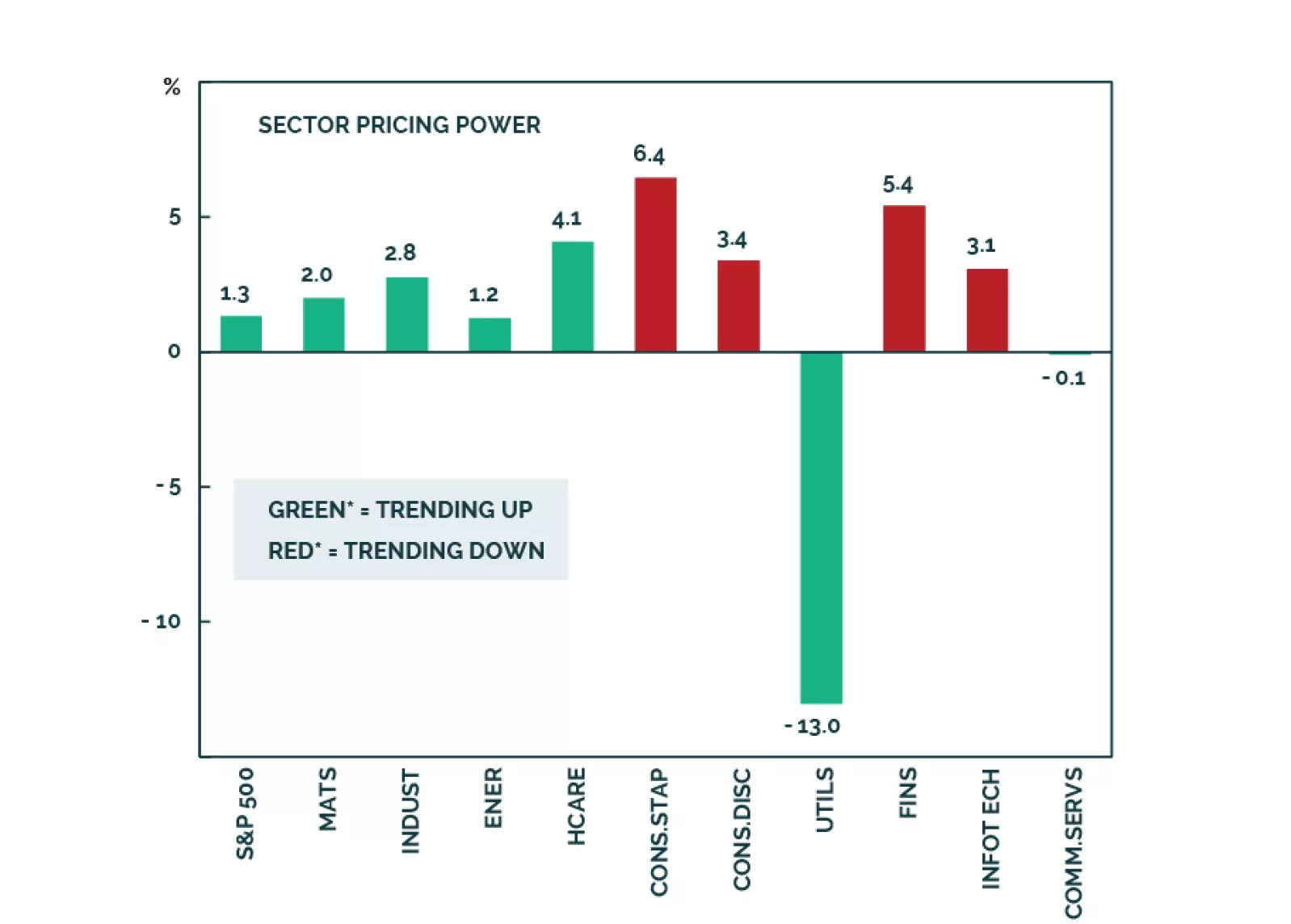

Sectors

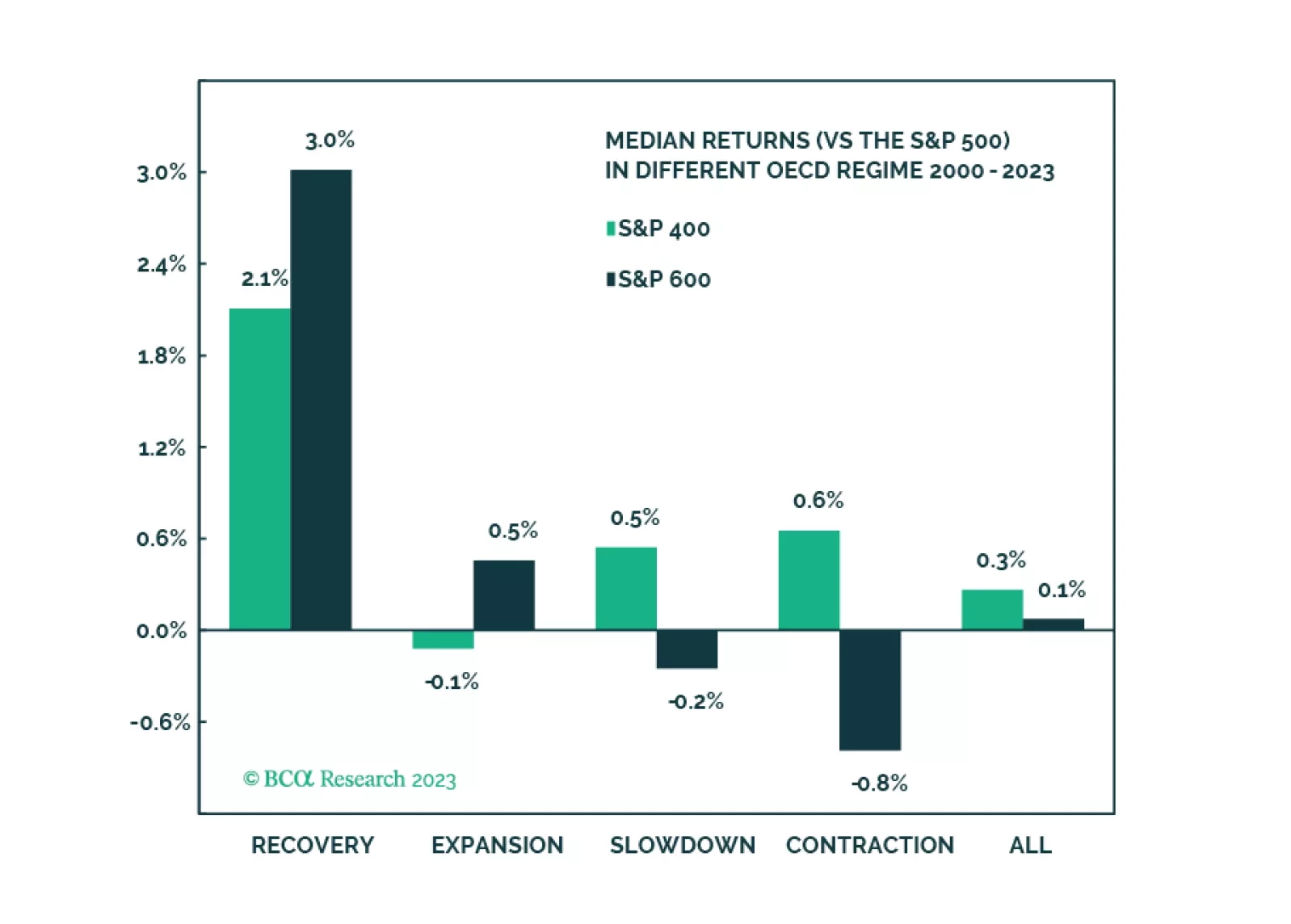

Mid-caps are the best of both worlds and are an excellent strategic overweight thanks to their size premium, but also better financial quality and higher dividend yield than Small. We are bullish on Mid near term and believe that this may be a great trade. We will initiate a position in the S&P 400 as a tactical overweight but will monitor it very closely.

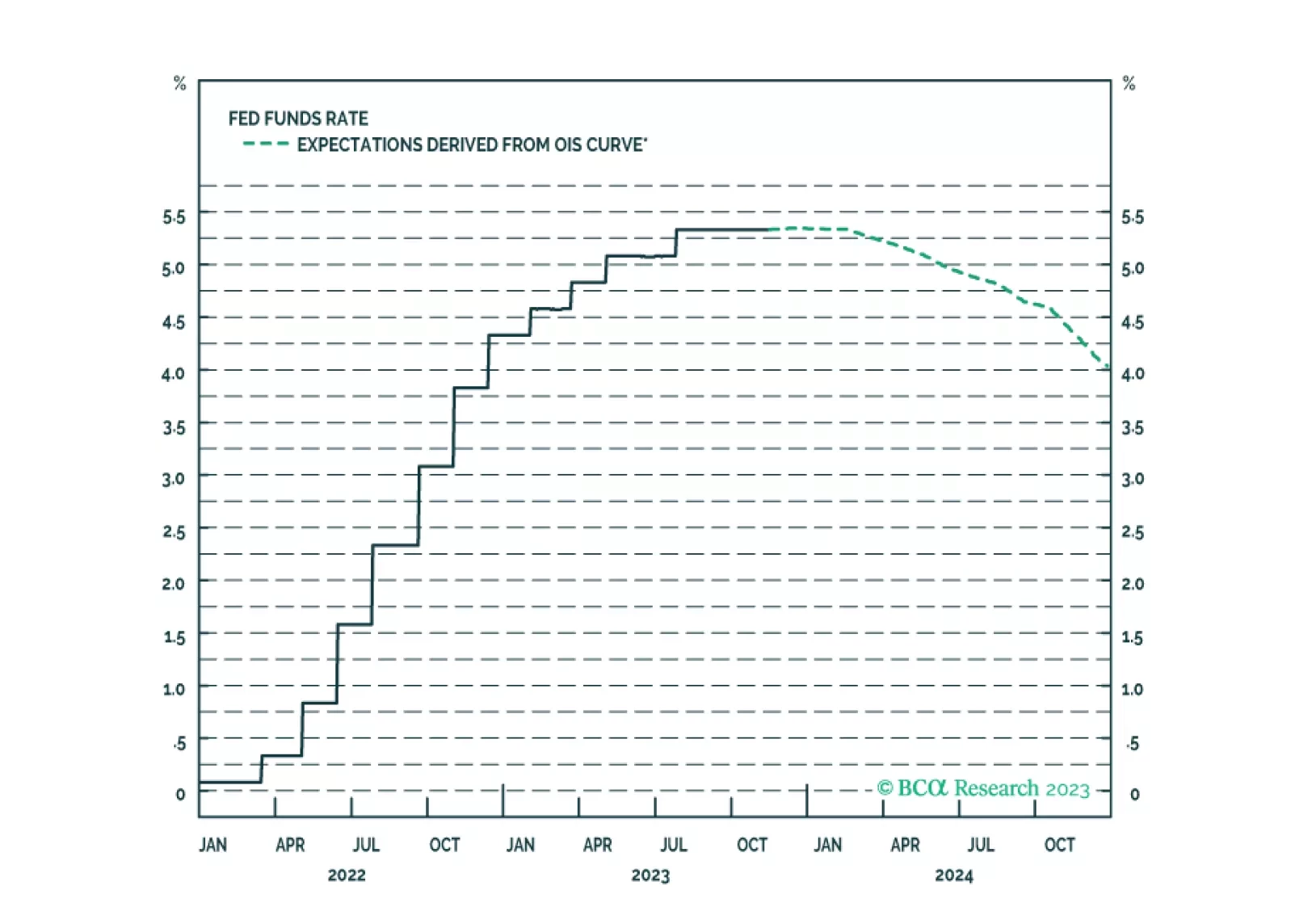

The soft-landing narrative has gotten nowhere at BCA but appears to be making some headway with broker-dealers and investors. We are preparing to lean against it once it pushes equity prices a little higher.

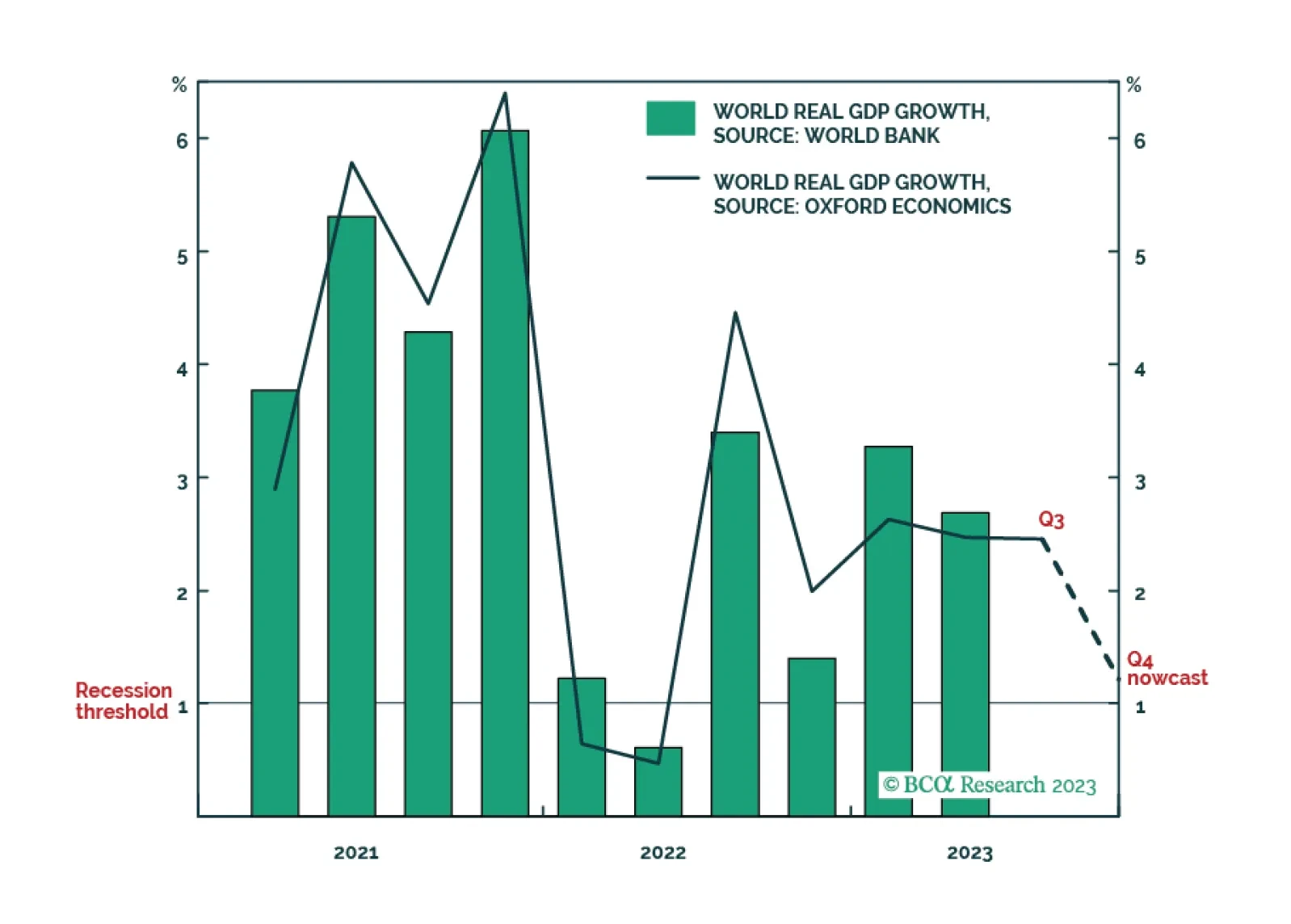

The latest ‘nowcast’ for world economic growth in the fourth quarter has plunged to just 1.2 percent, marking the cusp of another world recession. One important implication is that expectations for oil demand growth and industrial metal demand growth are way too optimistic.

Q3 earnings commentary has been broadly positive, despite intensifying macro headwinds. Going forward, a negative growth outlook and geopolitical risks, are a threat to buoyant earnings expectations. We project that earnings growth for 2024 will move lower than currently projected - a negative for equities. This Santa Claus rally is unlikely to be the start of a new bull market.

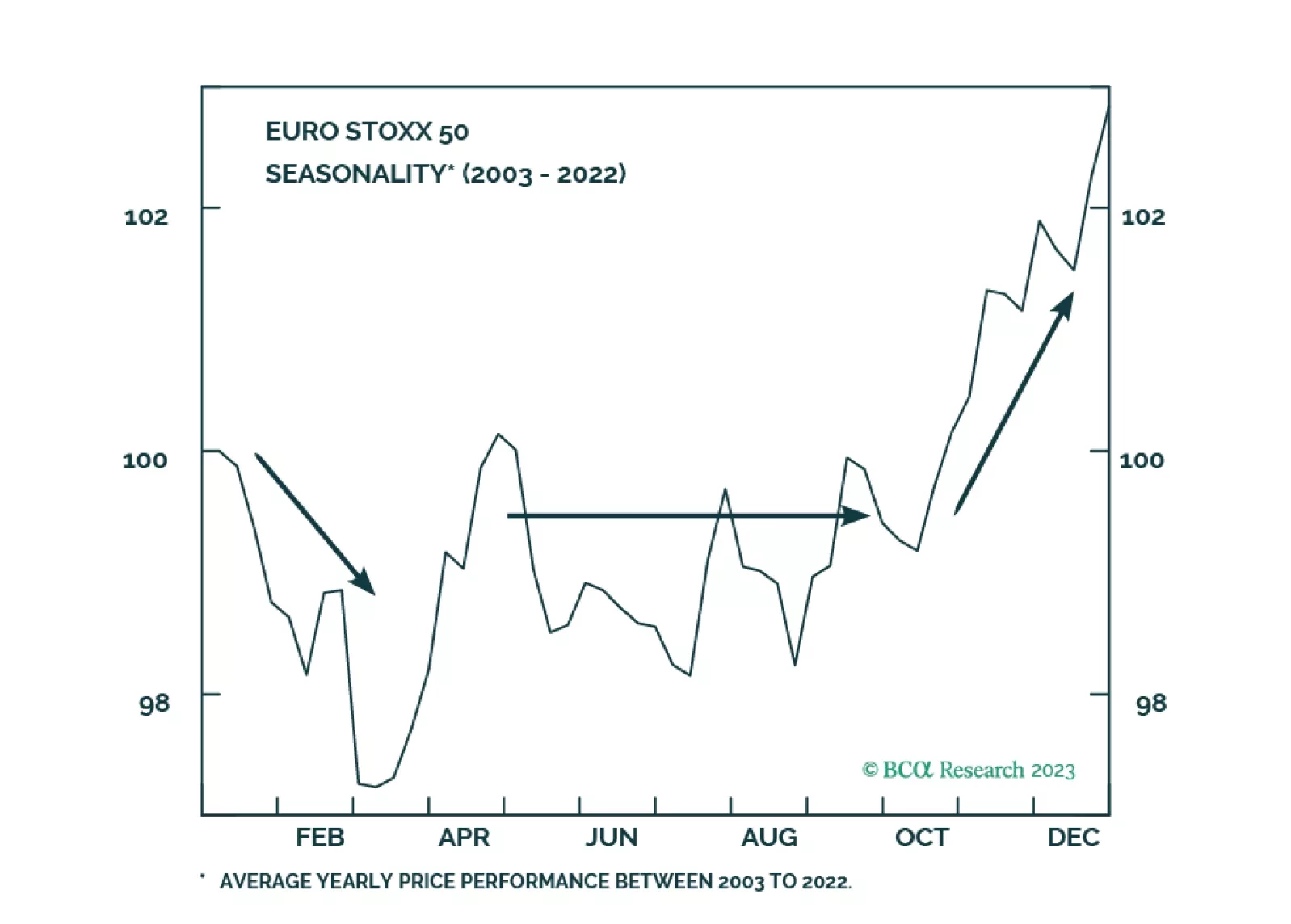

European markets have room to rebound in the coming weeks, however, a recession looms. What are the lessons from history that investors can use to position themselves under these conditions?

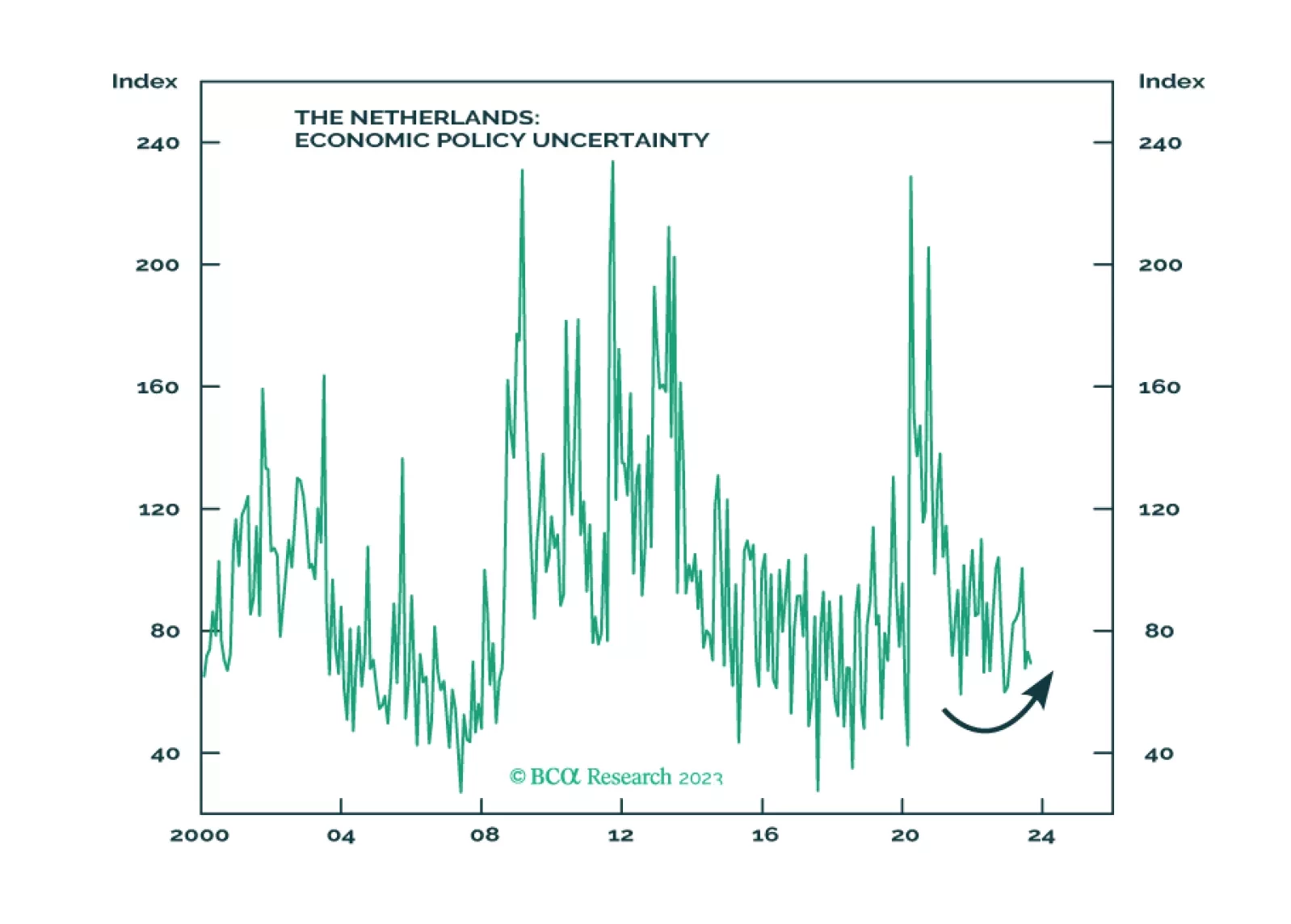

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.

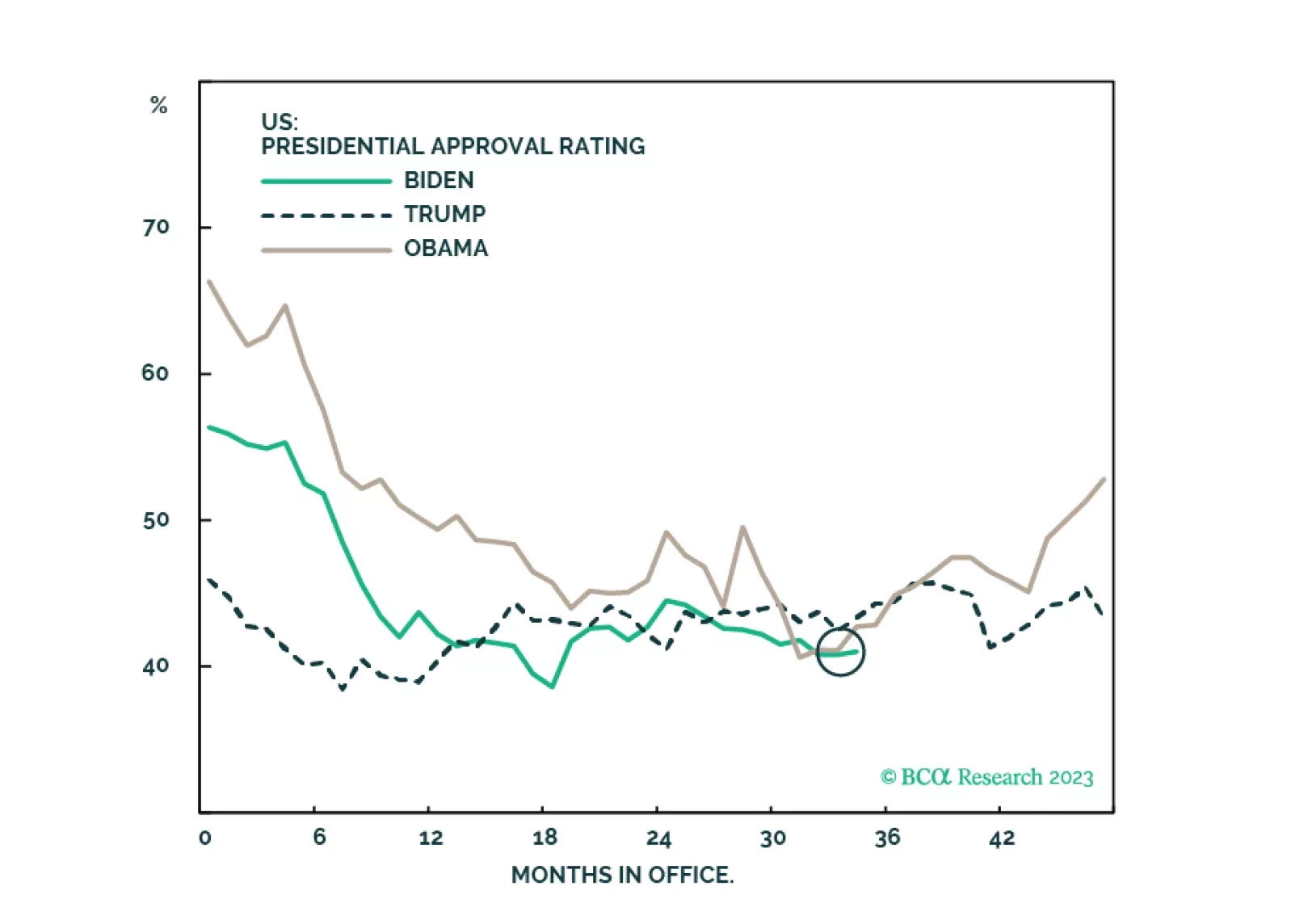

Results from Tuesday’s elections suggest that the Democrats are doing better than what their 2024 polling are showing. While the results are marginally positive for equities, investors should not overrate this off-year election, especially considering the slowing economy and the many foreign challenges facing the US.

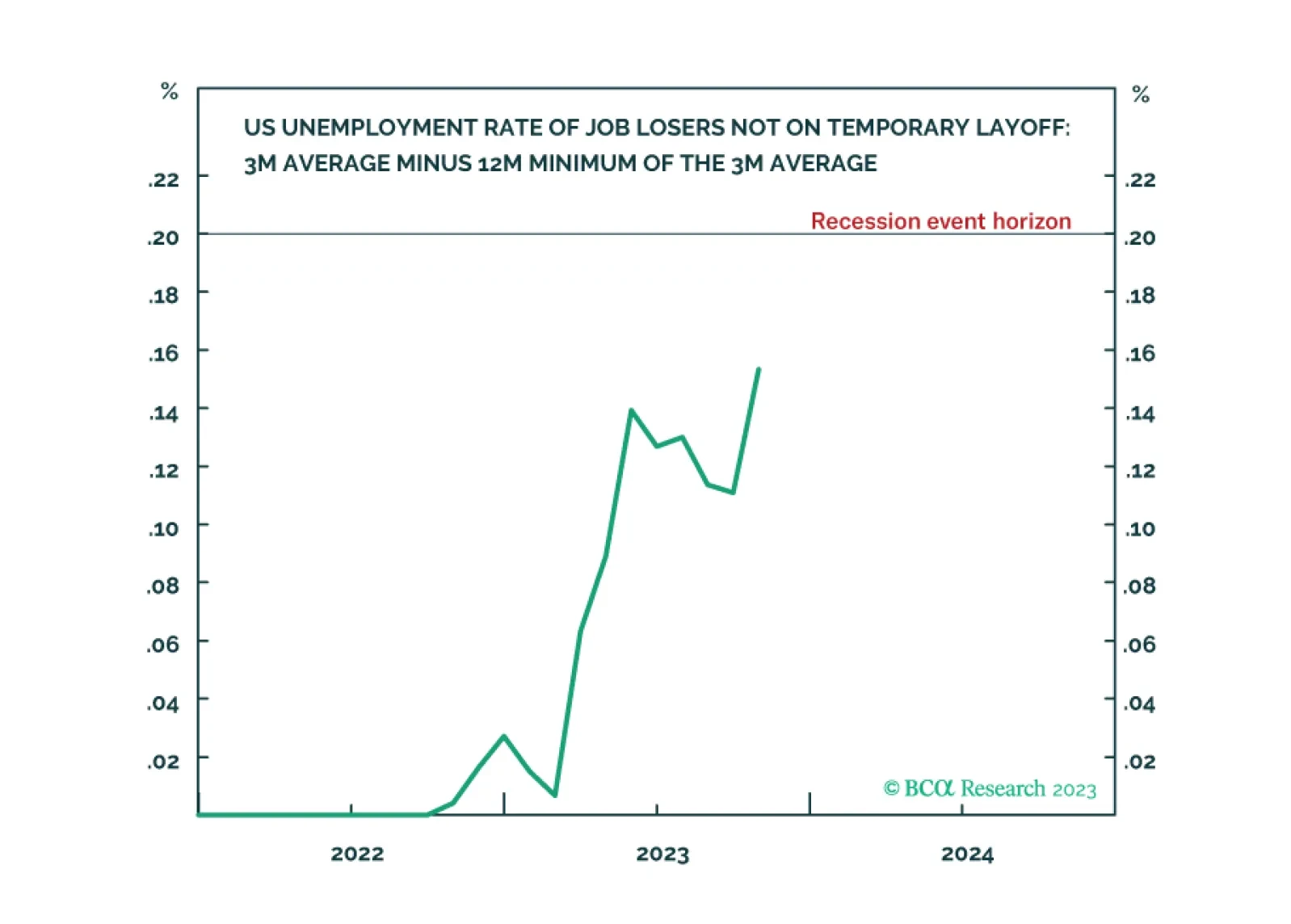

Following the October US jobs data, the ‘Joshi rule’ real-time US recession indicator increased from 0.11 to 0.15, meaning that it is fast approaching its event horizon of 0.20. We go through the investment implications. We also highlight a new long-term recommendation. Plus, the Norwegian krone is close to a potential rebound.