United States

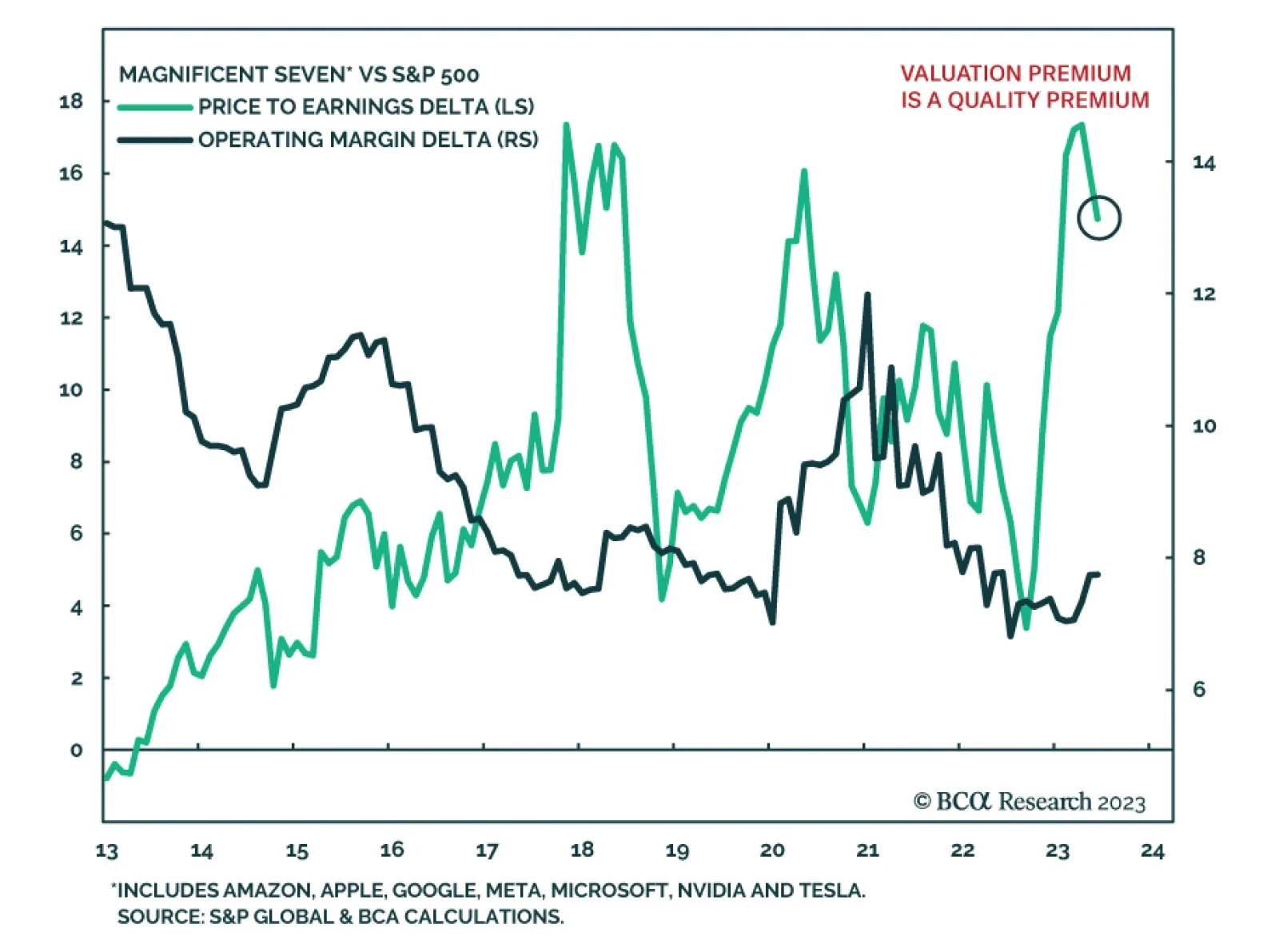

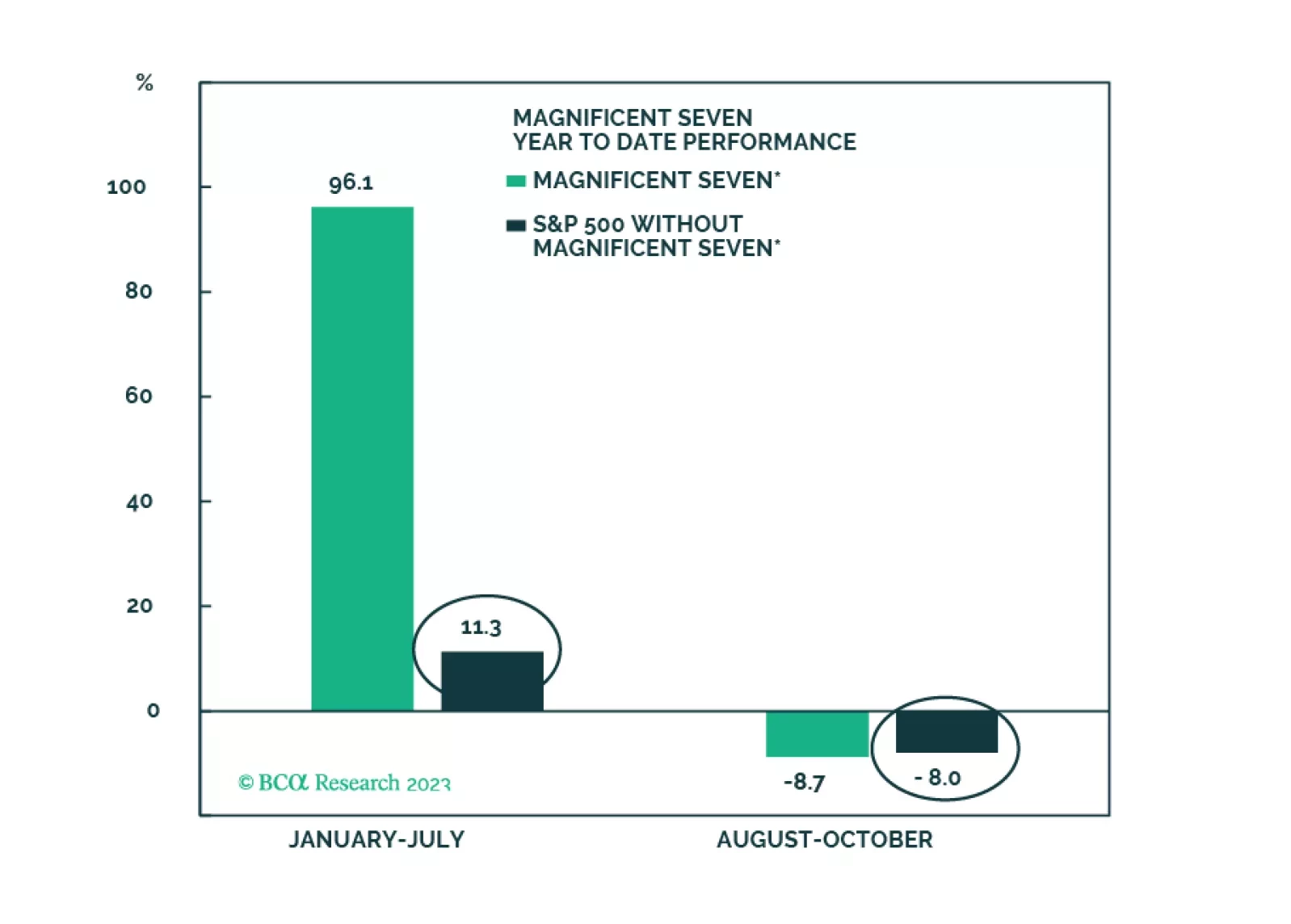

The Magnificent Seven constitute 26.7% of the S&P 500 and are the cohort responsible for the majority of S&P 500 returns this year. Fundamentals, and, specifically, the profitability of the group are behind the strong performance. If we compare the…

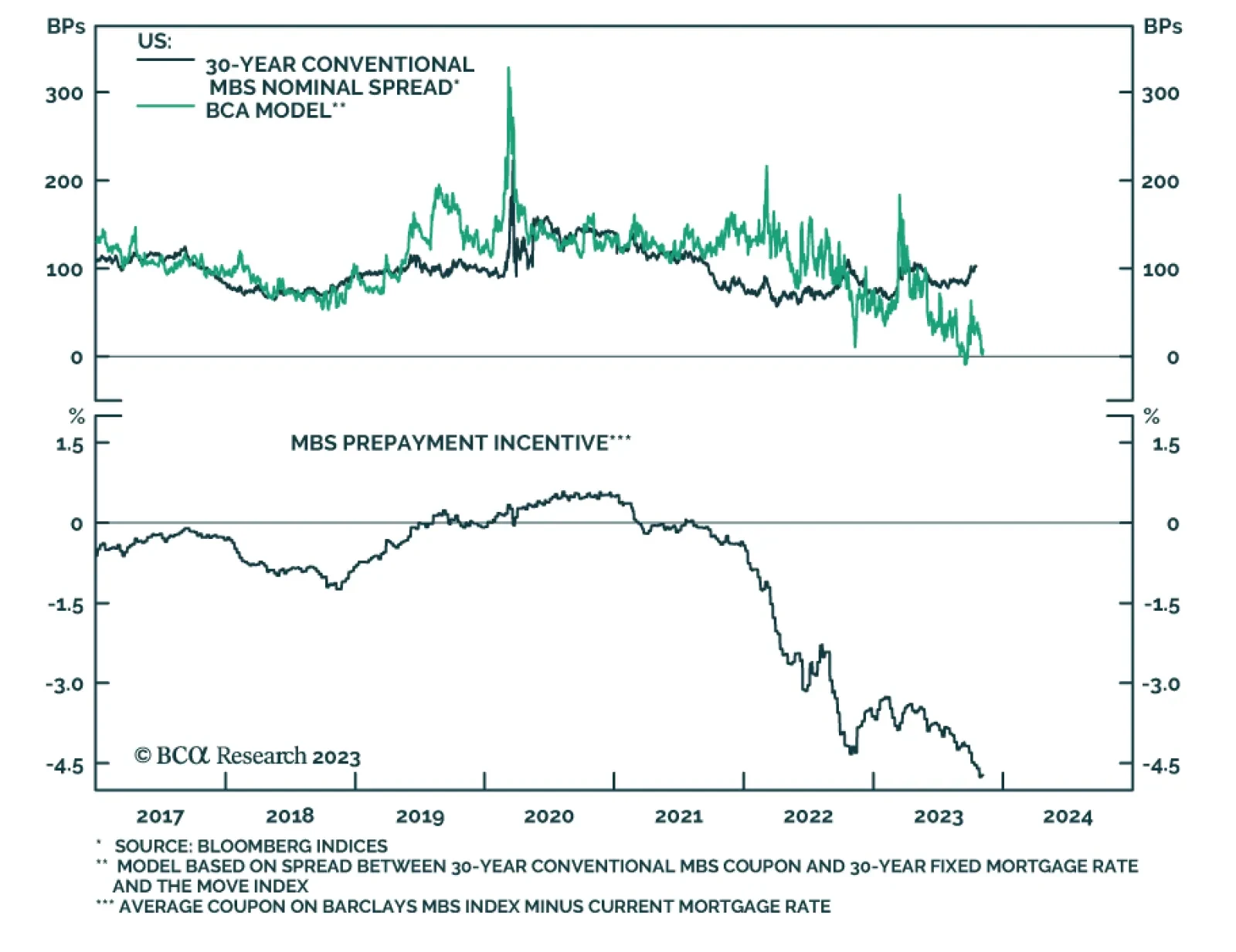

According to BCA Research's US Bond Strategy service, the current spate of MBS underperformance has created a lot of value in the sector. Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 64 basis points in October,…

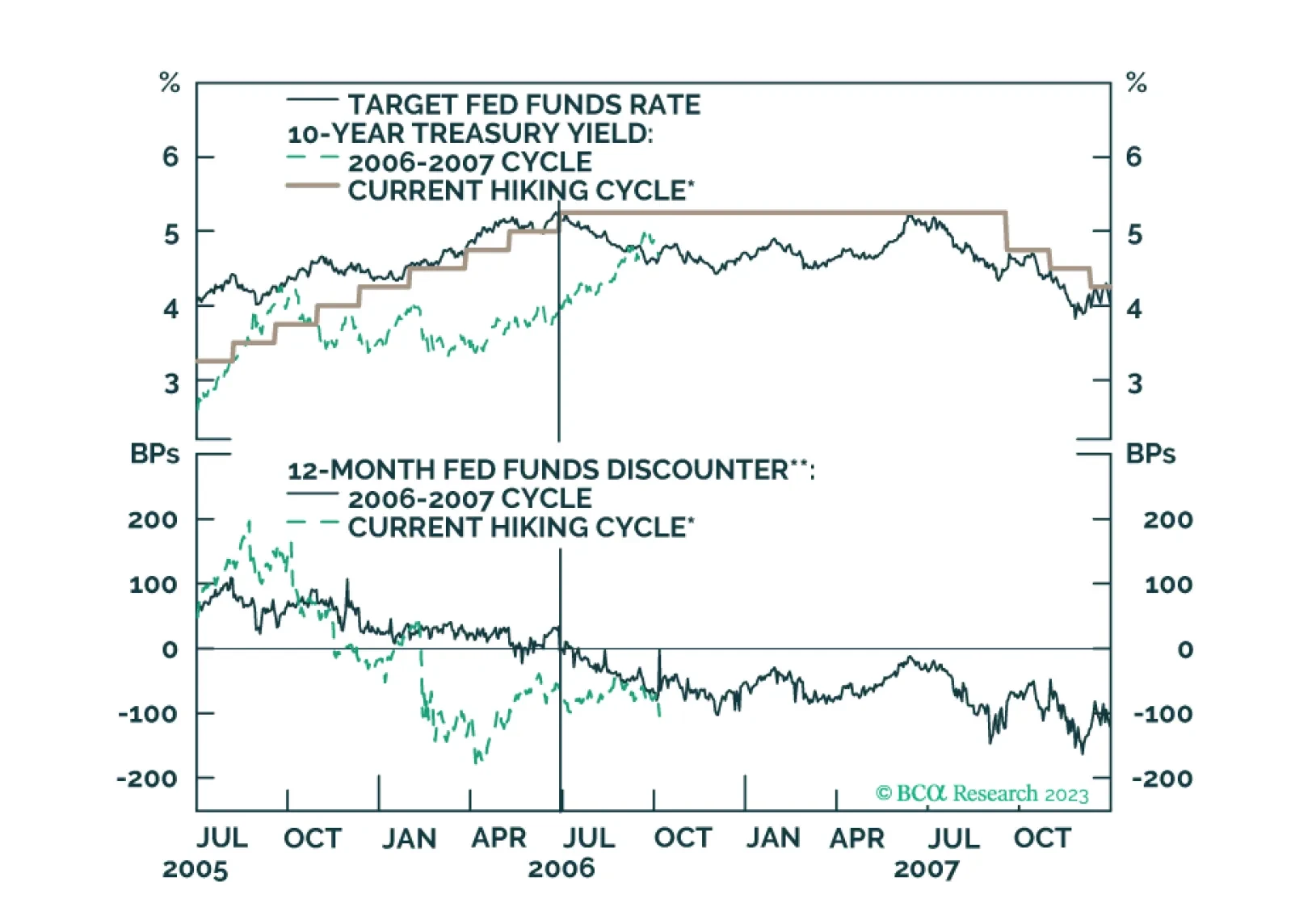

The Vicious Troika remains a long-term threat, but over the short term, rates will likely have another leg down on growth concerns, offering support to equities, which are now fairly valued and are no longer overbought. Longer-term outlook remains negative. The Magnificent Seven will likely lead a tactical rebound. Overweight Growth vs Value and FSemis.

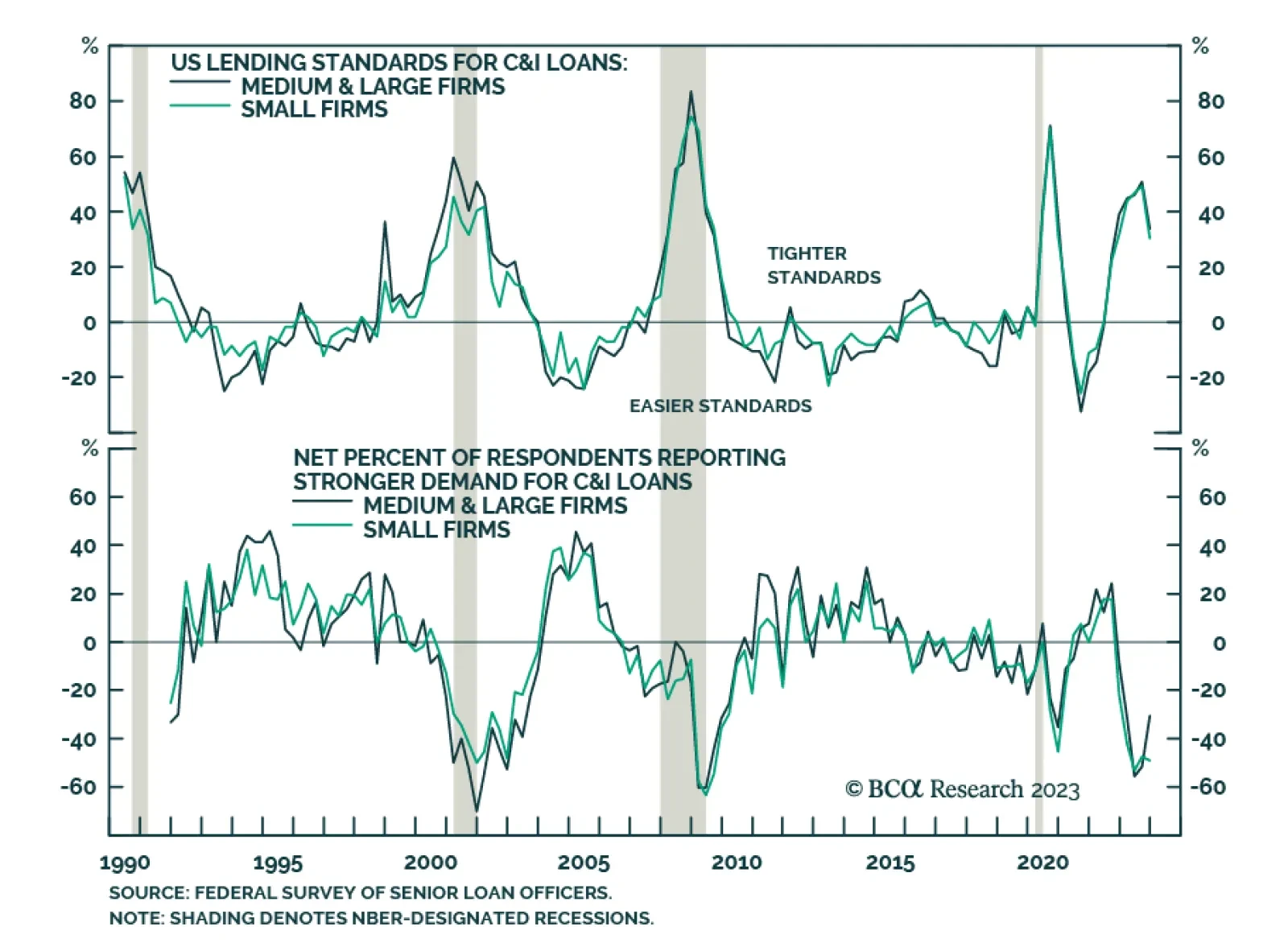

The US Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) reveals that US banks continued to tighten lending standards for commercial and industrial (C&I), commercial real estate (CRE), residential real estate (RRE) except government residential…

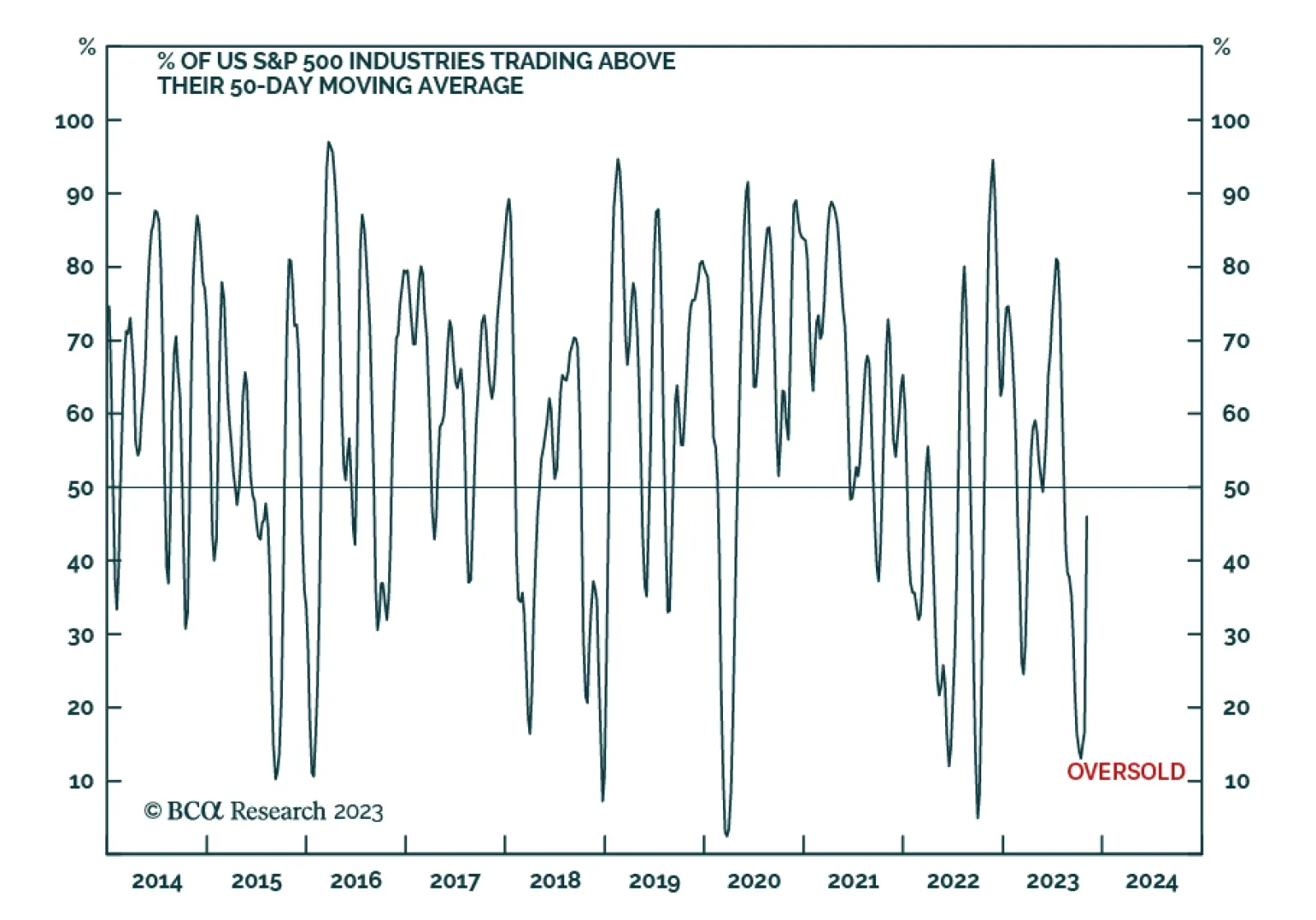

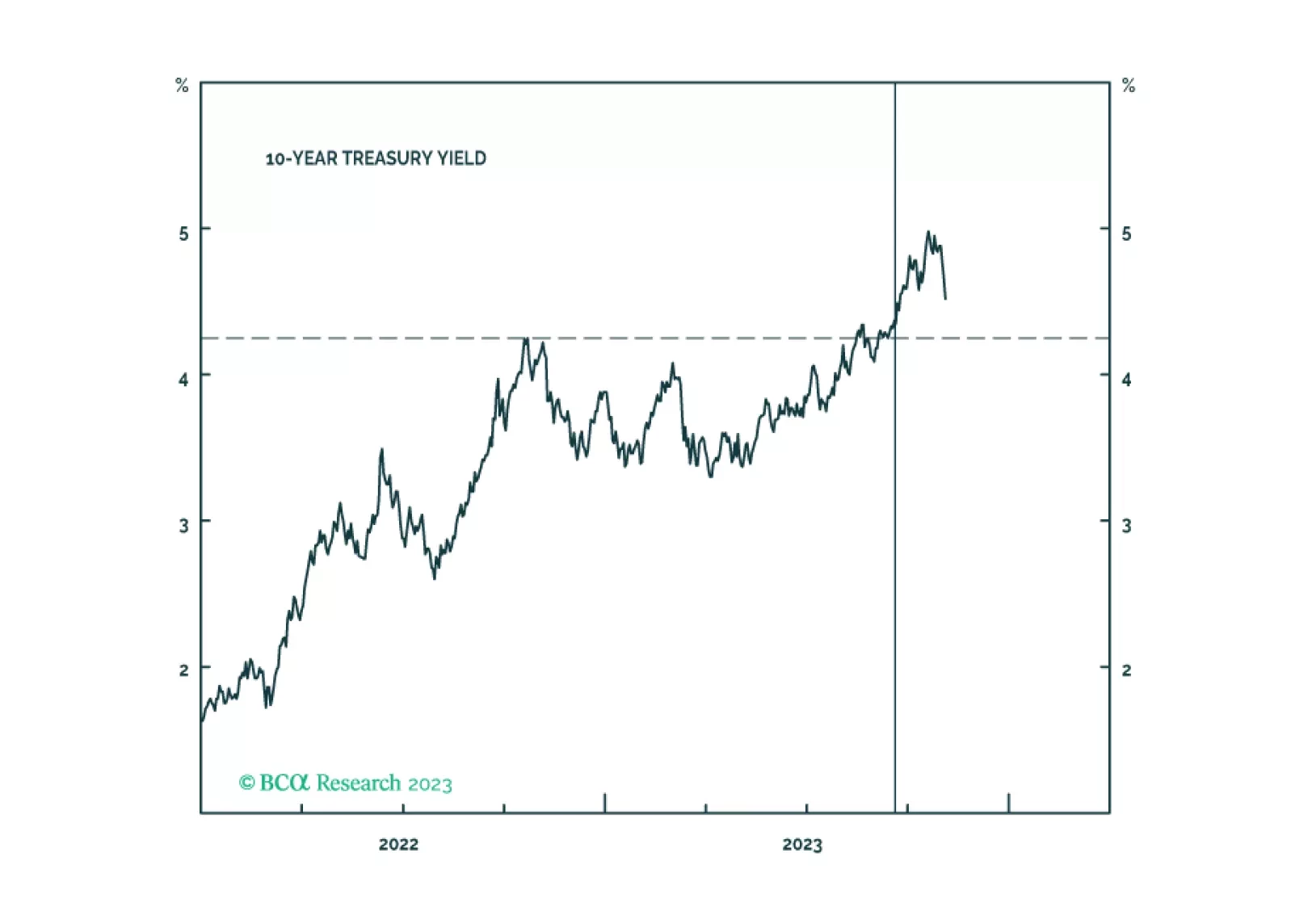

The S&P 500's 5.9% rally last week marks the greatest weekly price gain since November 2022. This sharp increase comes after a 10.3% selloff between the start of August and late-October, which put the benchmark in correction territory. A 36bps drop in the…

Our Portfolio Allocation Summary for November 2023.

We consider several uncertainties in this week’s report, from the interest rate outlook to the source of the mountain of cash households have amassed since the pandemic began. We have not adjusted our tactical asset-allocation recommendations but will do so soon to align with the defensive cast of our cyclical recommendations.

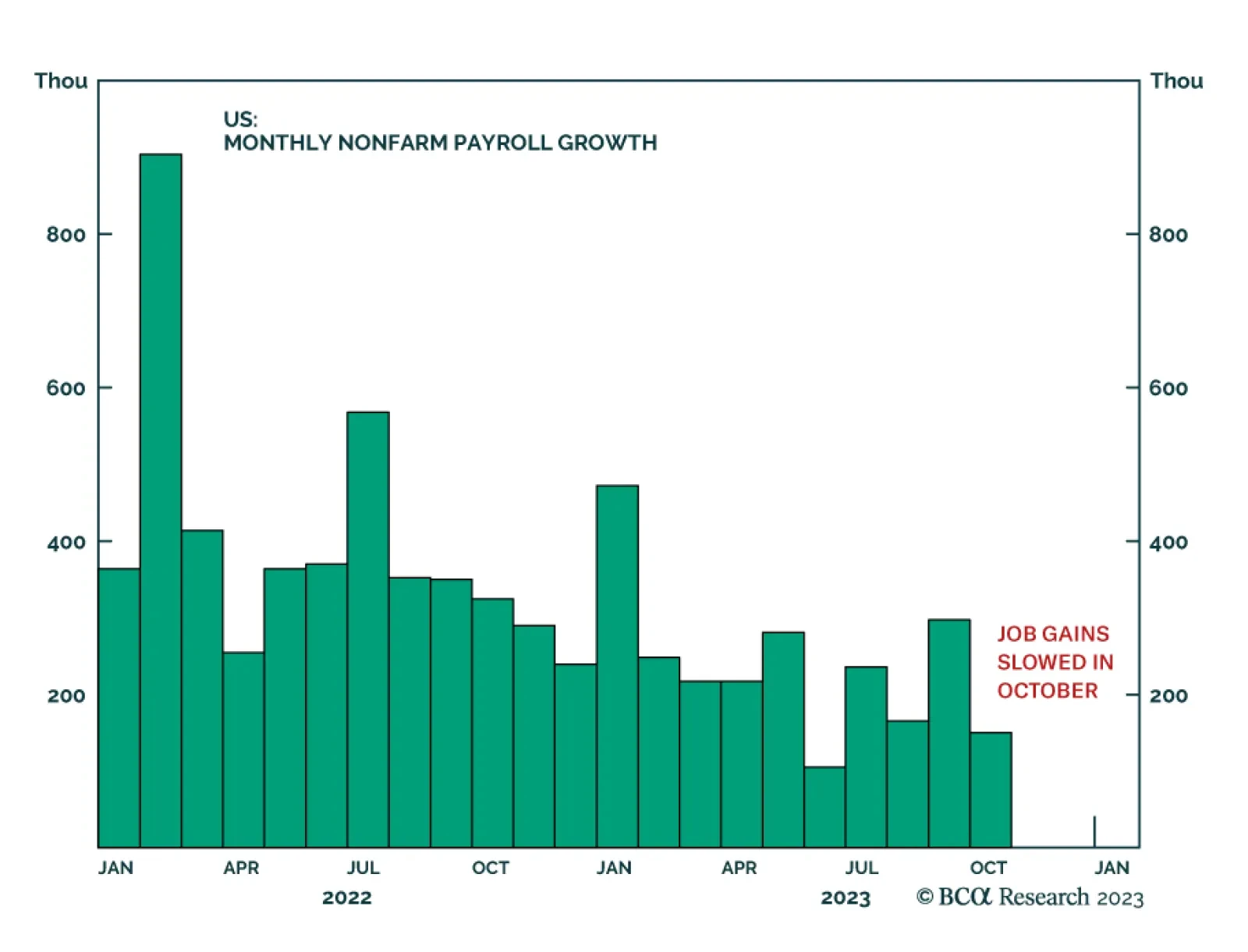

The US Nonfarm Payroll report indicates that labor market conditions cooled in October. The 150 thousand increase in payroll employment fell below expectations of 180 thousand and marks a slowdown from the 297 thousand increase in September. Moreover, the…

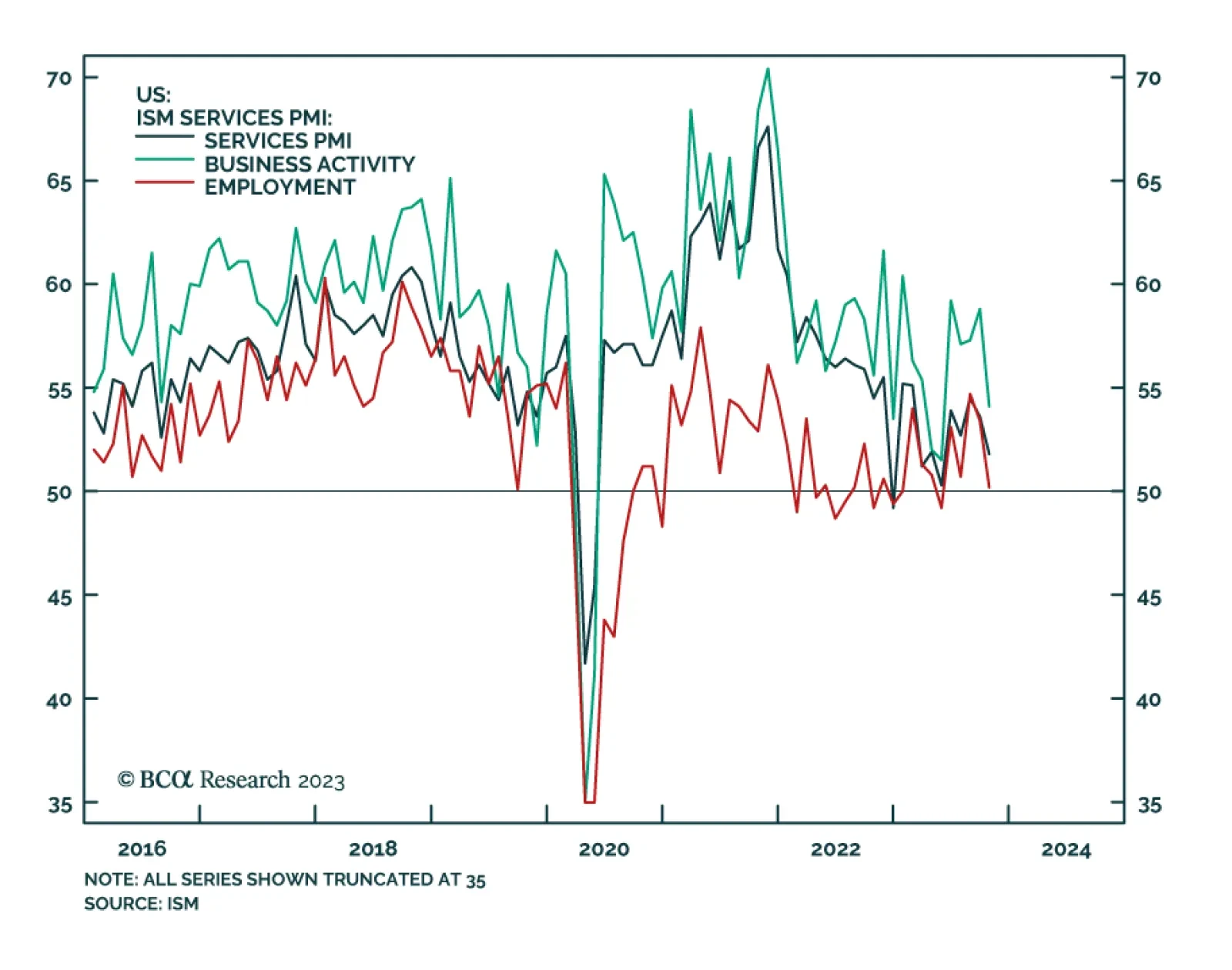

The US ISM PMI delivered a disappointing signal about service sector activity in October. The headline index fell from 53.6 to 51.8 – marking a sharp slowdown in activity and falling below expectations of a much more muted decline to 53.0. The index is now at…

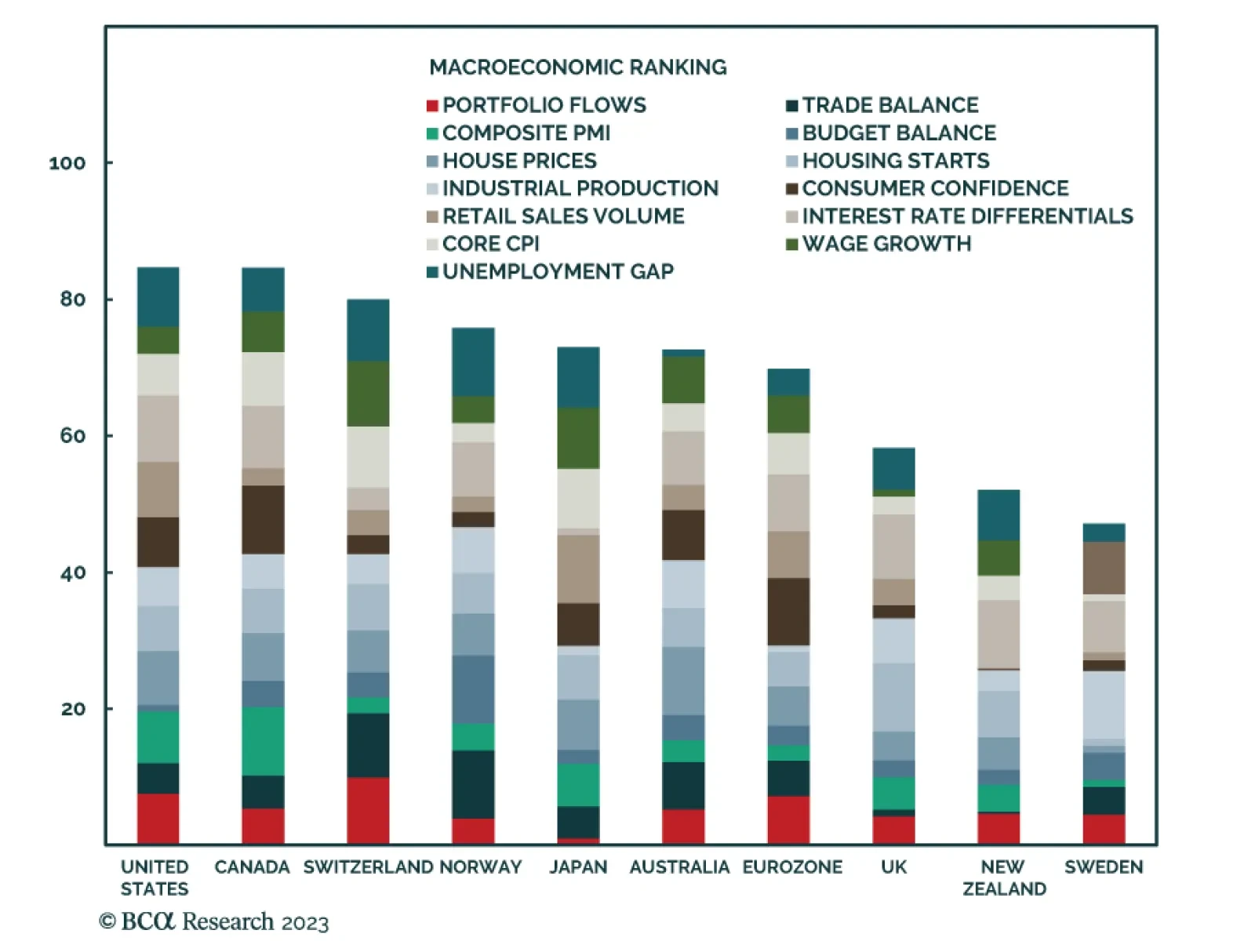

The FX G10 attractiveness model continues to favor the US dollar, but the tide could shift in the coming weeks. Currencies such as the NOK, CHF and even CAD have been rising in rankings in recent months. Using an aggregate of economic and financial…