United States

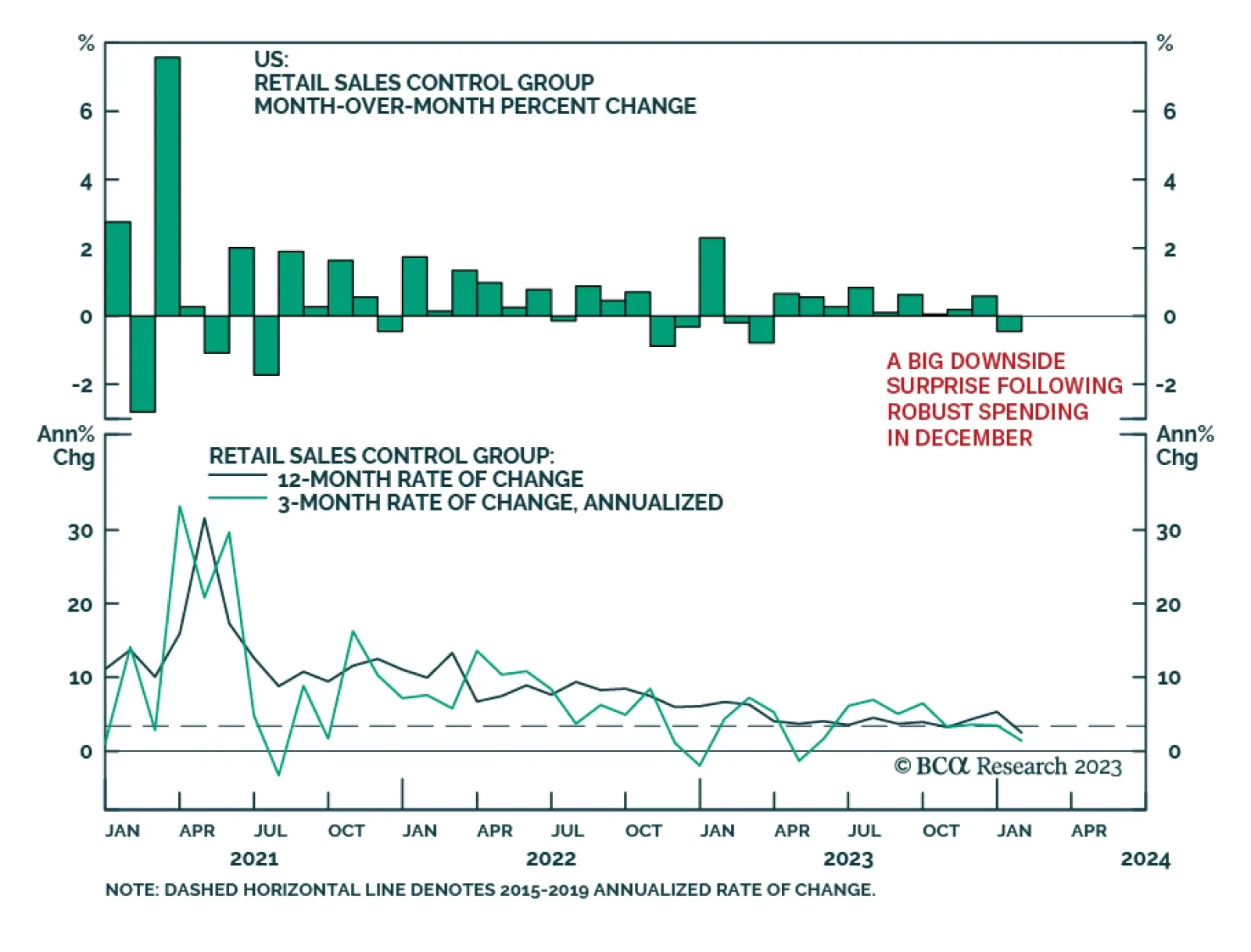

The US retail sales report for January delivered a disappointing message about consumer spending. The 0.8% m/m drop in overall retail sales was worse than expectations of a 0.2% m/m decline and marked the most severe monthly contraction since last March. The…

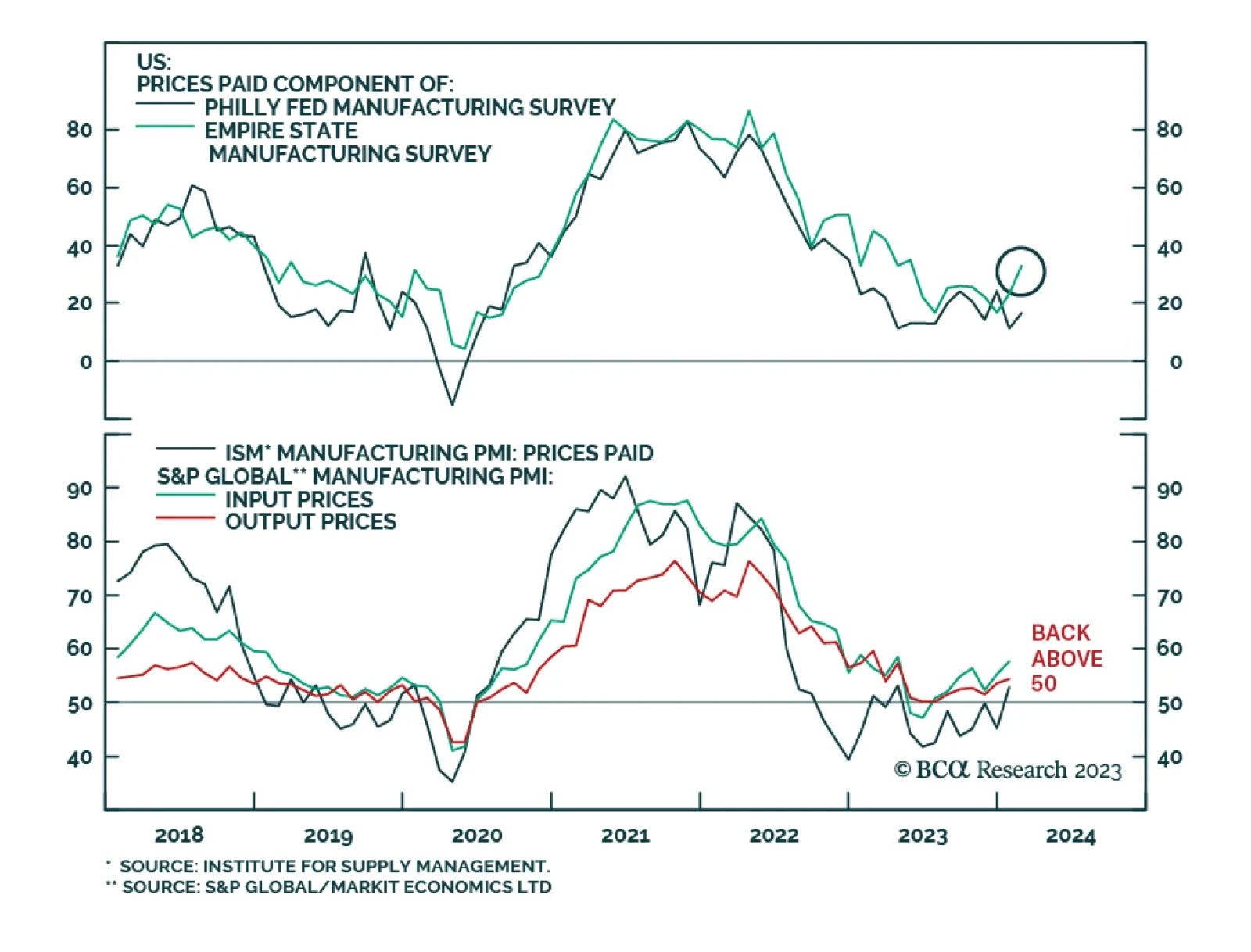

The first two regional fed manufacturing surveys for February delivered strong upside surprises. The New York Fed’s Empire Index surged from -43.7 to -2.4, unwinding its January slump. Similarly, the Philly Fed current activity index jumped by 15.8 points to…

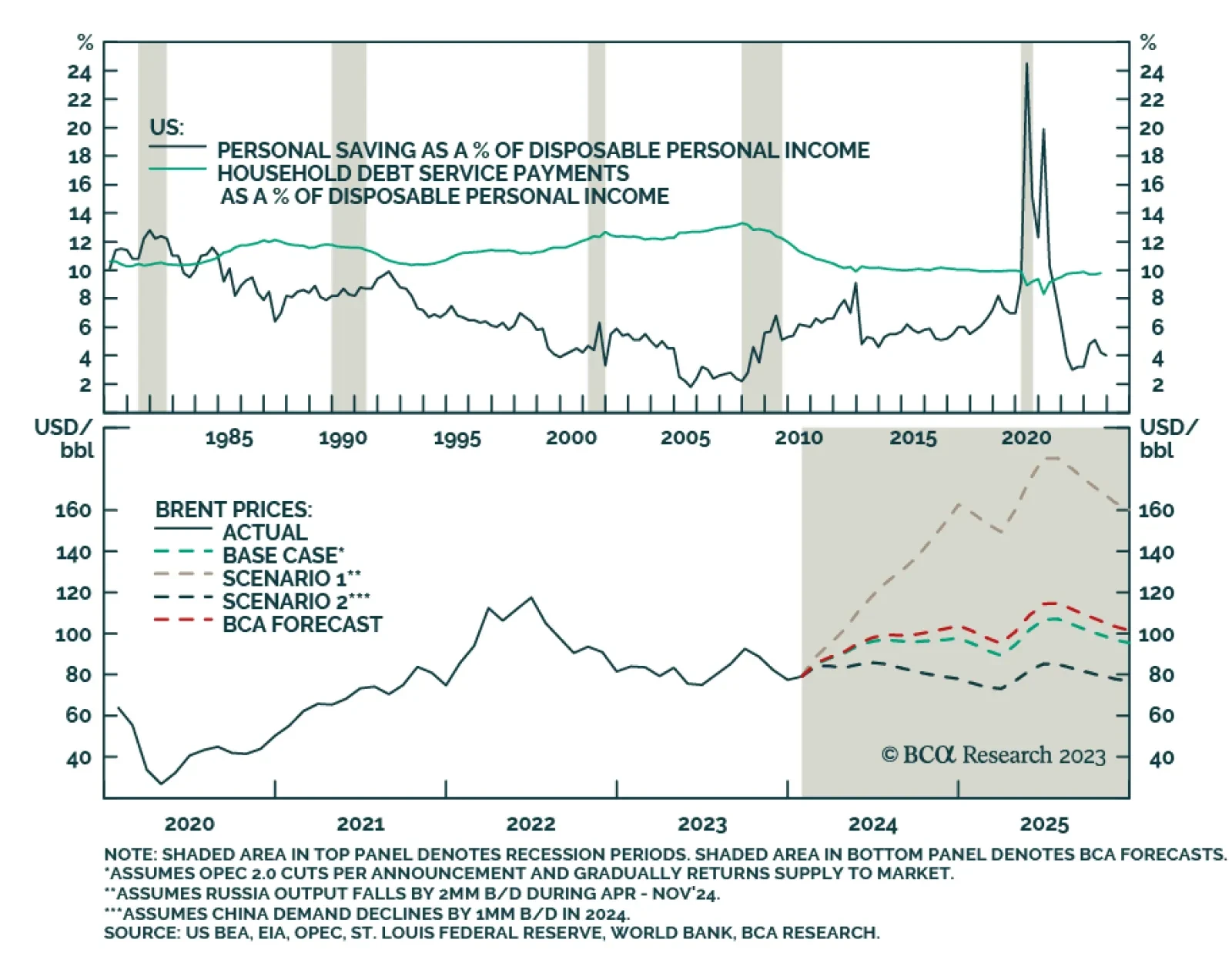

Our Commodity & Energy colleagues see oil markets balanced in the short run, which keeps their Brent price forecasts at $95/bbl and $105/bbl for 2024 and 2025. That said, they note the odds are increasing demand growth could surprise to the…

According to BCA Research’s Emerging Markets Strategy service, the diminishing pace of disinflation in the US could pose a threat to US share prices in the near term. In the medium term, the key risk to US share prices is shrinking corporate profits. …

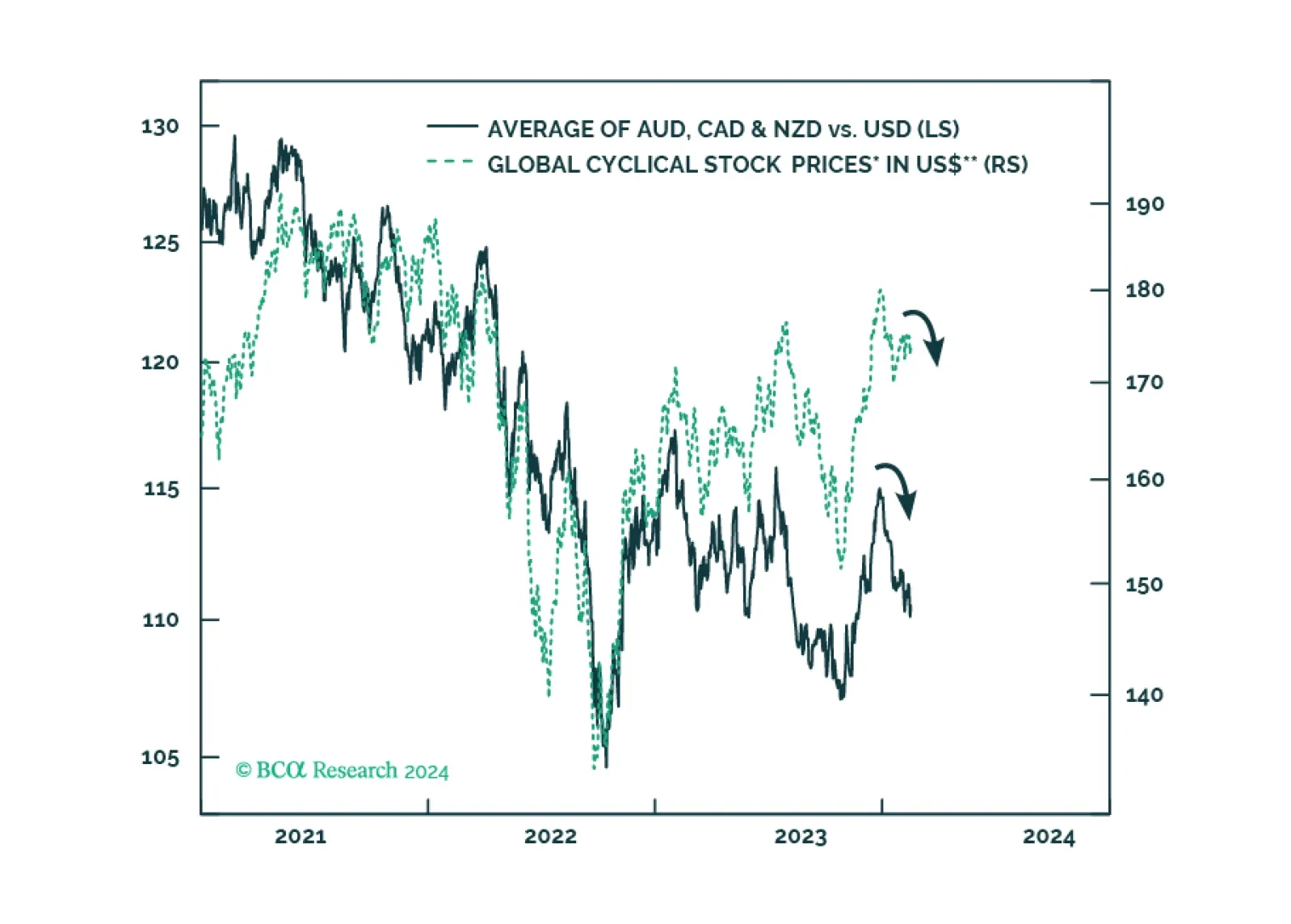

Over the next six months, the deterioration in non-US growth will occur earlier and be more pronounced than in the US. This expectation reinforces our confidence to bet on the strength of the US dollar. As usual, the flip side of the US dollar strength will be weakness in EM risk assets.

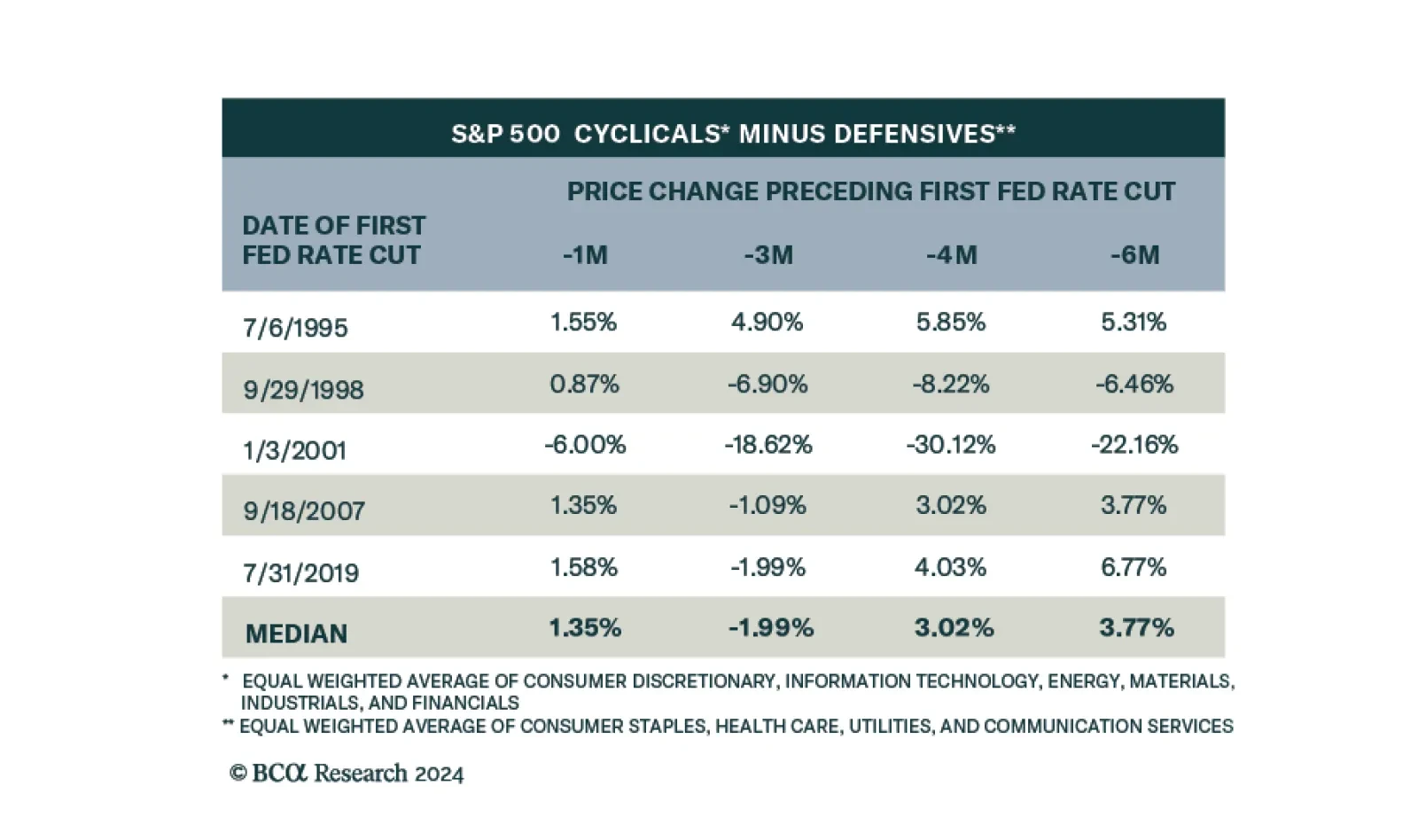

In a recent Insight we looked at the performance of equities following the start of monetary easing cycles. Specifically, we looked at the historical performance of US cyclical sectors versus defensive sectors at various points in time after the Fed’s first…

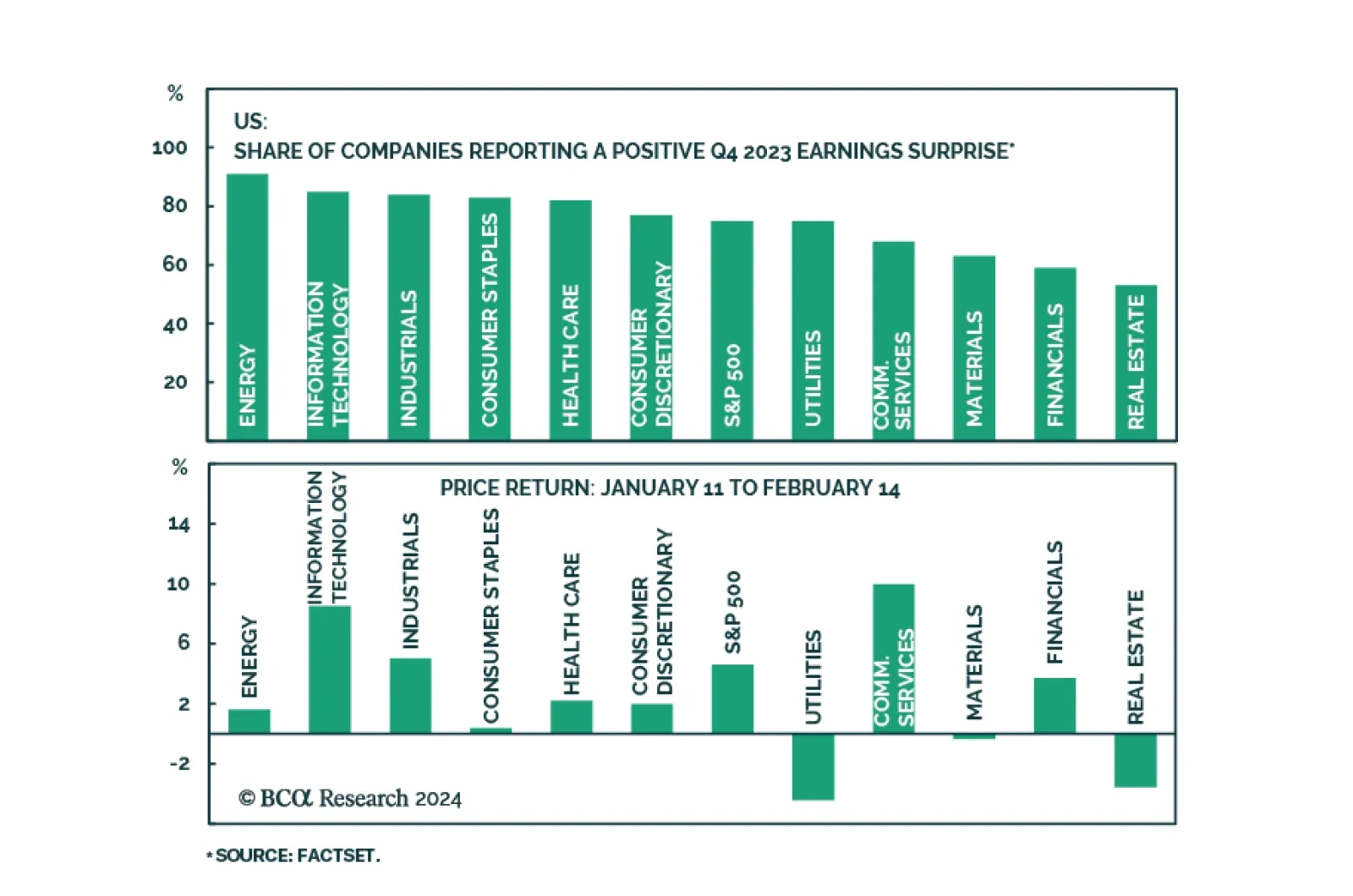

We are now more than midway through the Q4 2023 earnings season. Roughly two-thirds of the companies in the S&P 500 have released their earnings reports. It’s therefore worthwhile to stand back and observe some of the trends. According to FactSet, 75%…

According to BCA Research’s Counterpoint service, European stocks will be the big winners of the 2020s. Every decade has a big loser and a big winner. Which stock market will be the winner through the remaining two-thirds of the 2020s? The…

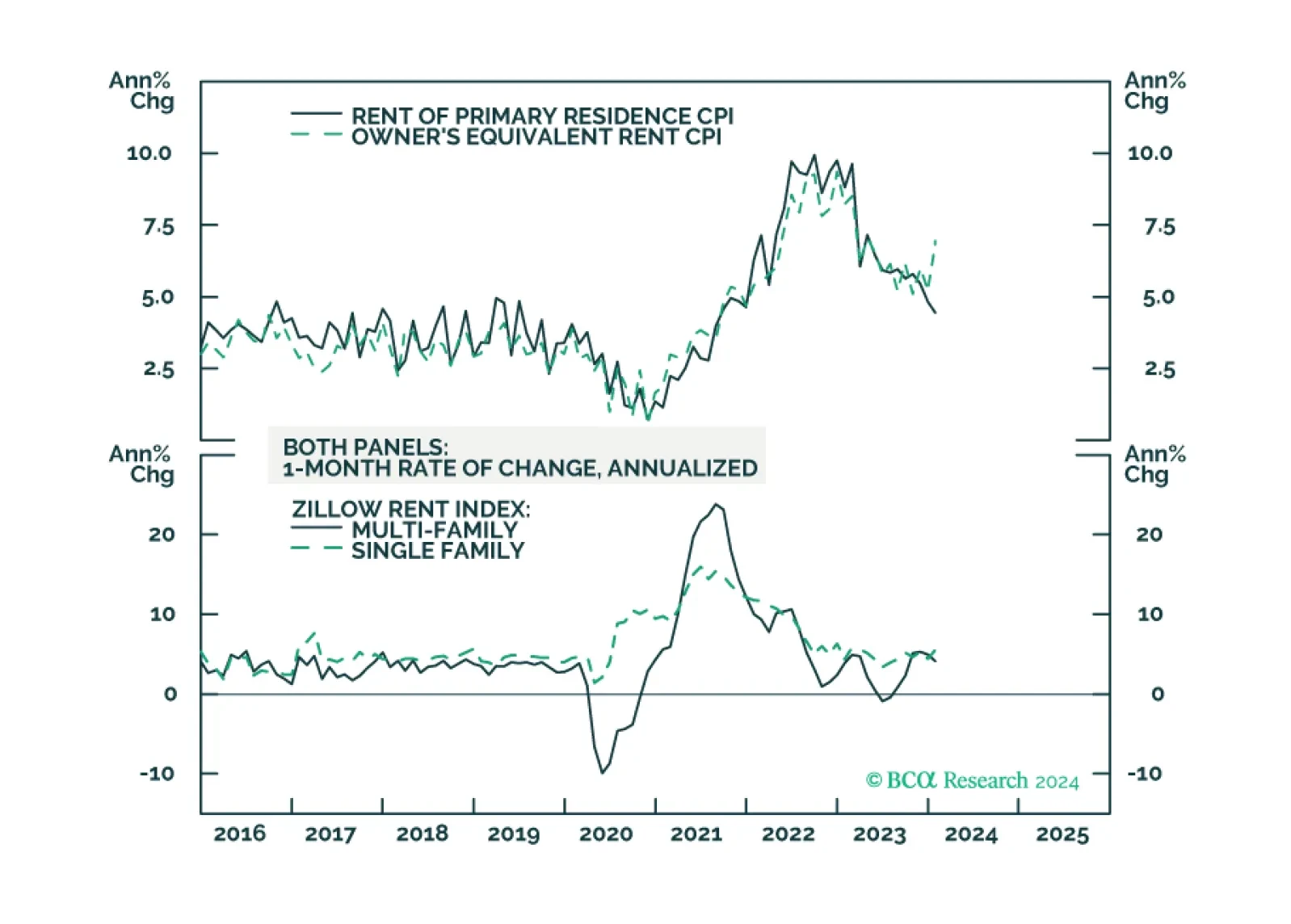

Comments on yesterday’s CPI report and yield moves.

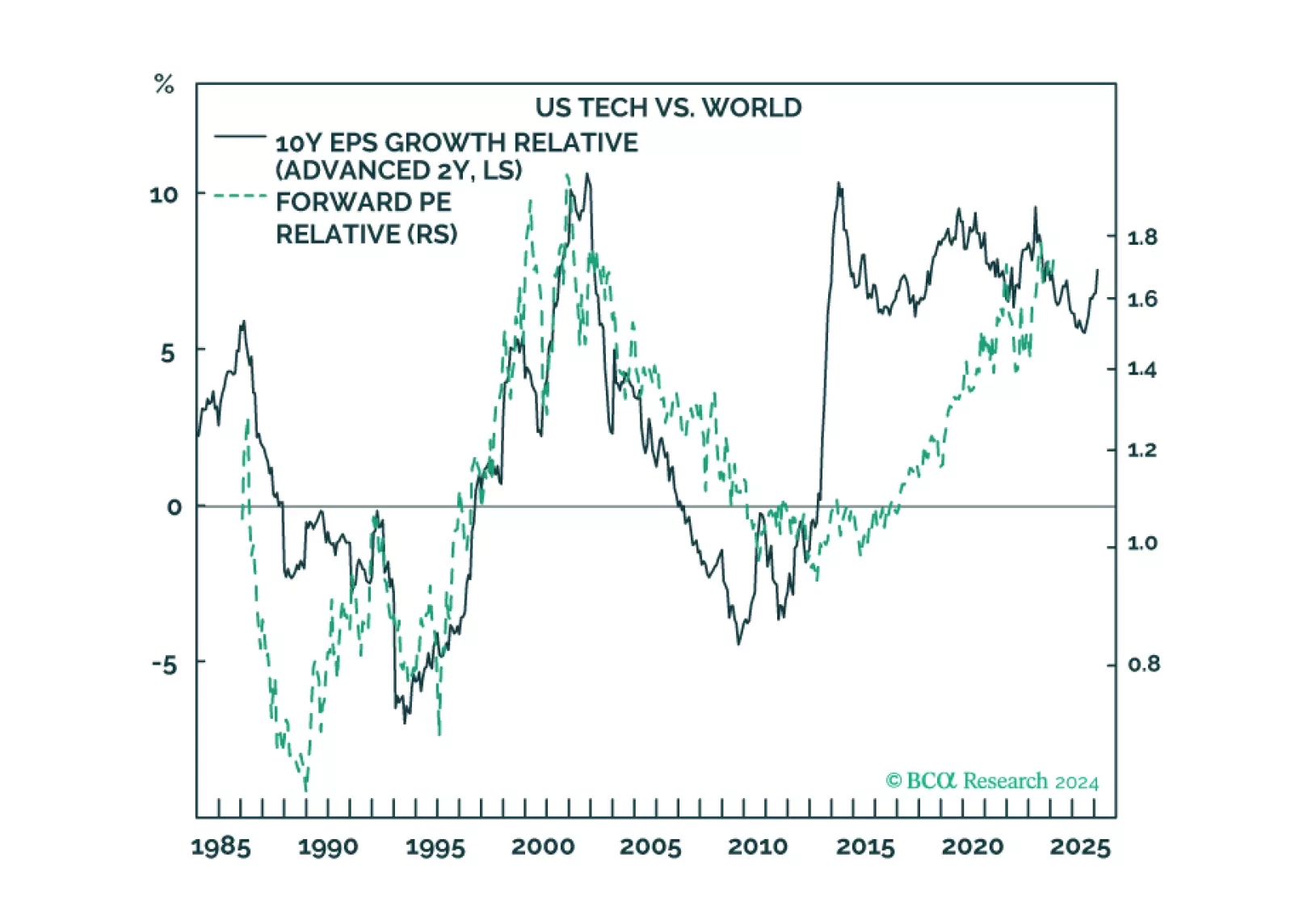

Our Valentine’s Day report is about two love stories: the infatuation with US tech and China’s infatuation with housing. We describe how these love stories will end, and why Europe could be the winner.