United States

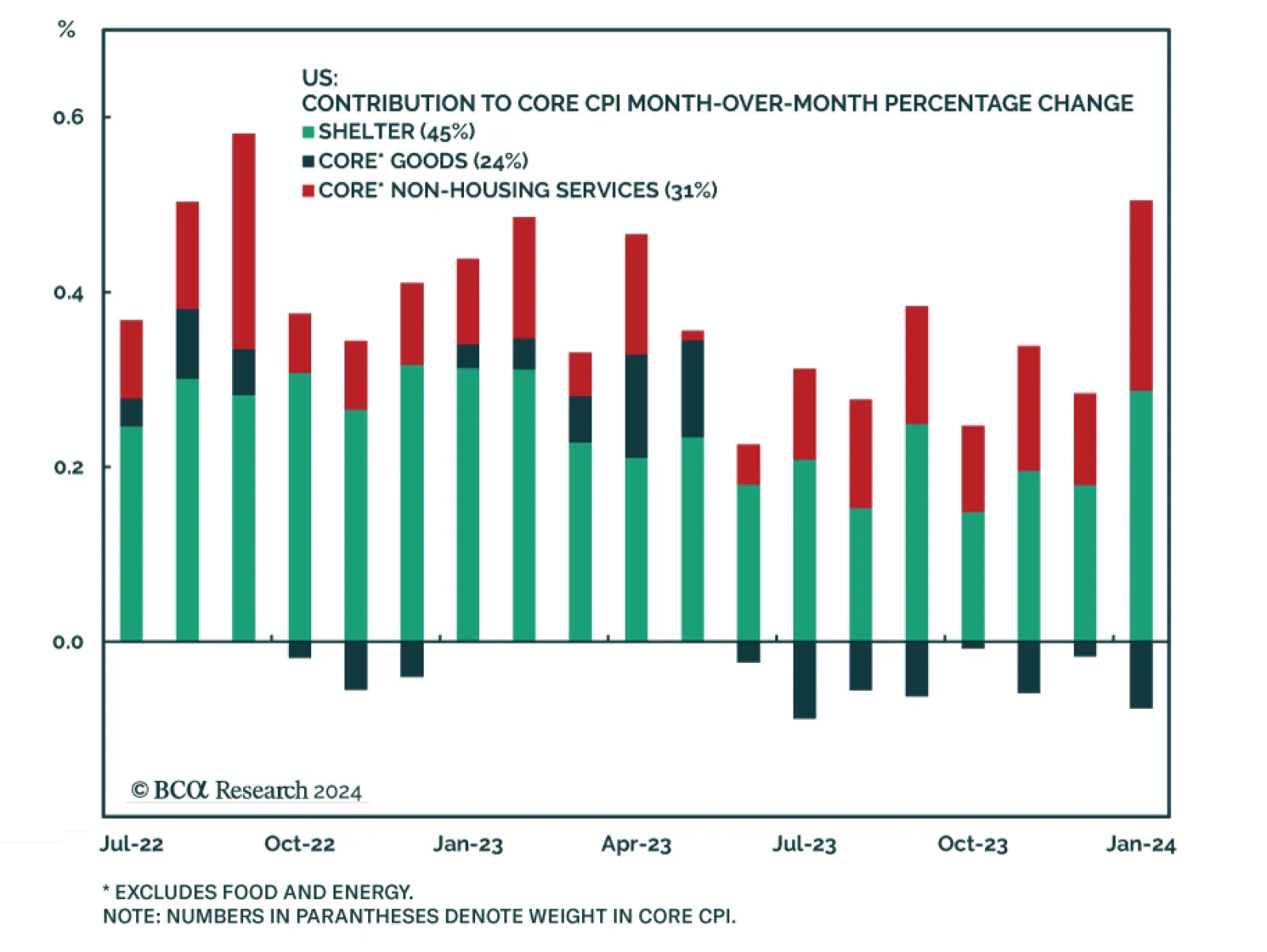

The US CPI report for January showed inflation did not cool as much as anticipated. Headline inflation accelerated from 0.23% to 0.31% on a month-over-month basis, higher than anticipations of 0.2% m/m. It fell from 3.4% to 3.1% on a year-over-year basis,…

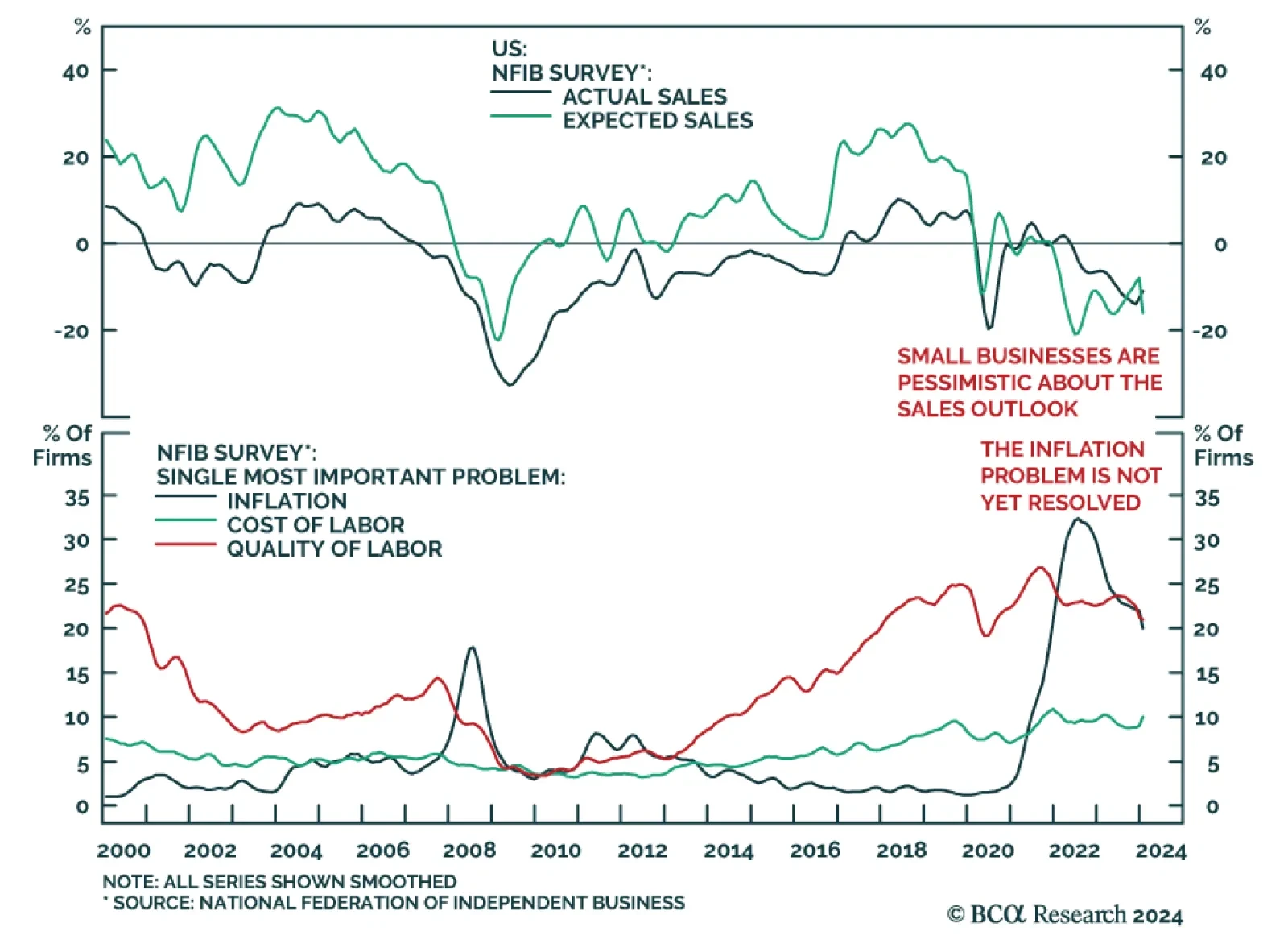

We highlighted in a recent Insight that positive economic surprises are prompting economists to revise up their US economic growth expectations. The Goldilocks narrative is supporting the rally in risk assets. However, results of the January NFIB survey…

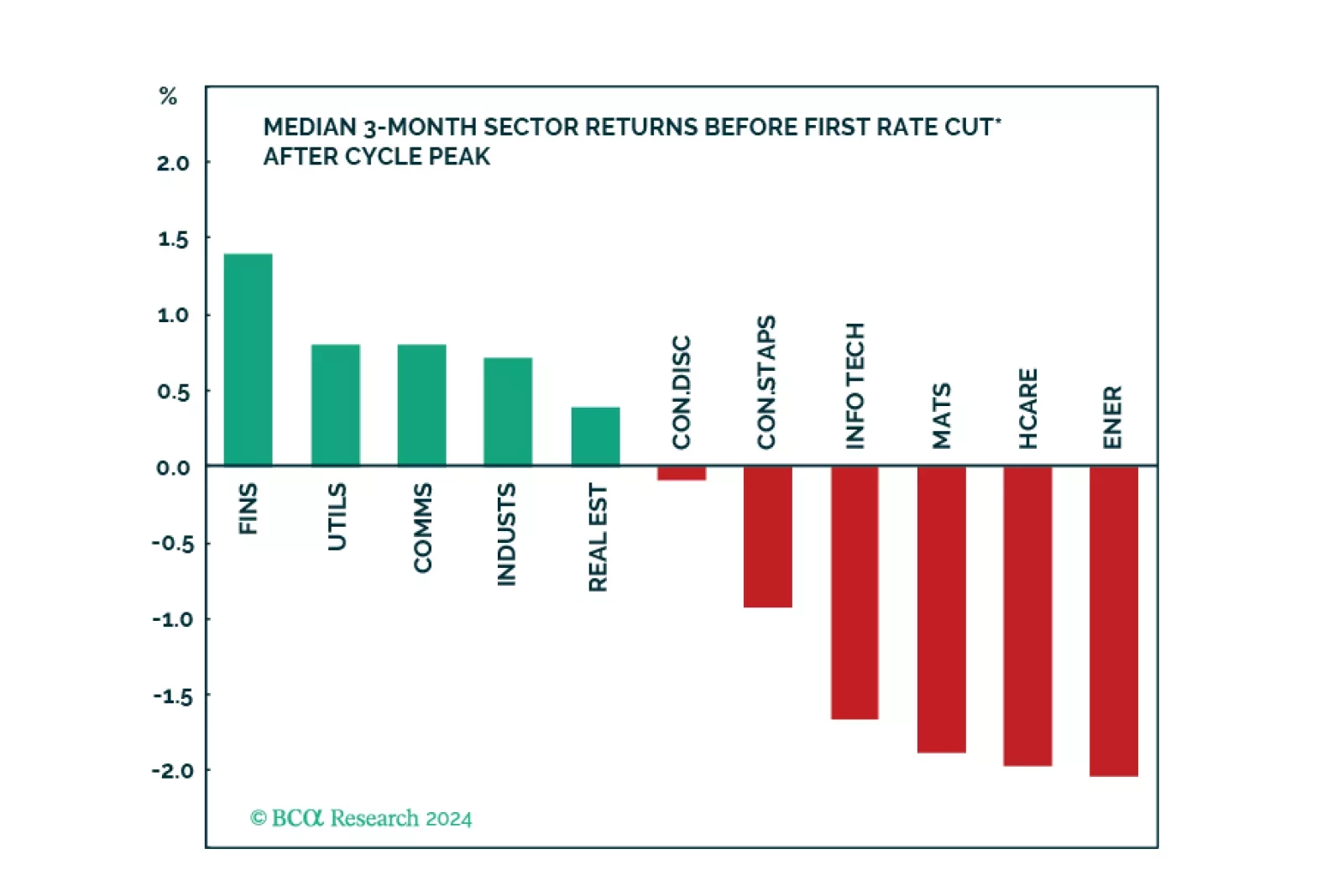

BCA Research’s US Equity Strategy service created a sector selection scorecard based on performance of sectors under various macroeconomic regimes. The current macroeconomic backdrop is characterized by the following regimes: Impending rate…

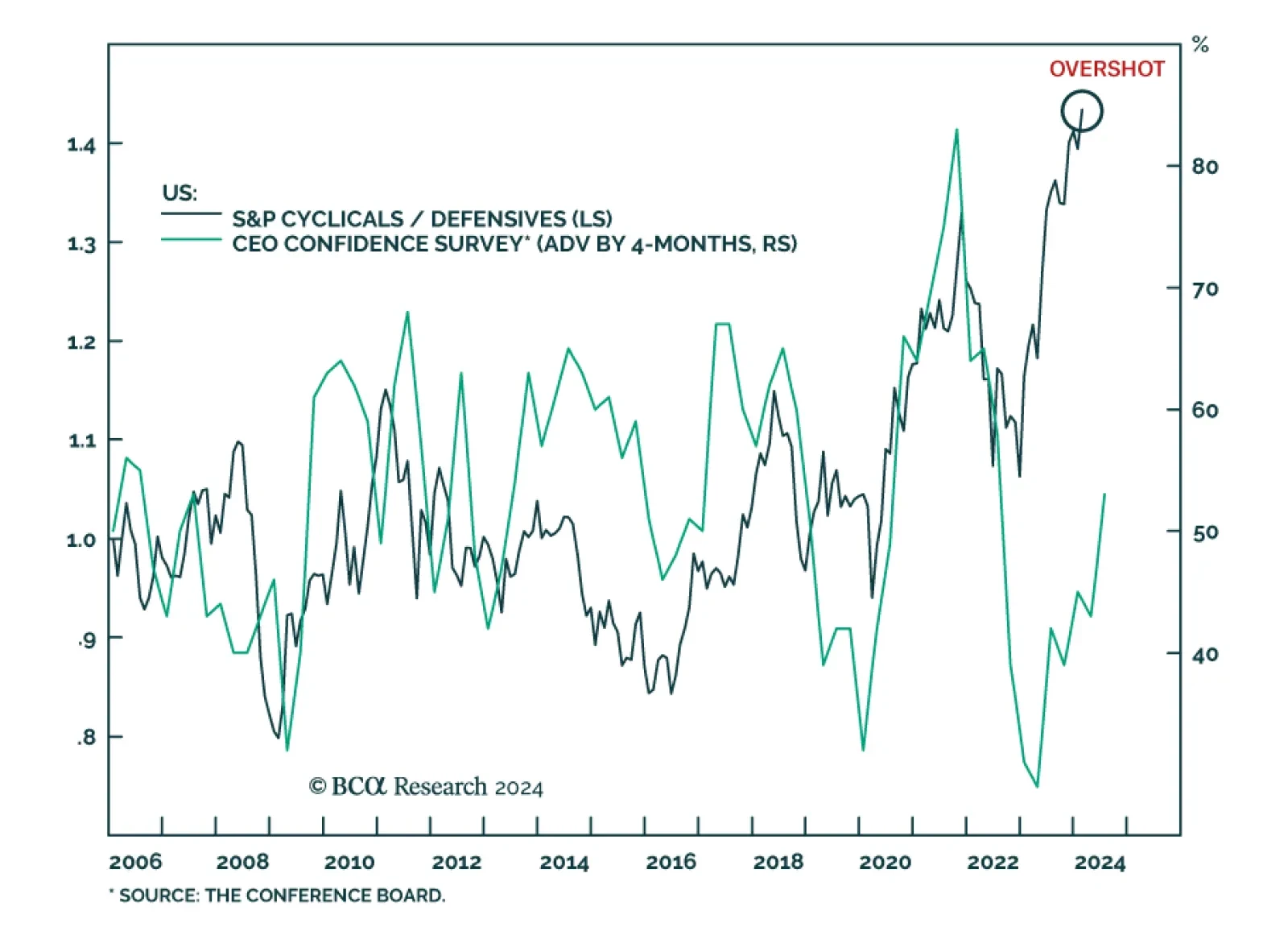

Results of the US Conference Board’s latest quarterly survey show an improvement in sentiment among business leaders. The CEO Confidence measure rose above 50 for the first time in two years – indicating that optimists now outnumber pessimists. CEOs are more…

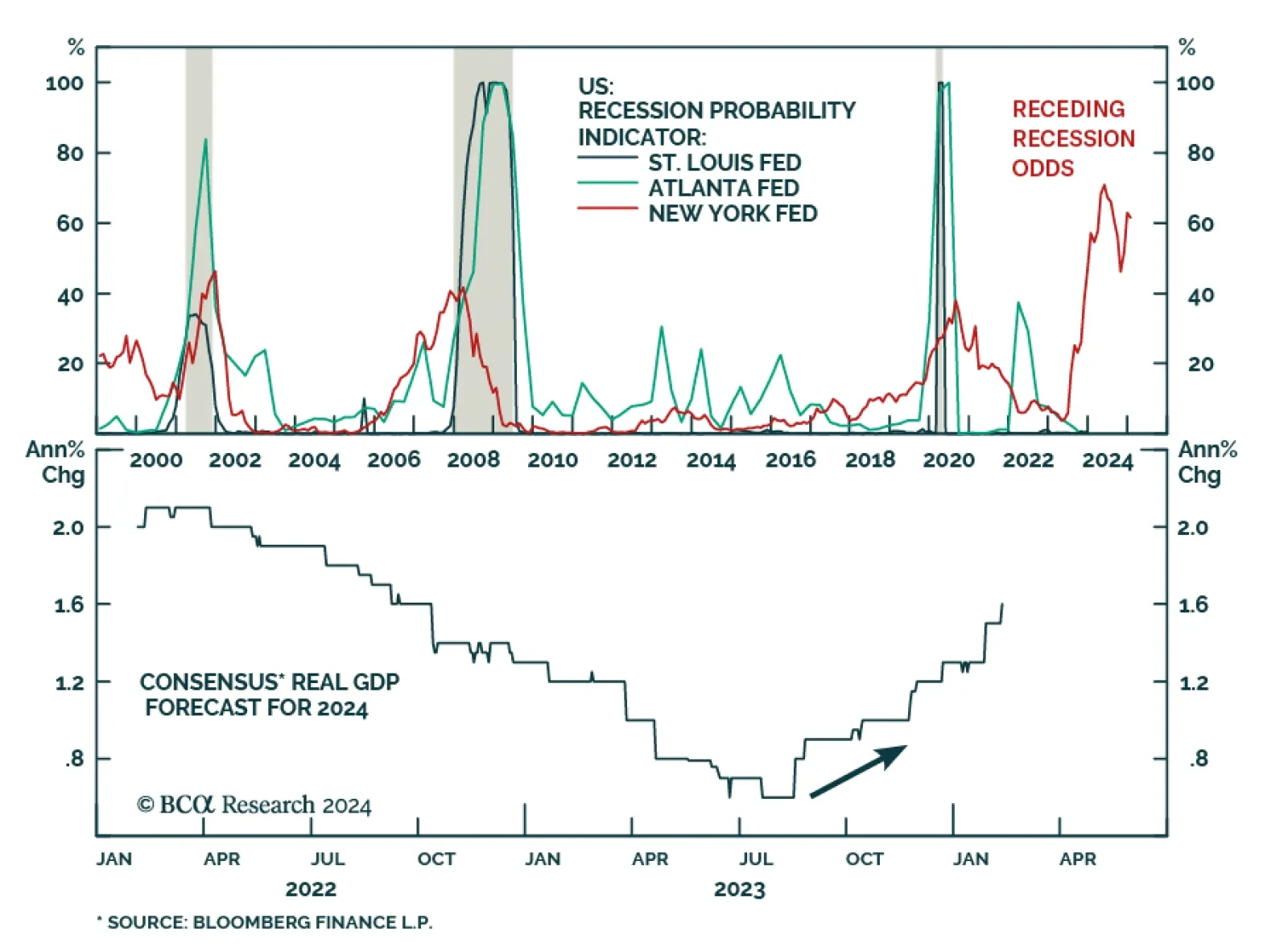

Expectations that the Fed will successfully deliver a soft landing for the US economy remains the dominant narrative. Since August, economists have been revising up their 2024 US GDP forecasts with the consensus now anticipating US growth to clock in at 1.6%…

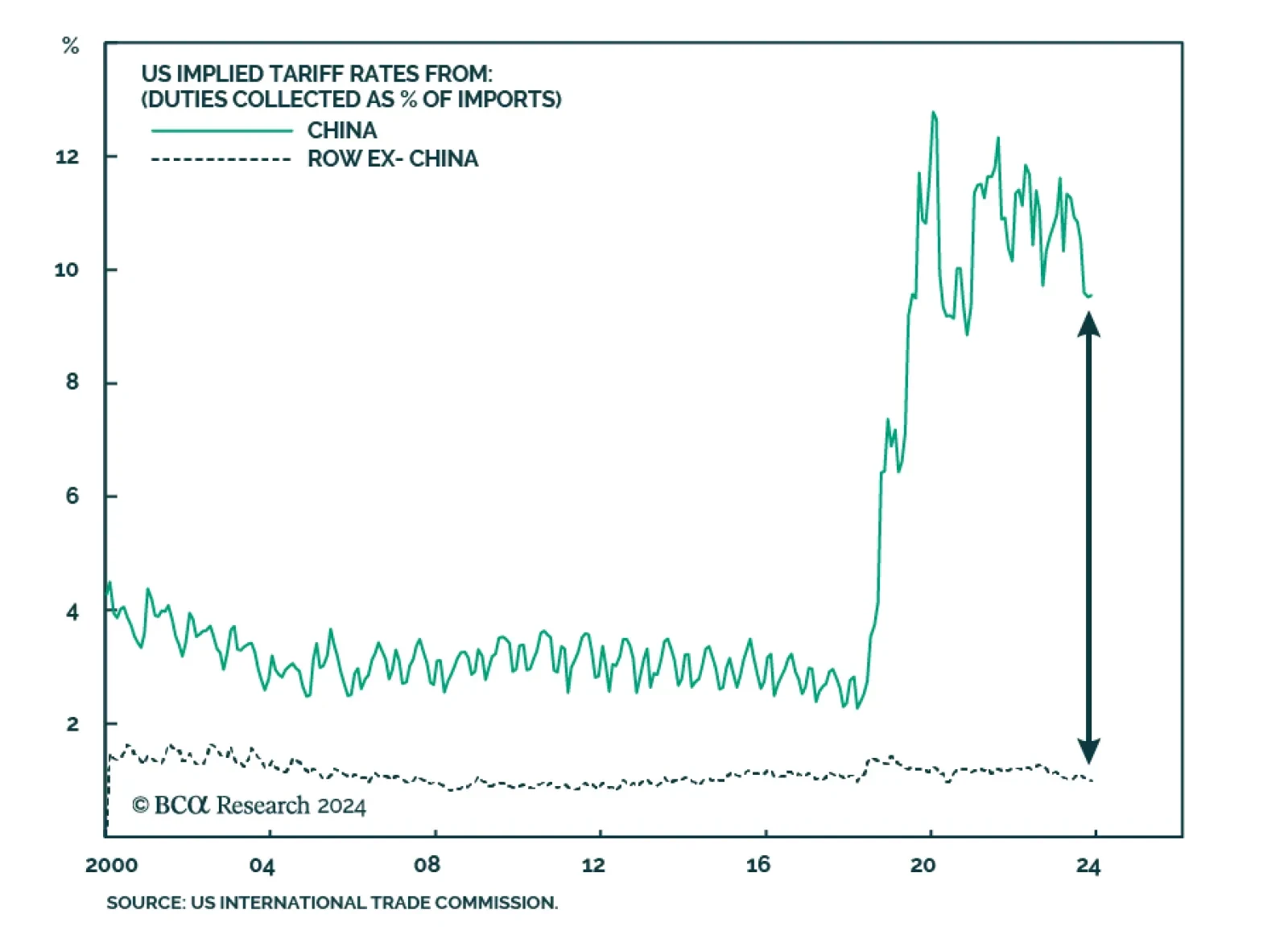

The Chinese economy continues to face deflationary pressures, reducing the odds that any intervention-driven rebound in equities will be sustained. In addition, our Geopolitical strategists have argued that US-China relations will not give investors good…

We created a sector selection scorecard based on performance of sectors under various macroeconomic regimes while taking into consideration revisions to expected earnings growth and valuations in a historical context. Our total sector selection scorecard suggests overweighting defensives such as Utilities, and Consumer Staples, and underweighting cyclicals such as Consumer Discretionary, Industrials, and Financials. Considering this analysis, we have adjusted our sector positioning accordingly.

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.

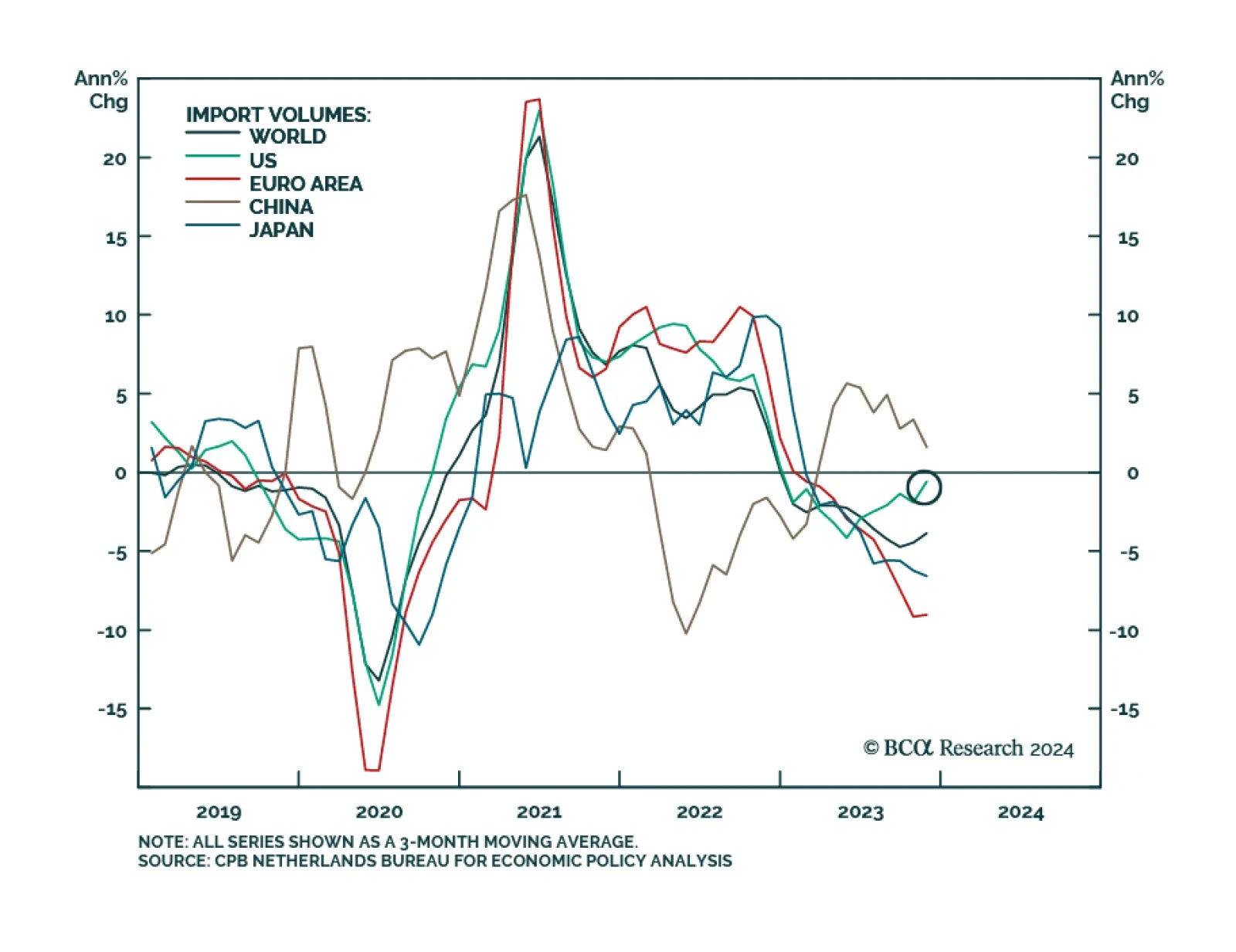

Over the past few months we have been highlighting that there are some budding signs of a recovery in global manufacturing activity. Most notably, the new orders-to-inventories ratio of Sweden’s manufacturing PMI has been rebounding. To the extent that Sweden…

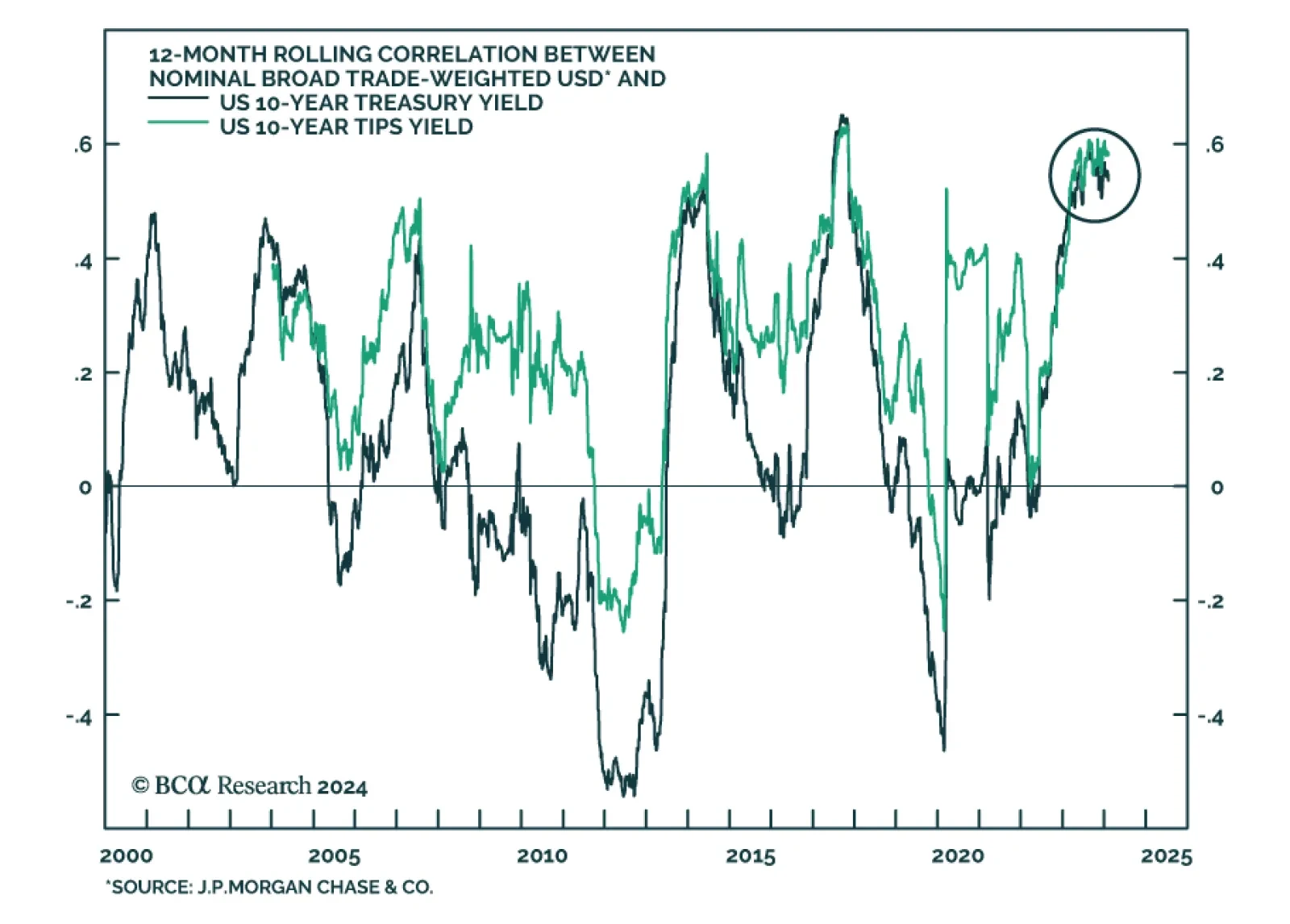

Our Emerging Markets team believes that the risk-reward profile of the US dollar remains very attractive. First, if US growth stays robust, US interest rate expectations will rise because rate cuts priced in will not be realized. Rising interest rates will…