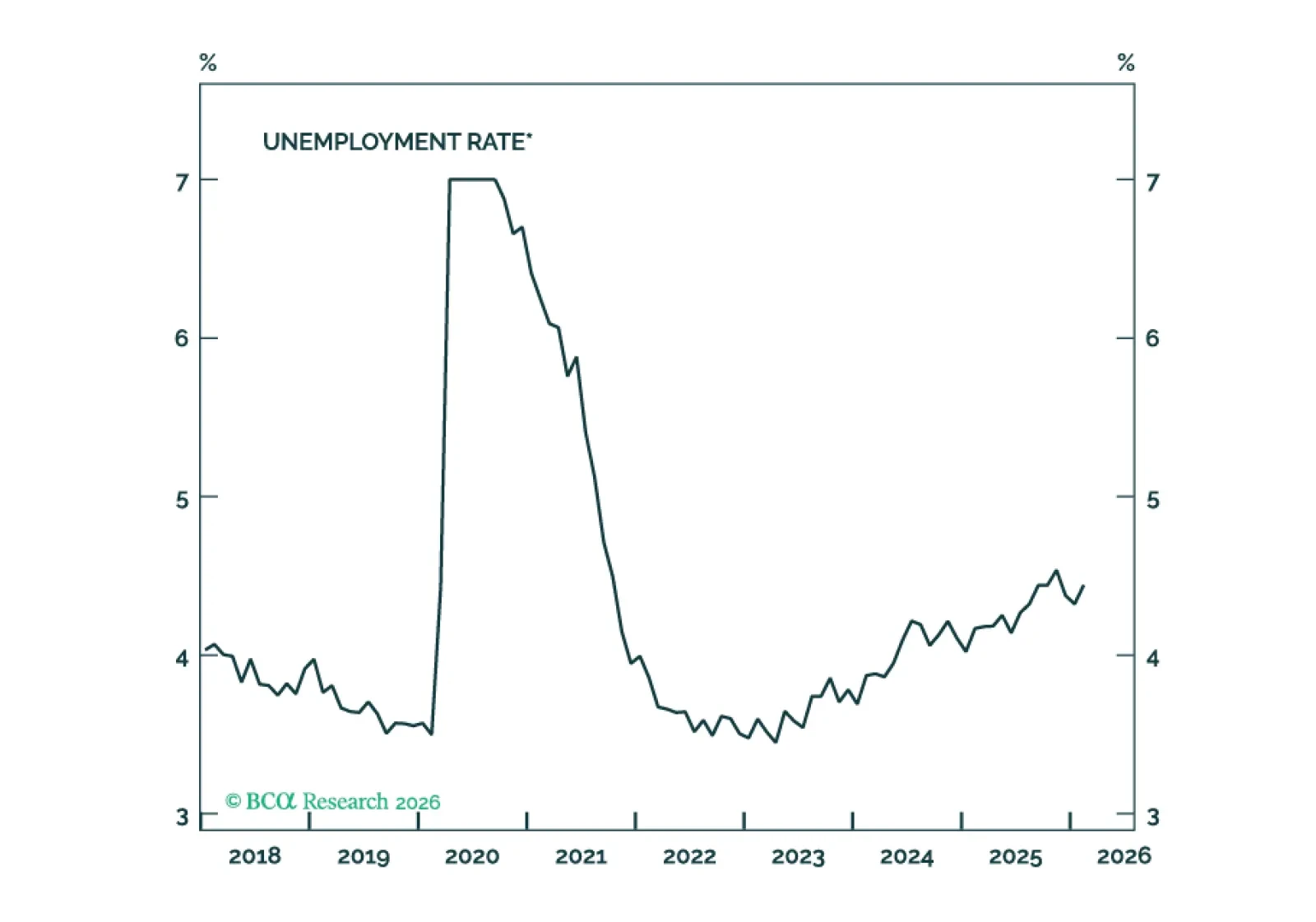

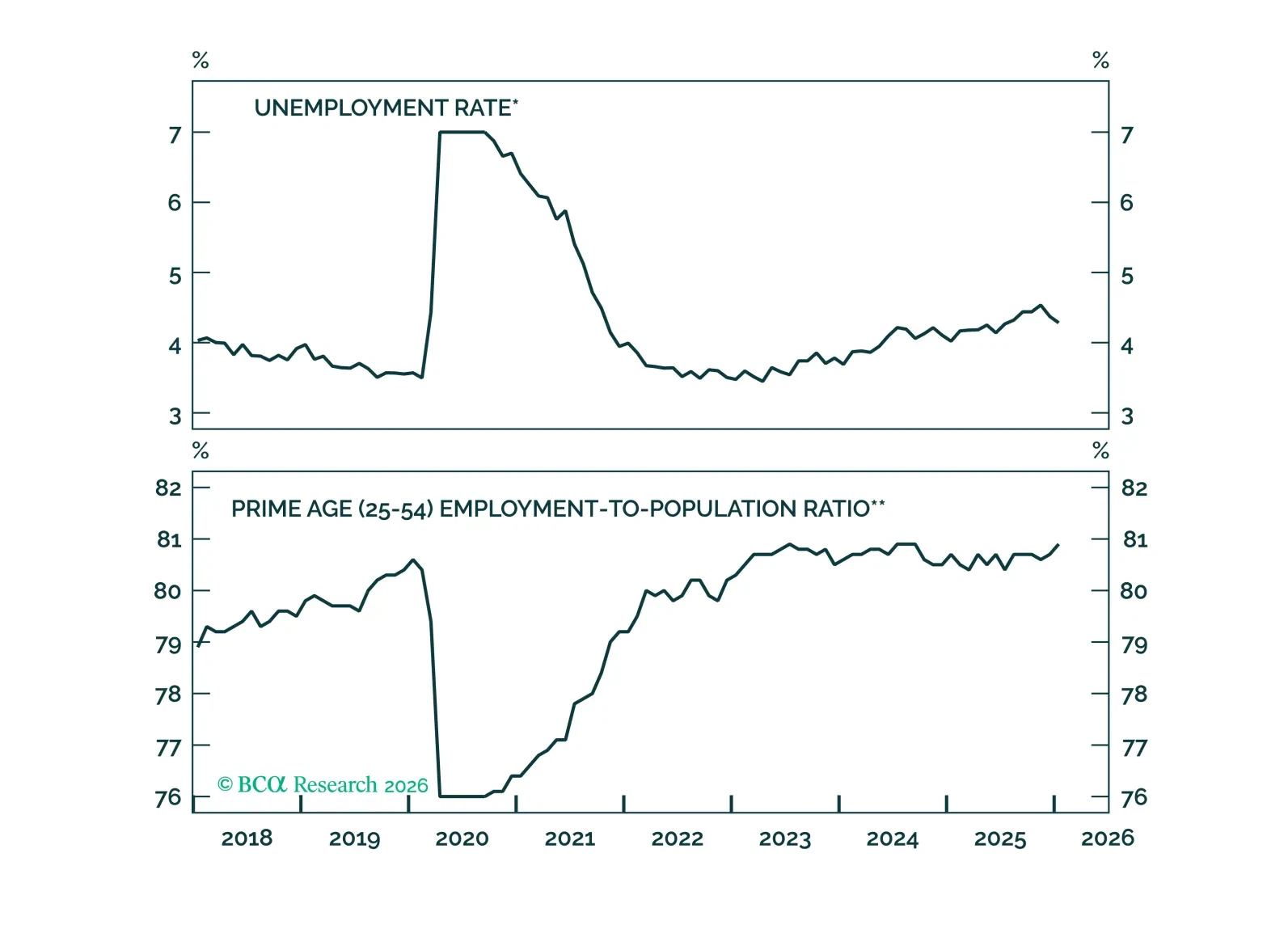

US Labor Market

In Section I, Doug revisits the situation in the Strait of Hormuz and its implications for growth in Europe and the US. In Section II, Jonathan explores whether Kevin Warsh's appointment as Fed Chair signals a return to Greenspan-era, rules-based monetary policy.

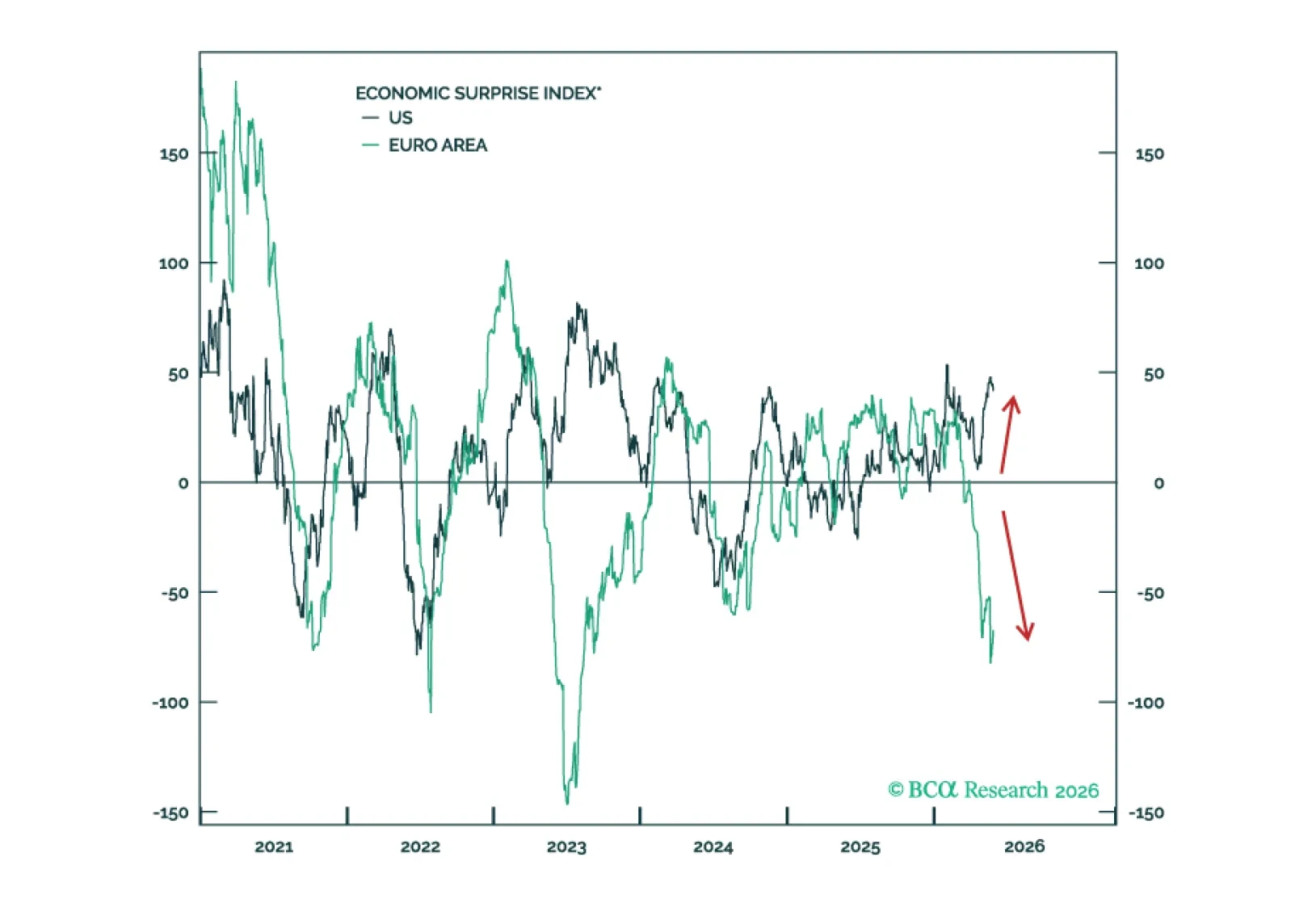

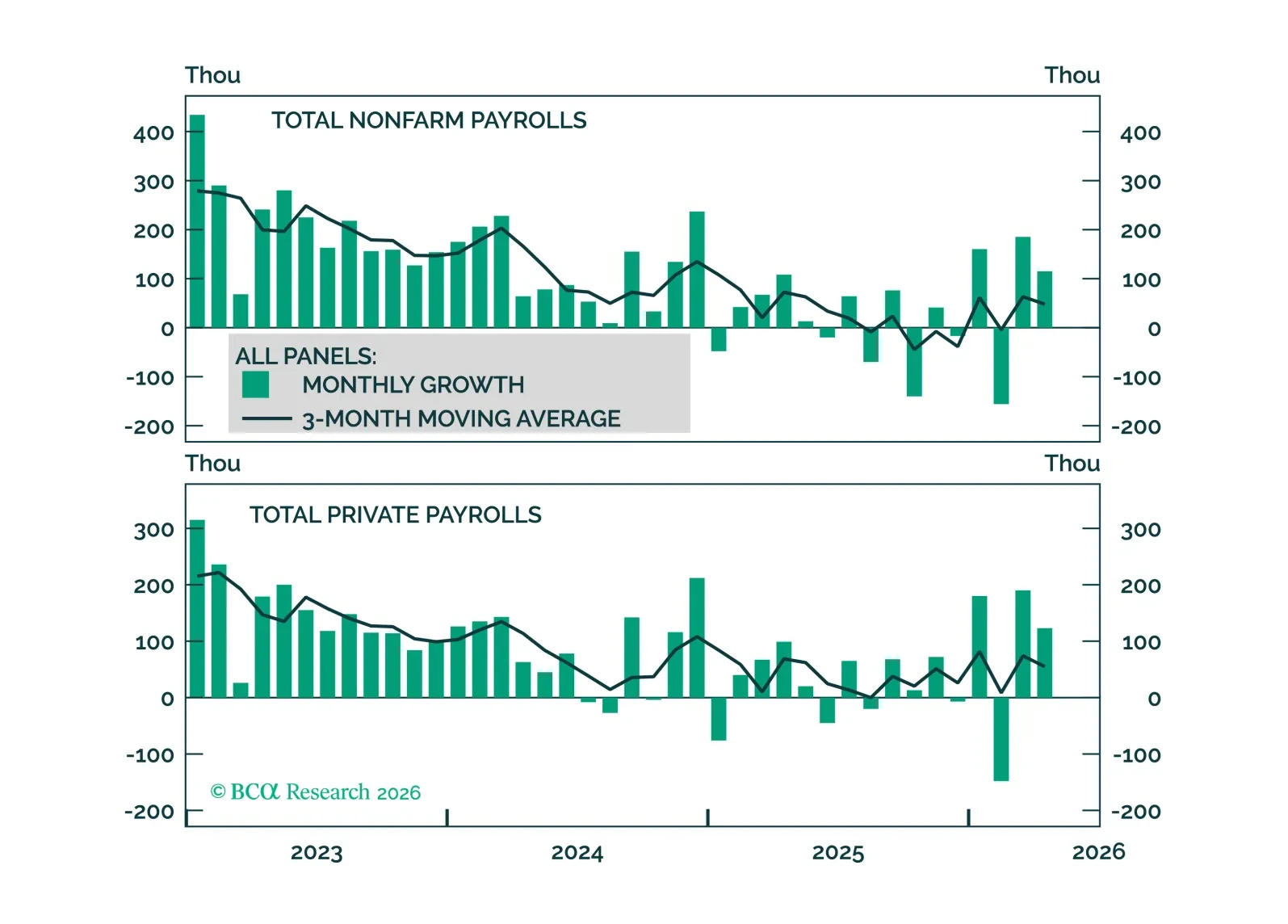

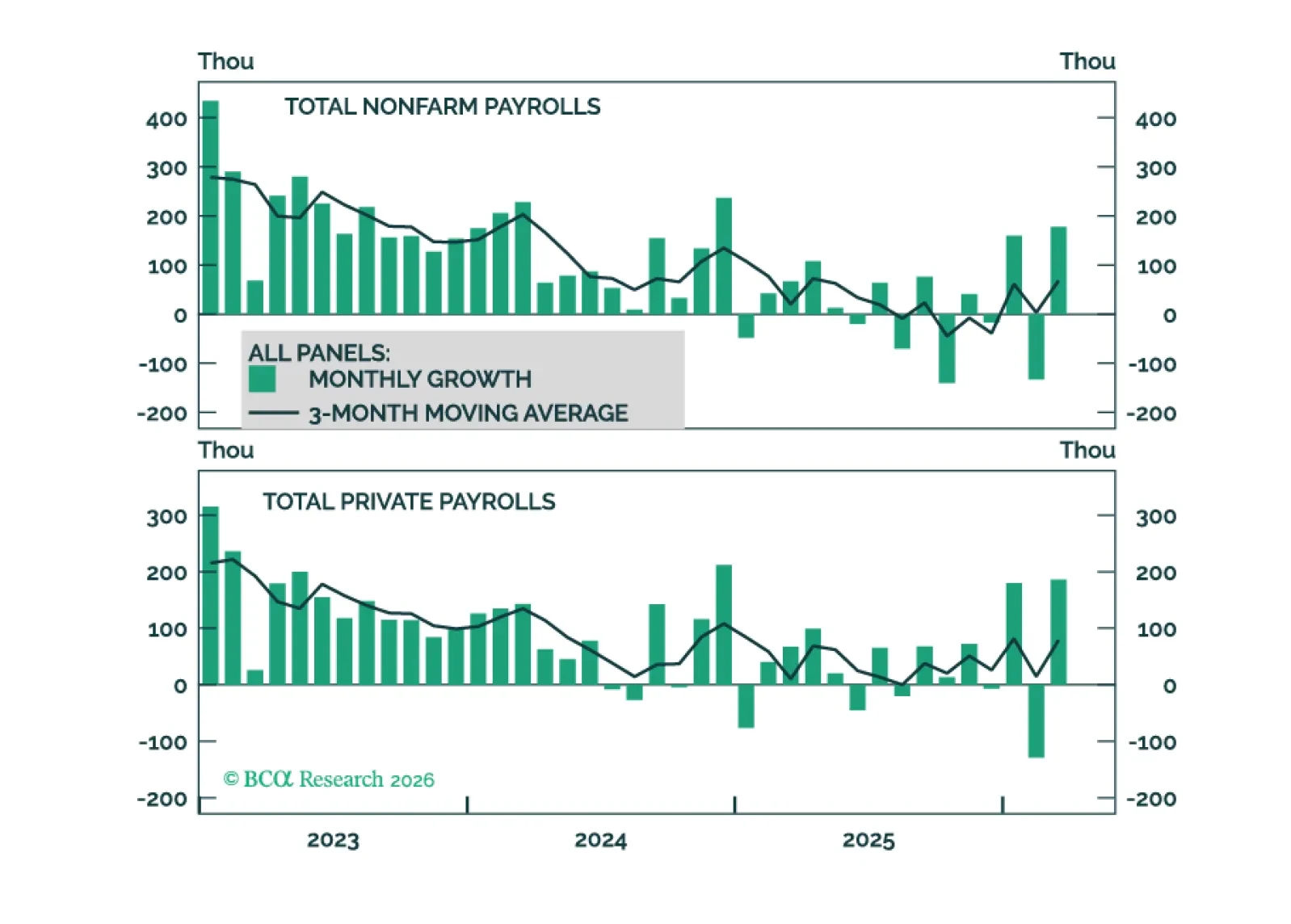

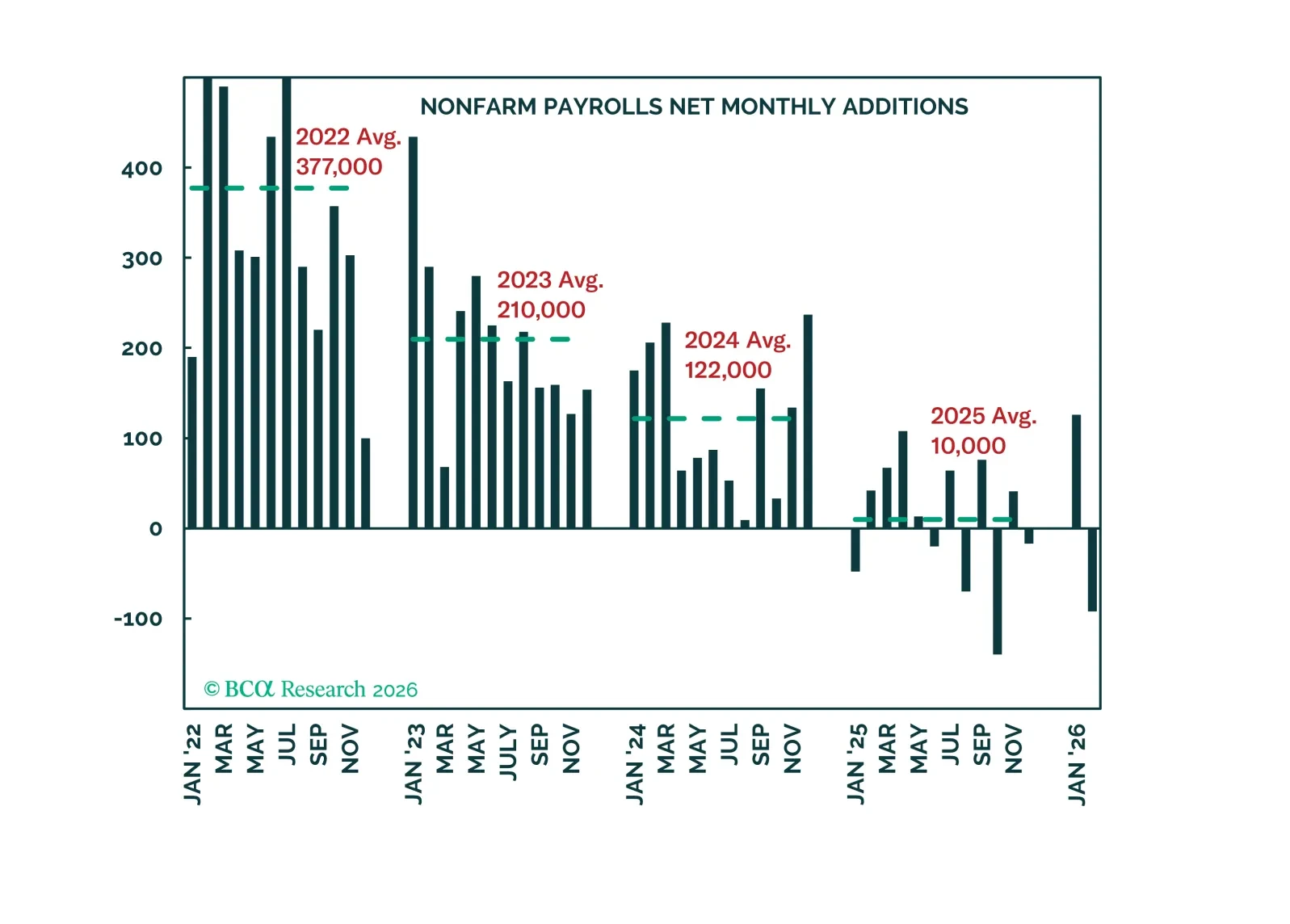

Improving job growth keeps Fed rate cuts off the table, but evidence of labor market tightening will be required before rate hikes become part of the discussion.

US employment data show some tentative signs of job growth acceleration and stable utilization. We see breakeven monthly job growth as closer to +30k per month than zero.

Job creation remains stalled, but consumers are carrying on and S&P 500 earnings have been growing by double digits. Although the repercussions from the war in the Middle East are not yet clear, the US economy was doing just fine before it began.

Looking through month-to-month volatility, job growth’s underlying trend is stable and consistent with a flat-to-slightly higher unemployment rate.

In Section I, Doug recommends cutting US equity exposure in favor of Europe as reduced recession odds make it unlikely that the US will draw safe-haven capital flows. In Section II, Jesse ranks middle economic powers across hard and soft power dimensions and recommends investing in their defense and industrial sectors.

In Section II, Jesse ranks middle economic powers across hard and soft power dimensions and recommends investing in their defense and industrial sectors.

The labor market tightened in January, significantly lowering the odds of a H1 2026 rate cut. Rate cuts driven by lower inflation are still likely in H2 2026.

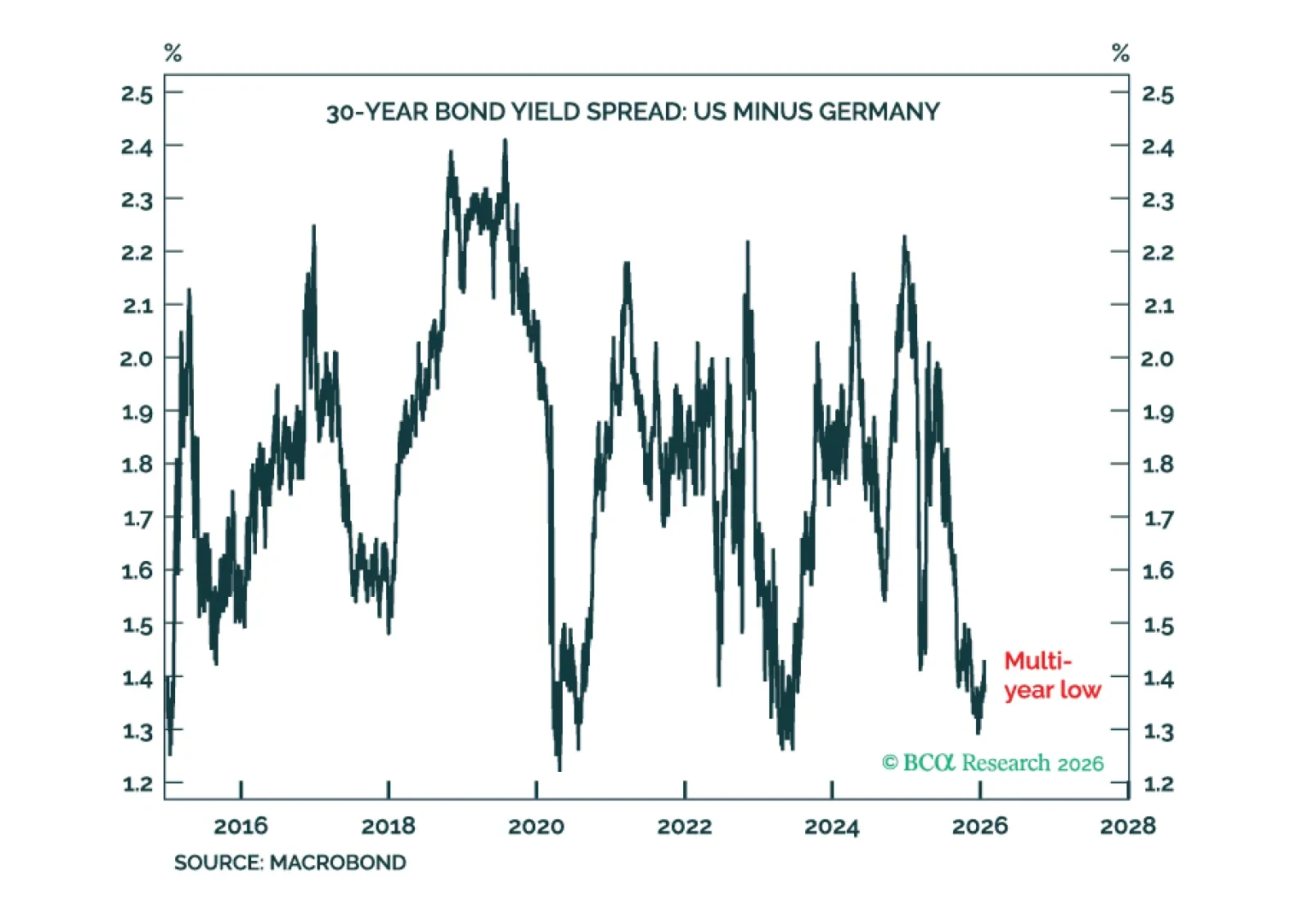

US Treasury yields require a higher premium for both geopolitical risk and inflation risk, but higher bond yields are not necessarily bad for stocks.

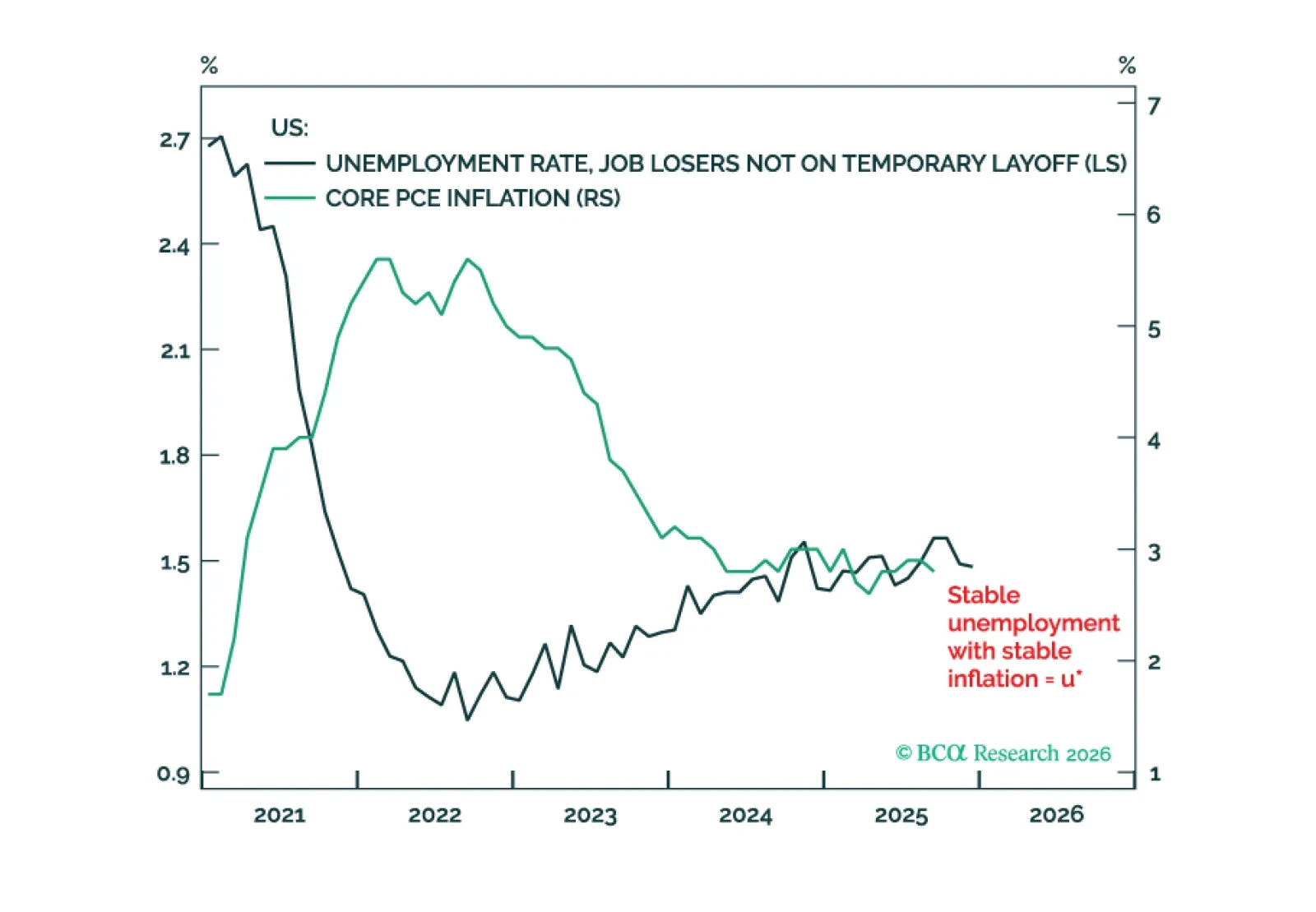

With the US unemployment rate and interest rate close to the ‘neutral’ u-star and r-star respectively, further Fed rate cuts risk pushing up inflation and long-term inflation expectations. This is bad for bonds but good for stocks. Plus, two new trades are: short TOPIX versus DAX; and short CAT versus SPX.