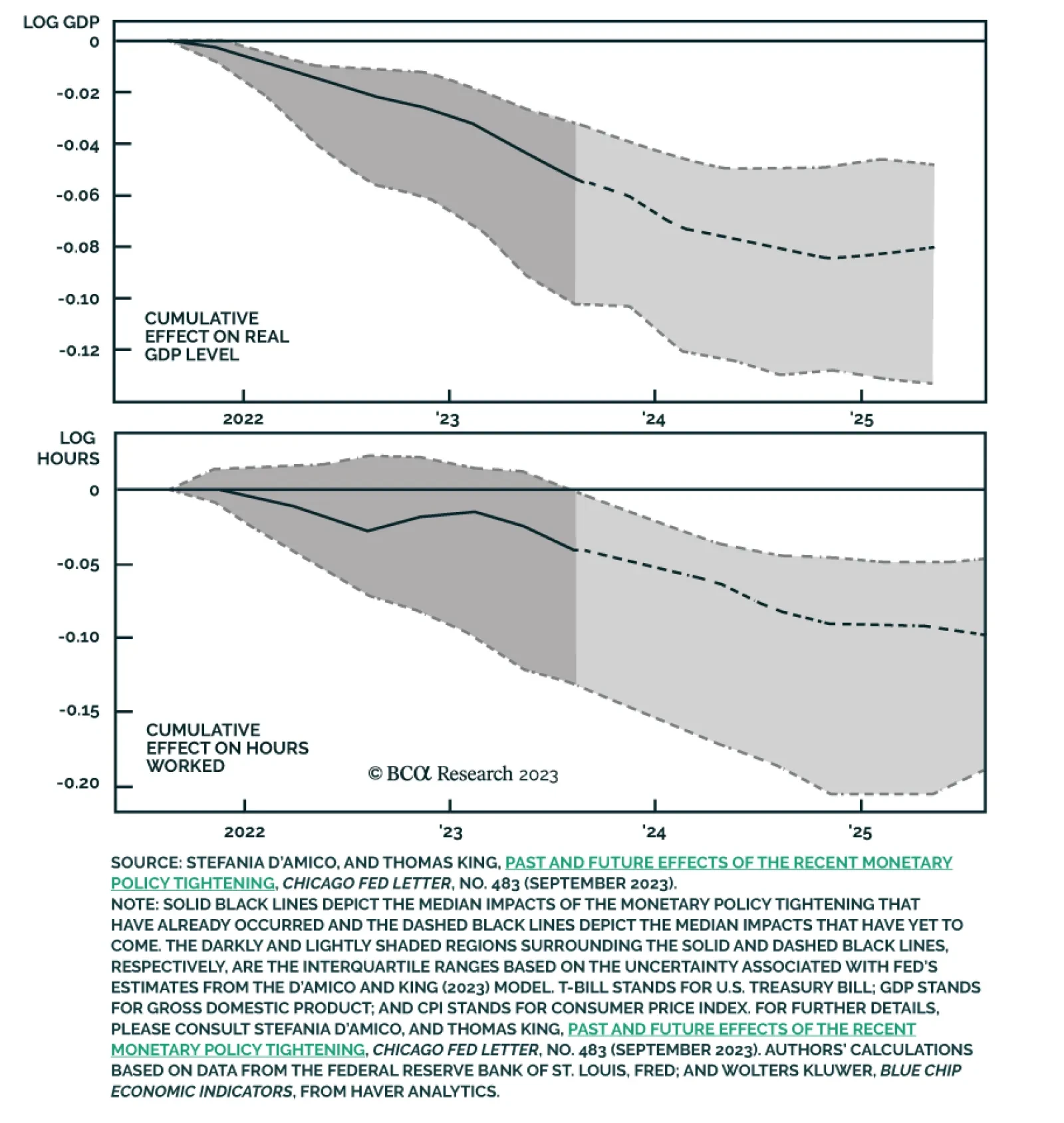

United States

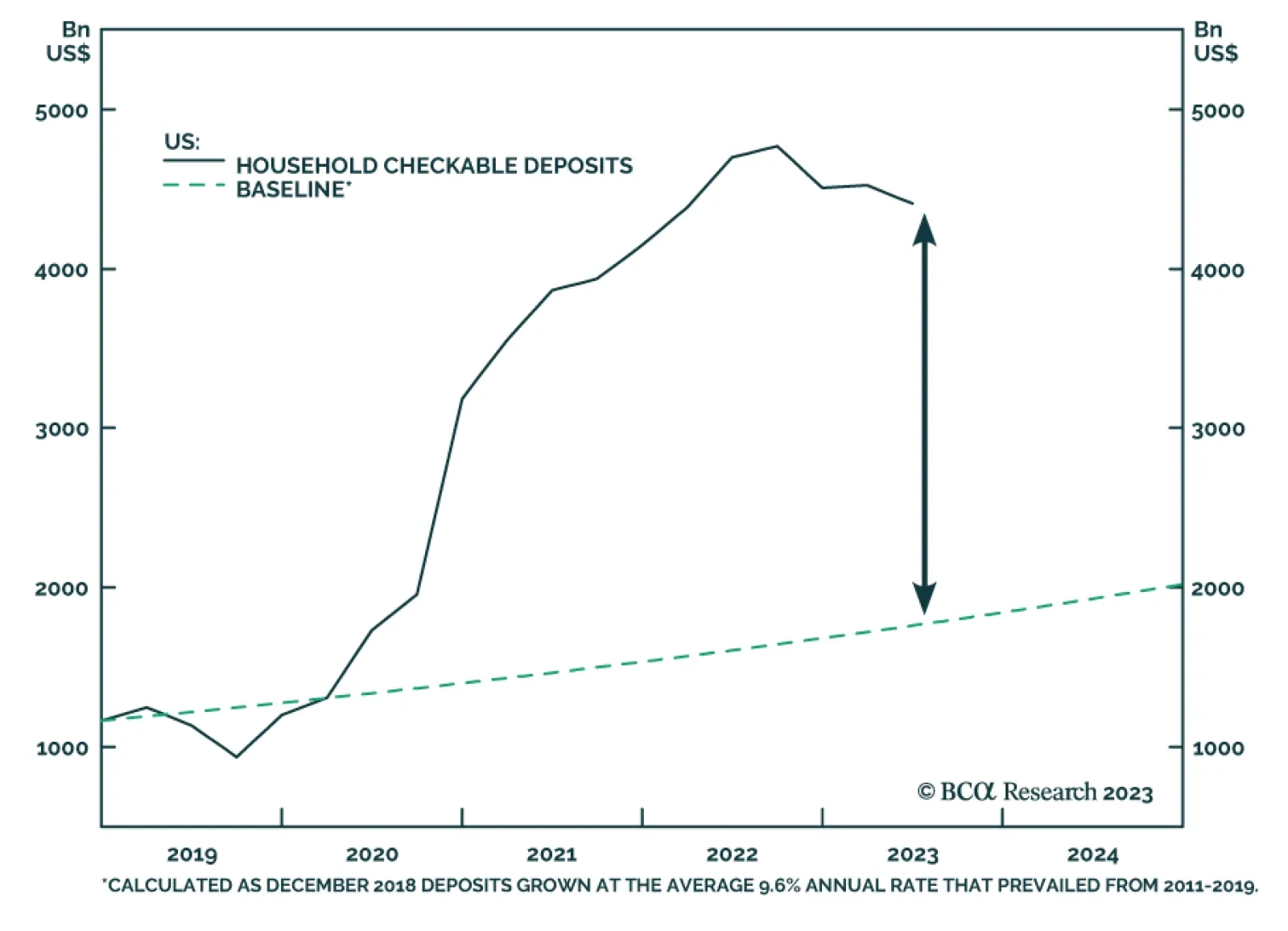

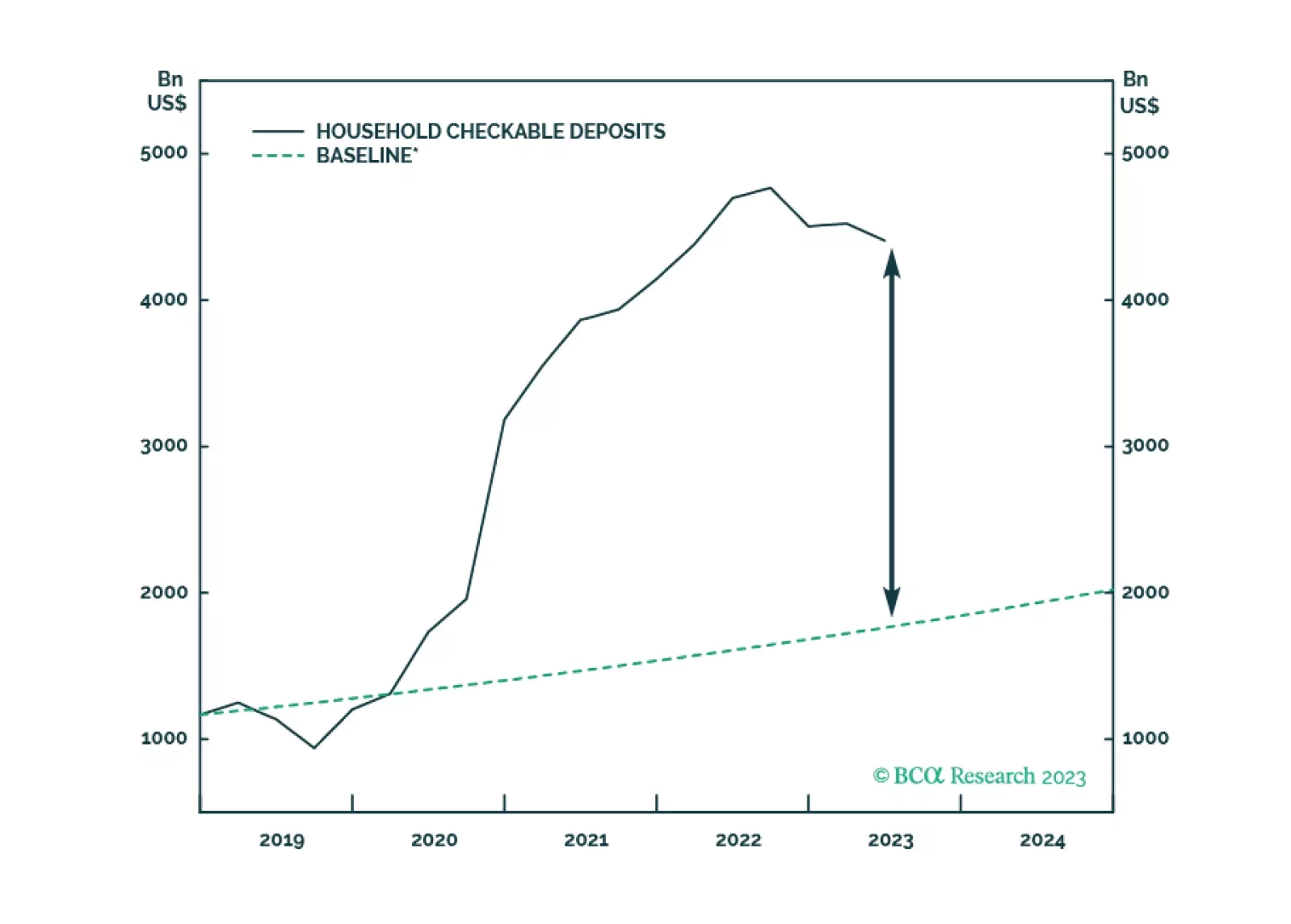

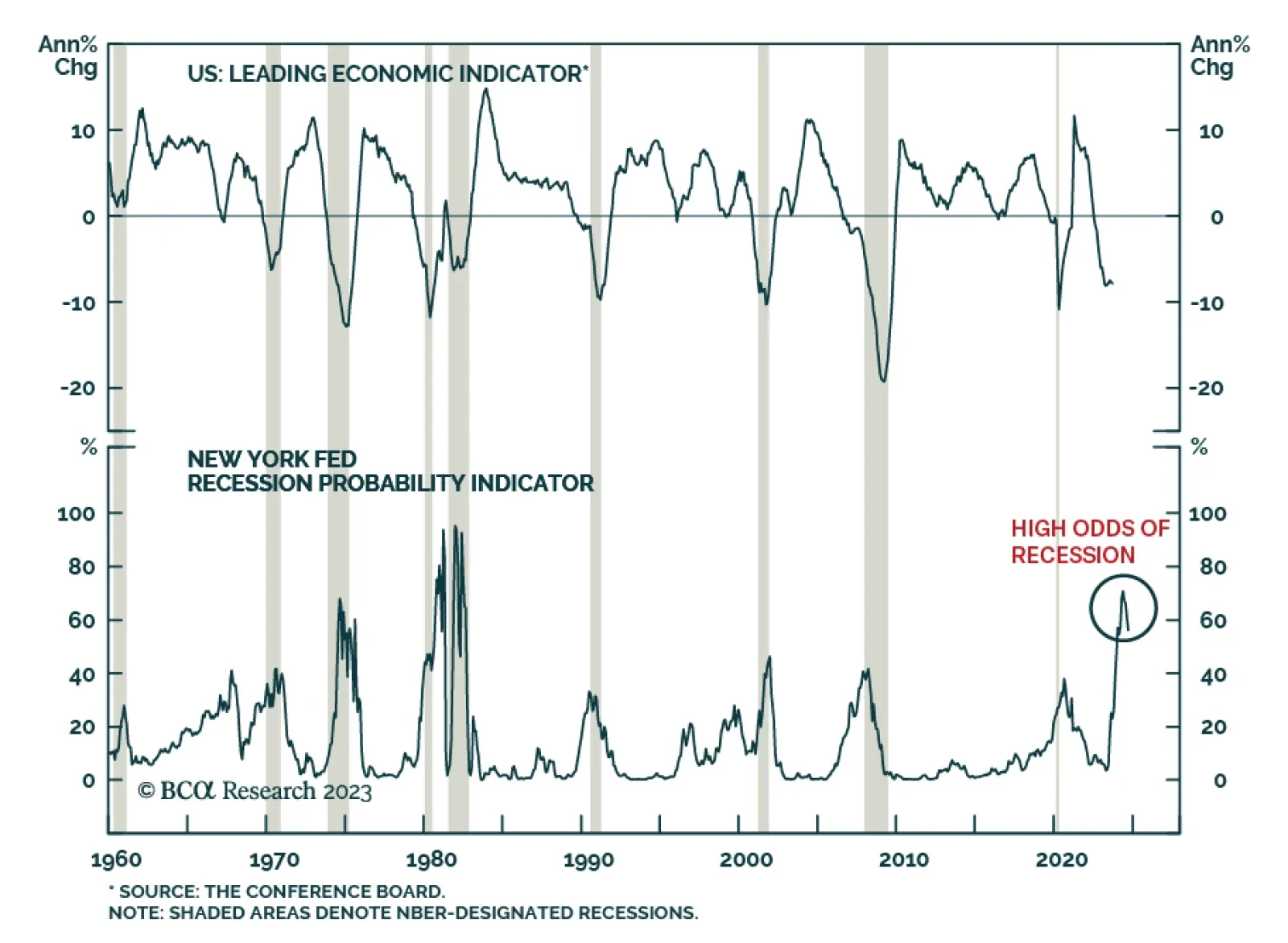

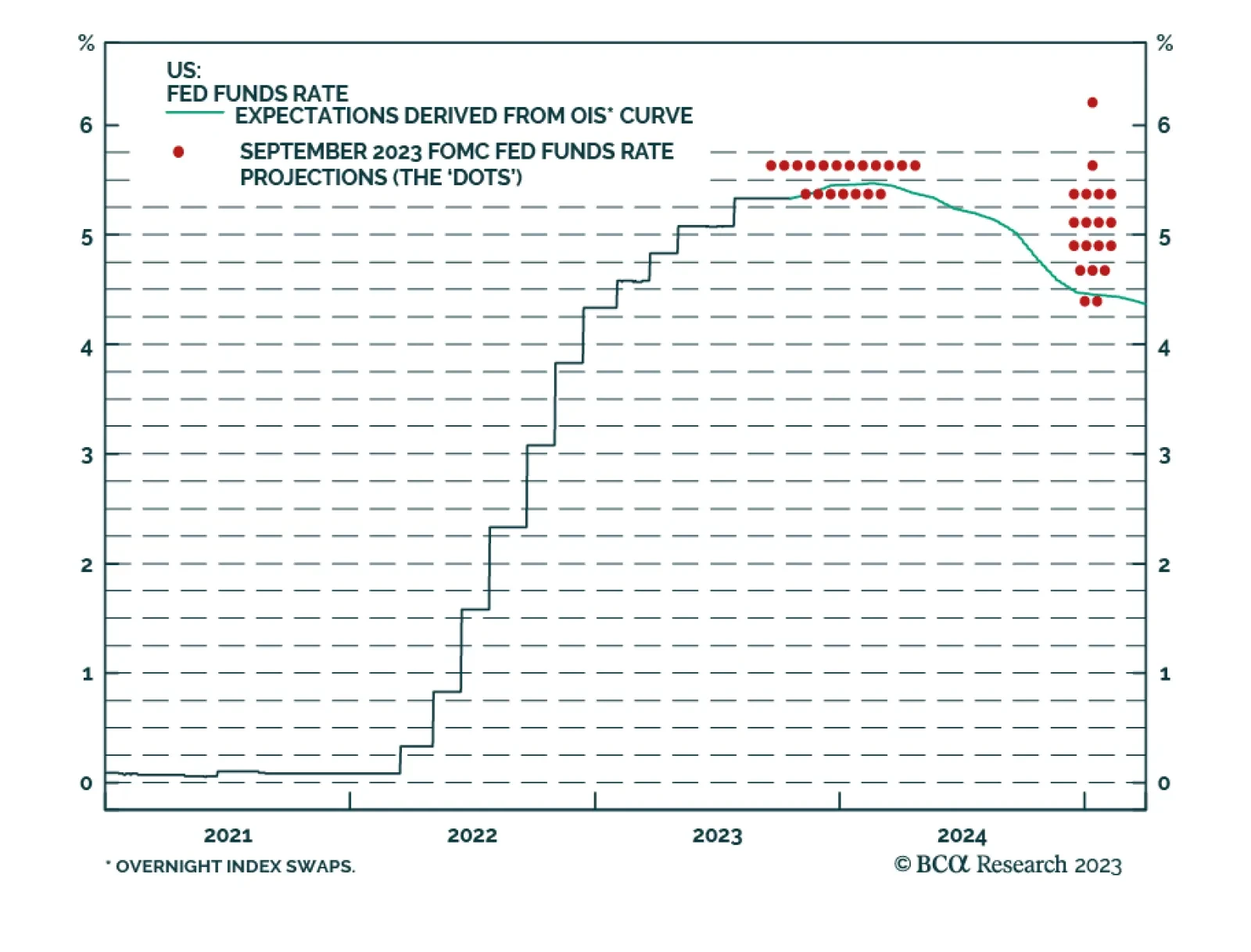

The biggest banks report that consumer credit card delinquencies still have yet to get back to pre-COVID levels and other credit performance indicators, leading and lagging, remain solid. There is still a great deal of cash sloshing around the banking system, though consumption has clearly slowed. We reiterate our view that a recession is coming, but not before the year is out.

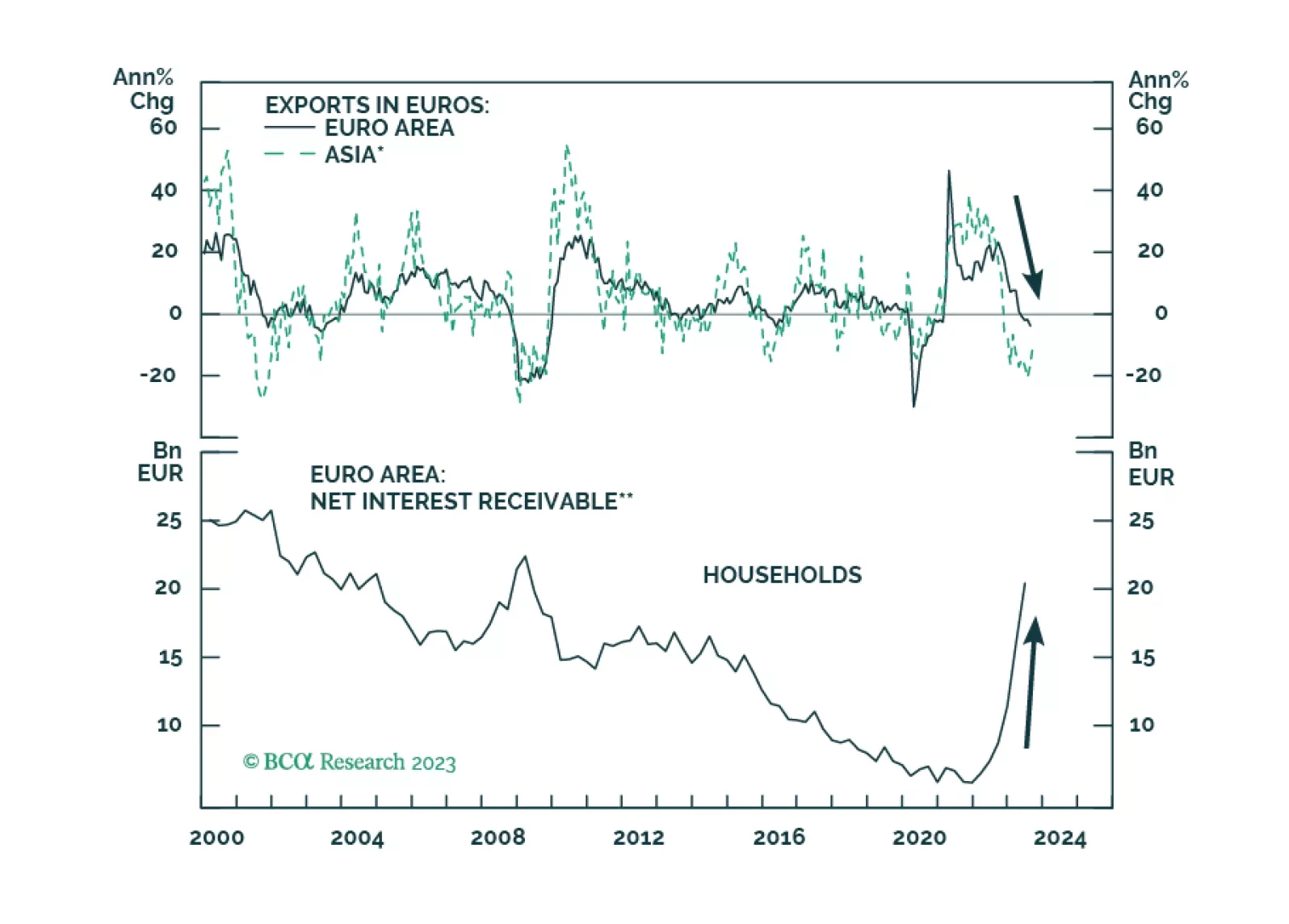

Europe’s weak patch is not about the ECB’s policy tightening, at least not yet. 2024 is another story, and the ECB’s policy will prompt a Eurozone’s recession around the summer.

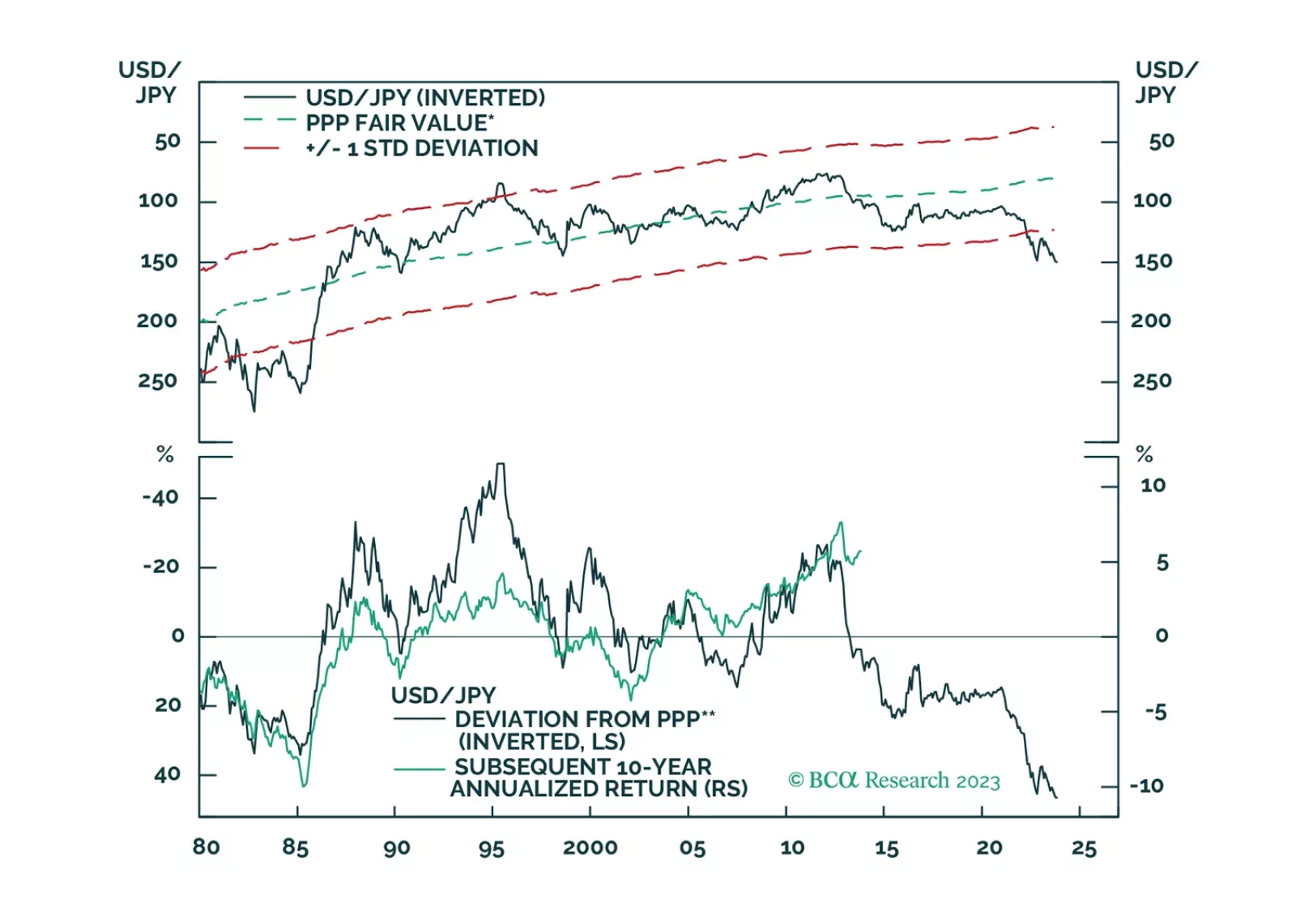

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

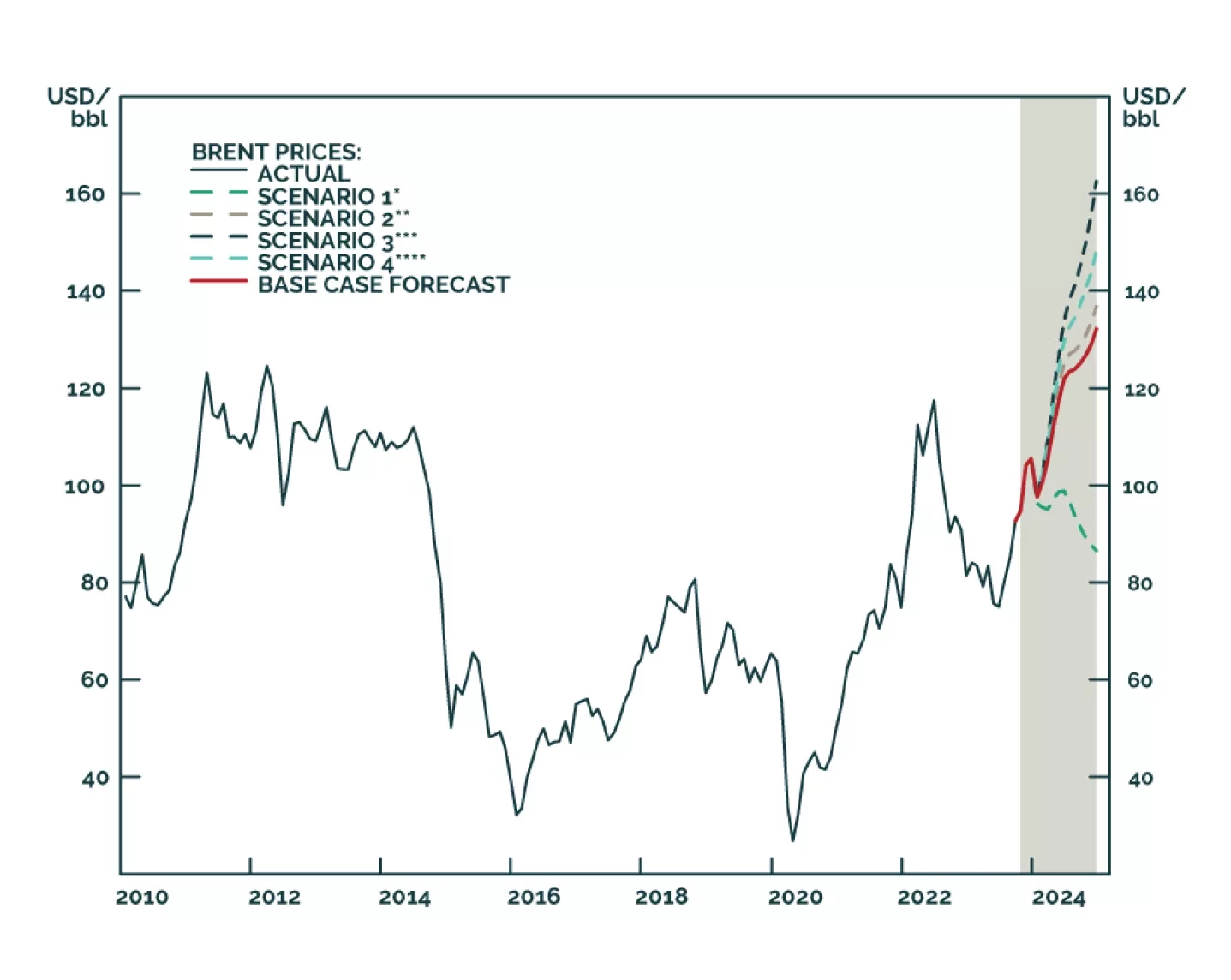

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.