US Labor Market

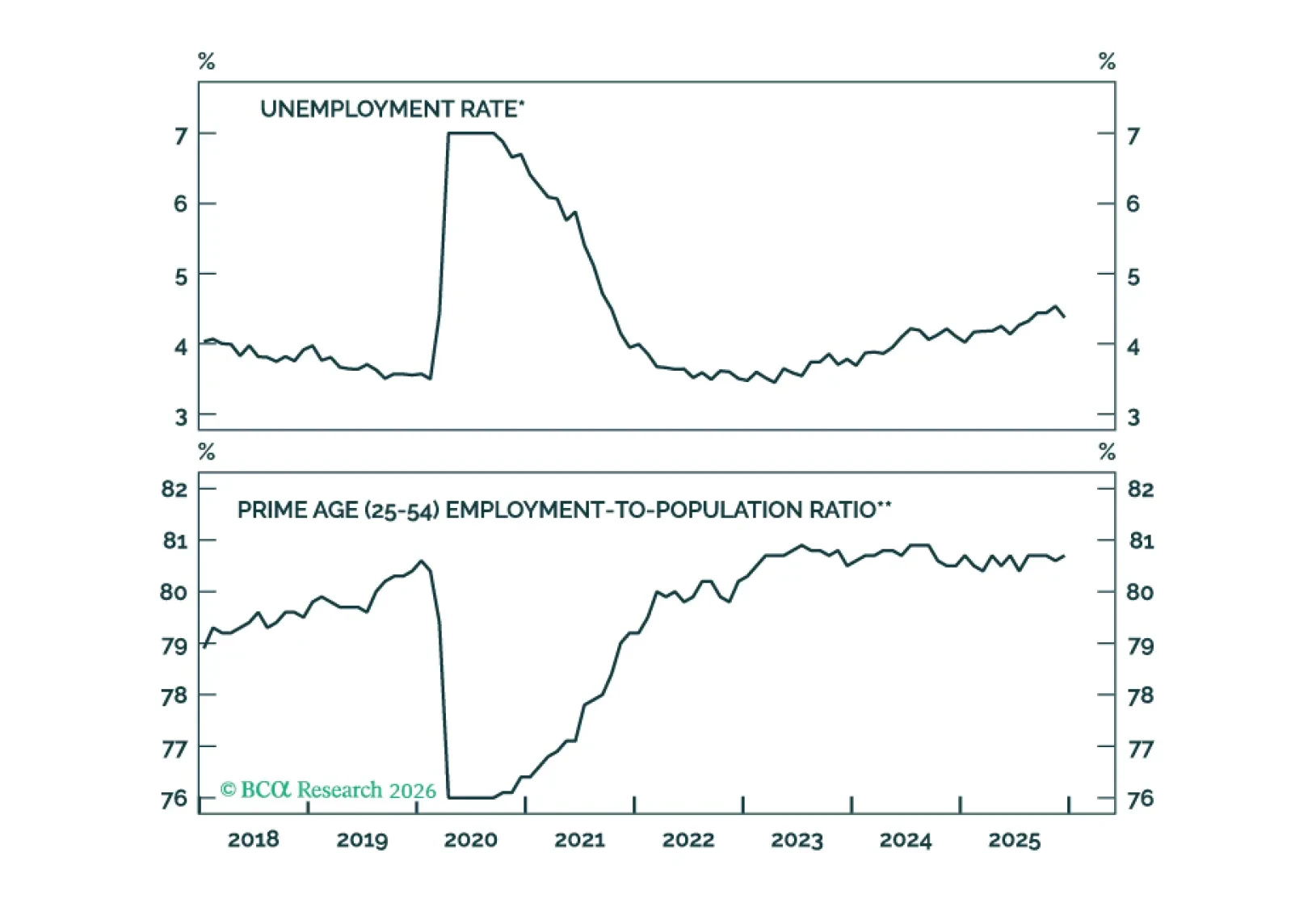

Measures of labor market utilization improved in December, ruling out a January cut and significantly reducing the odds of a March cut.

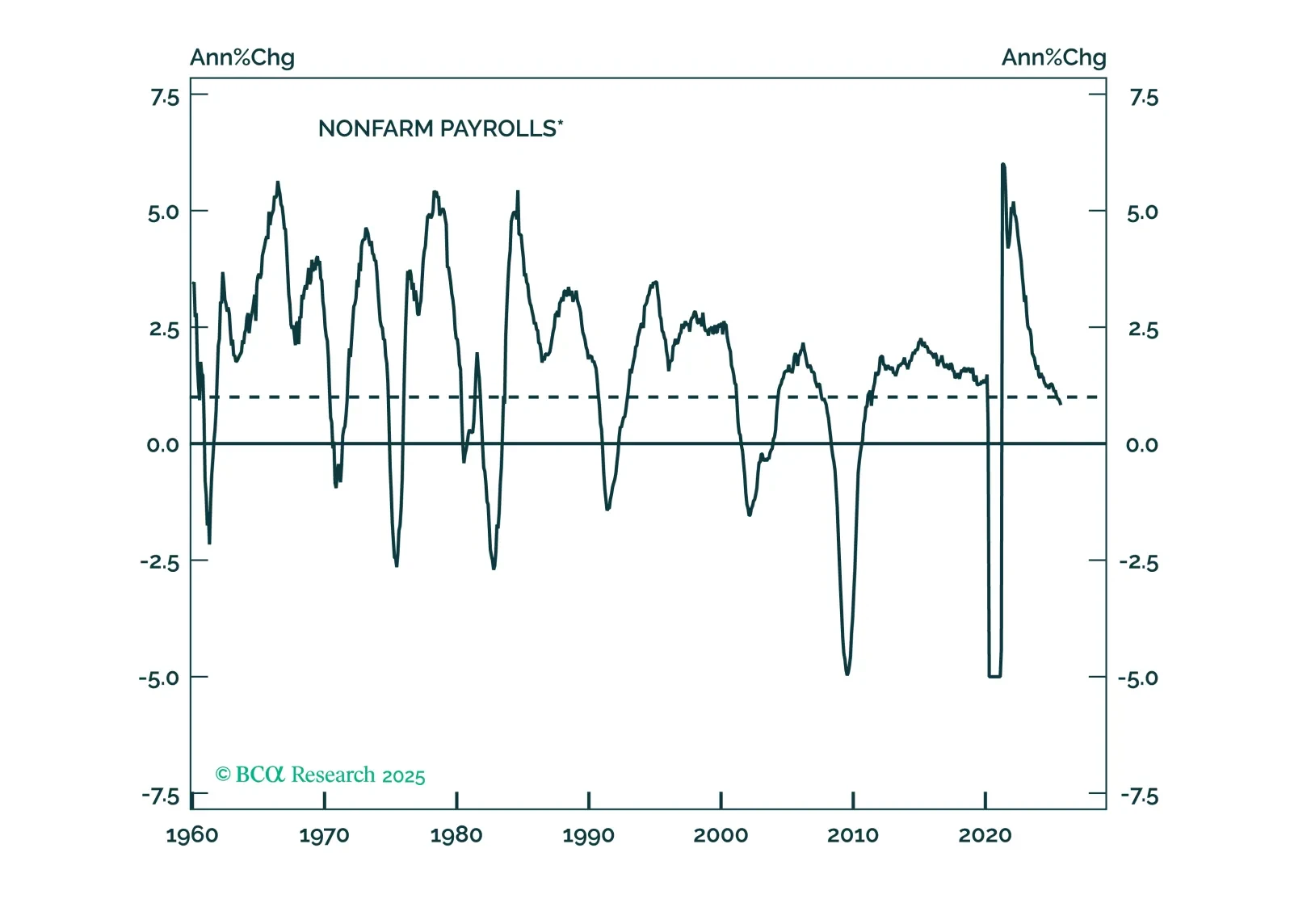

Employment Data Point To Dovish Policy Surprises In 2026

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

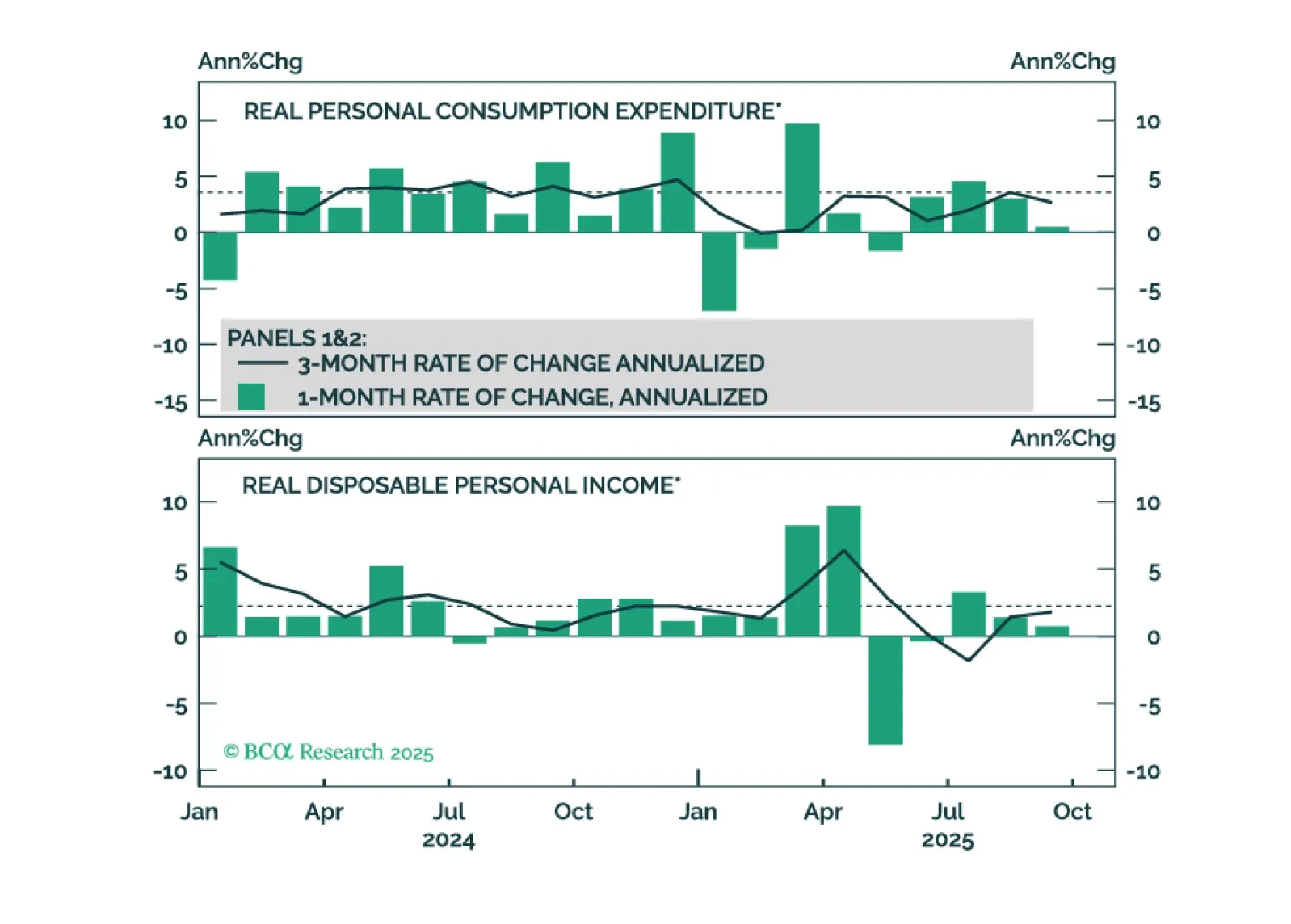

September’s weak consumer spending data challenge the K-shaped recovery narrative and suggest that spending will slow to match already-weak employment growth.

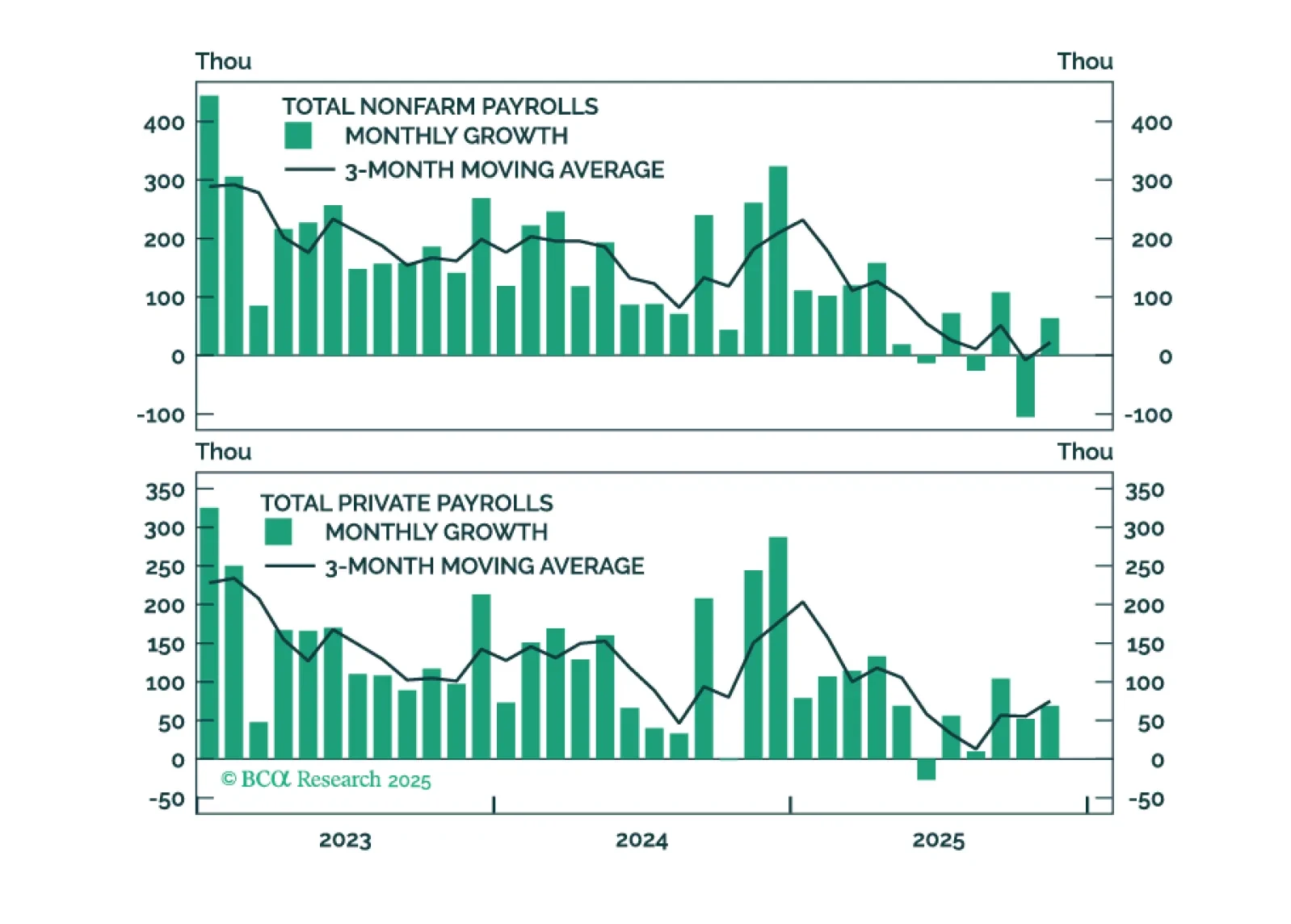

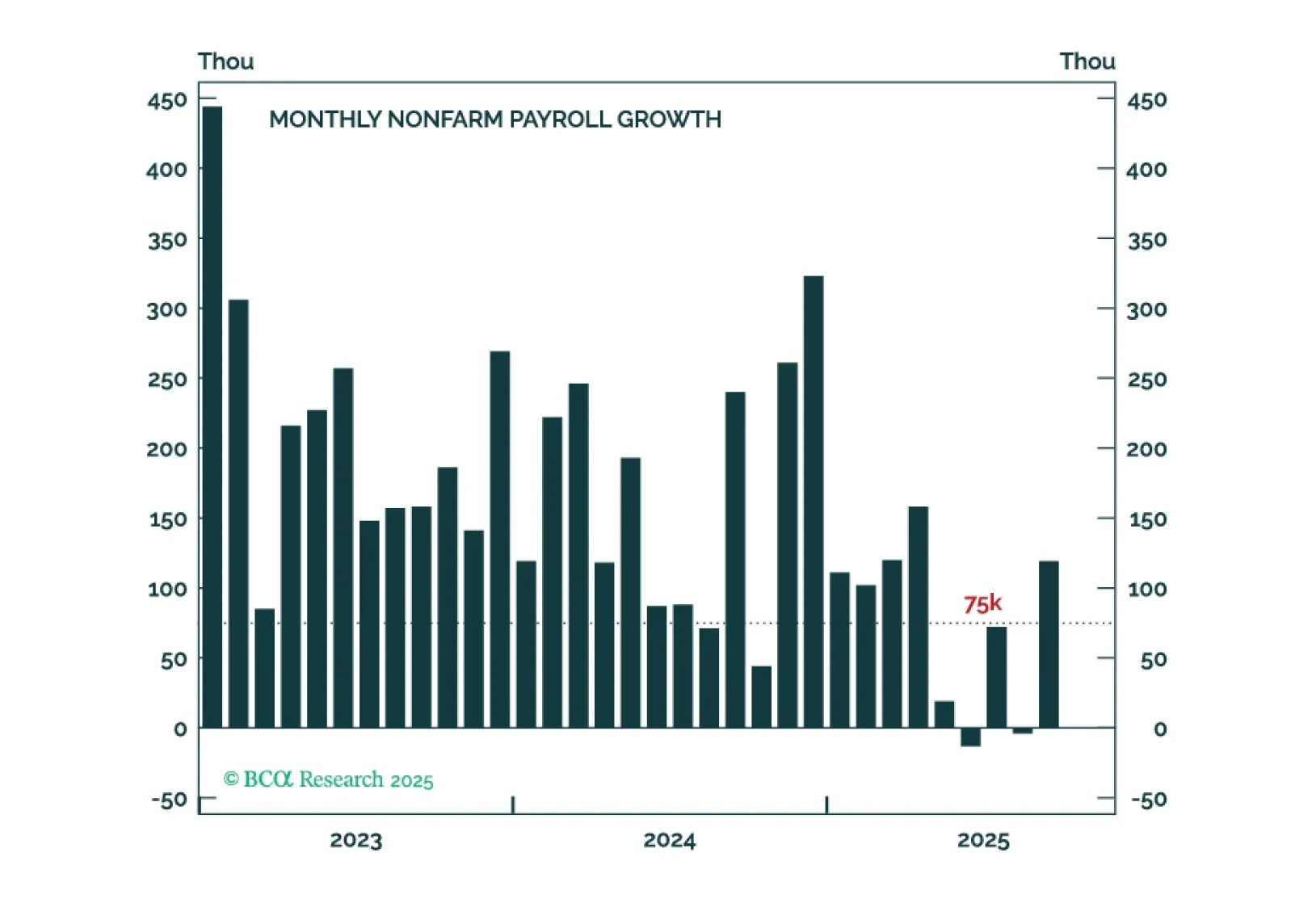

September job gains topped modest expectations, but year-over-year payrolls growth appears to have fallen below stall speed. We remain concerned about US activity.

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.

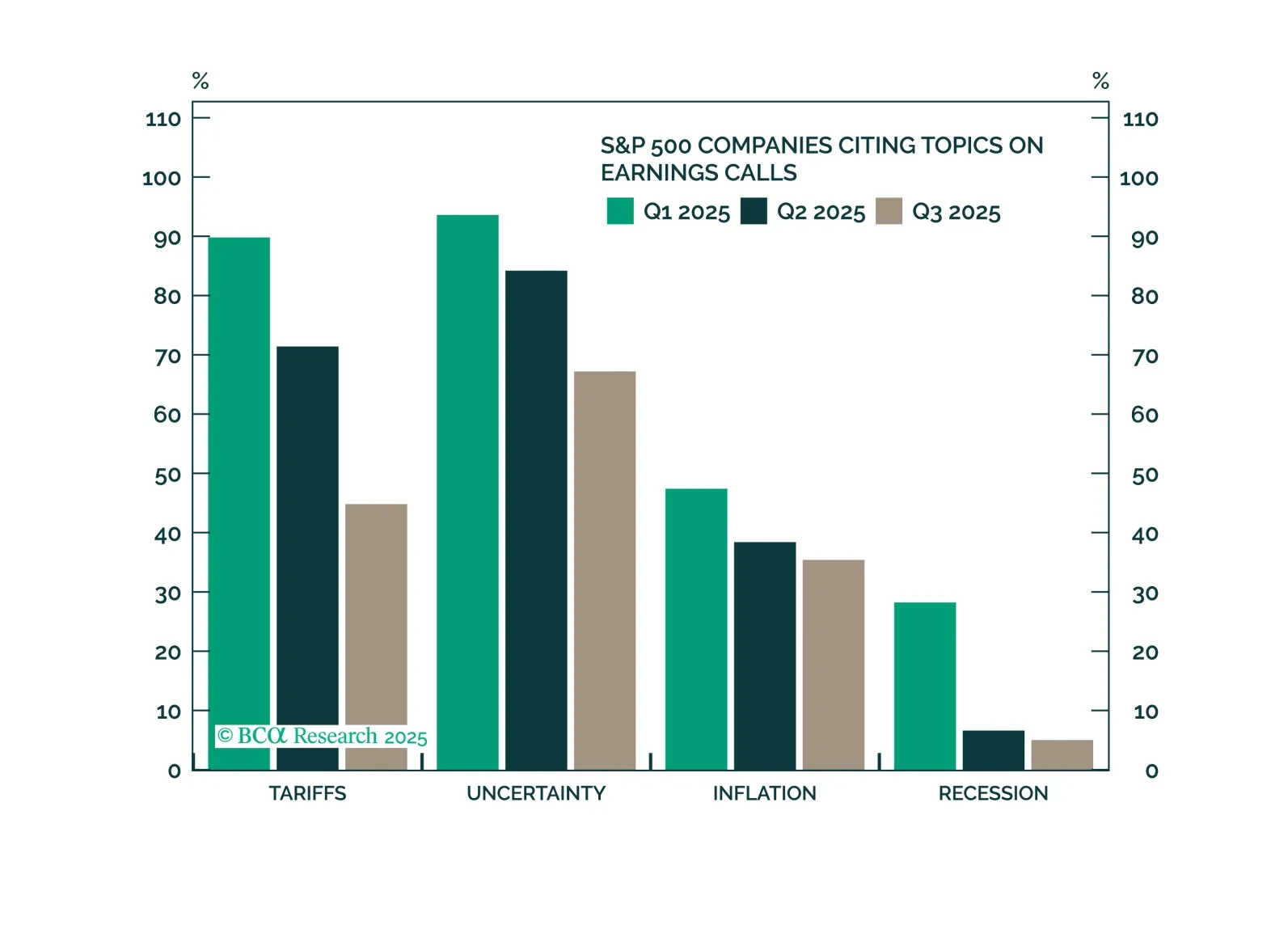

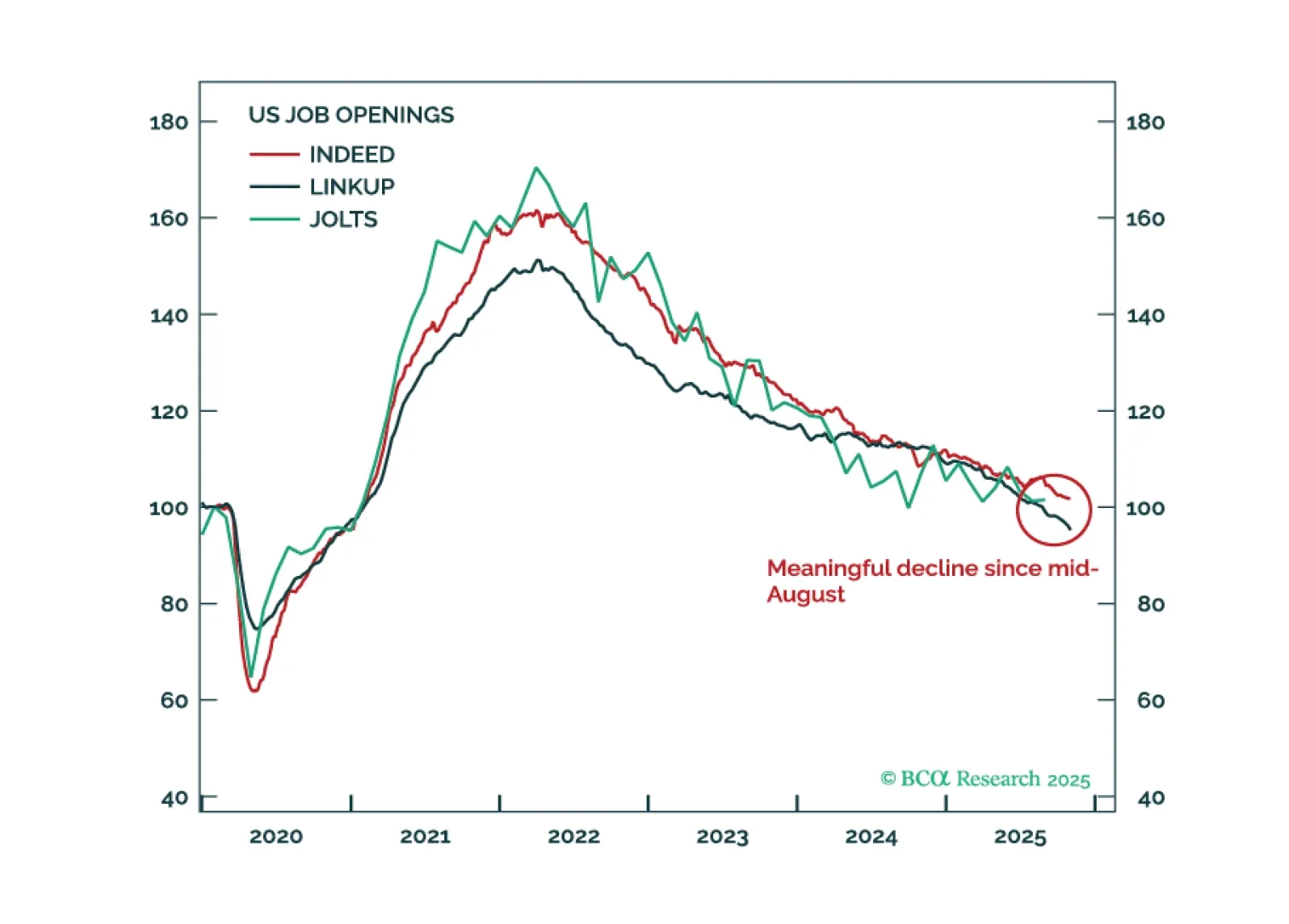

Tariffs are fading in importance as companies successfully mitigate cost pressures and preserve profitability. The recent wave of high-profile layoffs is more concerning, but there does not appear to be a systemic reason behind the announcements. However, emerging labor market softness could pose a major risk for equities. We remain vigilant.

In the absence of official government data, investors are turning to alternative sources to gauge the direction of the US economy. Our analysis of this data suggests that the economy has continued to expand at a moderate pace over the past two months. If the Supreme Court were to strike down the tariffs, this would reduce the near-term odds of a recession while raising the odds of overheating.

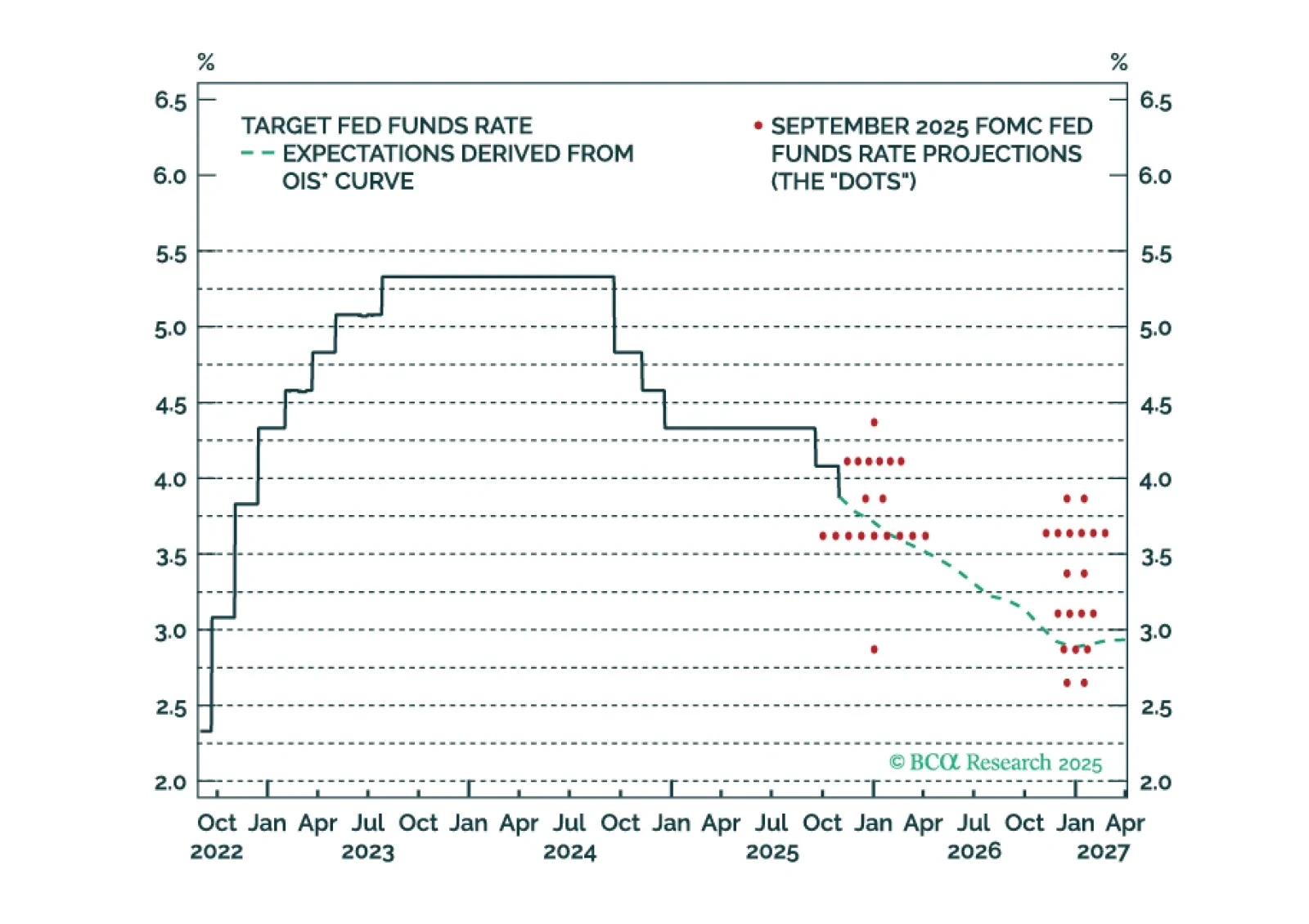

The Fed cut rates today, but a follow-up rate cut in December is uncertain. It will depend, in large part, on who wins a debate about the neutral rate of interest.