United States

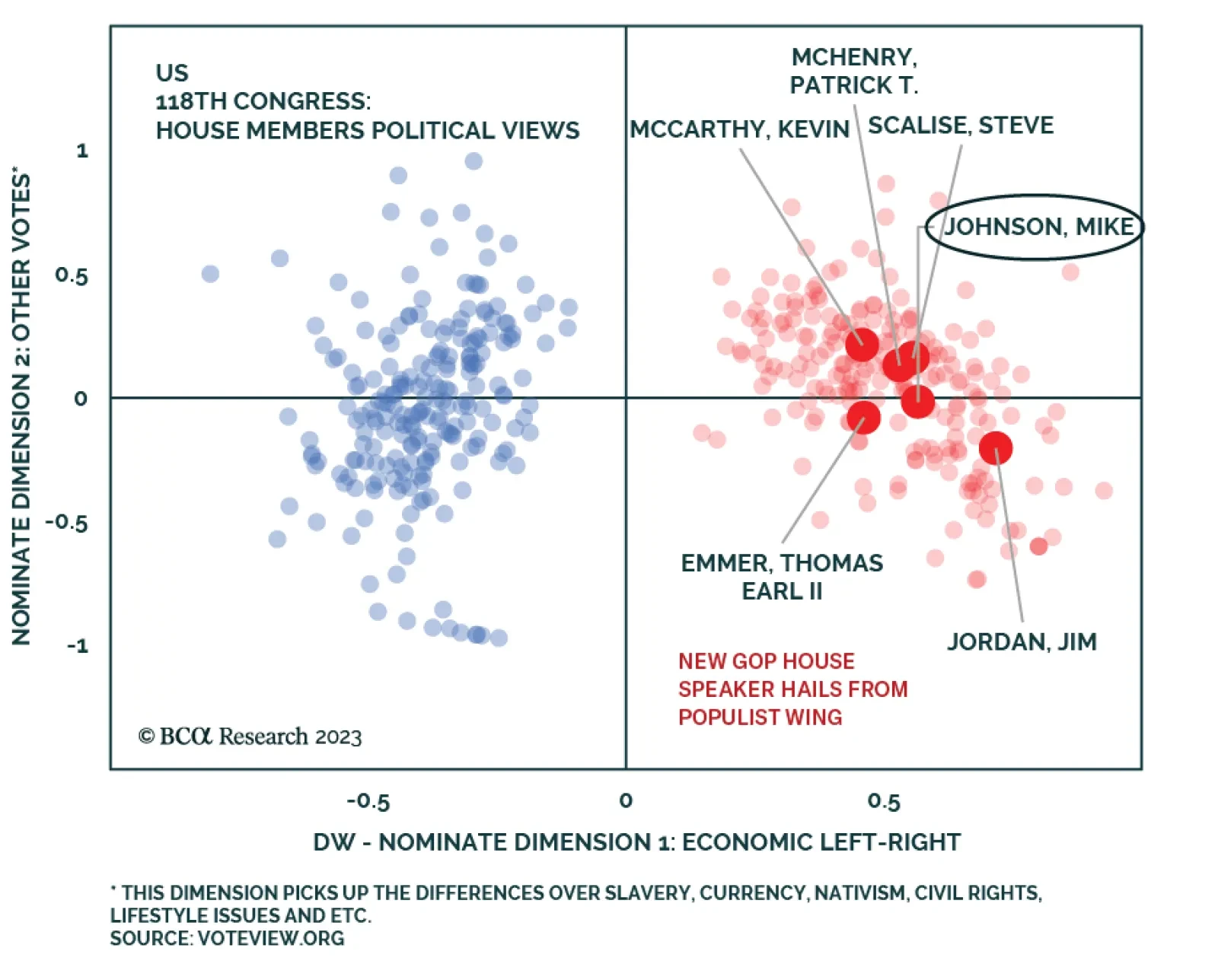

Stronger US growth elicits a response from the House Republicans. But a government shutdown is not devastating to the economy. What is more devastating would be a crisis in the Middle East, Europe, and Asia. Stay long US defense, energy, and large caps stocks.

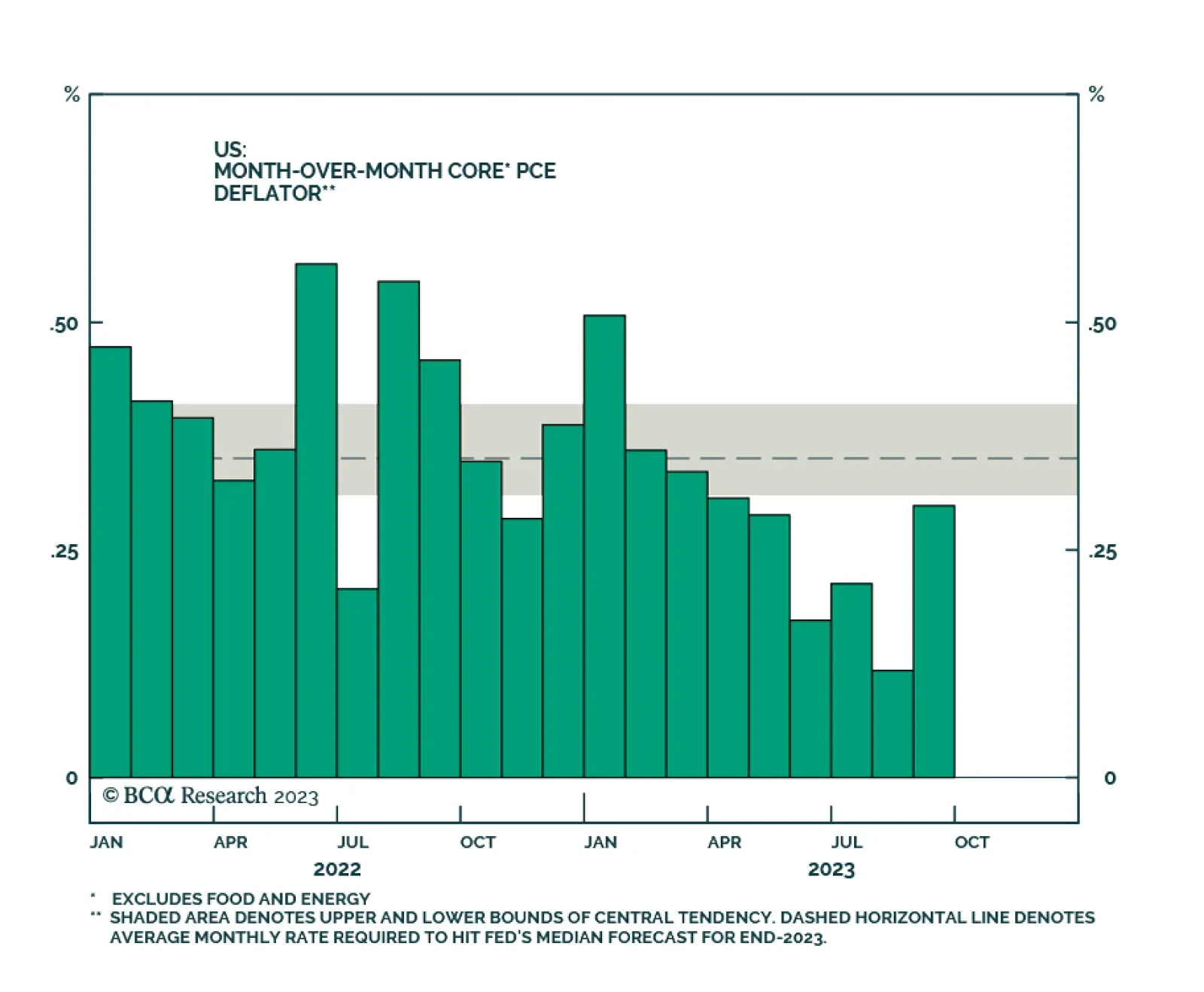

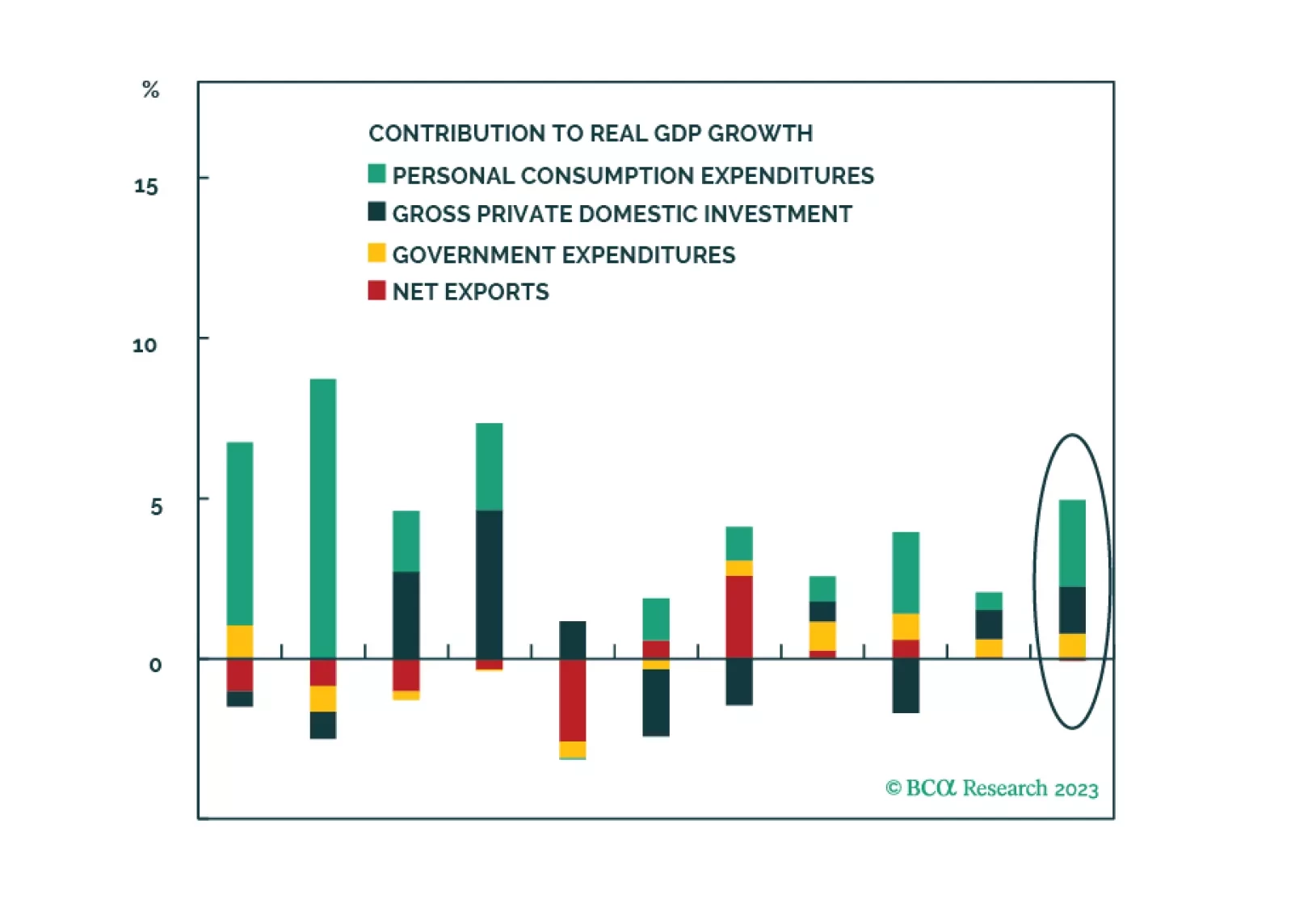

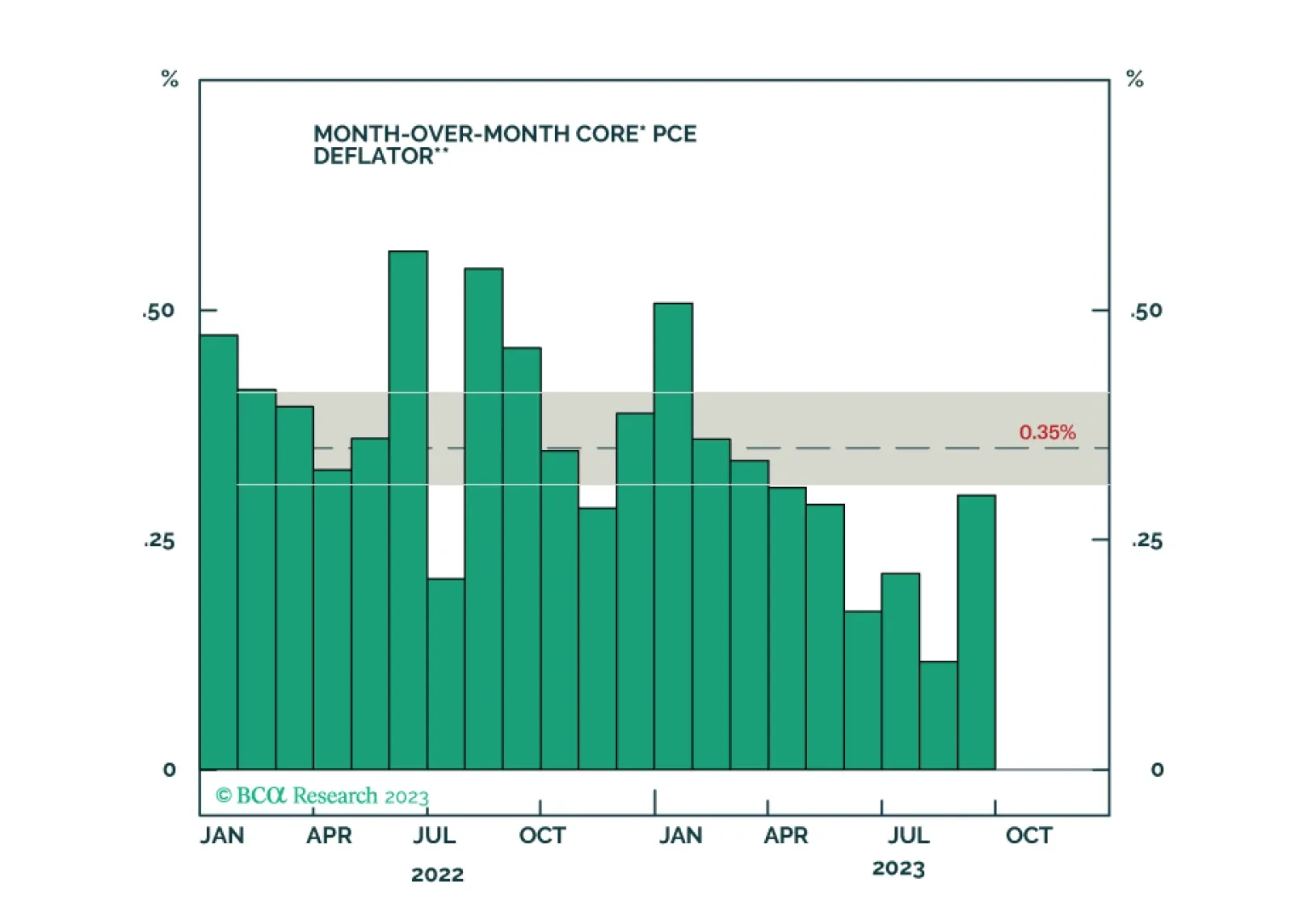

A look at recent data on economic growth, inflation and the labor market, and a discussion of the implications for Fed policy and bond strategy.

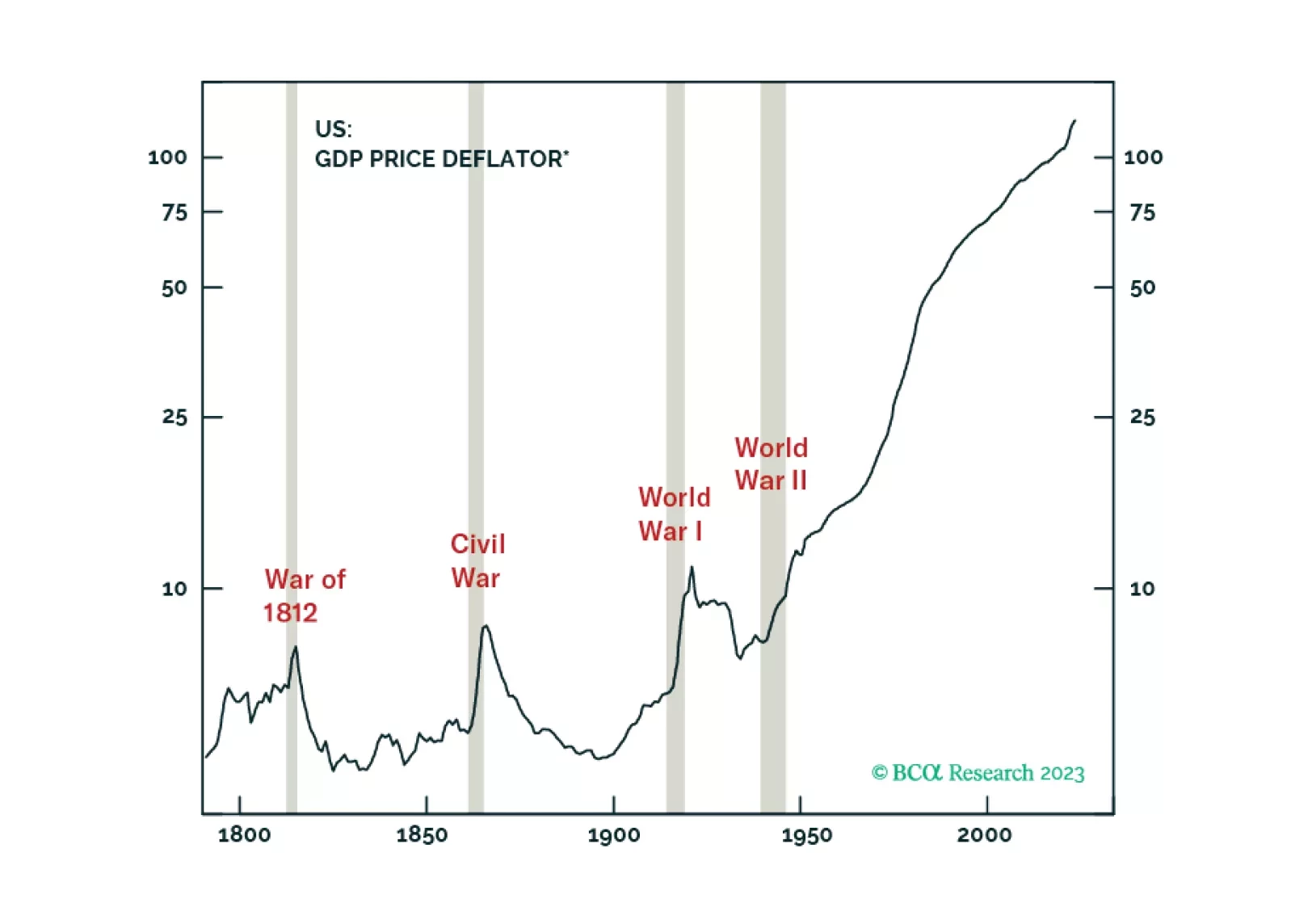

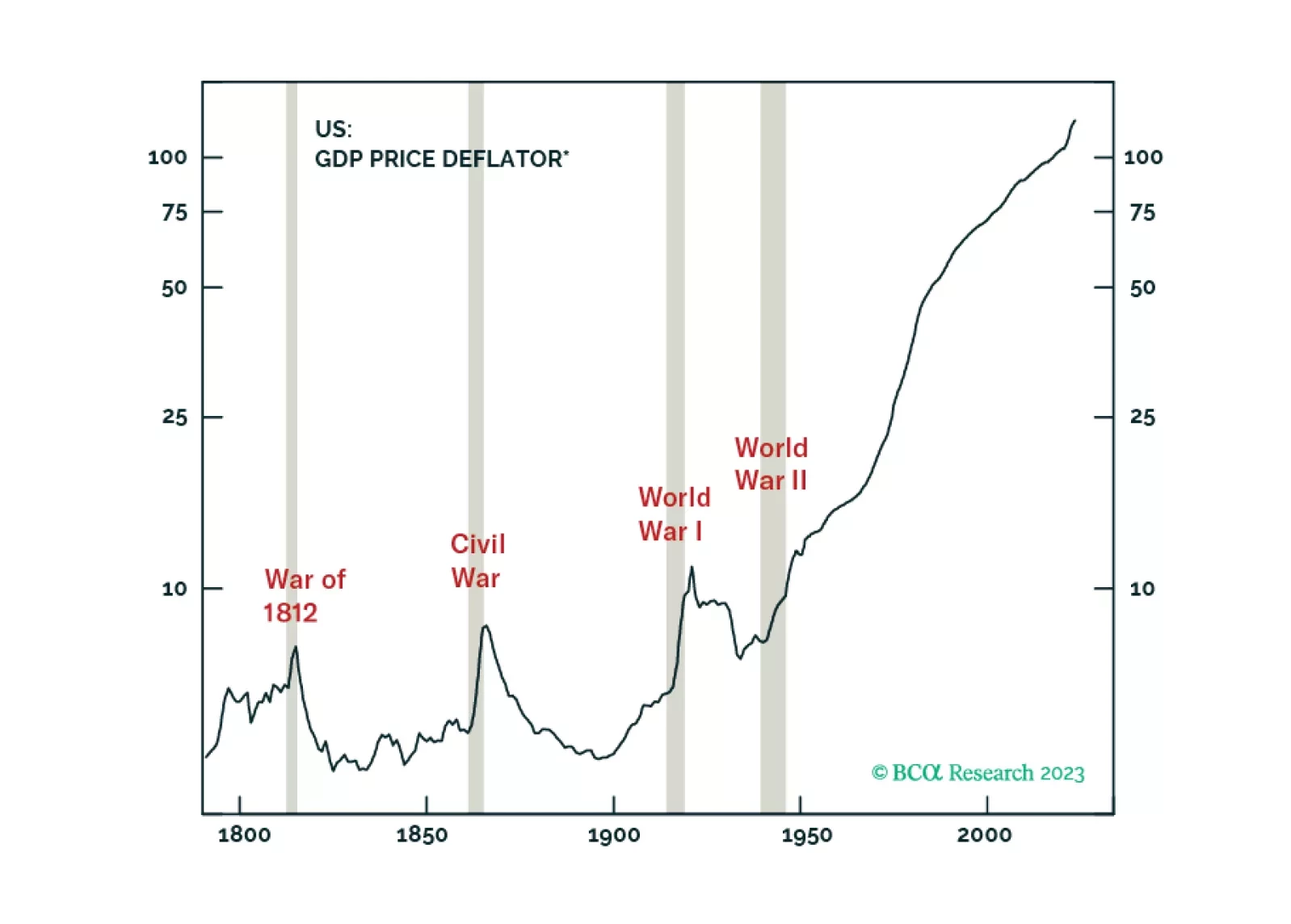

Section II of this month’s Bank Credit Analyst report is a guest piece written by Martin Barnes, which we are making available to all clients. Martin, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career, expresses his personal views about the long-run outlook for inflation. He argues that the multi-decade disinflationary era is over, which will bring significant challenges for both policymakers and investors.

In a guest authorship of Section I, Doug Peta presents a synthesis of the recent views expressed in our US Investment Strategy and Bank Credit Analyst reports. Doug underscores that excess savings are unlikely to support US consumer spending beyond the middle of next year, which argues for conservative investment positioning on a 6-12 month time horizon. Additionally, this month’s Section II is a guest piece written by Martin Barnes, who retired from BCA Research as Chief Economist in 2021 after a long and illustrious career. Martin expresses his personal views about the long-run outlook for inflation and argues that the multi-decade disinflationary era is over – which will bring significant challenges for both policymakers and investors.