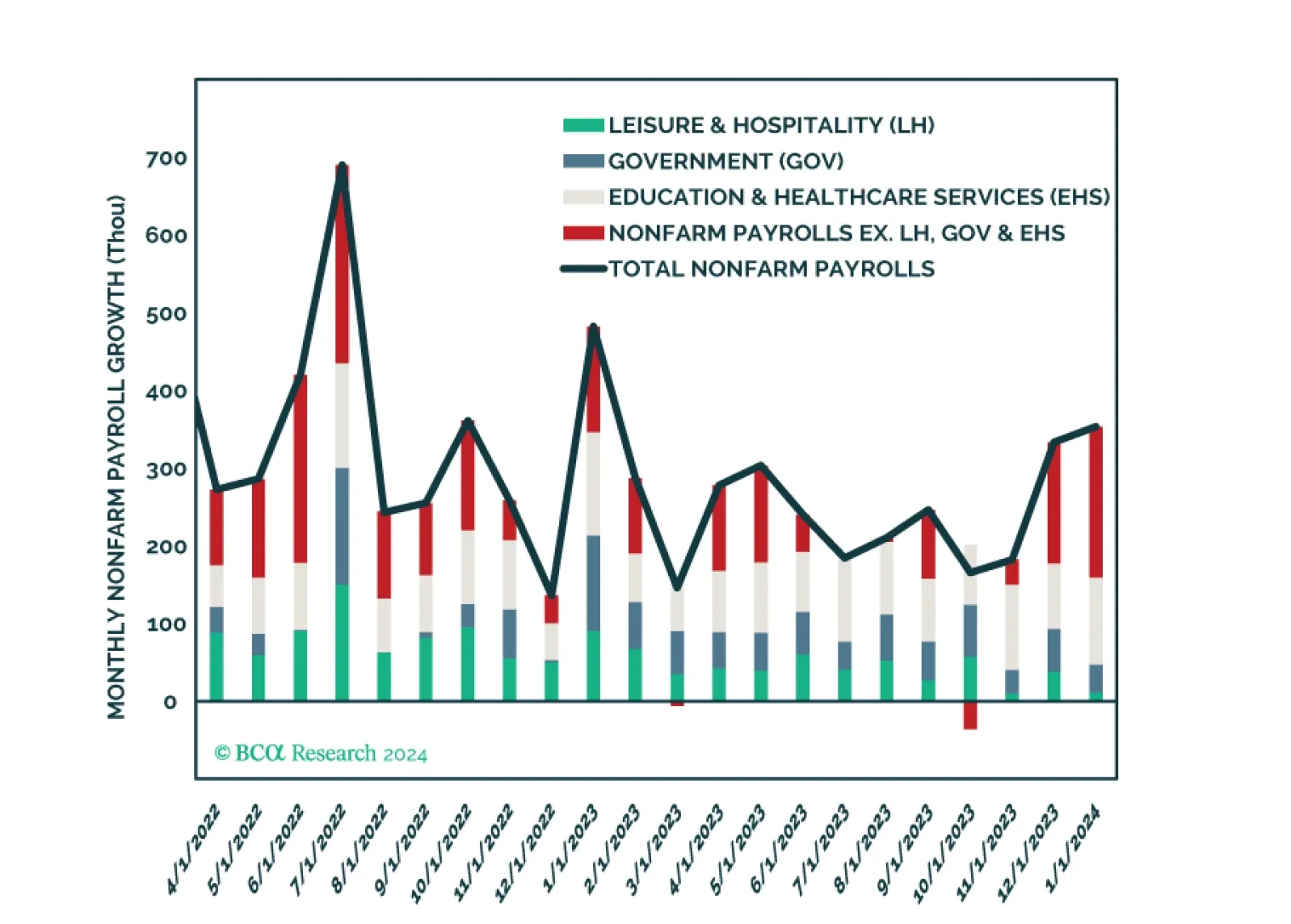

The US Employment report came in well above consensus expectations on Friday, delivering a strong positive signal on labor market conditions in January. The 353 thousand increase in nonfarm payroll employment beat expectations of a slowdown to 185 thousand.…

Our thoughts on bond positioning following this morning’s employment data.

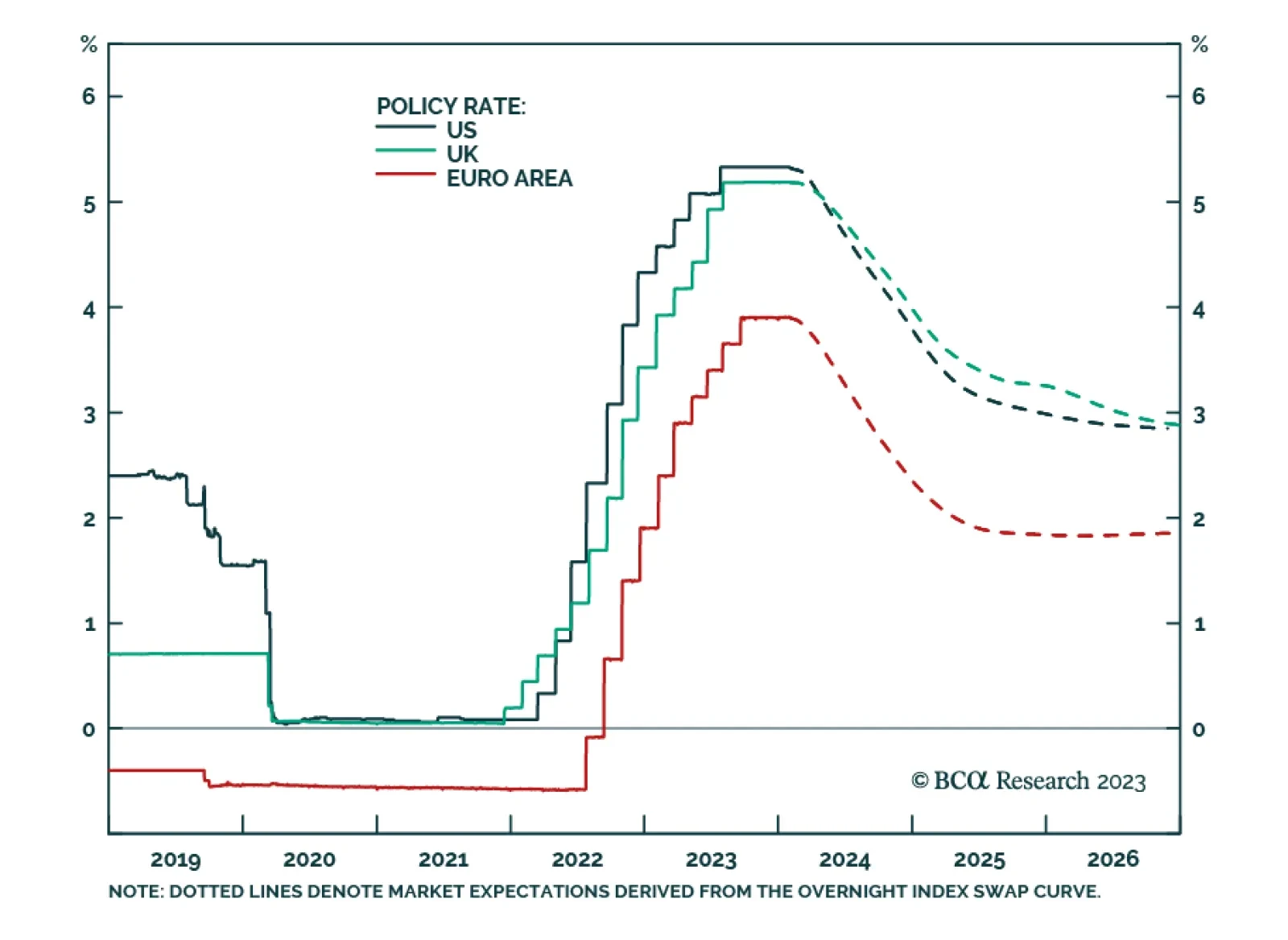

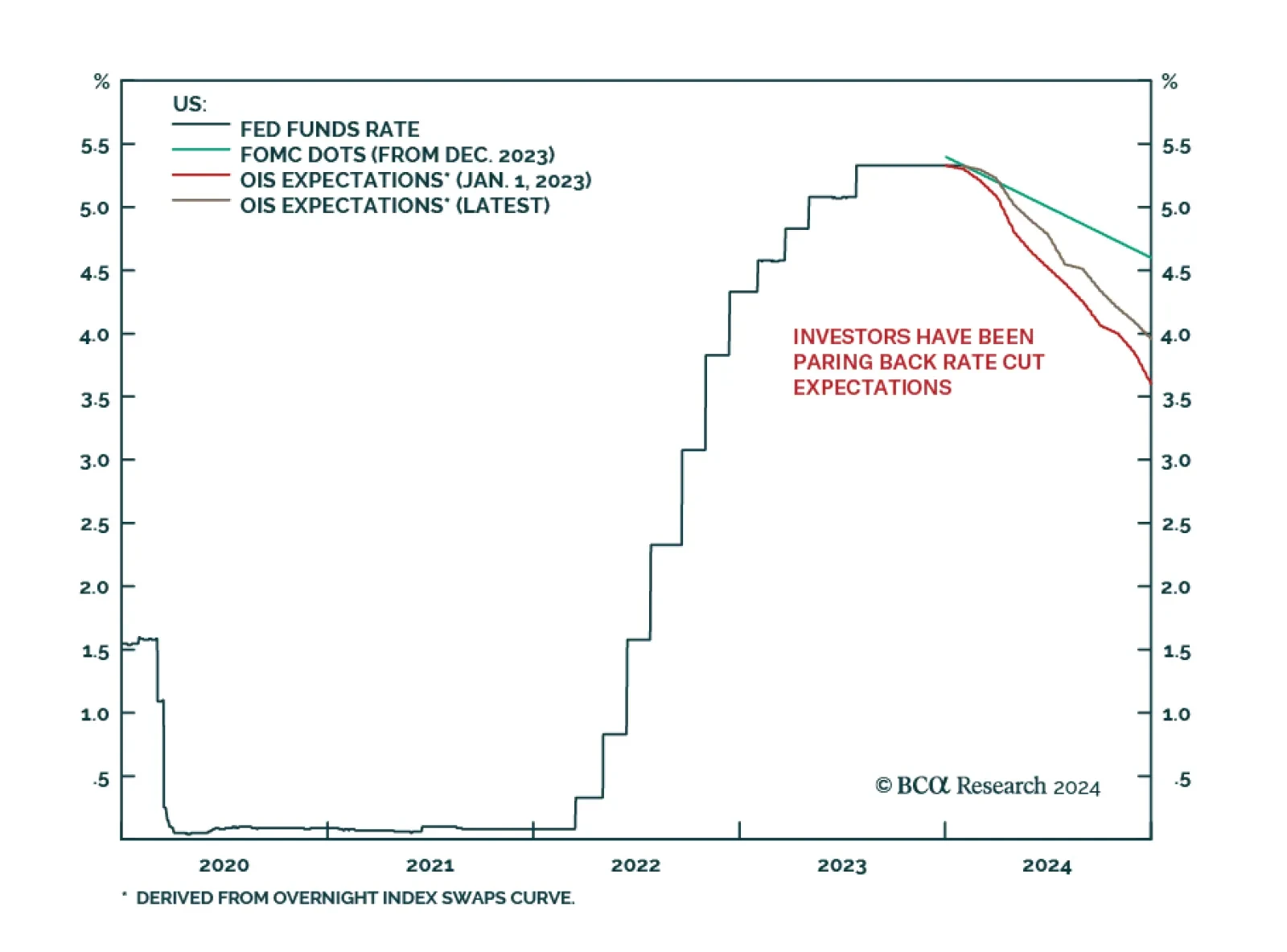

Given the huge disparities in wage inflation between the US, euro area and UK, it is remarkable that the markets are pricing near-identical rate cuts from the Fed, ECB, and BoE of around 150 bps through 2024. Assuming central banks don’t behave recklessly –…

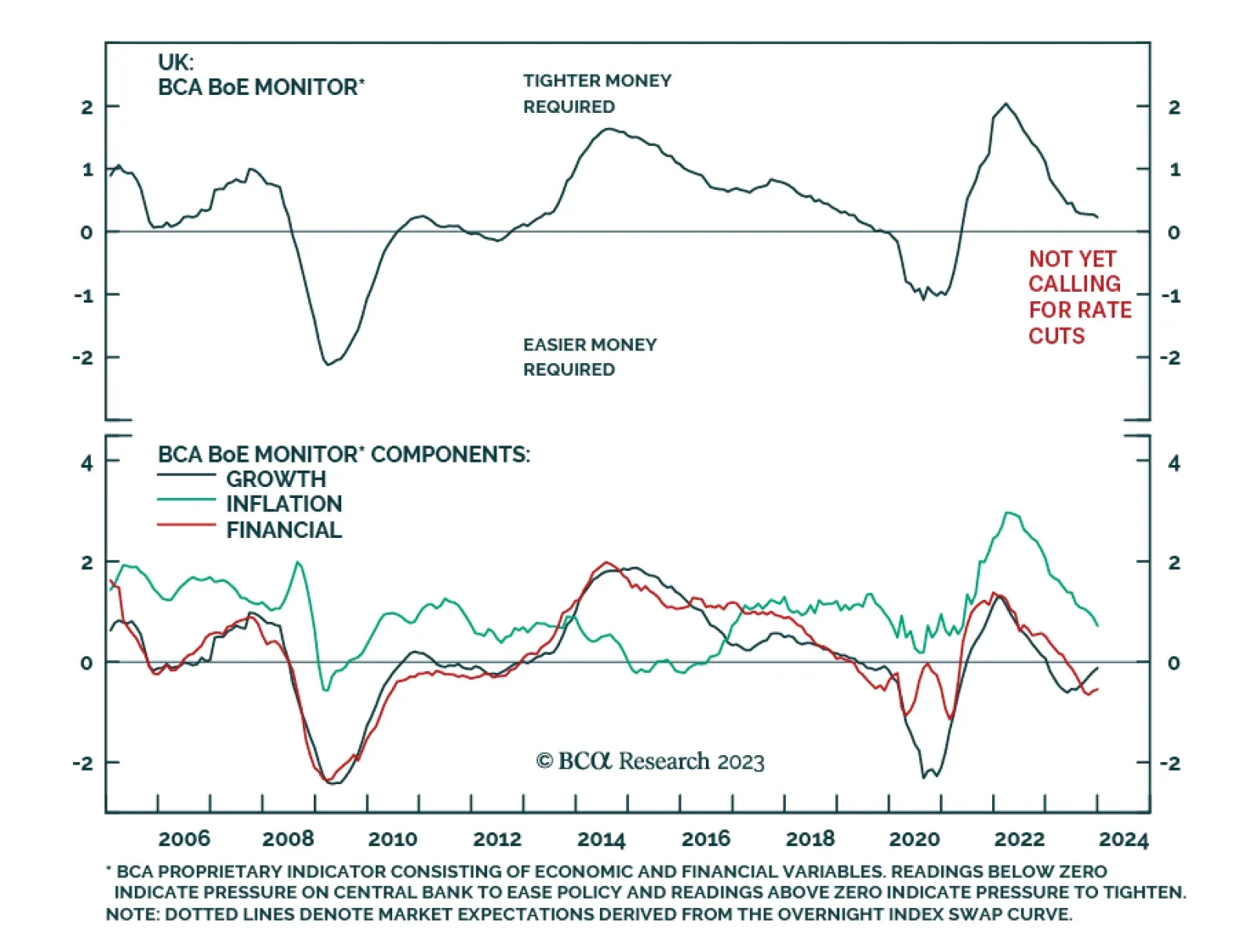

As expected, the Bank of England voted to keep its bank rate unchanged at 5.25% on Thursday – maintaining policy on hold for the fourth consecutive meeting. Two of the nine MPC members voted in favor of a 25bps rise (one less than in December) while one…

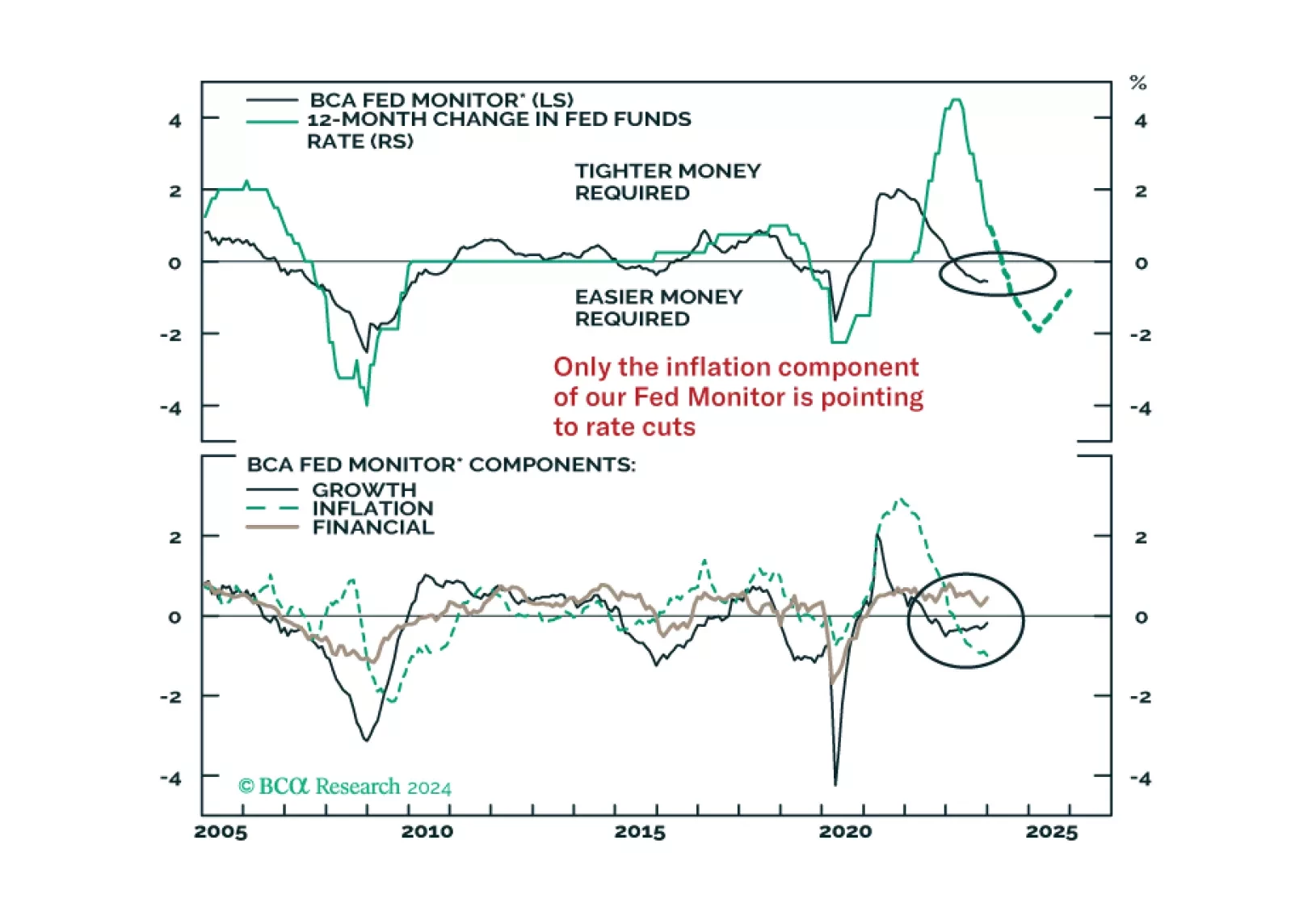

In this Insight, we share our thoughts on yesterday’s FOMC meeting and the Fed’s likely next moves, with implications for US bond strategy.

When will the US also buckle under high rates? We expect a US recession to begin around mid-year. Stay defensive.

As expected, the Fed decided to keep policy unchanged at the conclusion of the FOMC meeting on Wednesday. The changes to the Fed Statement generally indicate that the central bank is preparing to move towards easing monetary policy. Specifically, the…

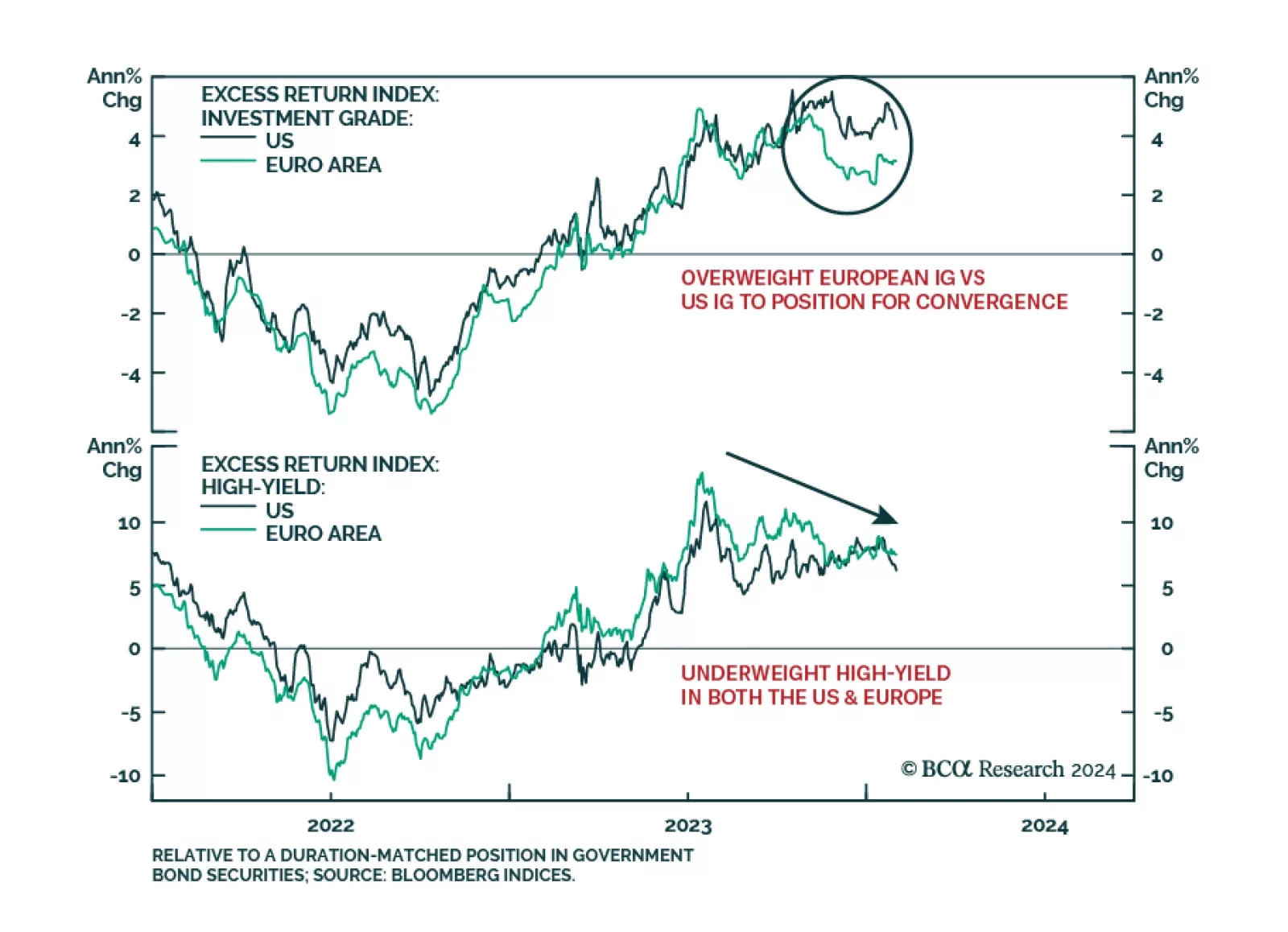

The strong H2/2023 rally in global credit markets can be attributed to lower global inflation and the associated reduction in global interest rate volatility. However, our colleagues at BCA Research’s Global Fixed Income Strategy service argue that credit…

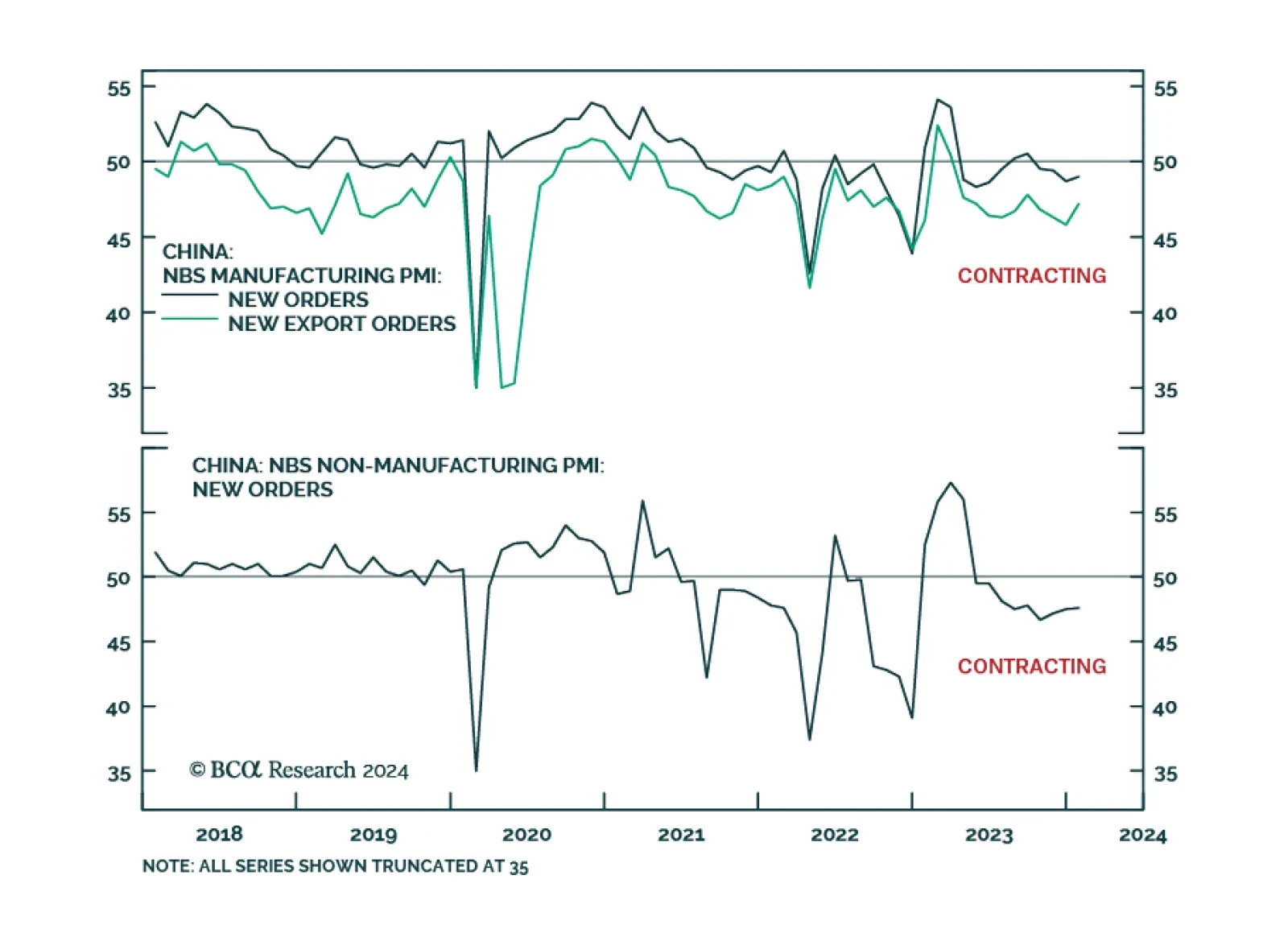

China’s official NBS PMI indicates that growth conditions remain sluggish. Although the composite index ticked up from 50.3 to 50.9, it is still barely in expansionary territory. Notably, the manufacturing PMI – which inched up by 0.2 points in January –…

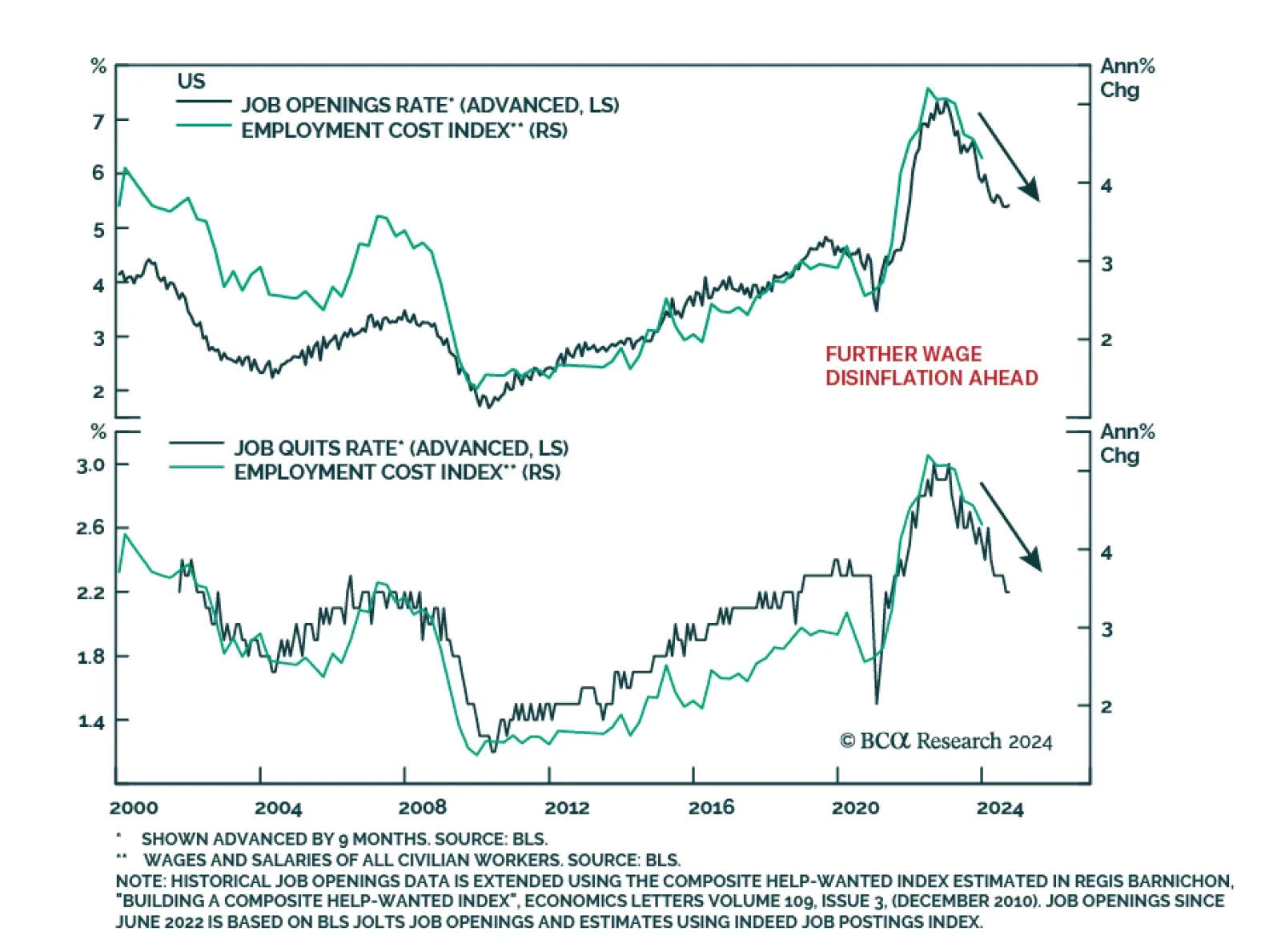

The US Employment Cost Index for Q4 delivered a positive signal that the disinflation process is intact. The ECI’s slowdown from 1.1% q/q to 0.9% q/q came in softer than anticipations of 1.0% q/q. This marks the slowest pace of quarterly increase since 2021Q2…