Recession-Hard/Soft Landing

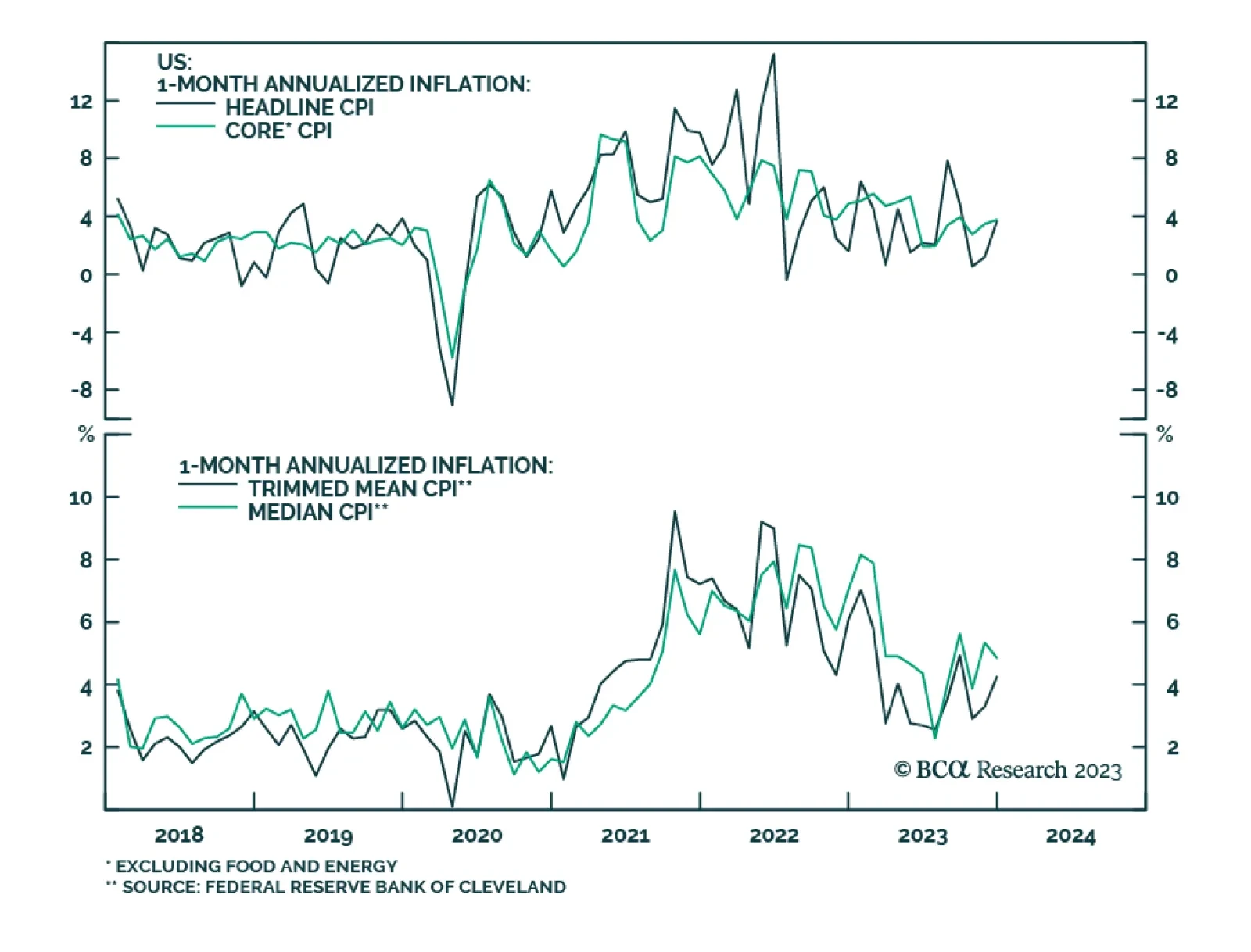

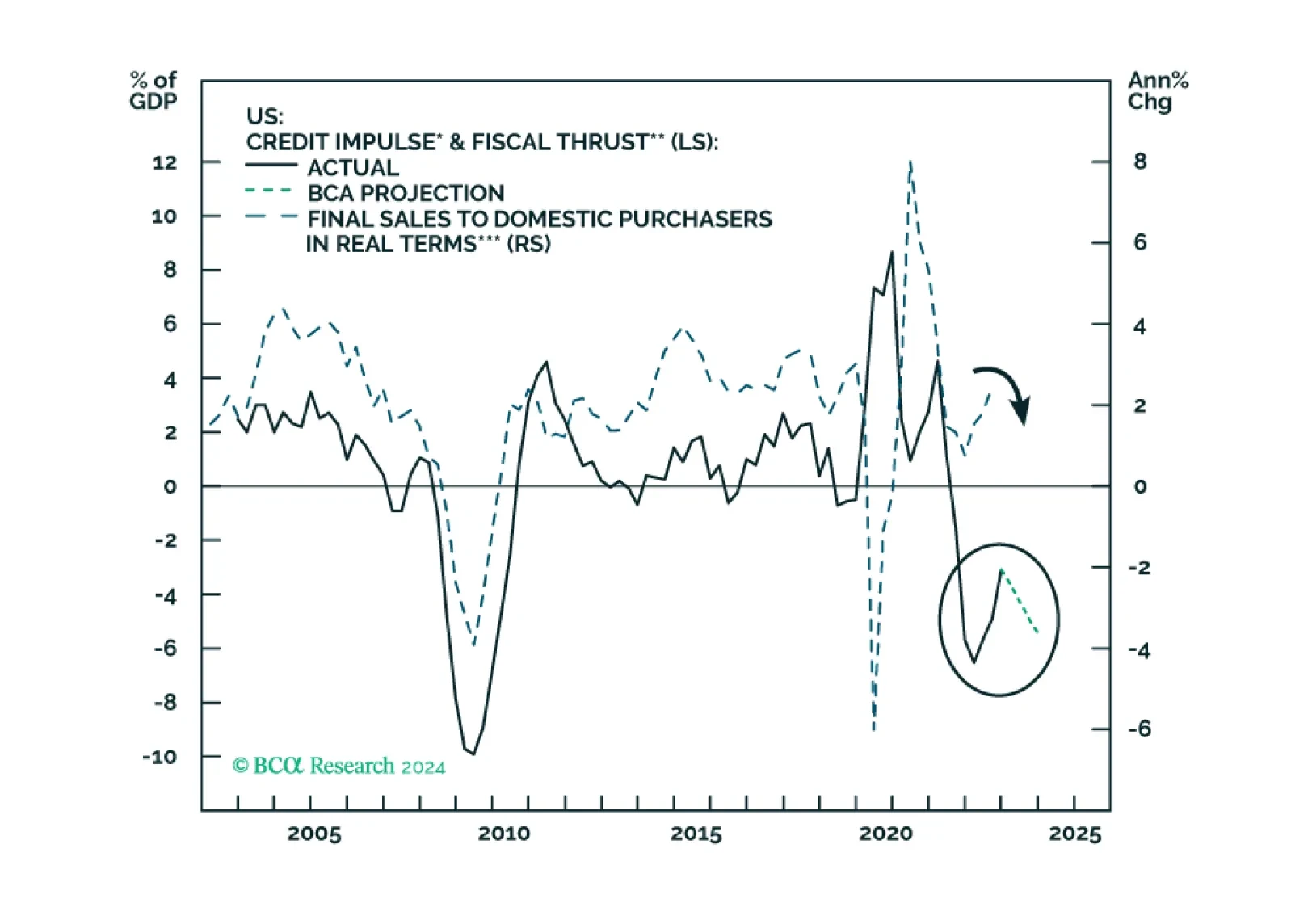

The combined US credit impulse and fiscal thrust indicator will likely relapse in 2024, heralding growth weakness. Stalling US sales volume and falling inflation, combined with sticky labor costs, will herald a non-trivial profit margin compression. The recent increase in Asian exports will likely prove to be a mid-cycle improvement rather than a cyclical recovery.

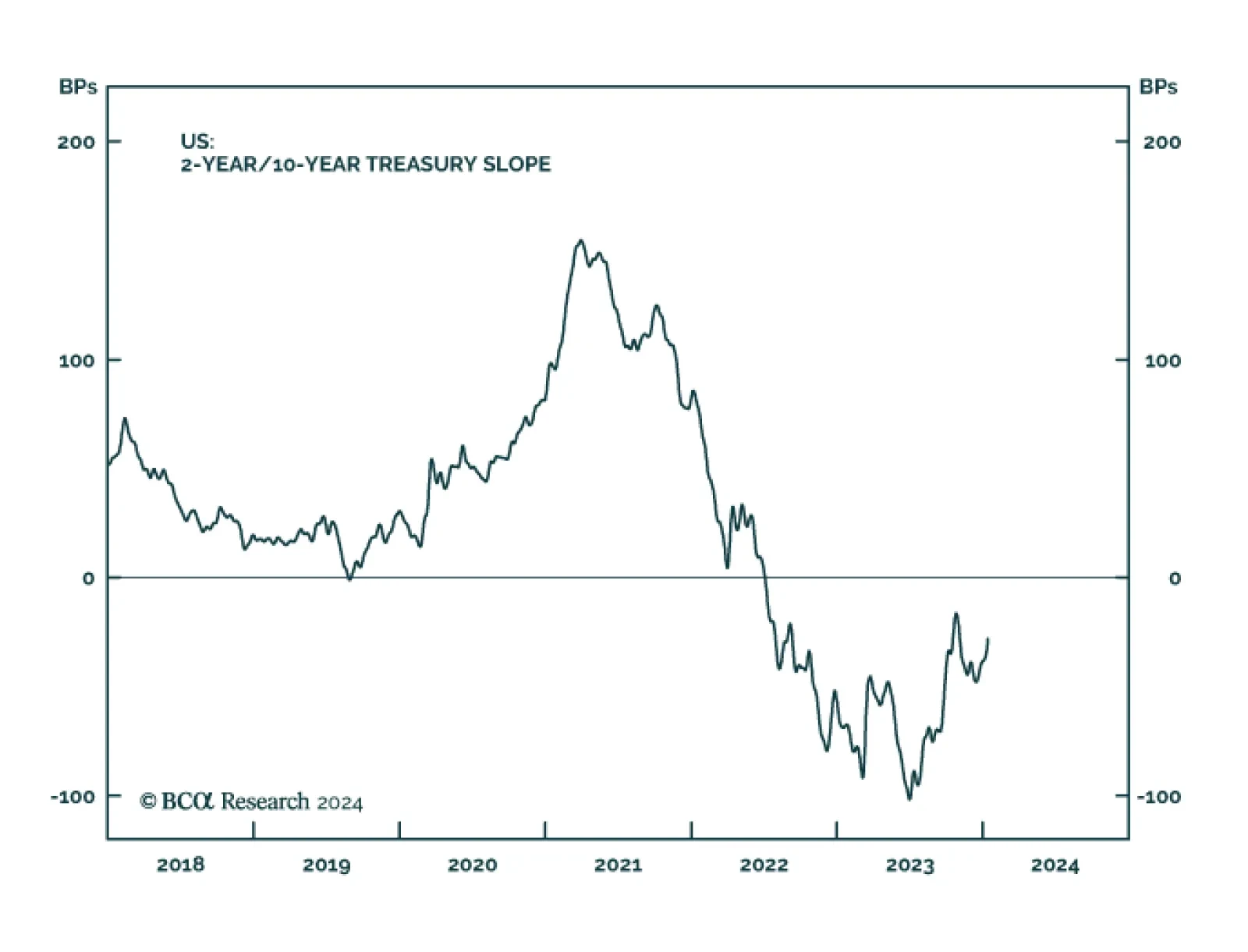

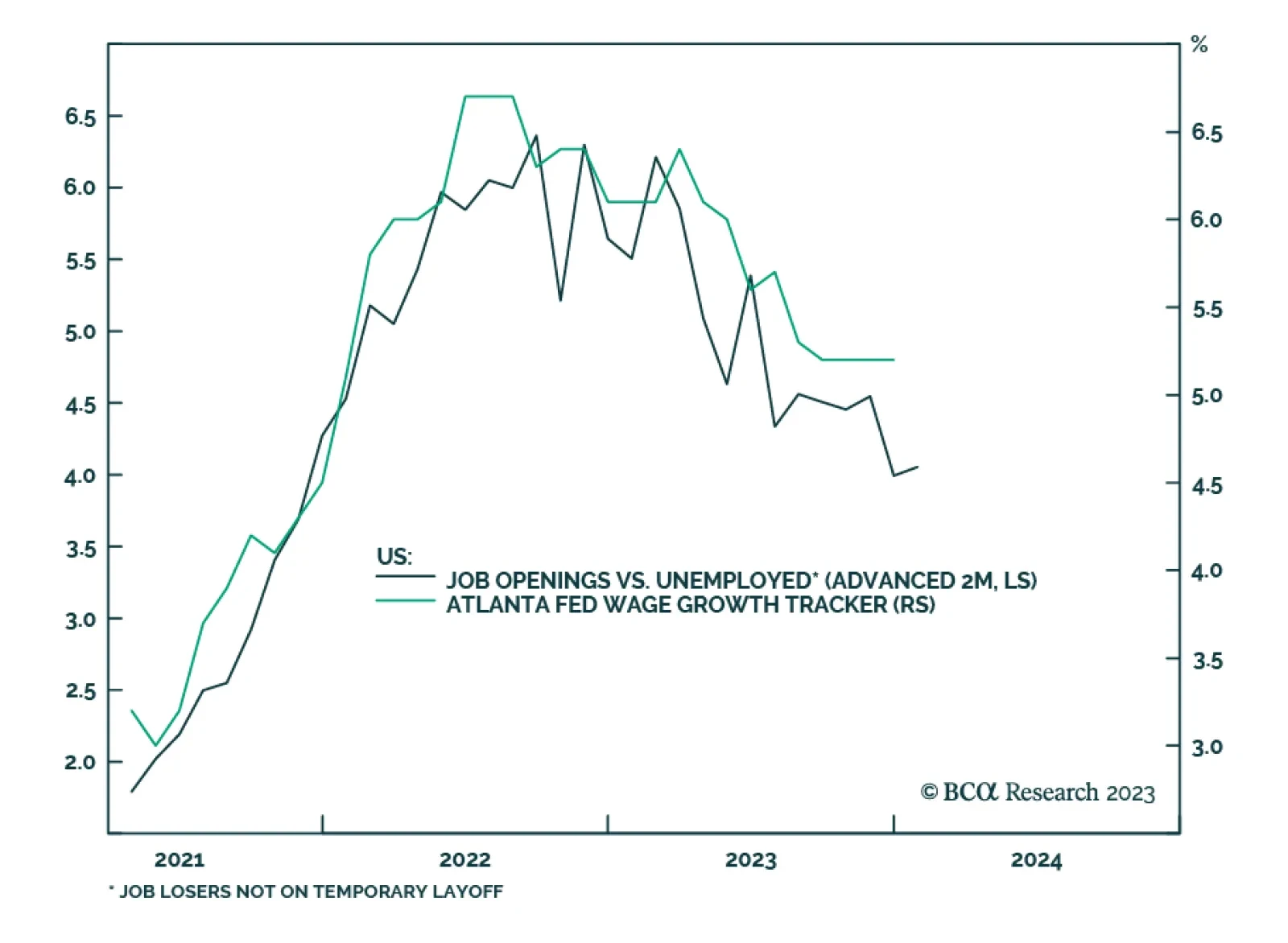

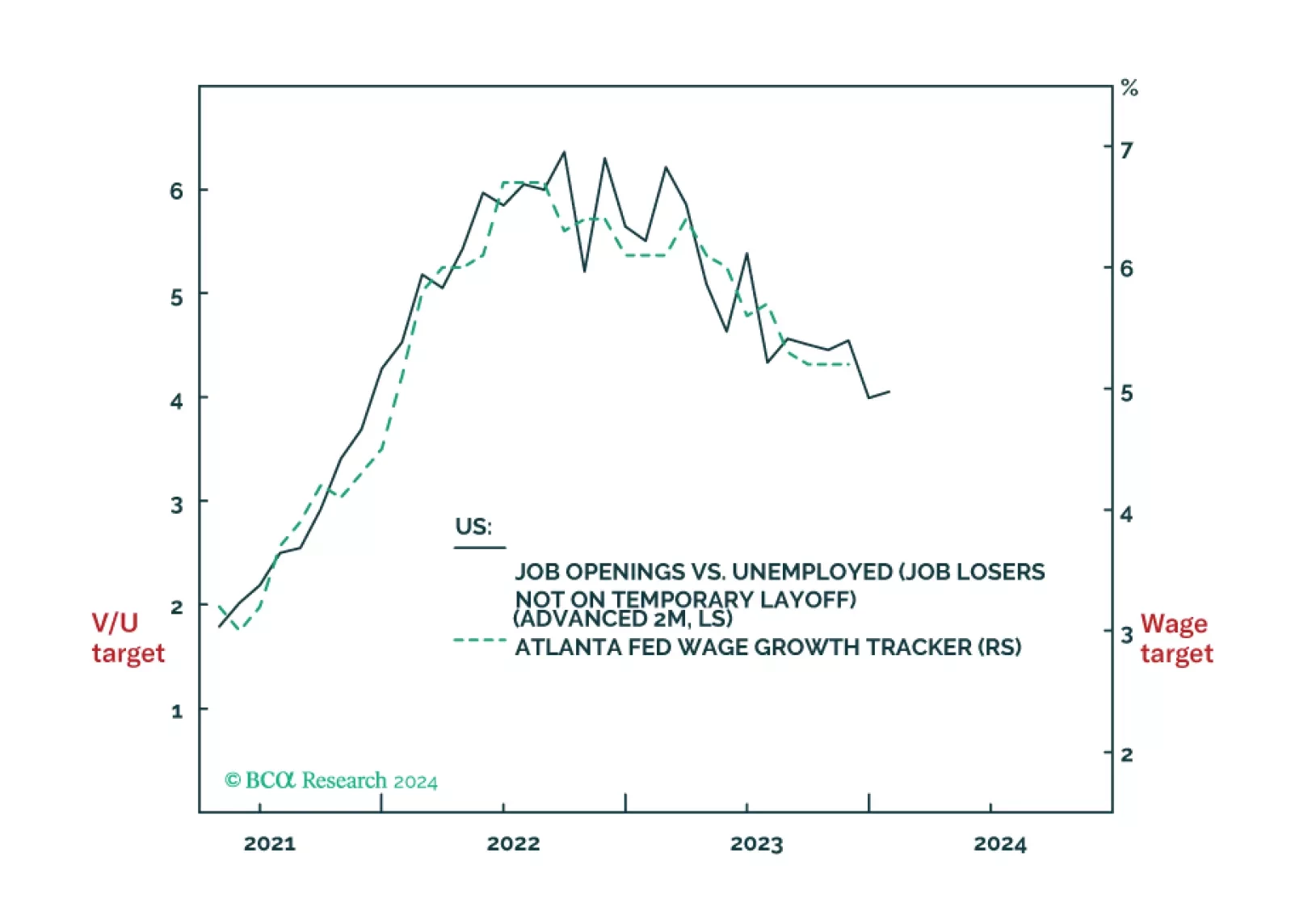

The Fed faces a dilemma. Cut rates early to avoid a recession, but at the risk of not slaying wage inflation. Or, not cut rates early to ensure that wage inflation is slayed, but at the risk of a downturn. Faced with such a dilemma, the lesser evil is to slay wage inflation even at the risk of a downturn. Meaning that the market has overpriced early rate cuts. We discuss some other investment implications, and identify two rebound candidates.