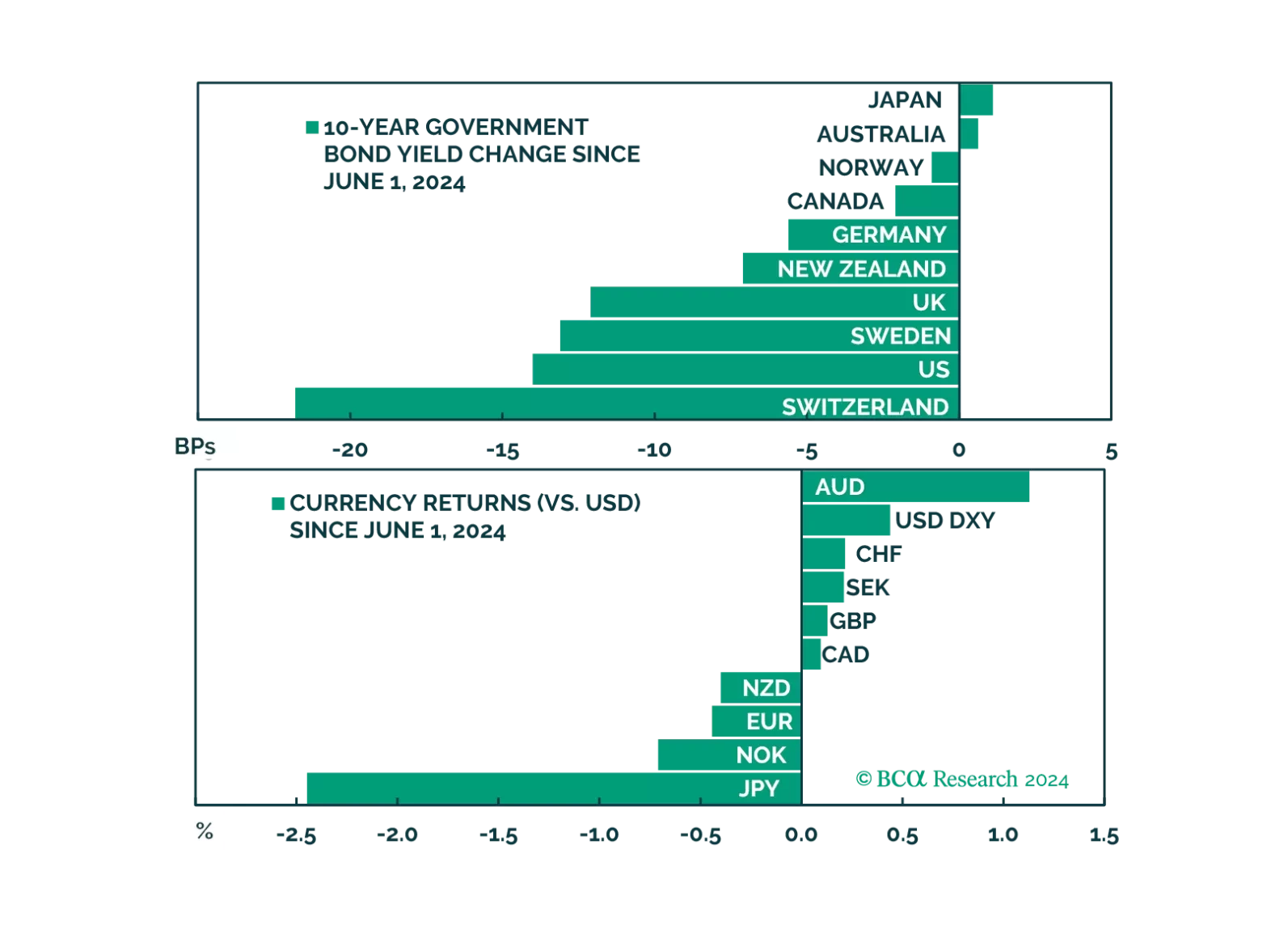

US Dollar

The conventional wisdom is wrong: Trump is not going to substantially cut taxes once in office; he is going to raise taxes by jacking up tariffs. To the extent that this dampens economic activity, it is bad news for stocks but good news for bonds.

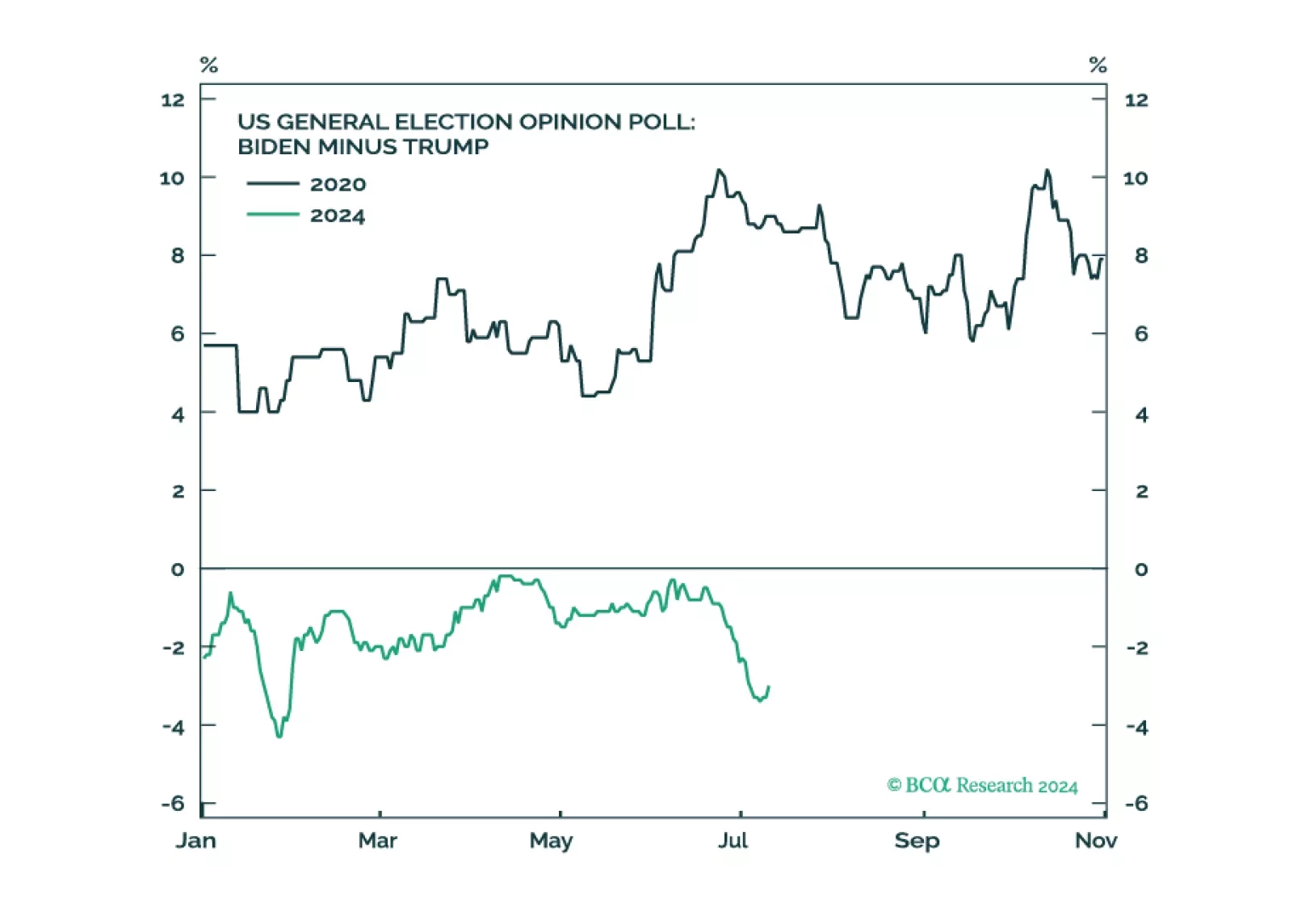

In this week's report, we review the impact of political developments, as well as incoming fundamental data, on our positioning.

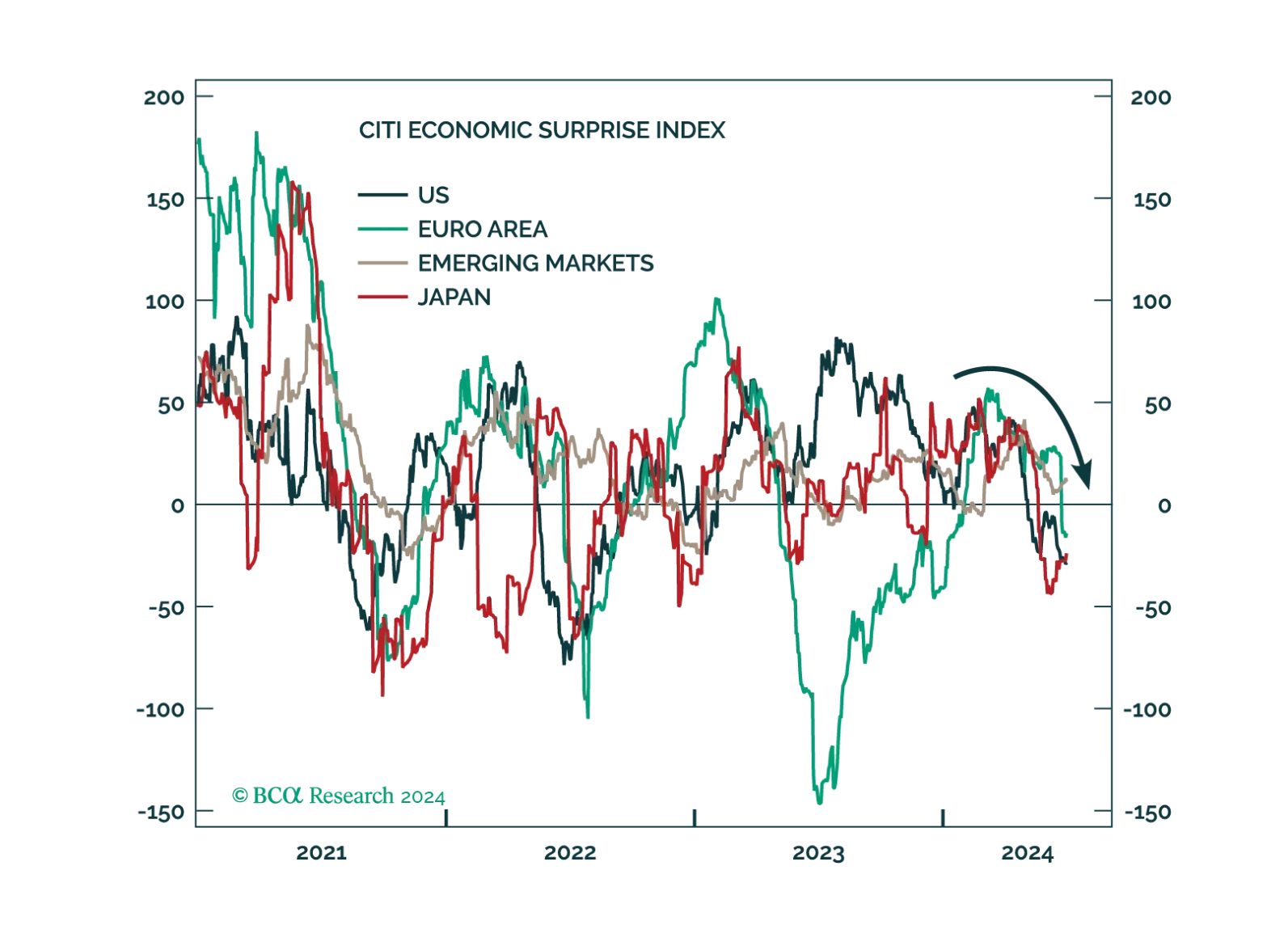

Concerns about the global economy have shifted from sticky inflation to faltering growth. Tight monetary policy is finally starting to bite. We suggest increasing portfolio defensiveness.

In this report, we try to gauge how long the exceptional performance of the US can last, but from a more nuanced angle – inflows into US assets and the impact on the dollar and bond yields. Our work suggests that investors should not make any huge bets on the dollar today, but should be short over the longer term (3-5 years). Empirical evidence also suggests you want to be long US bonds into any downturn, relative to global-ex-US duration-matched government securities, but that view becomes less certain if the global economy avoids a downturn in the next few months. What is interesting in this report are high some conviction views across currencies, bonds and precious metals.

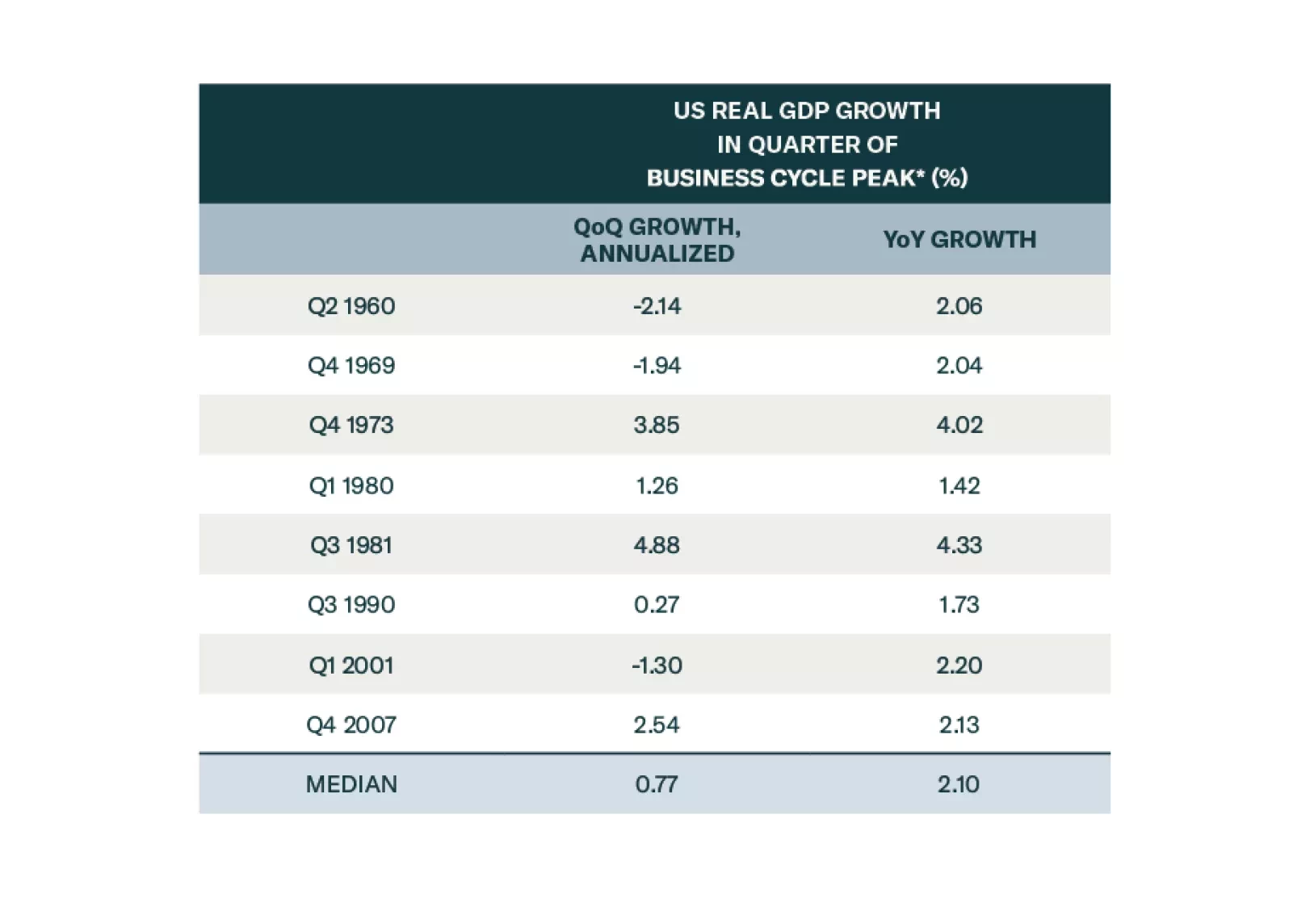

The consensus soft-landing narrative is wrong. The US will fall into a recession in late 2024 or early 2025. We were tactically bullish on stocks most of last year, turned neutral earlier this year, and are going underweight today. We conservatively expect the S&P 500 to drop to 3750 during the coming recession.

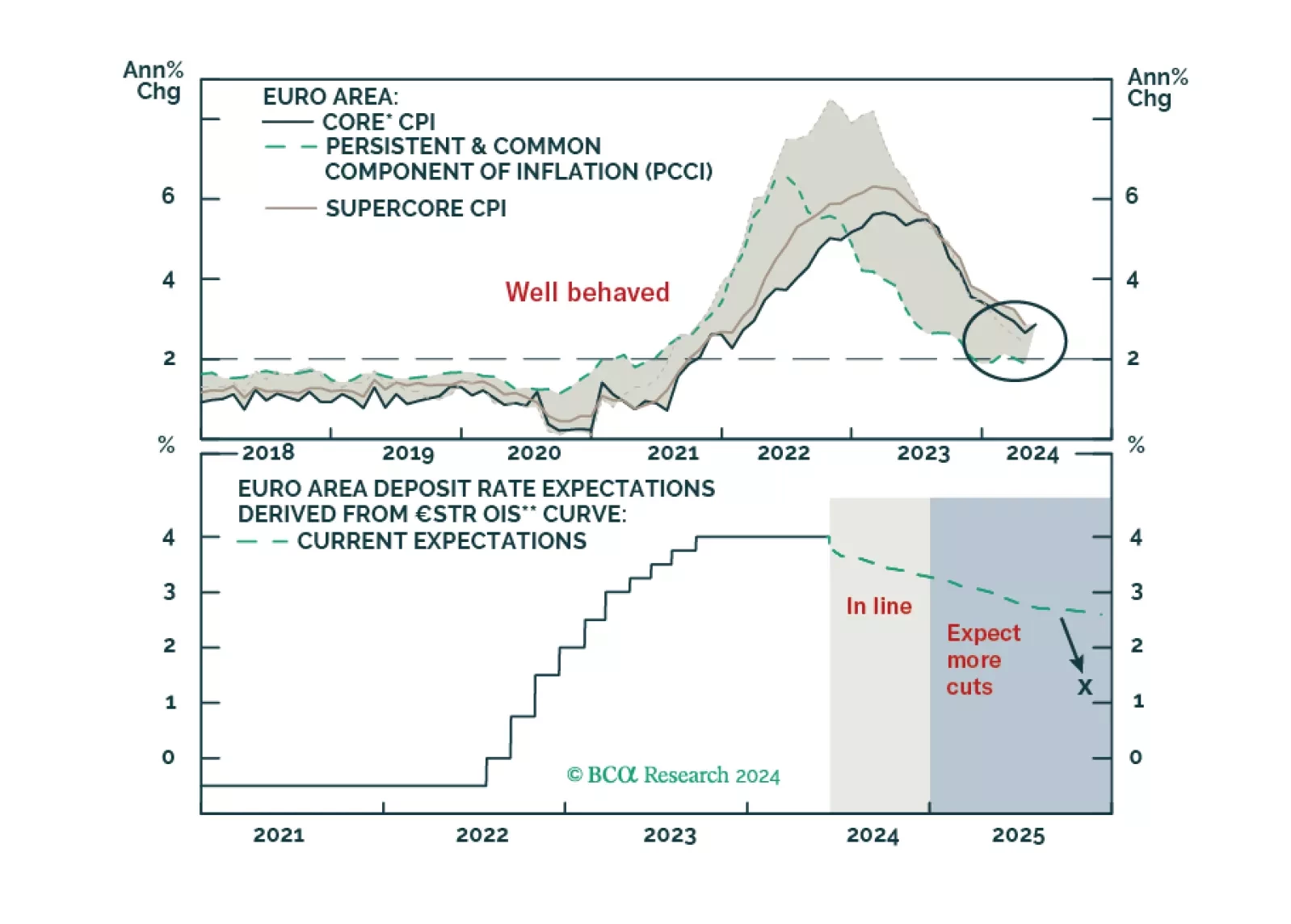

The ECB is now firmly in easing mode, even if it refuses to pre-commit to a specific rate path. What does this data dependency mean for the euro and European yields?

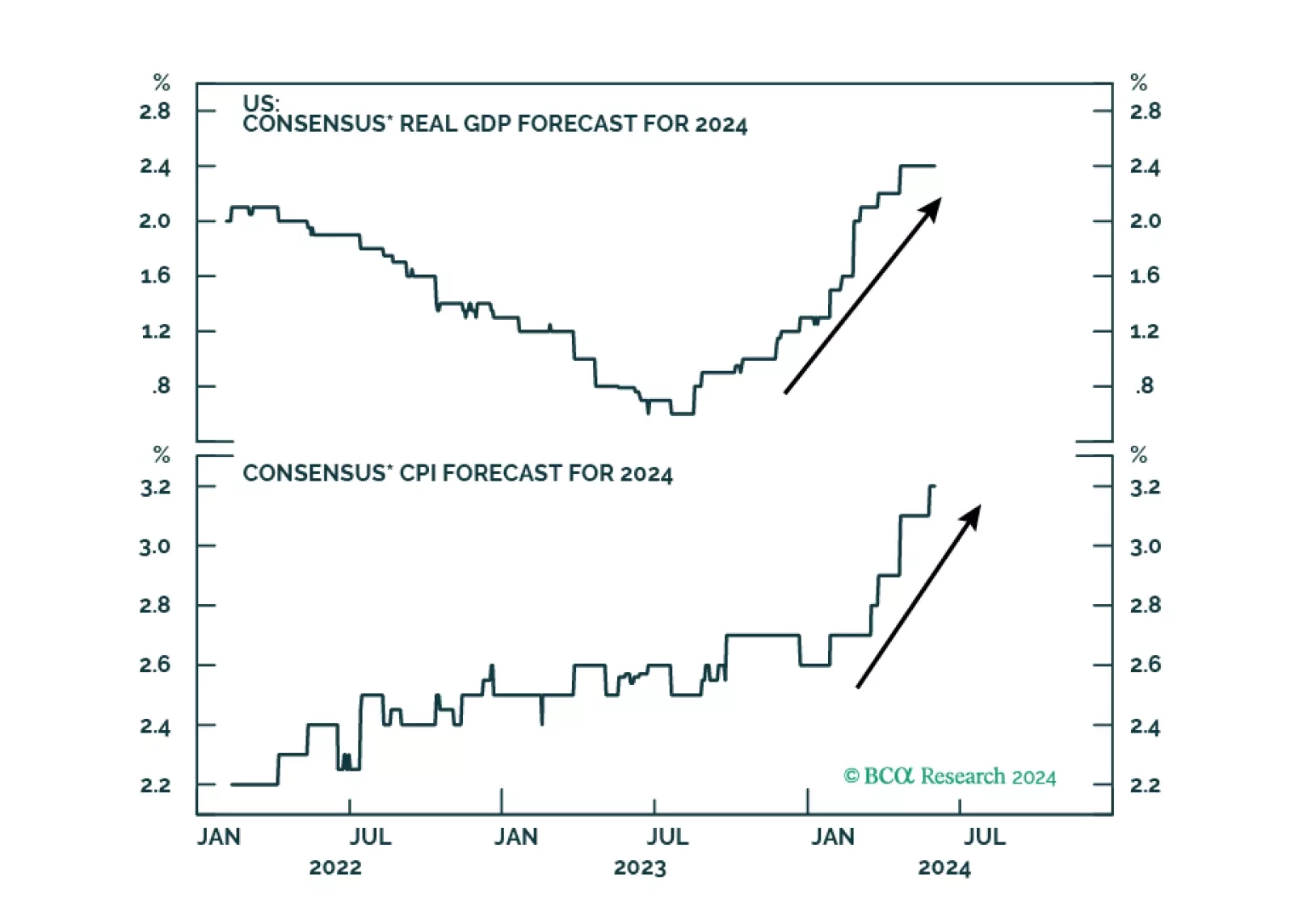

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.