United States

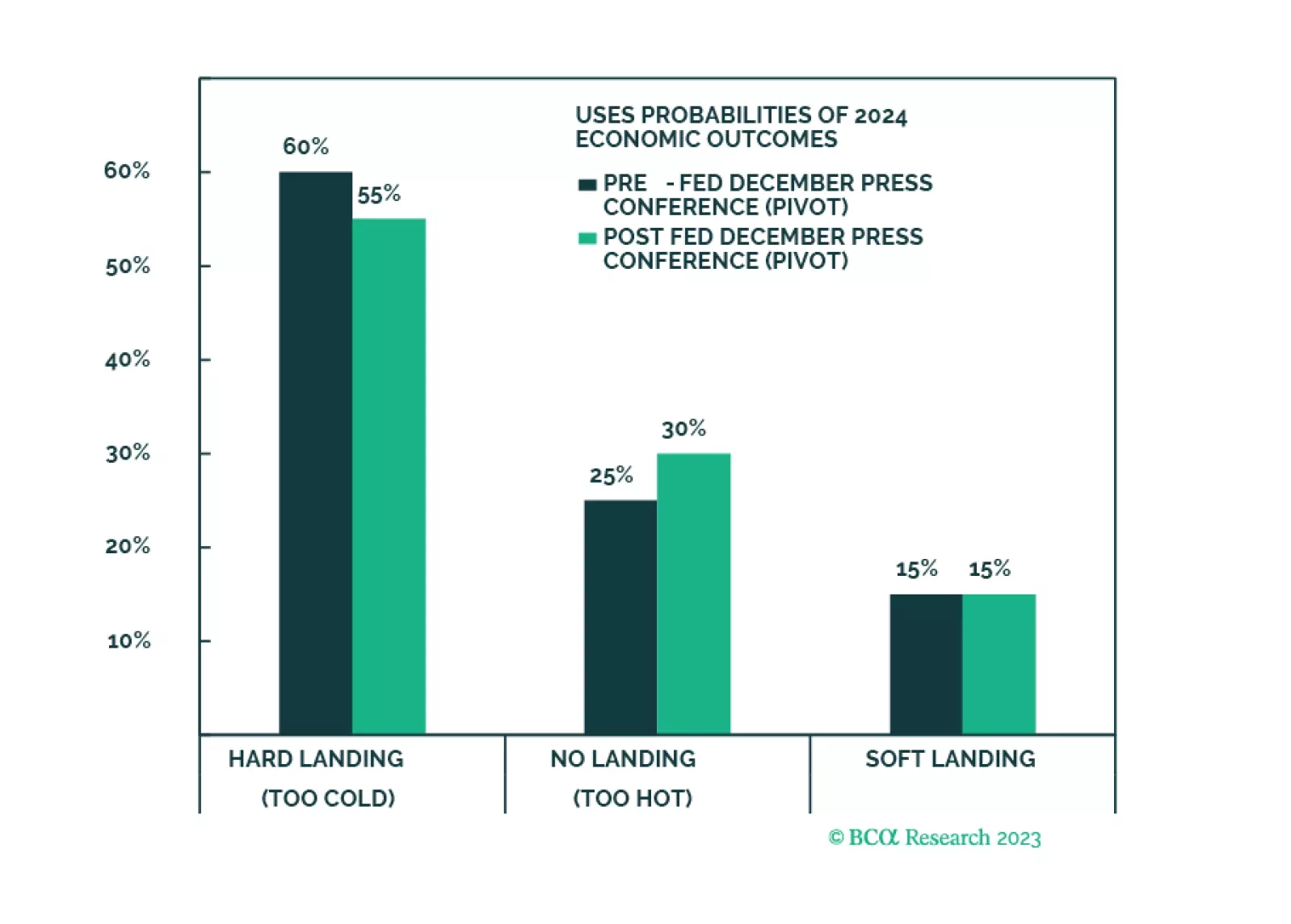

A soft landing can be achieved but not maintained. We are cutting our tactical recommendation on stocks from overweight to neutral and scaling back our long-duration stance.

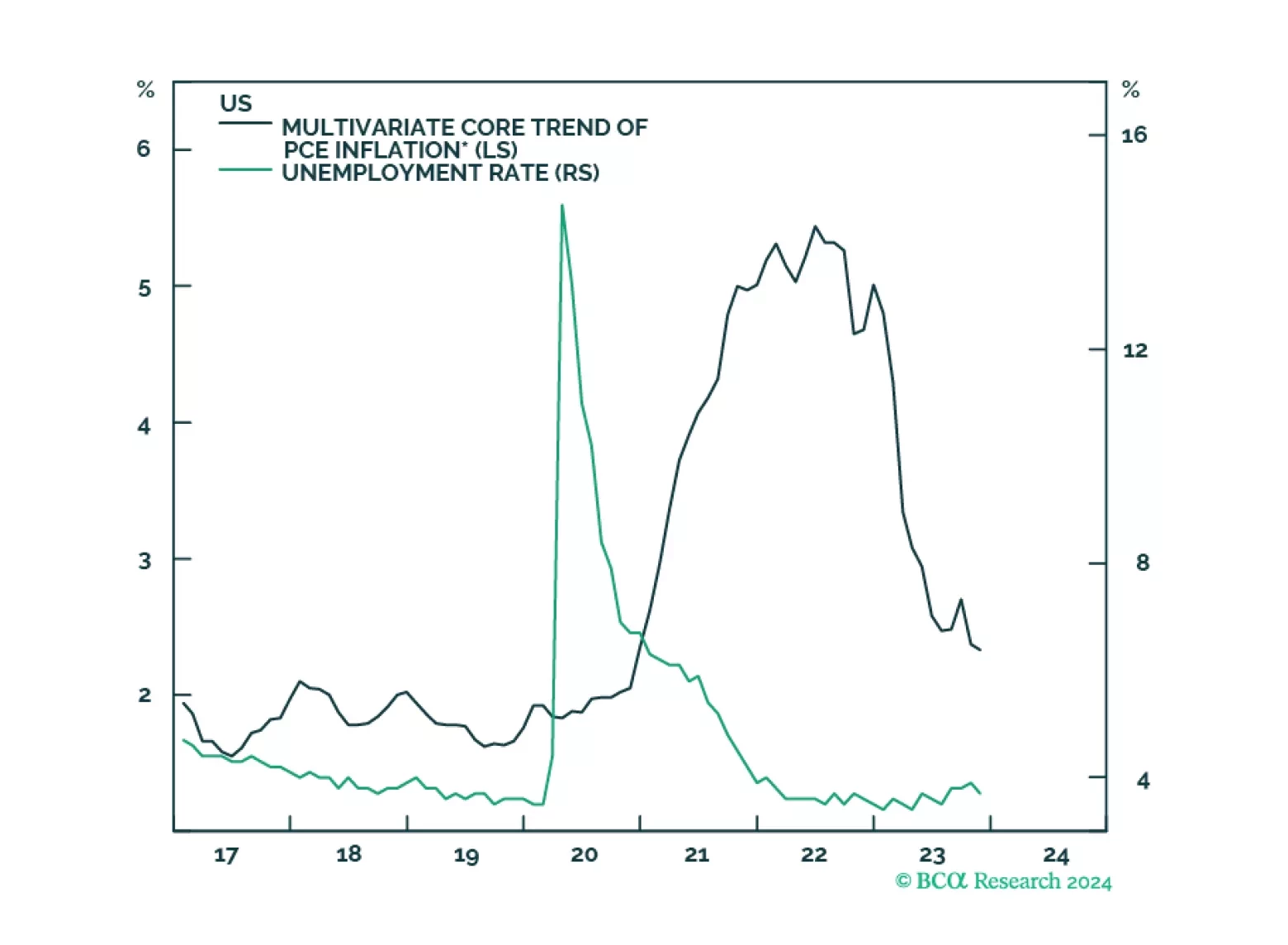

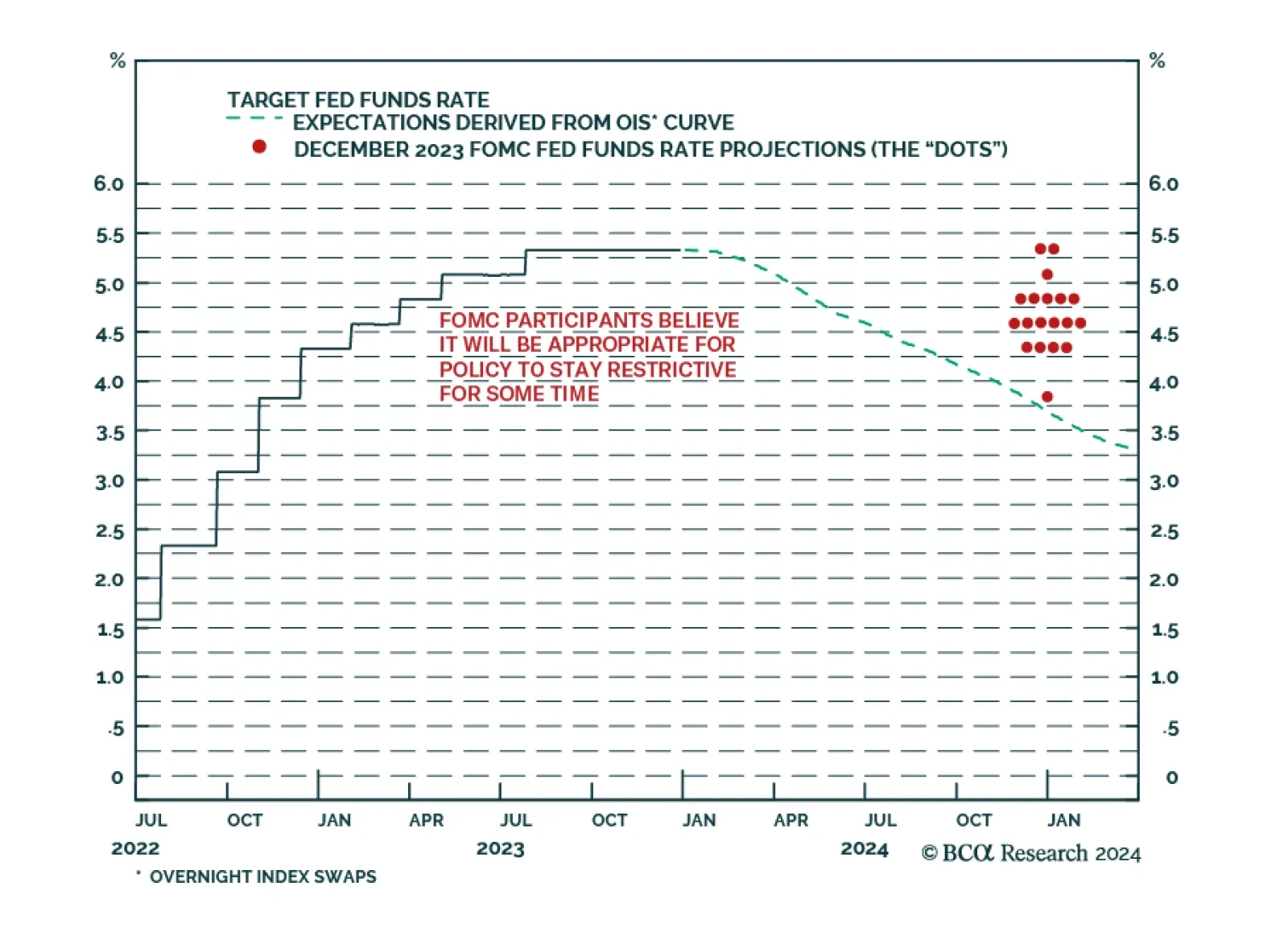

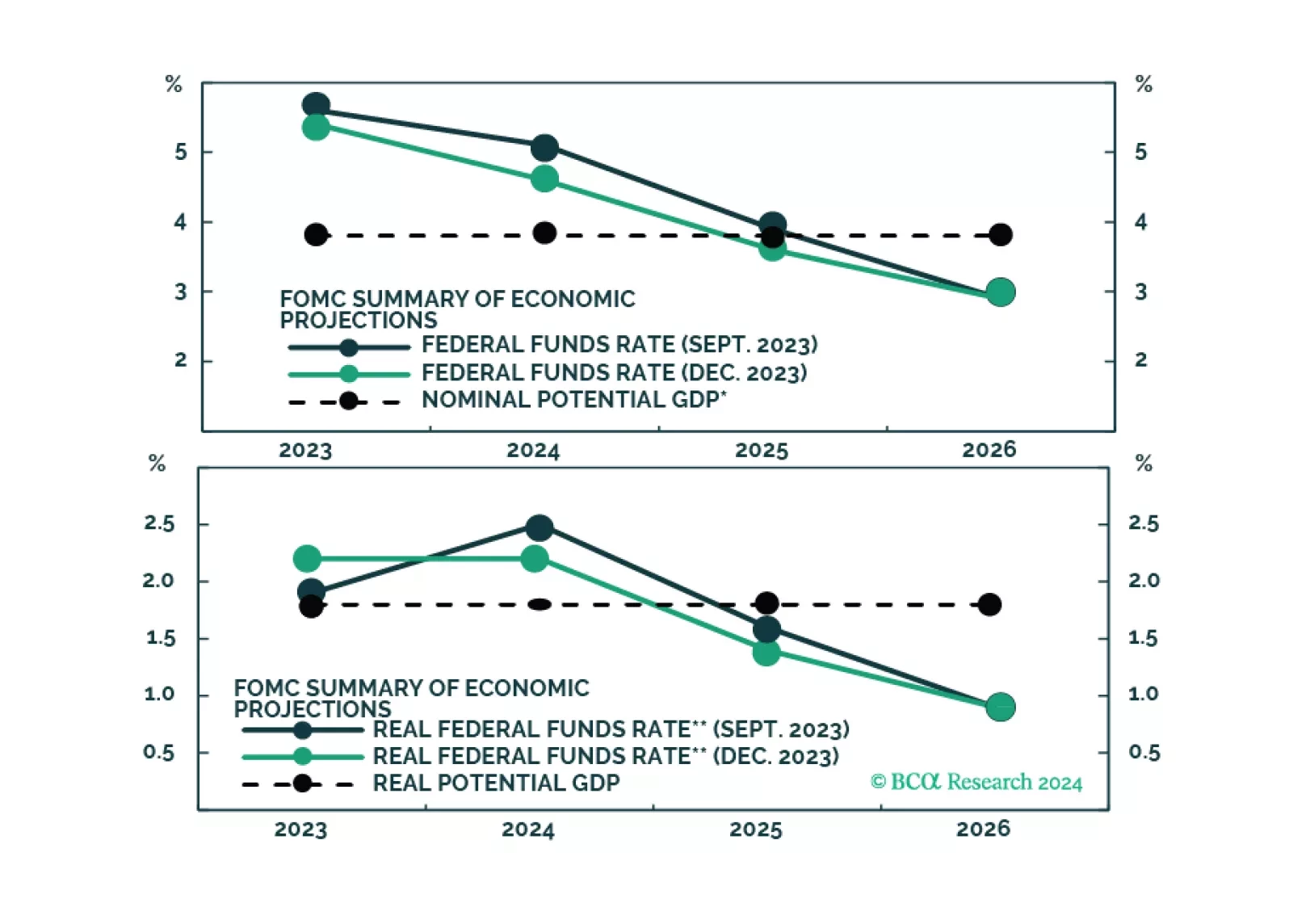

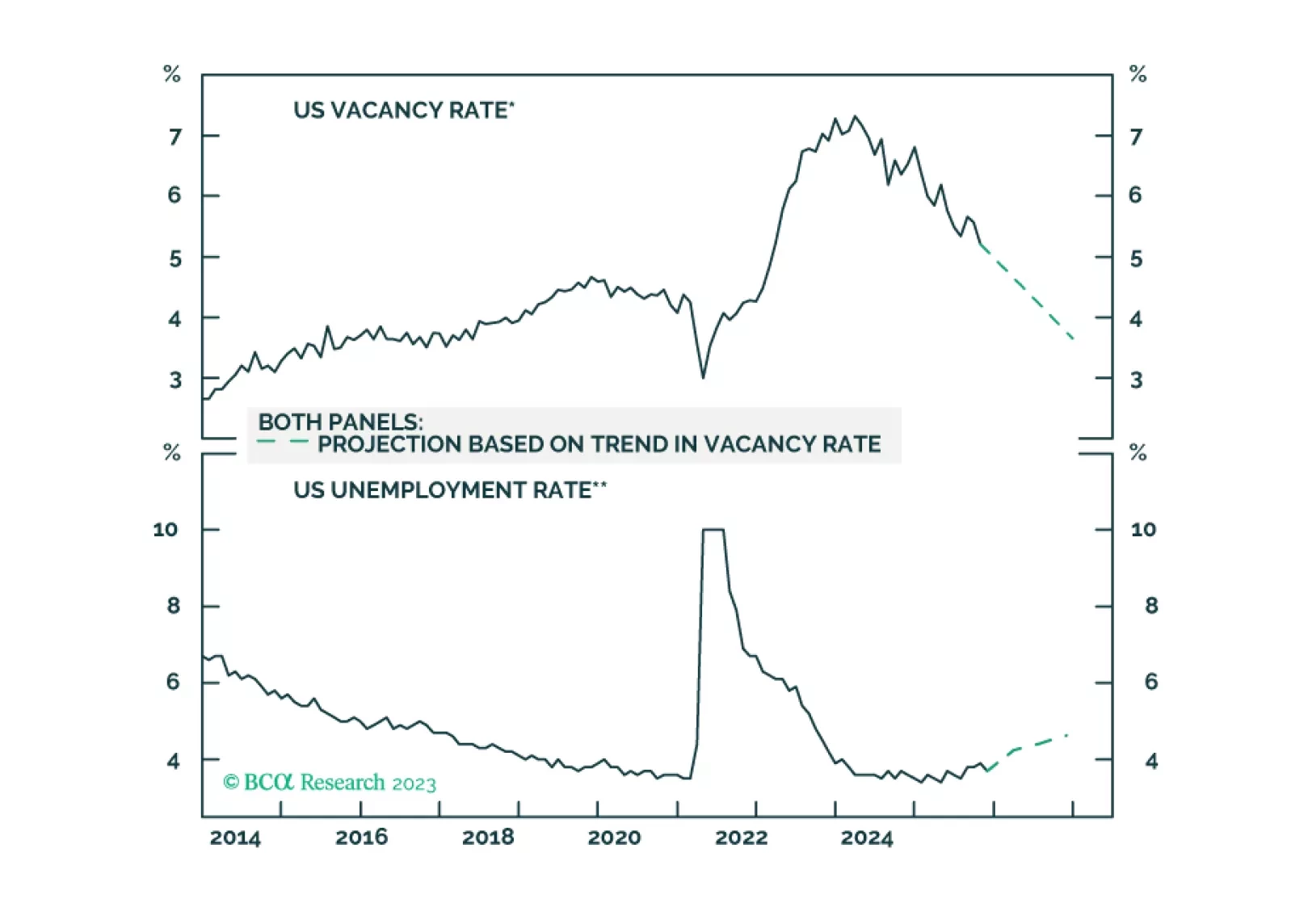

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

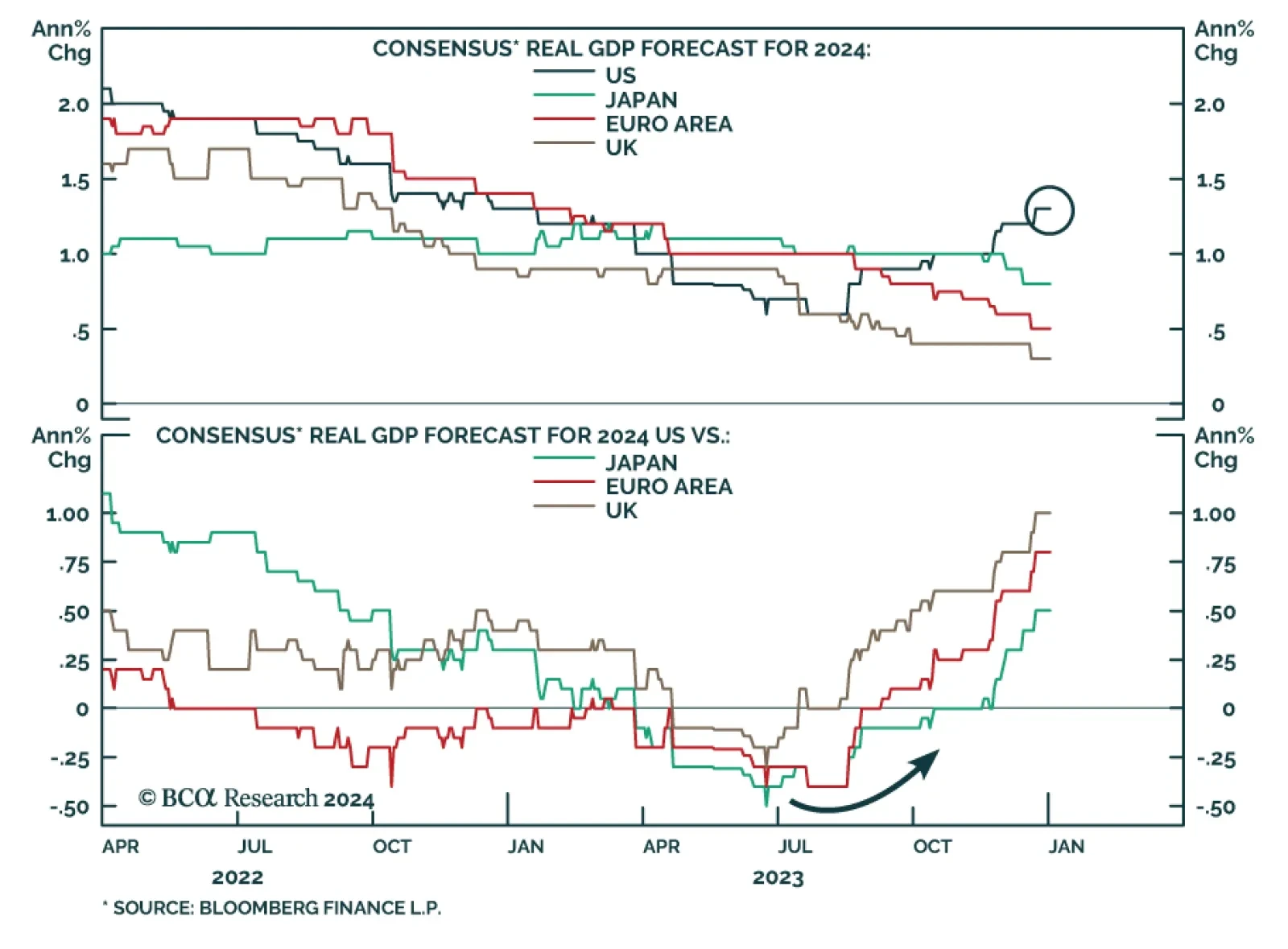

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

In this final note for the year, we take profits and close several long-term investment positions: Overweights in Insurance and Commercial Services, and underweights in Utilities, and Retail and Commercial REITs.

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.