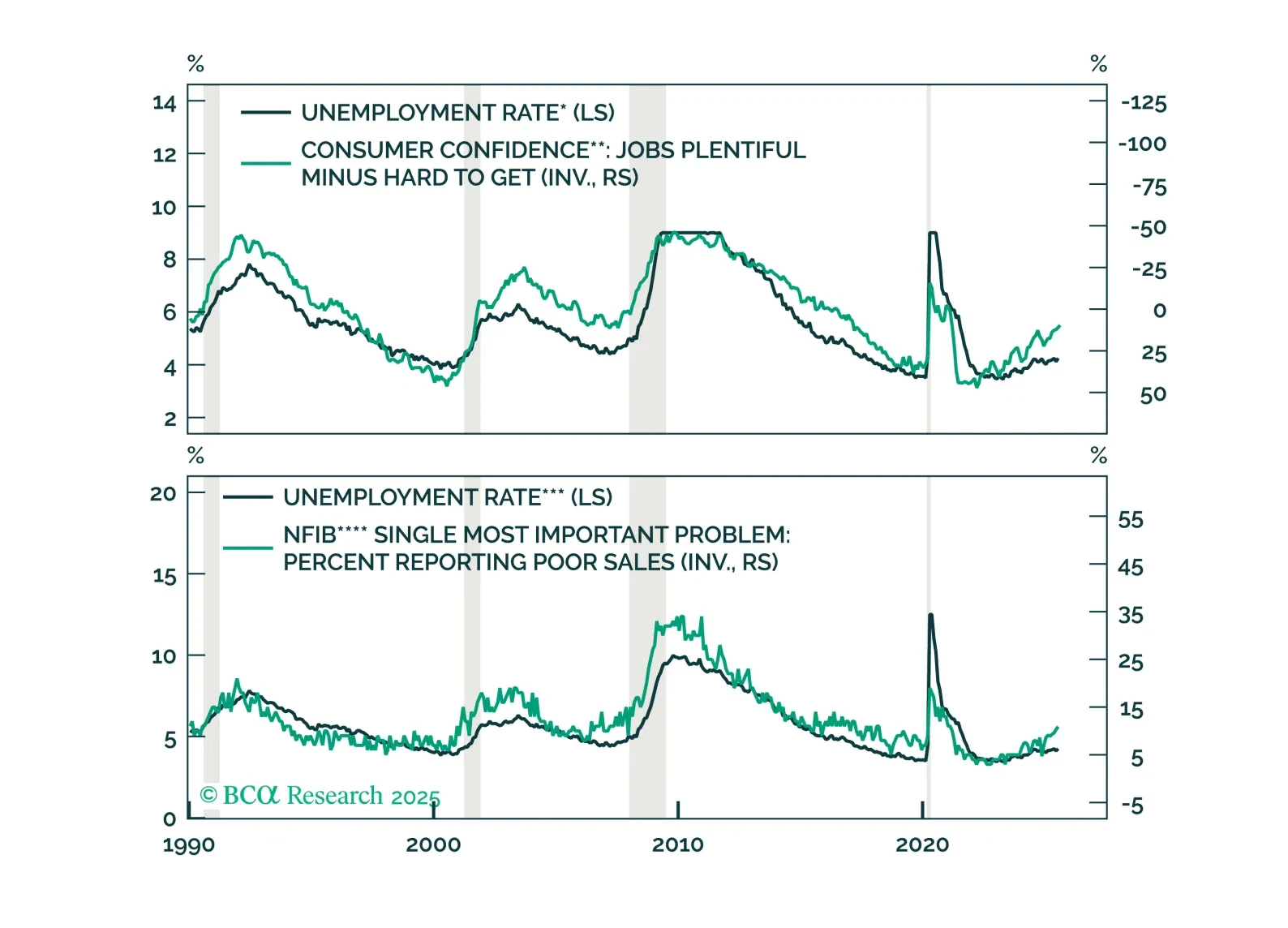

Sectors

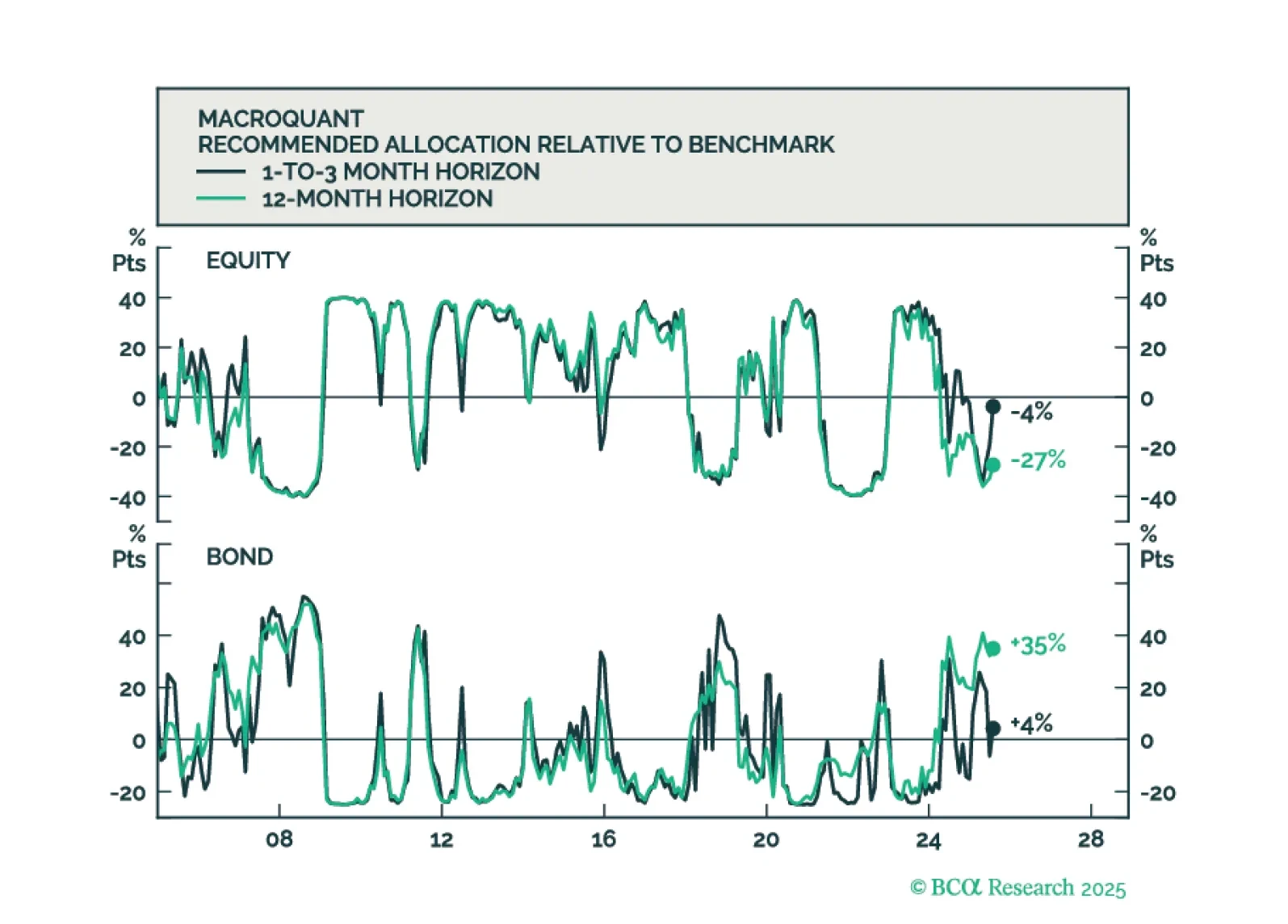

MacroQuant has downgraded equities to underweight, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is still bullish on gold.

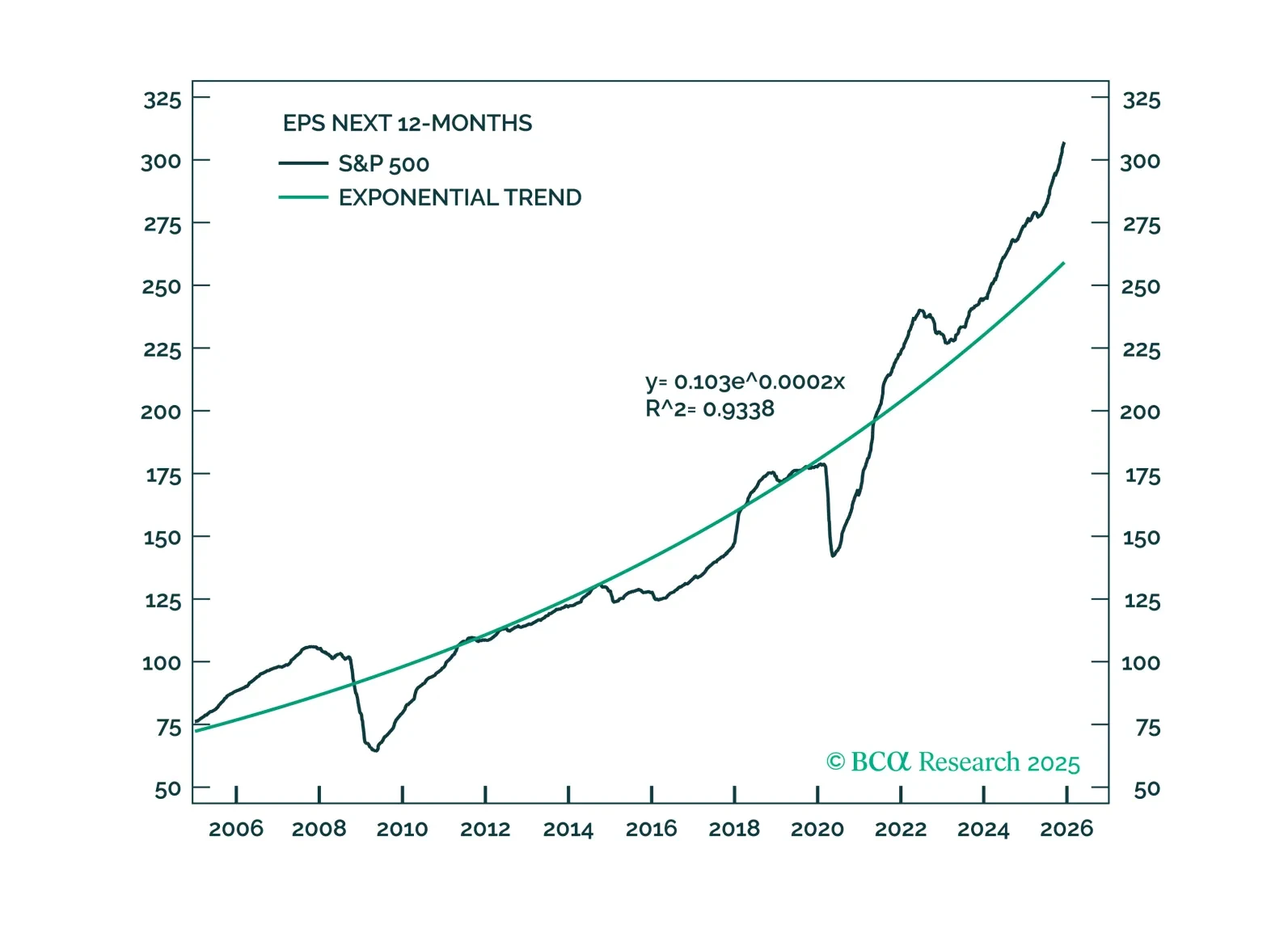

We are constructive on equities in 2026, as monetary easing, fiscal support, GenAI-related capex, and strong earnings growth are unequivocally positive for the asset class. Valuations are extended, but concerns about a bubble are overstated. Despite the favorable backdrop, we expect the S&P 500 to return only 5–10%, ending 2026 between 7,200 and 7,500.

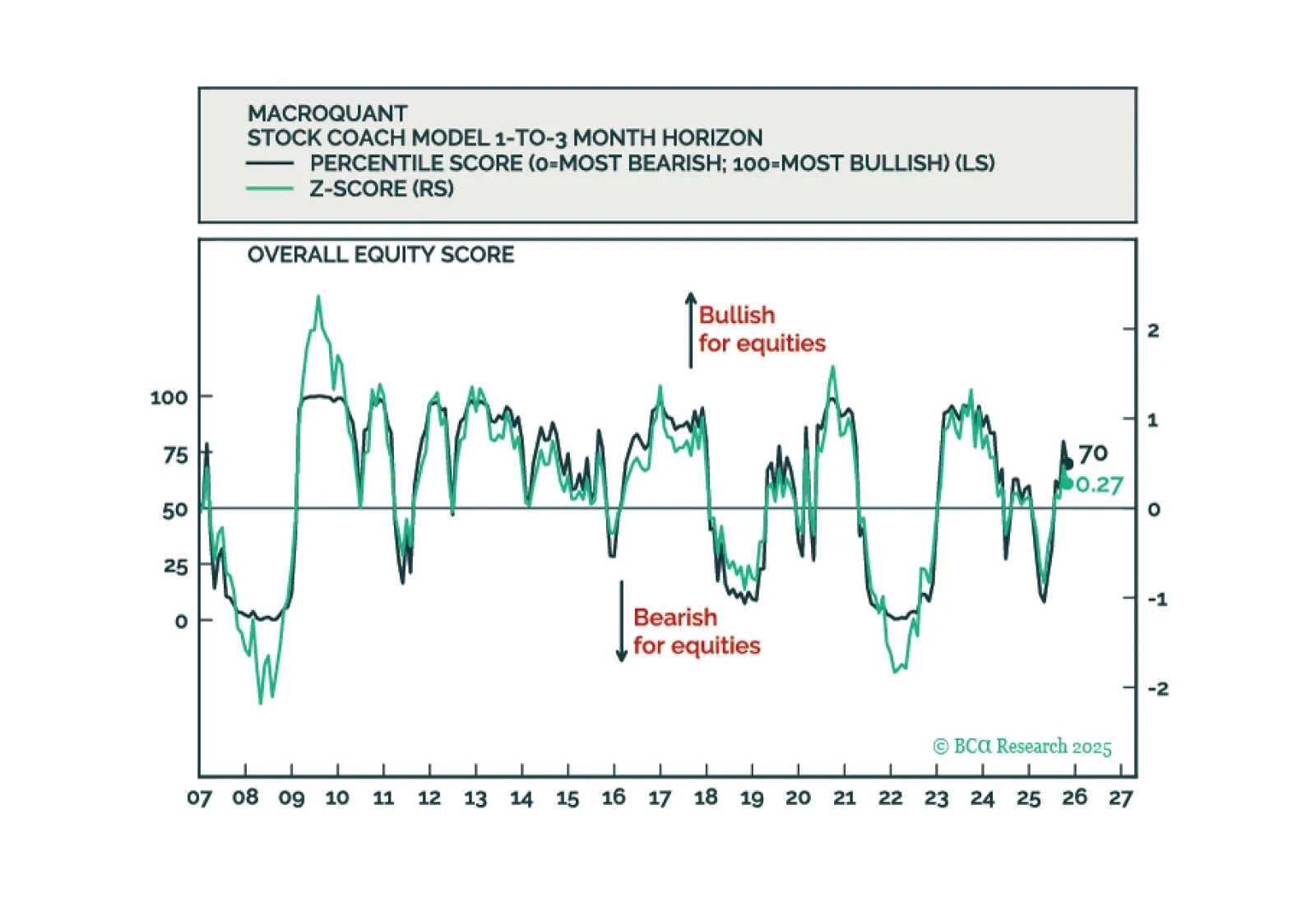

MacroQuant remains tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold.

Disparities between households and between companies’ earnings and equity performance are widening, but the overall status quo remains in place. We reiterate our neutral asset class recommendations while watching for early signs of whether activity might break out or break down.

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

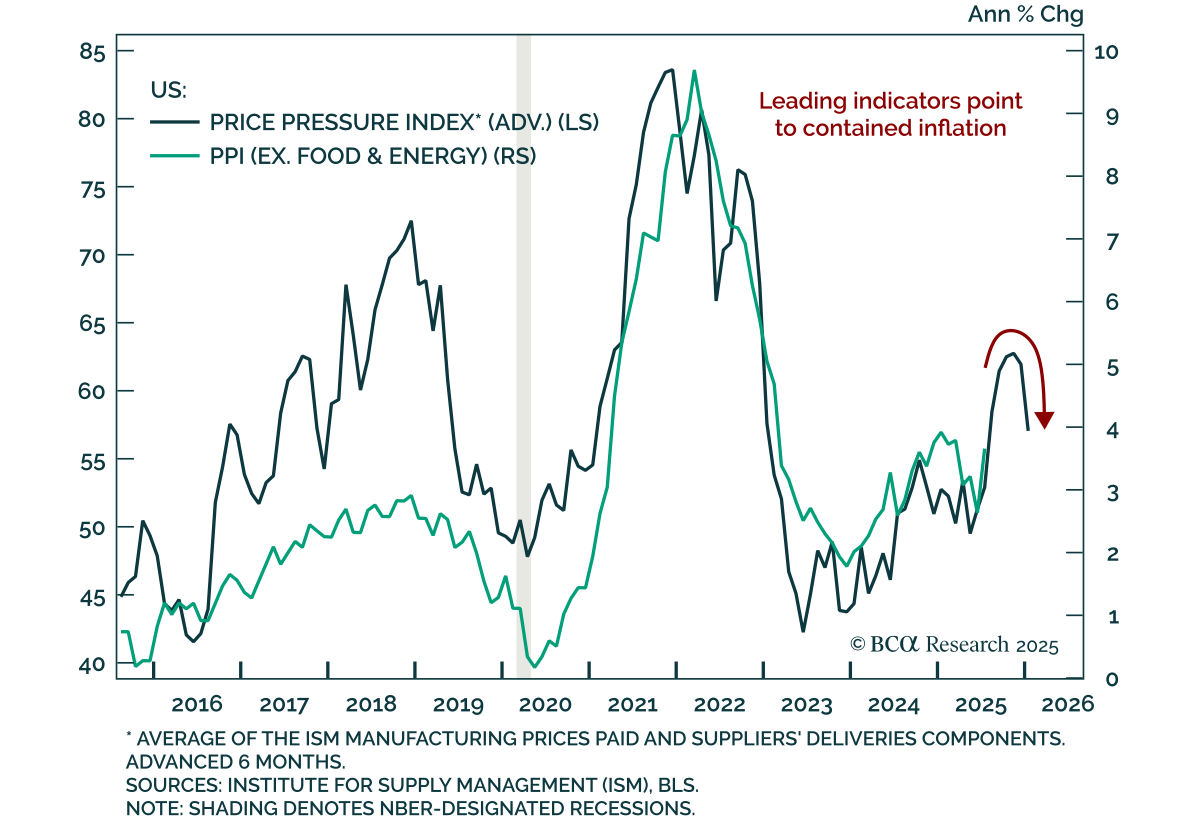

The economy is slowing, but not collapsing, and monetary easing is imminent — a backdrop that will benefit equities. We remain strategically bullish, with a close eye on GenAI and resilient earnings, even amid numerous risks. However, we are tactically cautious, as seasonality, elevated valuations, and stretched technicals present near-term headwinds.

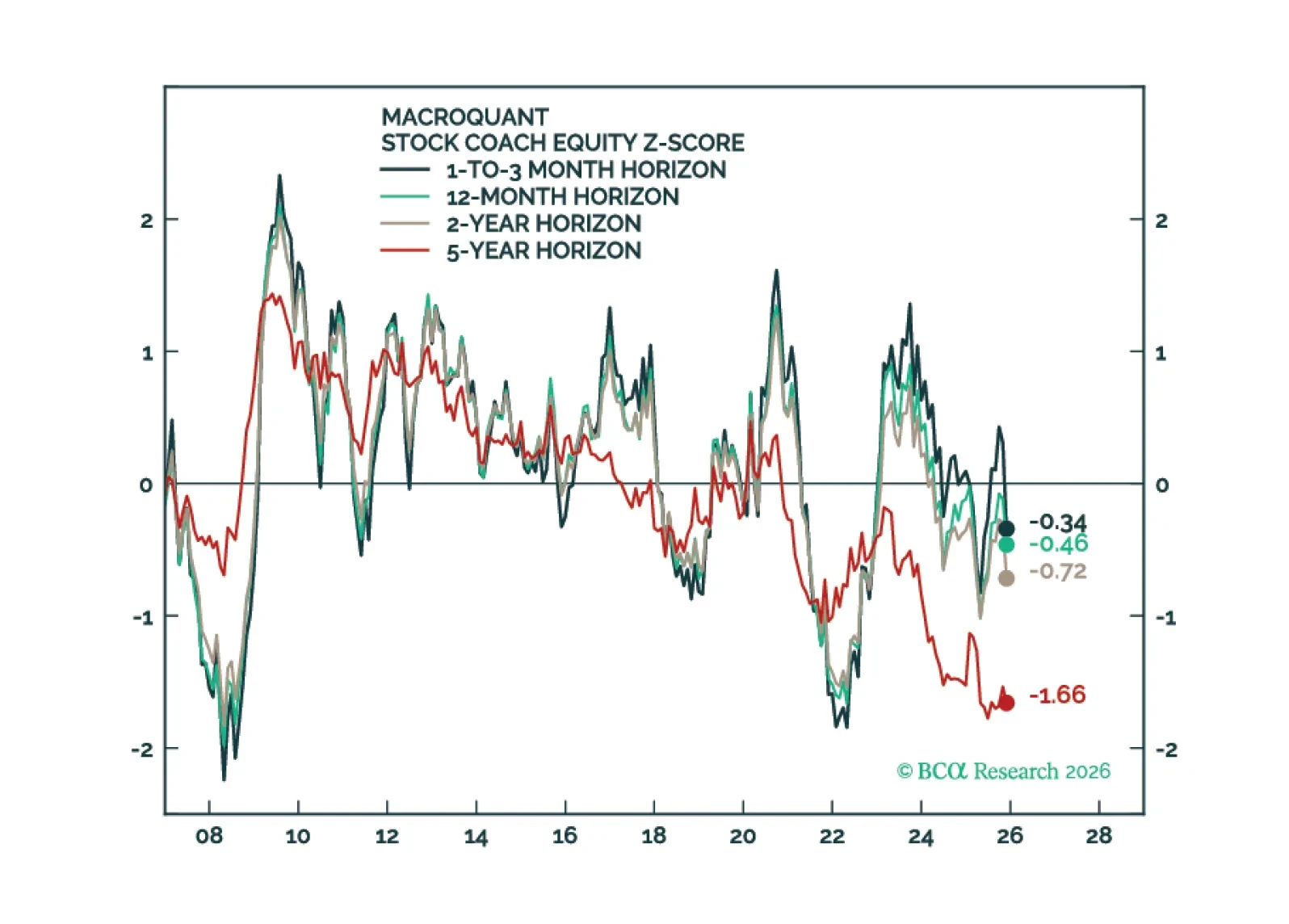

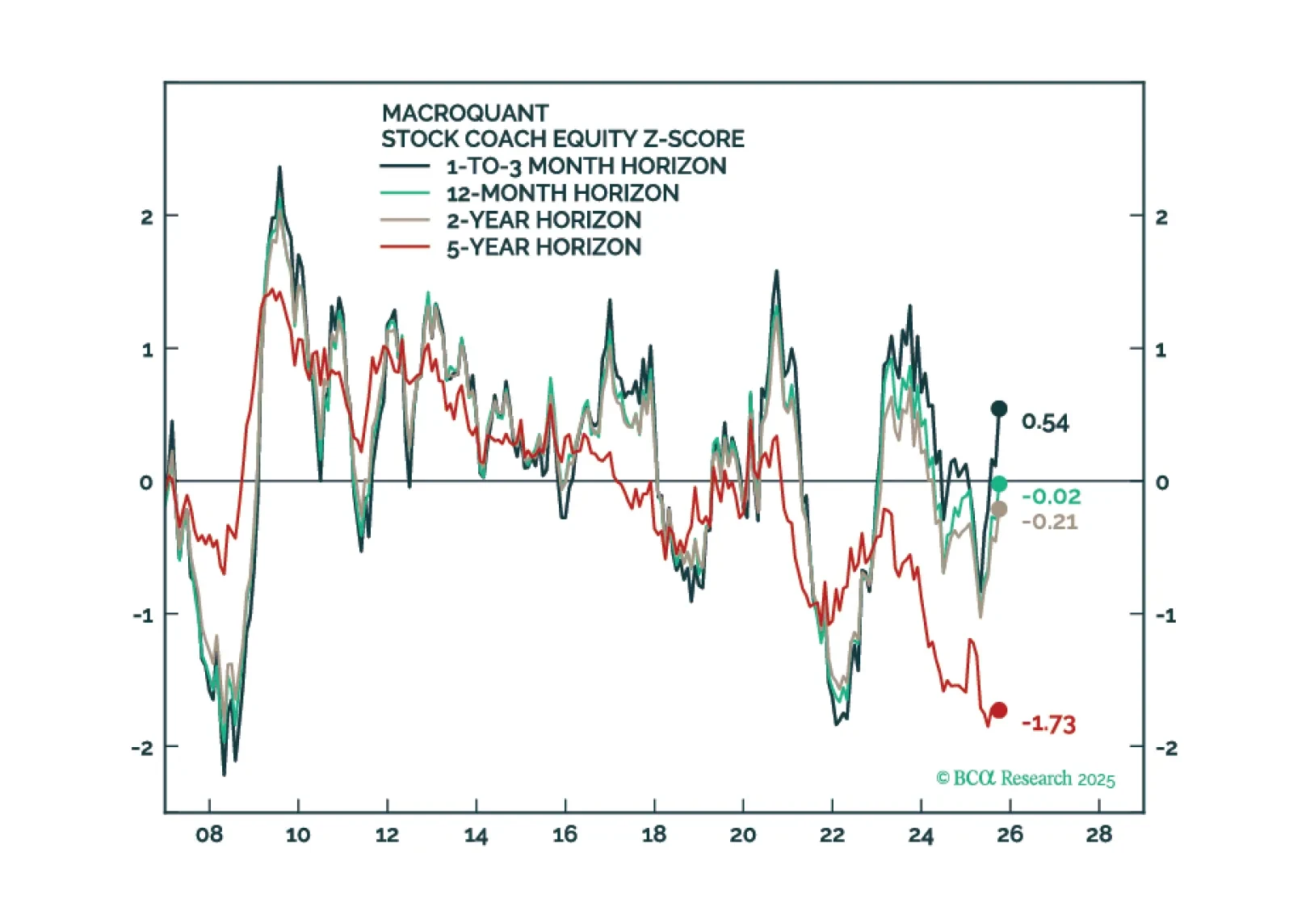

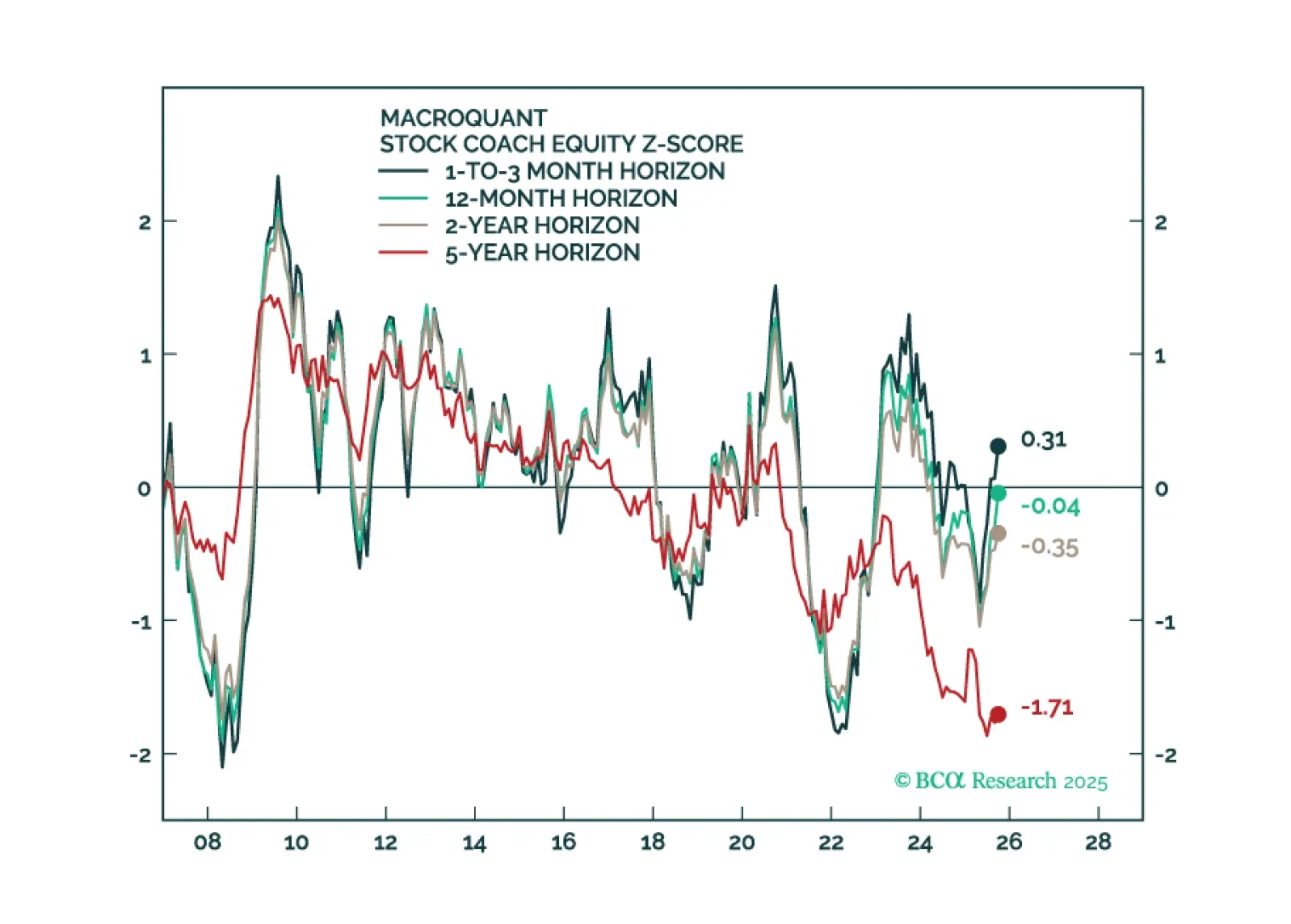

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.