United States

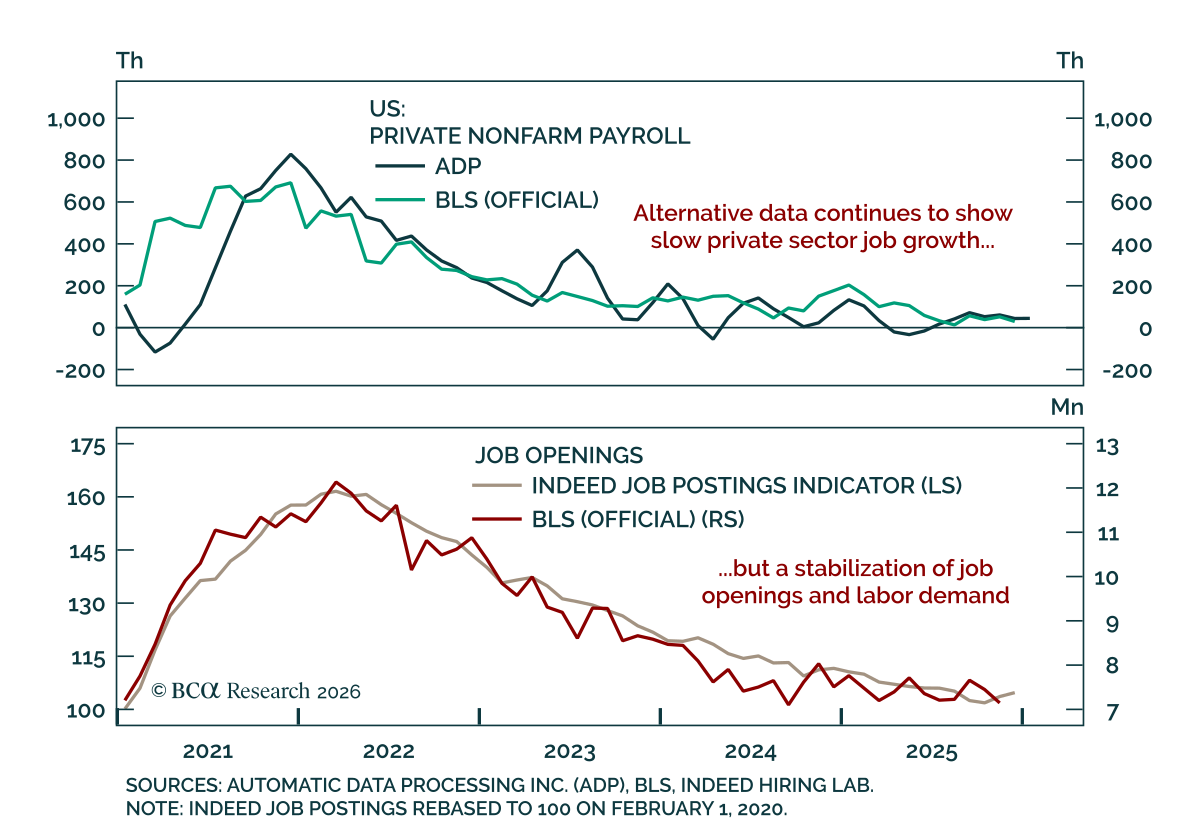

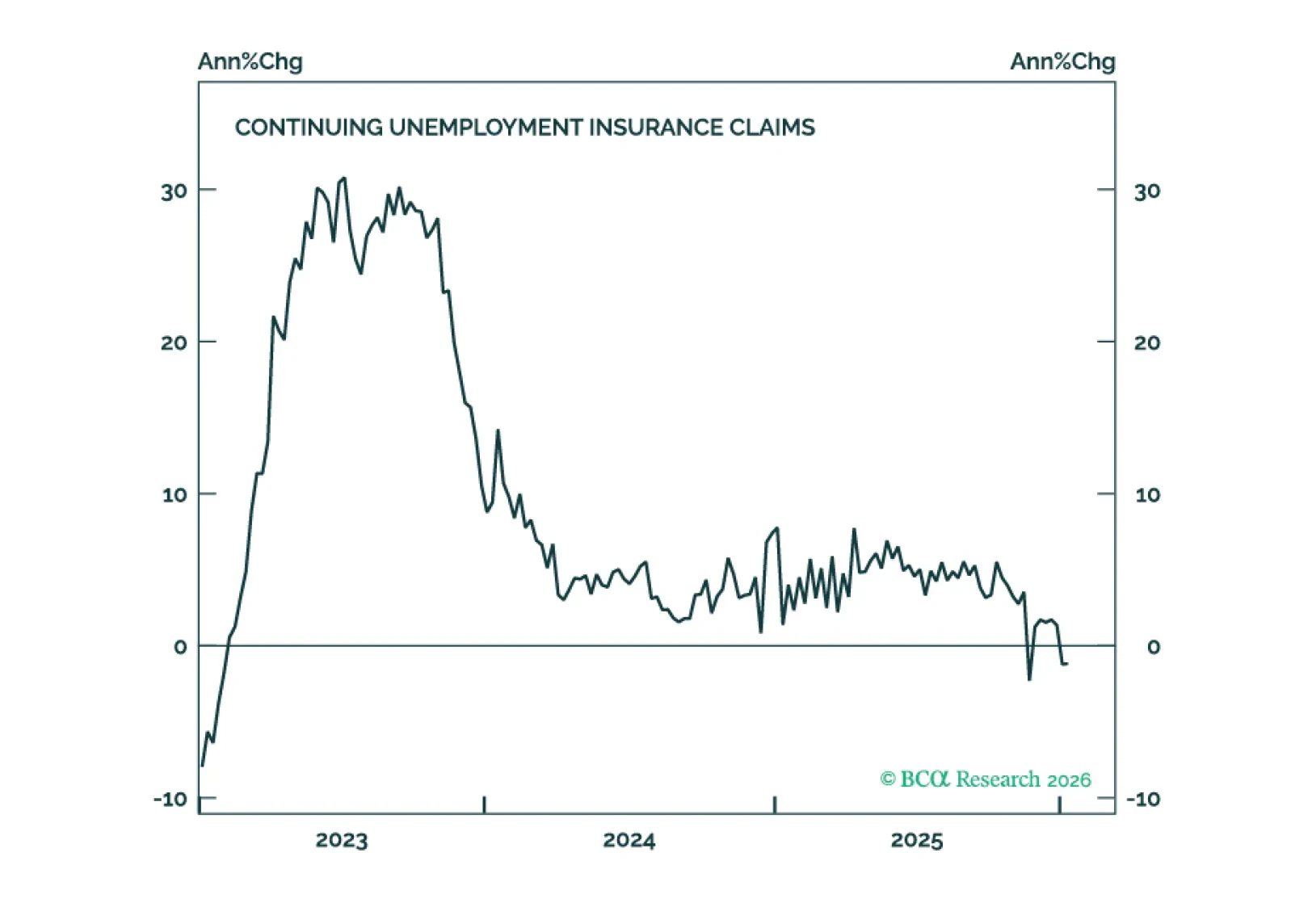

The US labor market remains weak but stable, leaving both labor conditions and US rates at a pivotal point. Given the partial government shutdown, Friday’s January employment report has been postponed to February 11. Alternative data show the US labor market…

Our Portfolio Allocation Summary for February 2026.

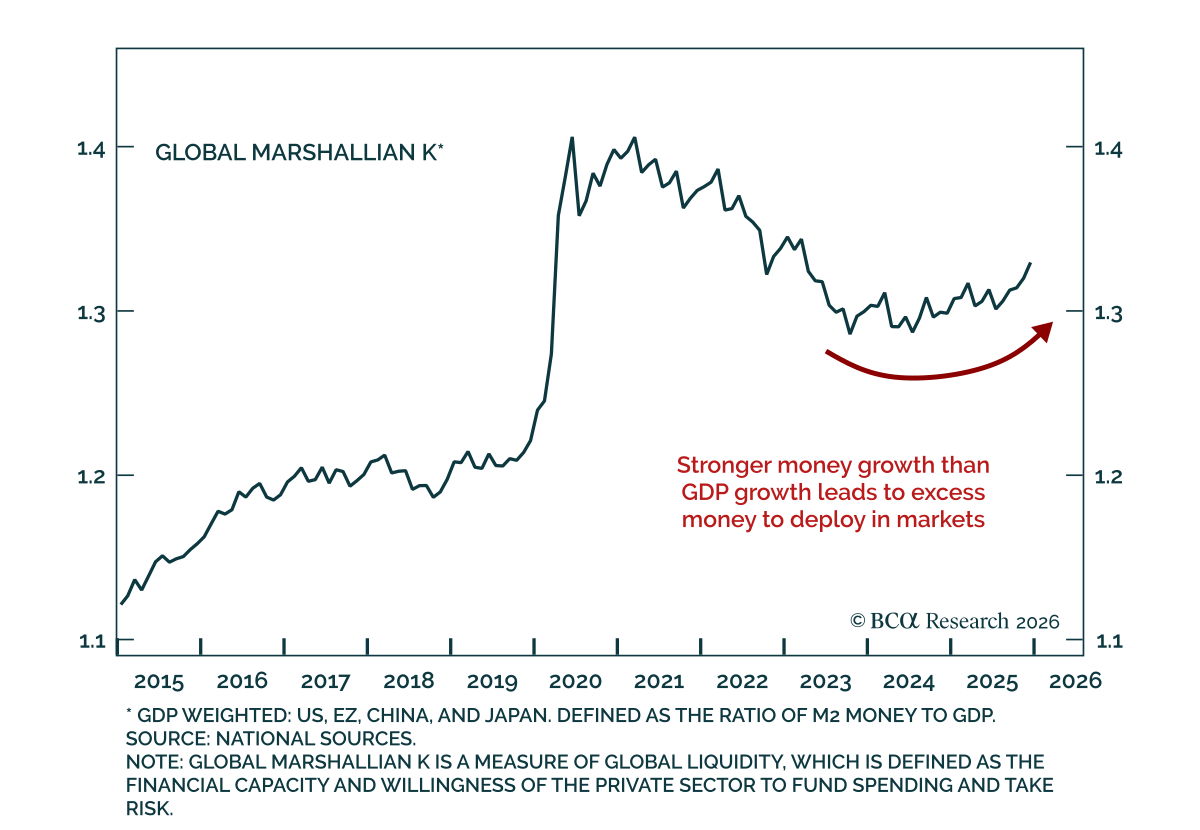

Our Developed Markets ex-US strategists view global liquidity as the decisive macro variable in 2025 and expect it to remain broadly supportive through most of 2026. They therefore stay neutral on equities versus bonds, keep a positive bias toward metals,…

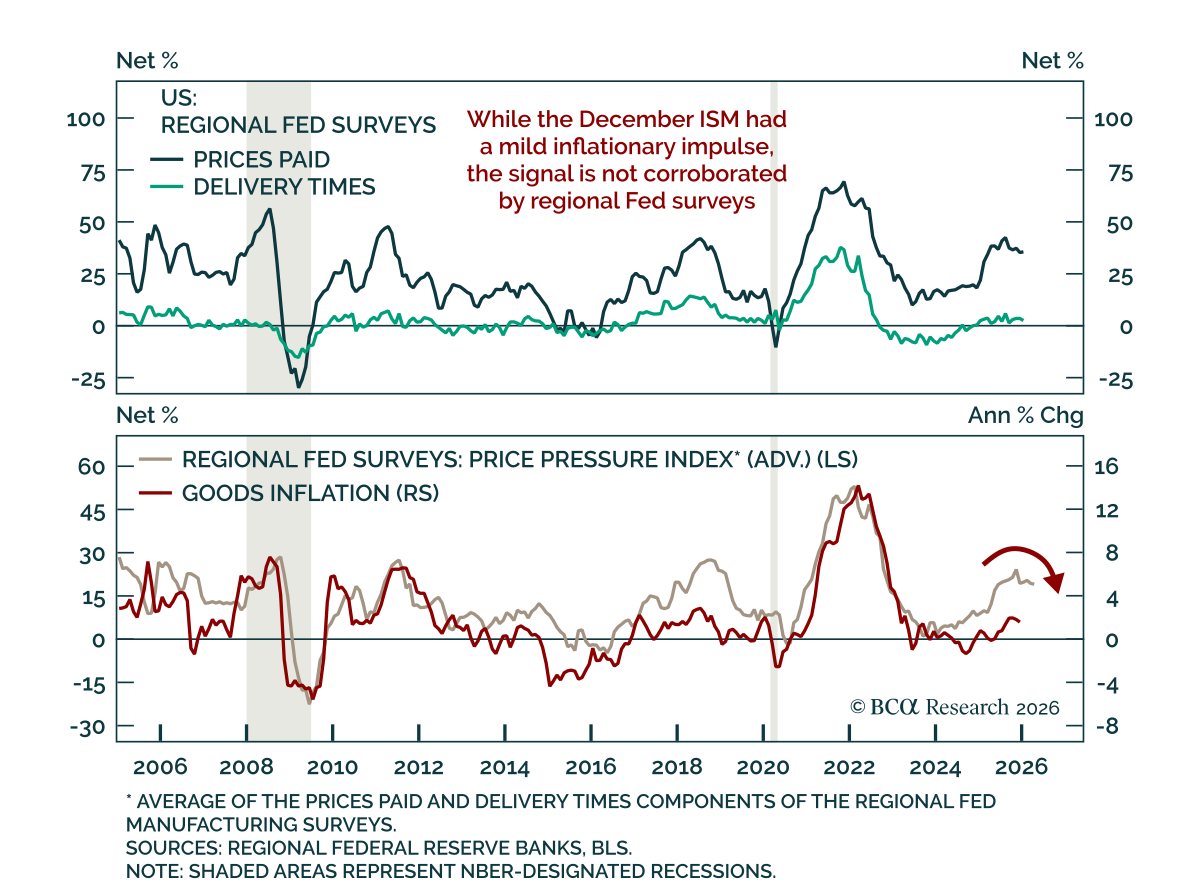

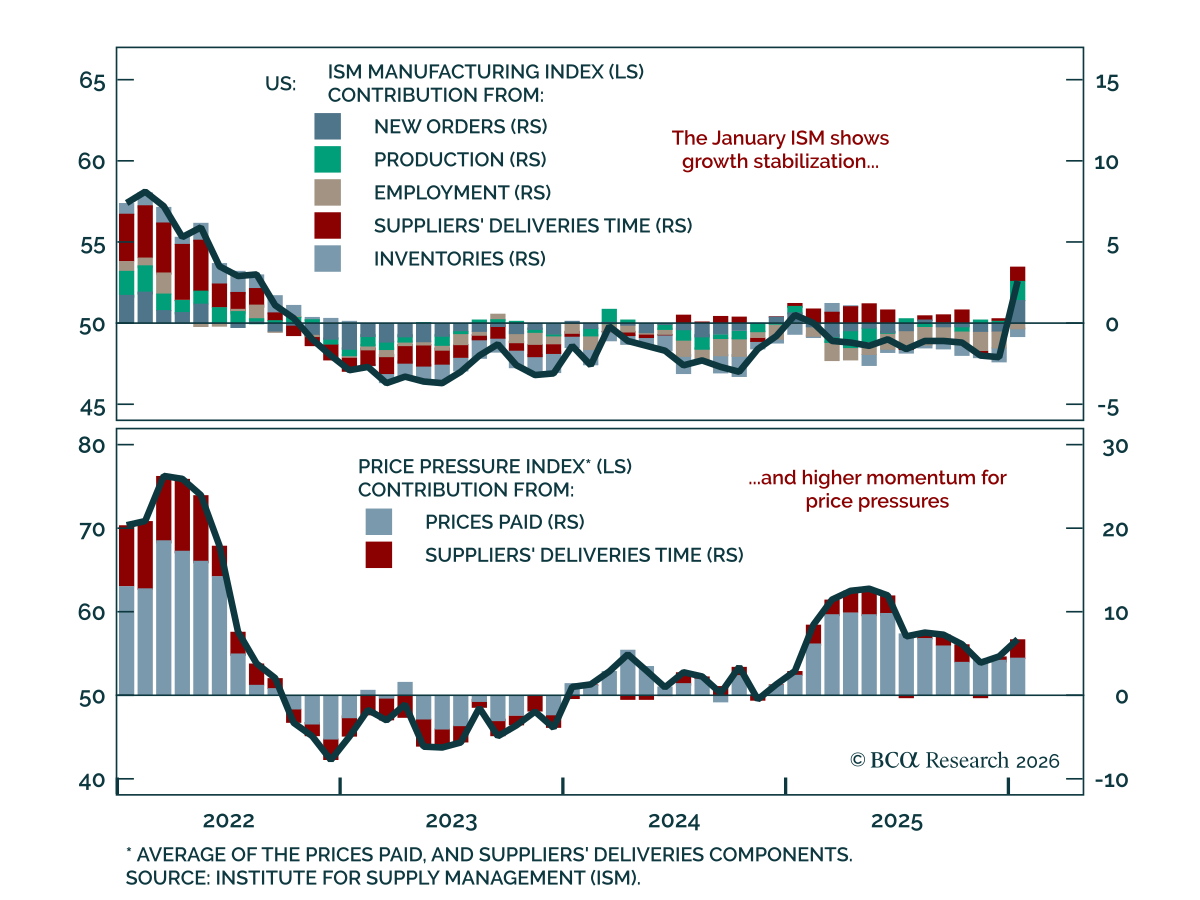

Maintain an overweight duration stance and curve steepeners within US bond portfolios, as the recent uptick in ISM price pressures comes from delivery times, not accelerating costs. While the December ISM Manufacturing report delivered positive growth…

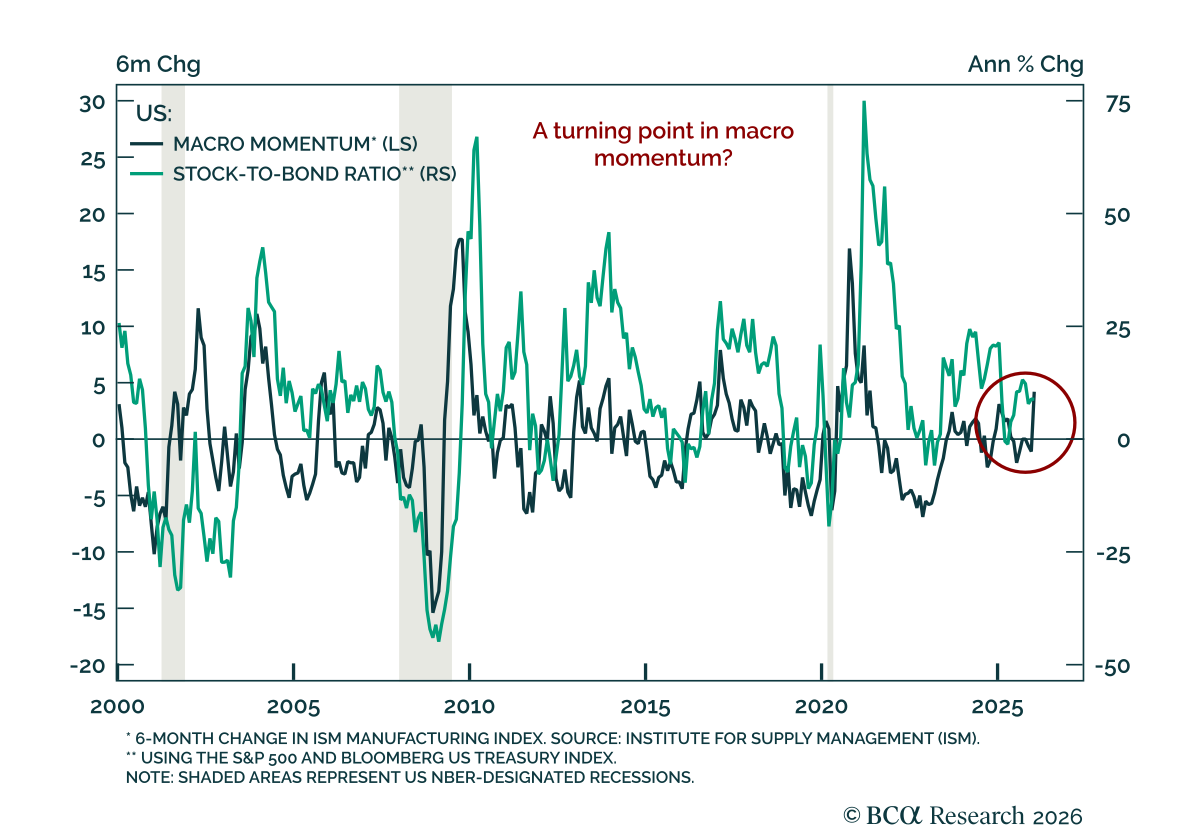

Global manufacturing is stabilizing, with early indications that macro momentum could be turning. The global economy slowed through 2025 due to tariffs and uncertainty, but there are now signs of recovering manufacturing. While DM composite PMIs have largely…

Manufacturing data points to resilience after a prolonged slowdown, with inflation risks tilting modestly higher. The January ISM Manufacturing index beat expectations and moved back into expansion at 52.6, after ten consecutive months of contraction through…

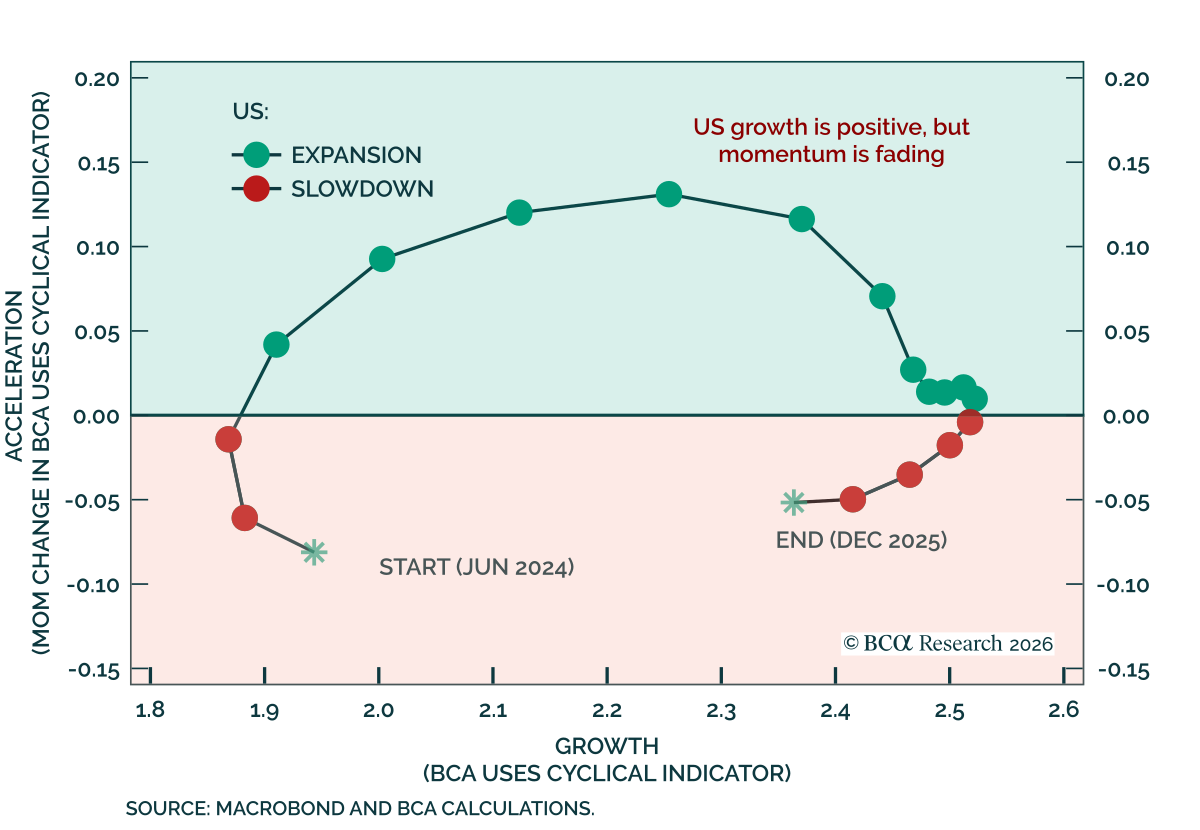

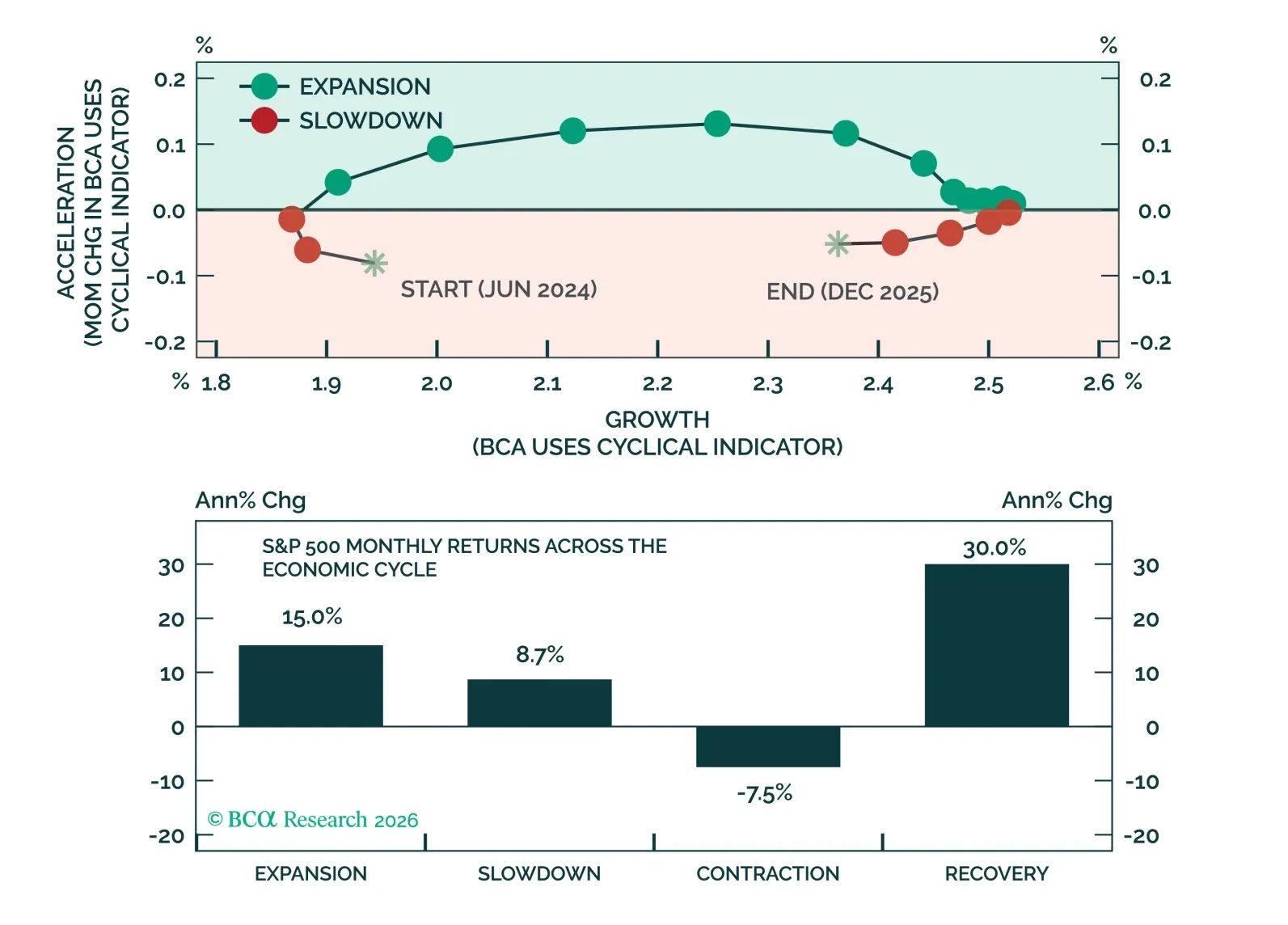

Our US equity strategists expect another year of gains for the S&P 500 in 2026, with returns capped by revenue growth as the bull market matures. The US economy is slowing but not contracting, pointing to positive but more modest equity returns. Equity…

2026 should see another year of gains for the S&P 500, but, as the bull market matures and growth slows, returns will be capped by revenue growth rather than being boosted by expanding margins and multiples. We think Tech can outperform, but leadership will broaden and performance gaps will narrow.

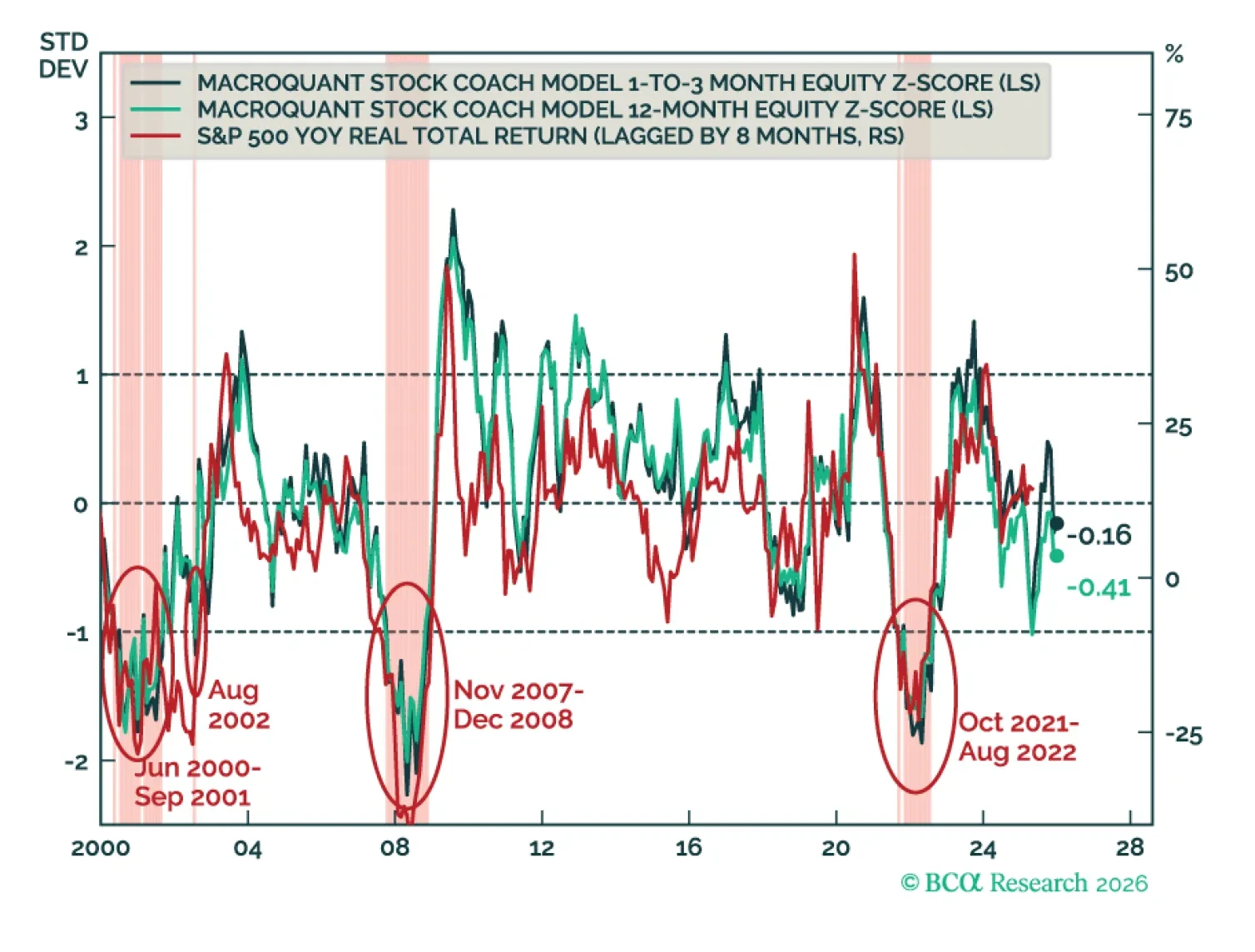

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

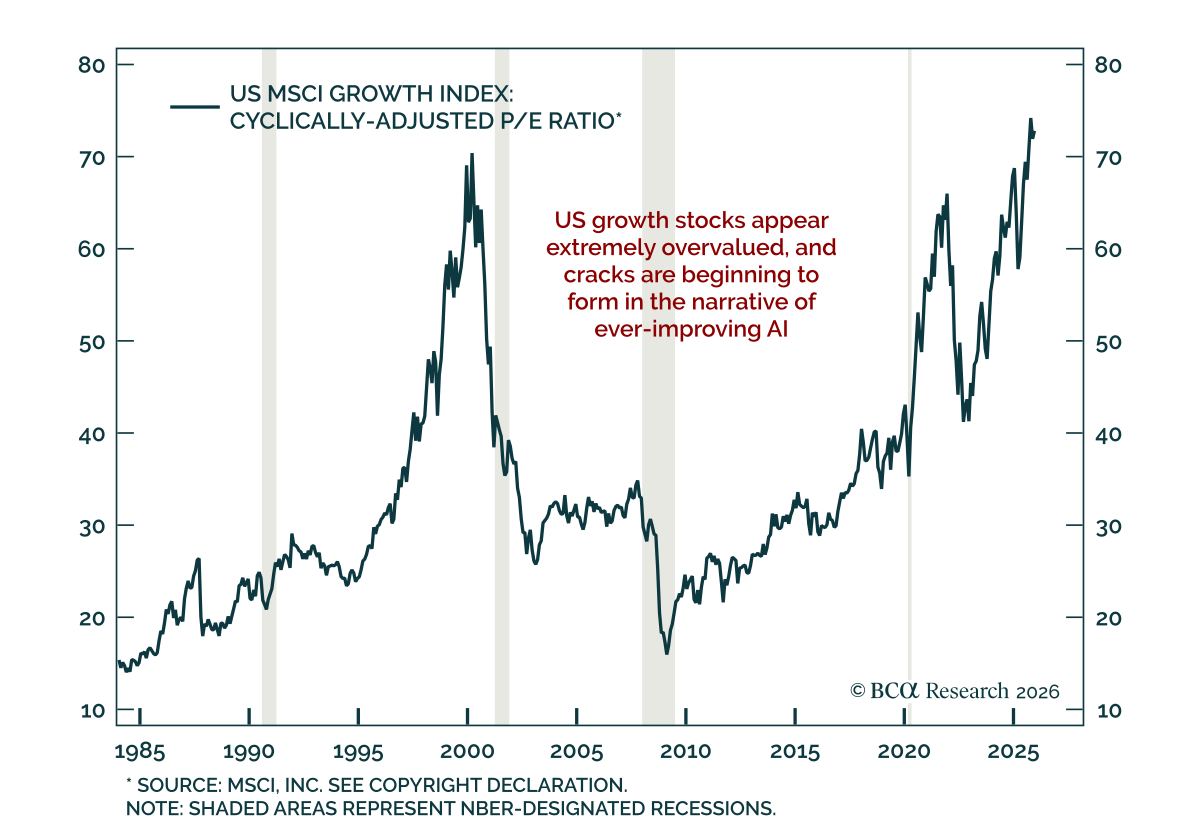

Our Bank Credit Analyst colleagues see an increasingly asymmetric risk profile for global equities, as technology expectations hinge on continued exponential progress in AI models. Expectations for tech earnings, semiconductor demand, and US data center…