Sectors

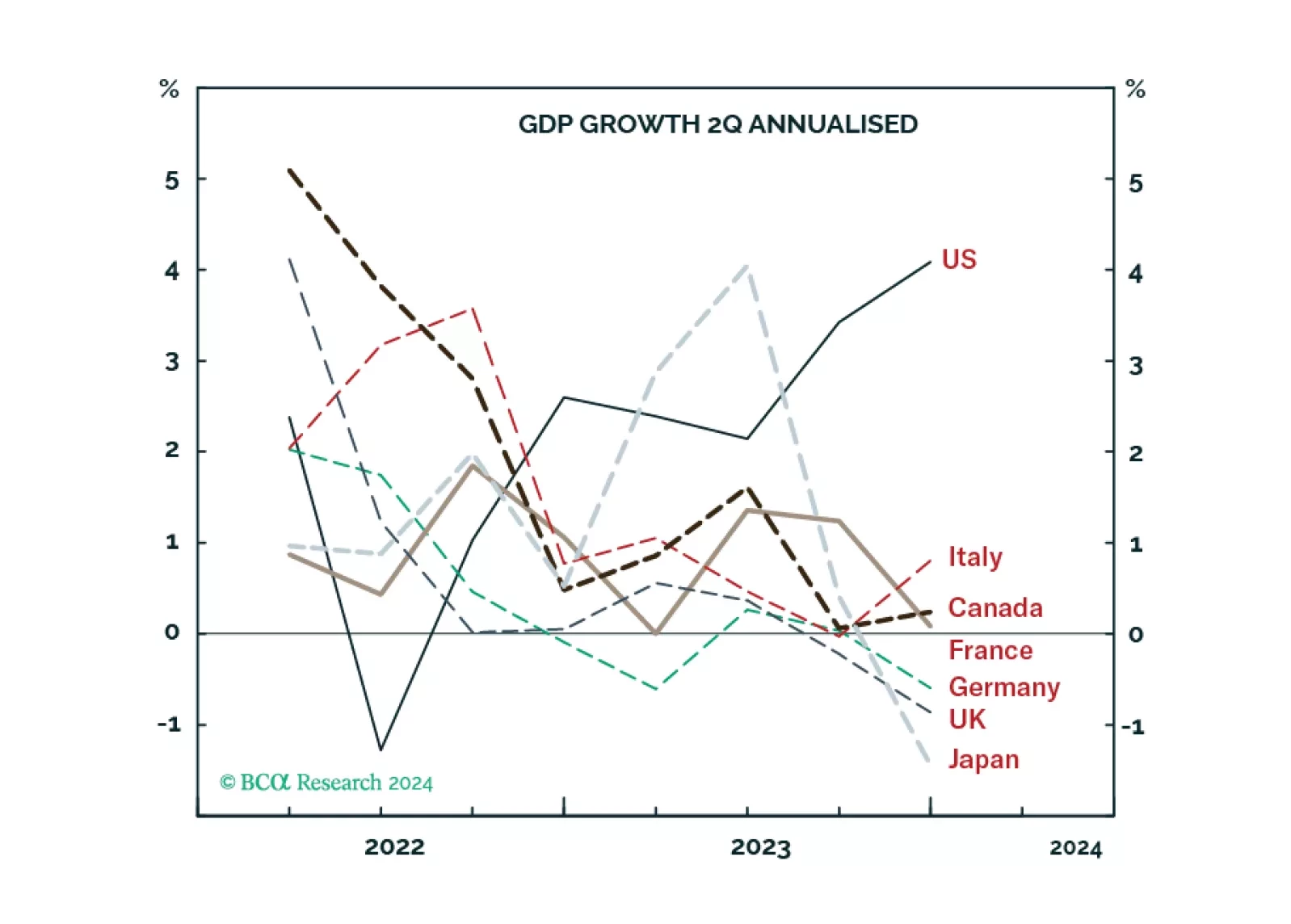

Unlike most advanced economies that are flirting with recession due to weak demand, the ‘inverted’ US economy is motoring along due to strong supply, from a combination of surging labour participation and surging immigration. We go through the implications for stocks, bonds, interest rates, and the dollar. Plus: IXJ, PEP, and MCD are good tactical outperformance candidates.

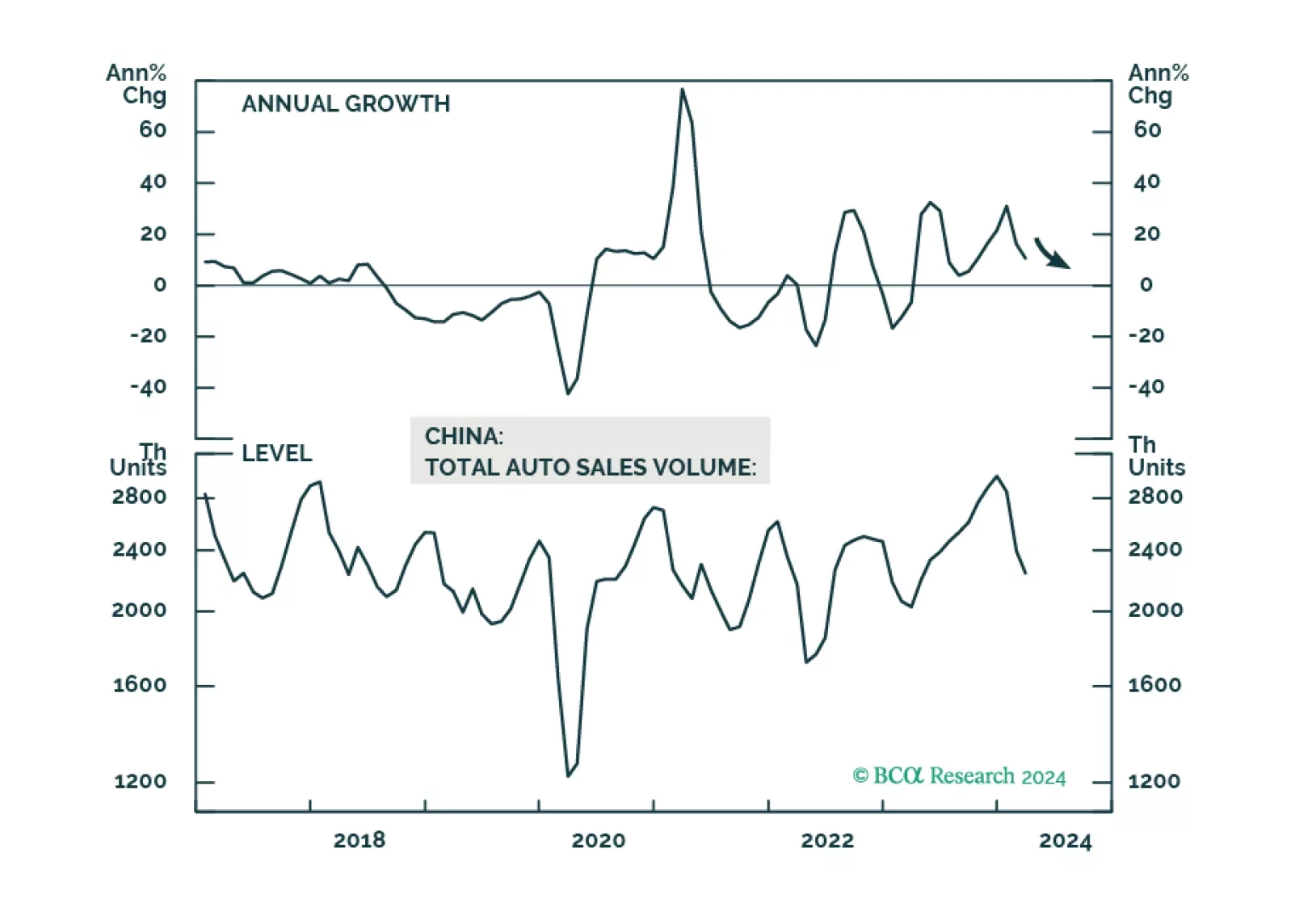

This year’s cash for clunkers program will have only a mildly positive impact on domestic demand for automobiles and home appliances in China. In the meantime, the equipment renewal program will prop up domestic manufacturing moderately as well as help the country reduce its reliance on high-end equipment imports. We recommend continuing to overweight onshore auto stocks relative to the A-Share Index.

The Telecoms industry is highly concentrated, and carriers compete on price and quality of service in a slow growing market. Demand for capex is relentless. The roll out of 5G has disappointed. Recently, capex outlays have slowed, and operating cash flow has rebounded. Further, Telecoms is a quintessential defensive industry that will outperform during a market pullback.

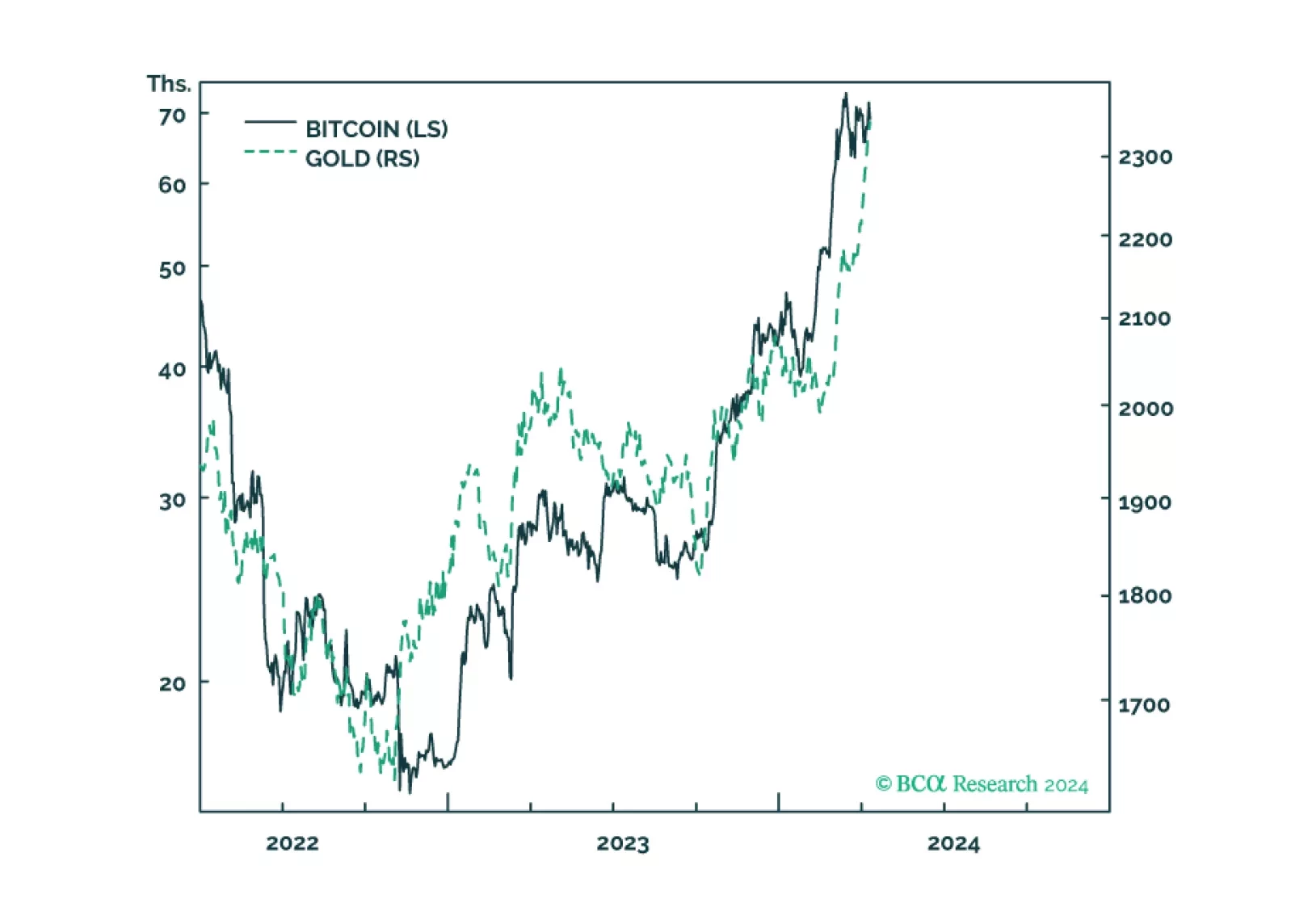

Gold and bitcoin are conceptually joined at the hip because the value of both comes from their ‘non-confiscatability’ by inflation, by bank failure, and in the case of bitcoin, by state expropriation. The sharp recent rallies in both gold and bitcoin reflect that the market has suddenly upped the value of non-confiscatability, and a plausible explanation is that recent US inflation data show that the journey to sustained 2 percent inflation has stalled, raising the risk that the Fed might balk at finishing the journey. Plus: JPM, CL, and USD/CHF are tactical reversal candidates.

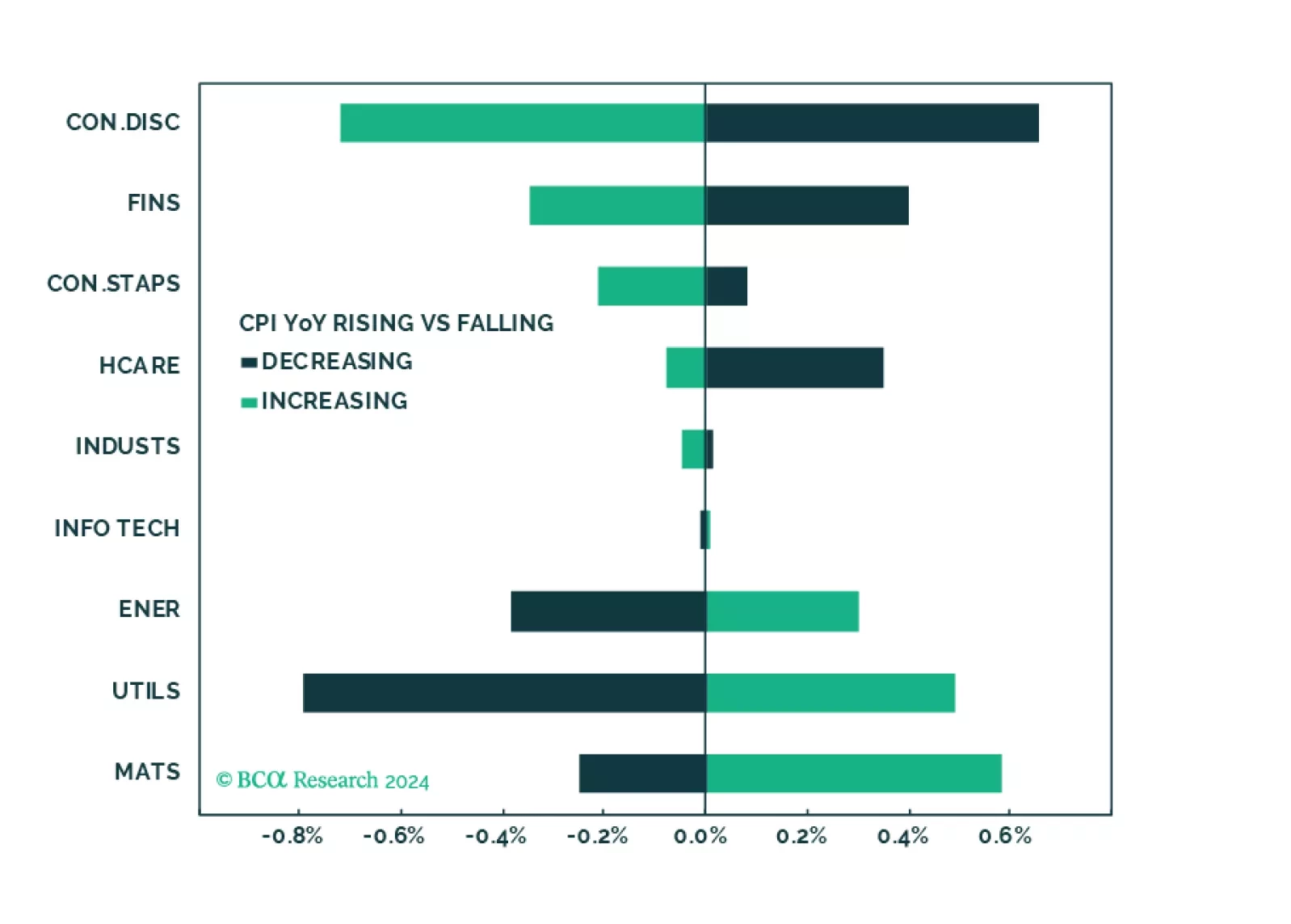

Fears of a hard landing are abating as growth has been surprising to the upside. New worries are emerging, such as the trajectory of disinflation, and the pace and timing of rate cuts. In this environment, it is important to build a resilient all-weather portfolio, which protects against a correction, rising rates, or stubborn inflation but also has exposure to the AI theme.