US Election

The US is ripe for a third major political party, but the two-party system will probably prevail in the 2028 election. The macro context will determine whether the US elects a left-wing populist.

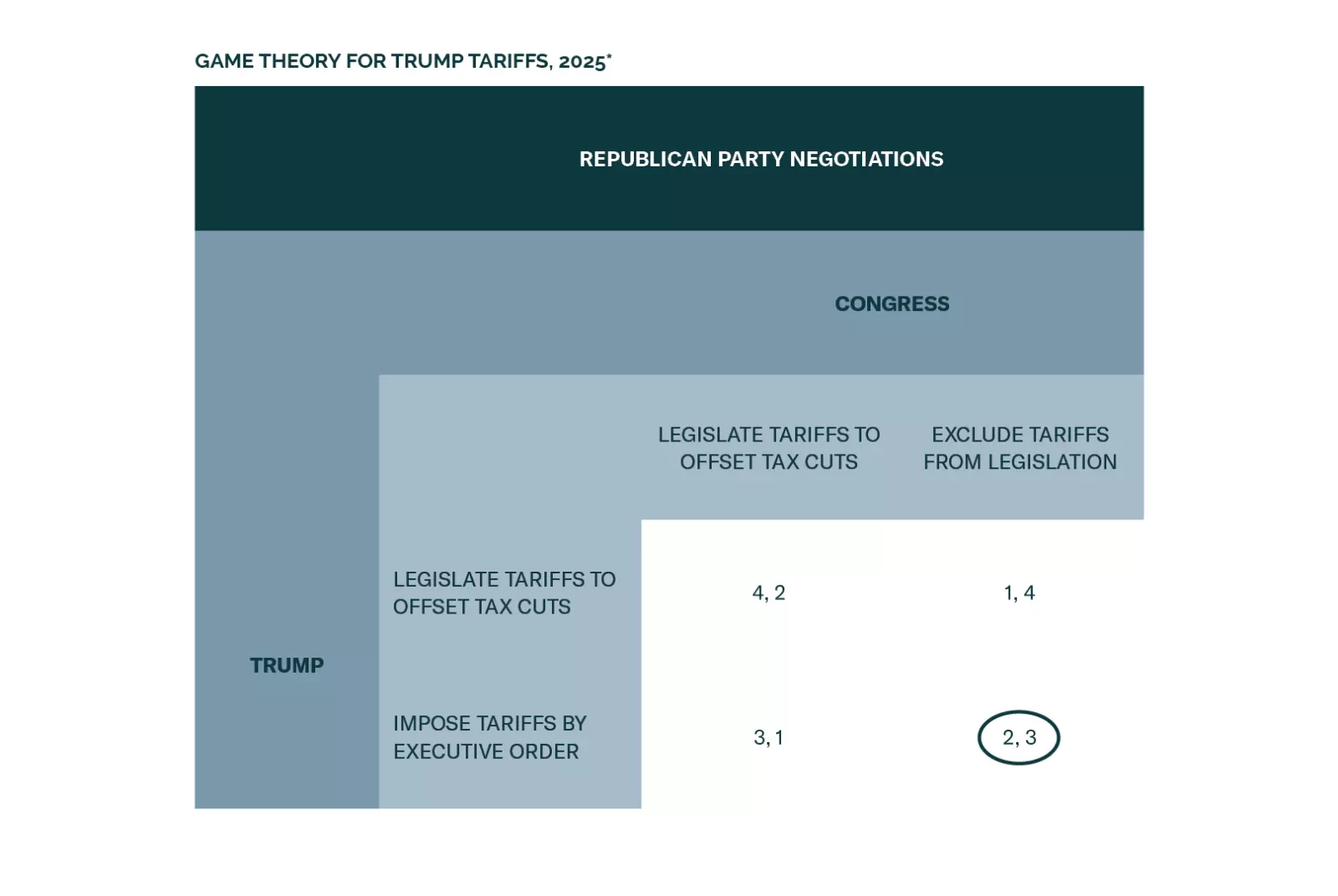

Simple games allow us to model several of the Trump administration’s most disruptive policies in 2025. We find that markets face an increase in volatility as Congress expands the budget, Trump implements tariffs on the world, China retaliates, and Taiwan tensions persist. A ceasefire in Ukraine is a marginally positive outcome for Europe, although it is not a long-term peace treaty.

We were stopped out of our defensive asset allocation recommendations last Thursday, when the S&P 500 closed above 6,100, but our reading of the labor market tea leaves still supports a bearish fundamental view.

President Trump is only the second president to have won, lost, and won again in US history, so today’s inaugural address was unlike any other since Grover Cleveland in 1893.

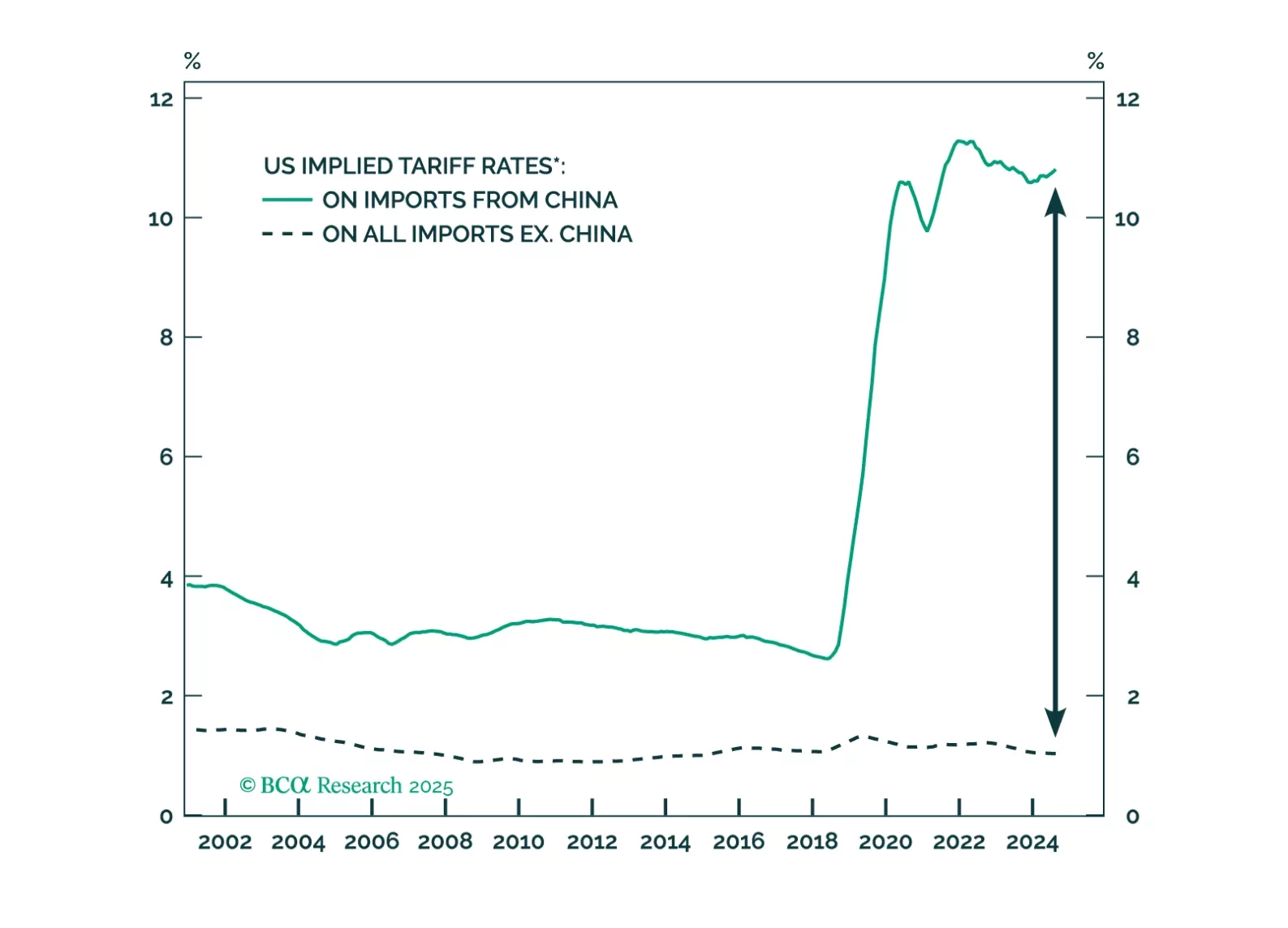

Inauguration Day or shortly thereafter will see either a global tariff of 10% or targeted but substantial tariffs on China, Mexico, and Canada. Treasury yields will rise on tax cuts, the dollar will stay strong, yet oil will also continue to rally, causing equity volatility in the near term.

Investors are overstating the positive fiscal impact of the Trump presidency. The bond market will have something to say about the scope for further deficit expansion via tax cuts. As such, the trade after the trade of the Trump 2.0 administration may involve less growth out of the US, not more. In the interim, however, investors should continue to expect higher yields and increased equity volatility. There are plenty of risks ahead, including geopolitics, trade, and uncertainty surrounding fiscal policy.

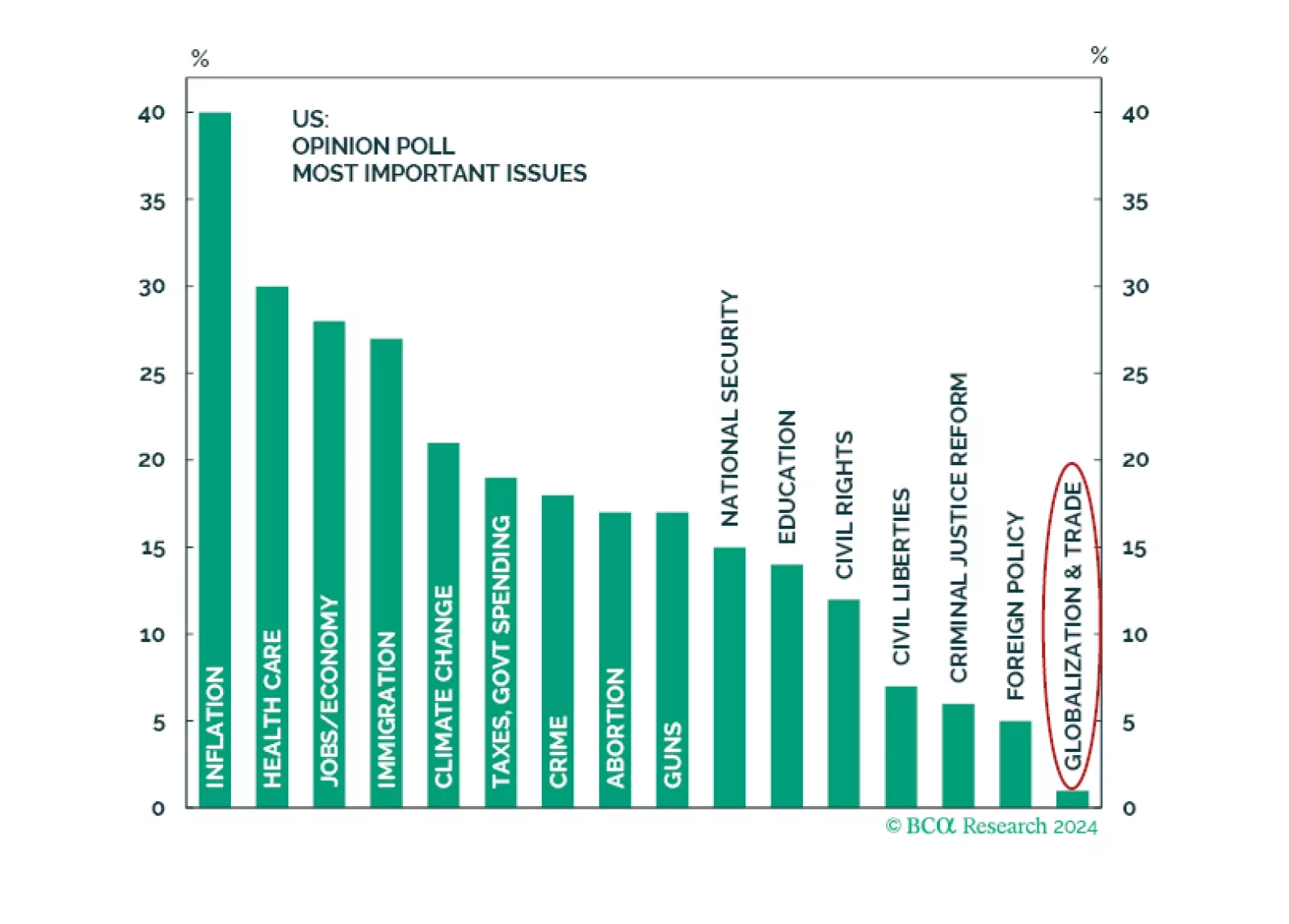

Ultimately, 2024 is not 2016 — a seemingly obvious point, but one with market relevance. In 2016, voters gave Trump a strong mandate for nominal GDP growth. It is not clear if this is the case today. Inflation is the most important issue, least relevant is trade and globalization. As such, Trump’s renewed mandate is for supply side reforms, not more populism and protectionism.

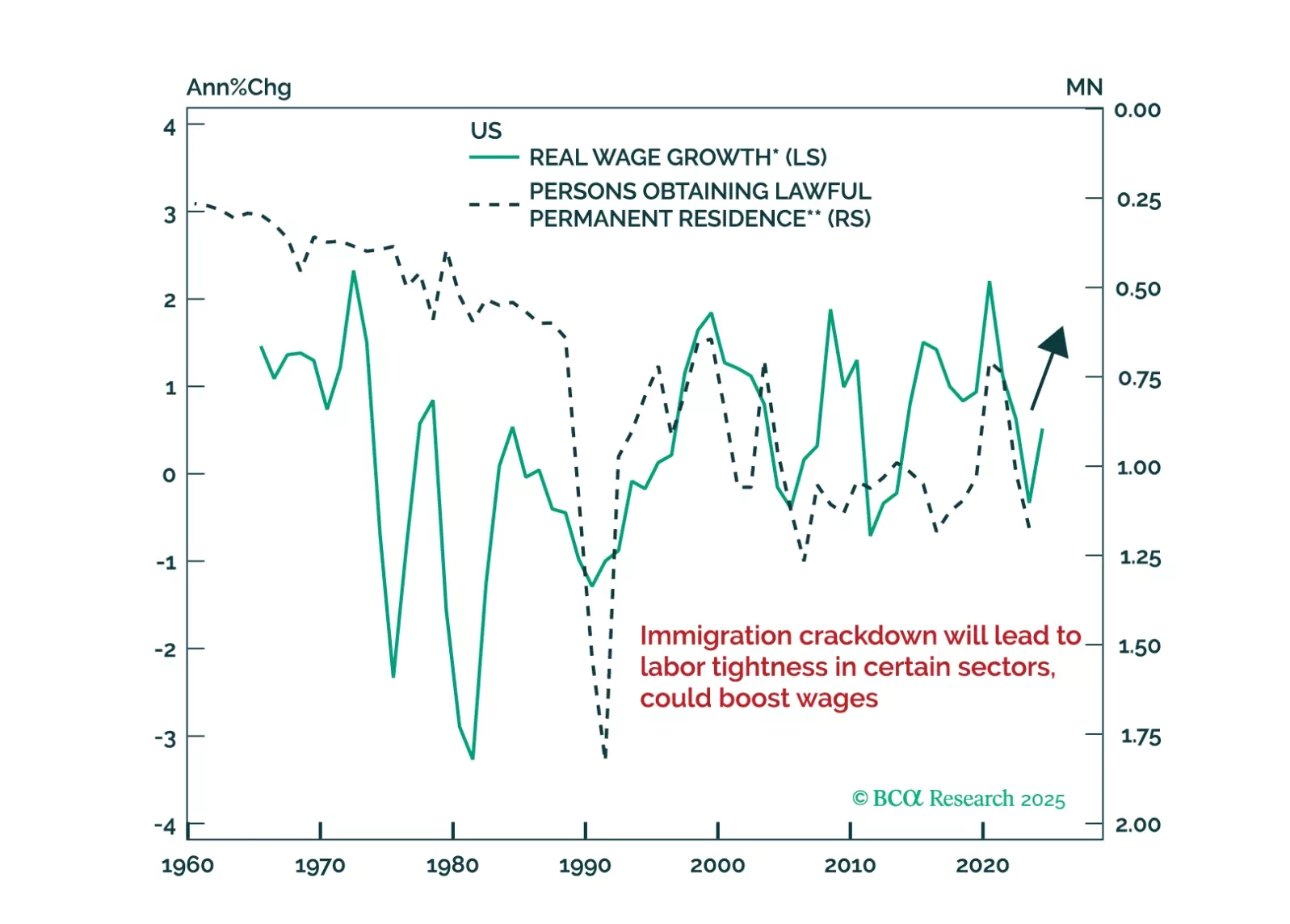

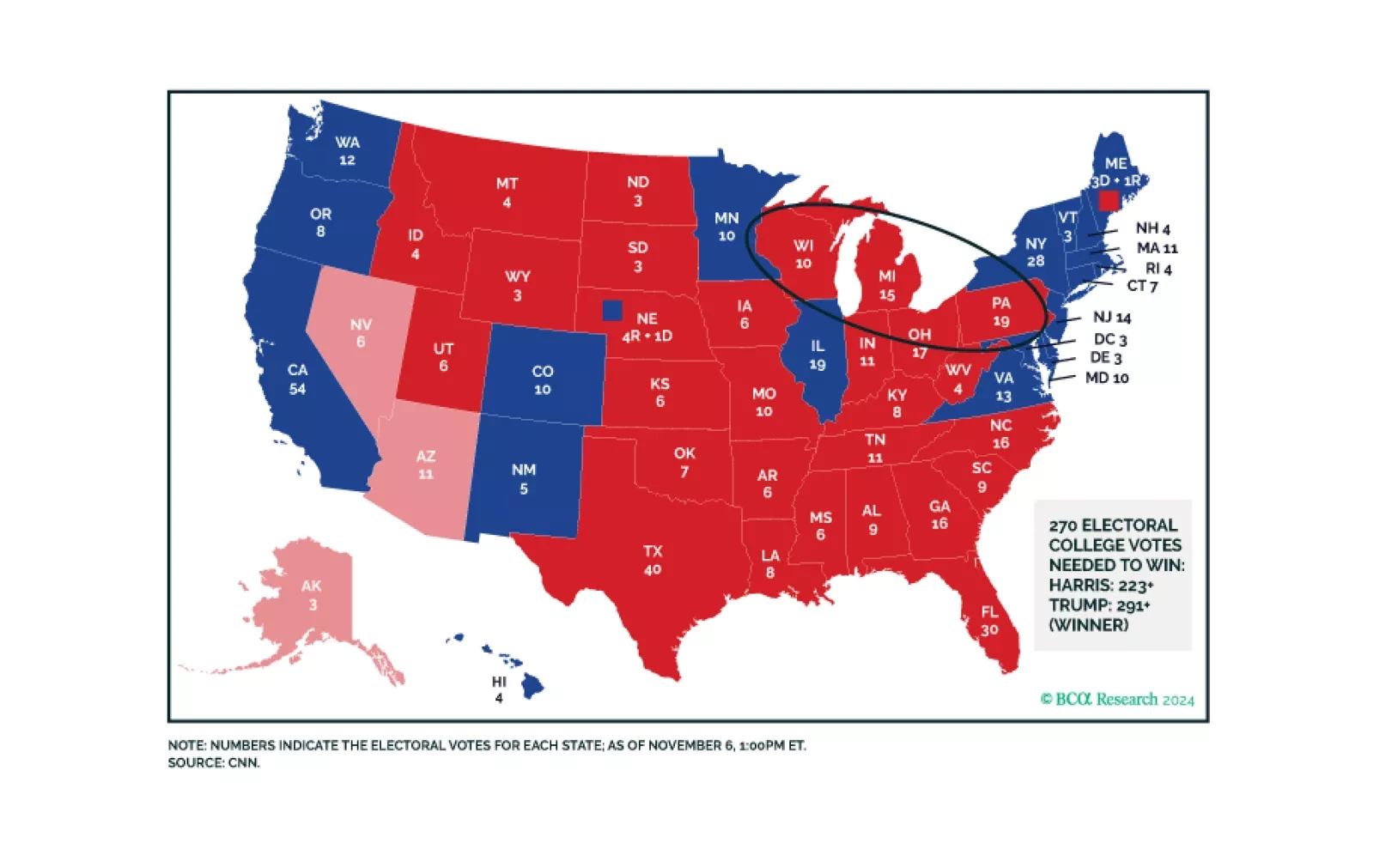

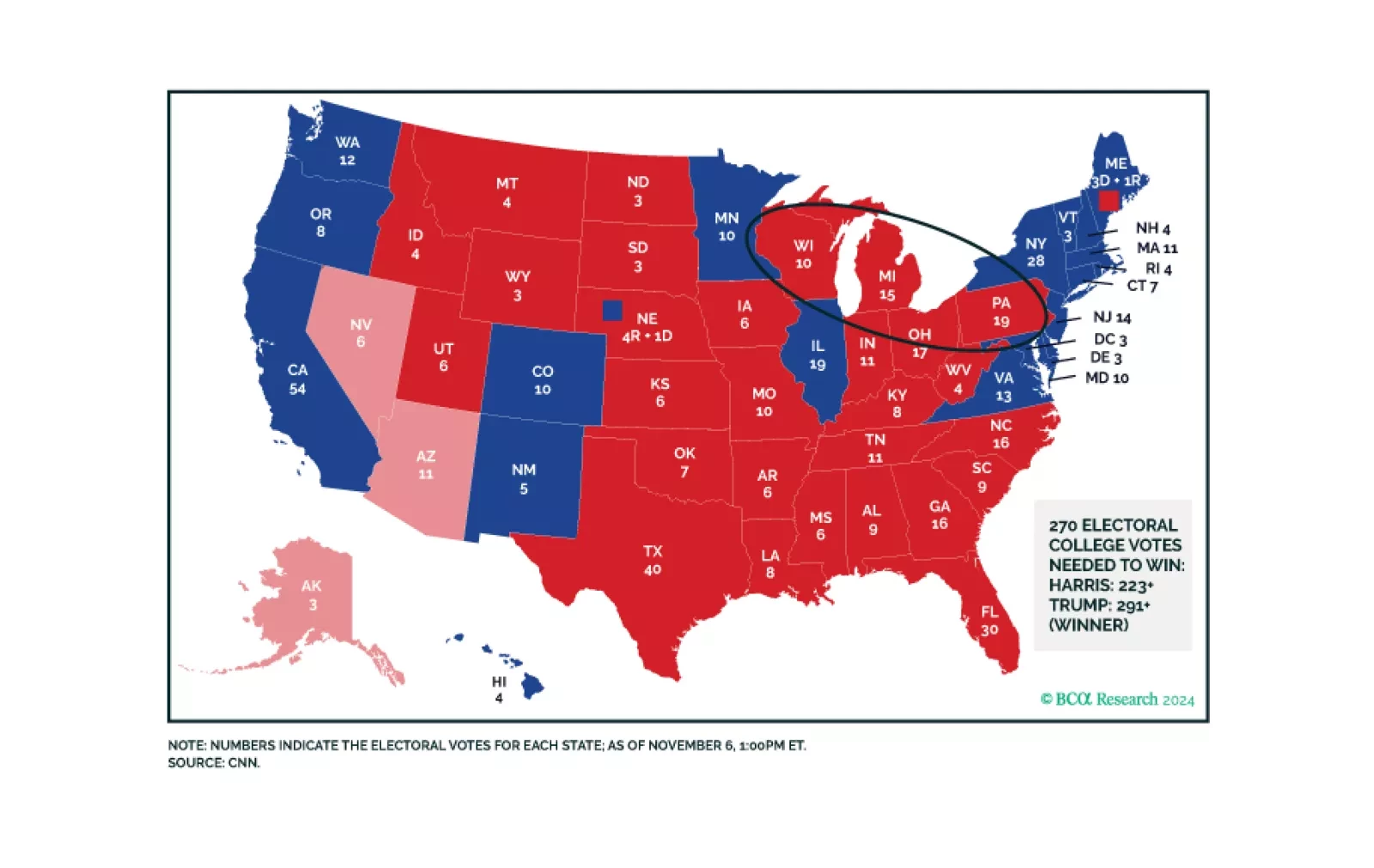

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.

The prospect of a new trade war more than offsets the other pro-business parts of Trump’s agenda. With the labor market already weakening going into the election, we are raising our 12-month US recession probability from 65% to 75%.