United States

More equity volatility is coming in the short run. Trump’s nomination looks to be smooth, which marginally reduces the incumbent party advantage and increases policy uncertainty.

Yields remain the force dominating the evolution of markets. A peak in yields would help European assets rebound, but the war in the Middle East could push higher energy prices, with negative consequences for Europe.

Investors underestimate the likelihood of the war in Israel spilling outside of Gaza, and engulfing wider swaths of the Middle East, endangering energy supplies. Stay overweight Energy and Aerospace & Defense.

This week's Insight gauges the potential of a dollar breakout or breakdown and suggests a few trade ideas.

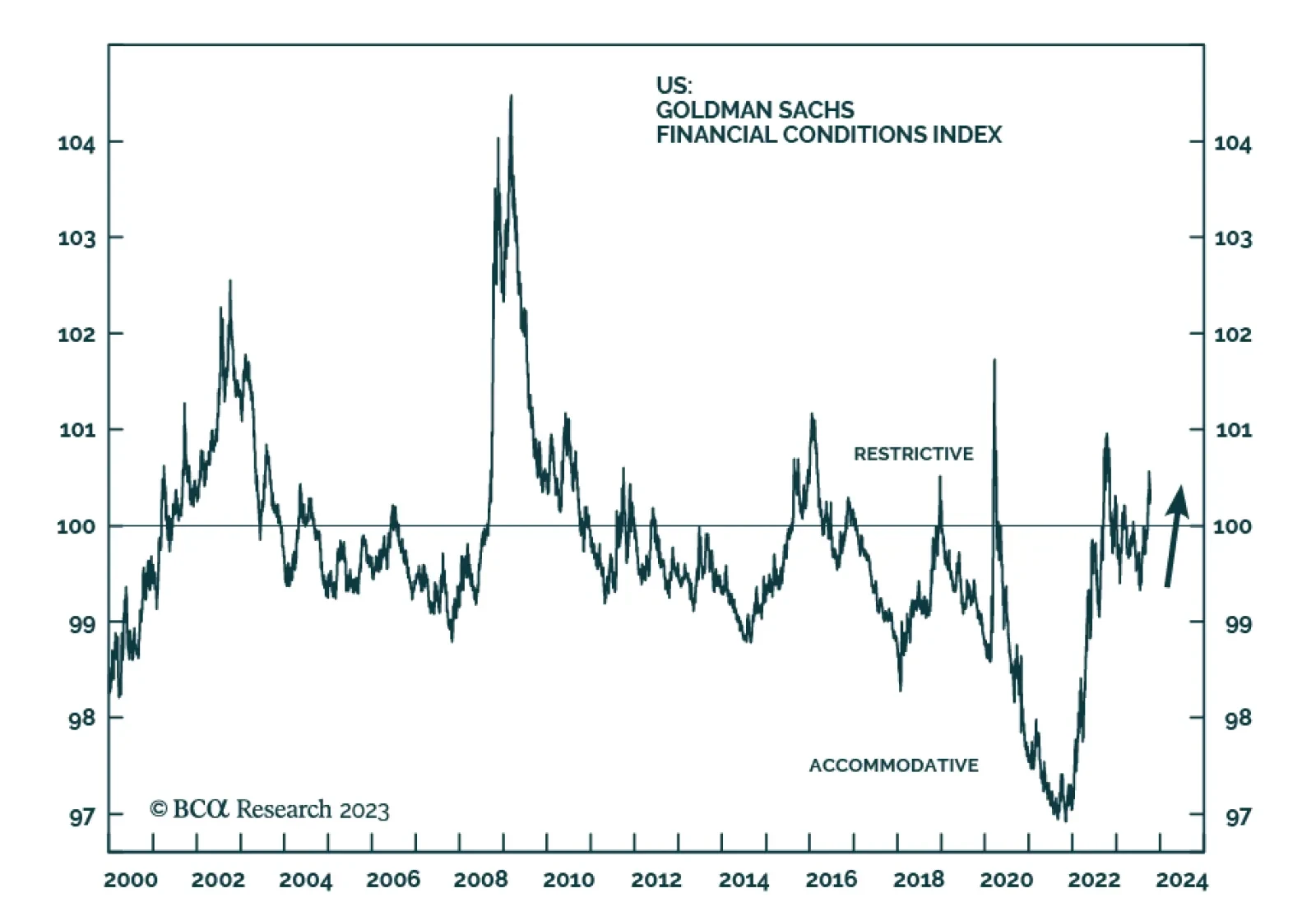

US monetary policy is restrictive, as evidenced by a falling jobs-workers gap. The reason that unemployment has not risen is because labor demand still exceeds supply. That will change in the second half of 2024 when the US economy succumbs to recession. Investors should increasingly favor bonds over stocks.

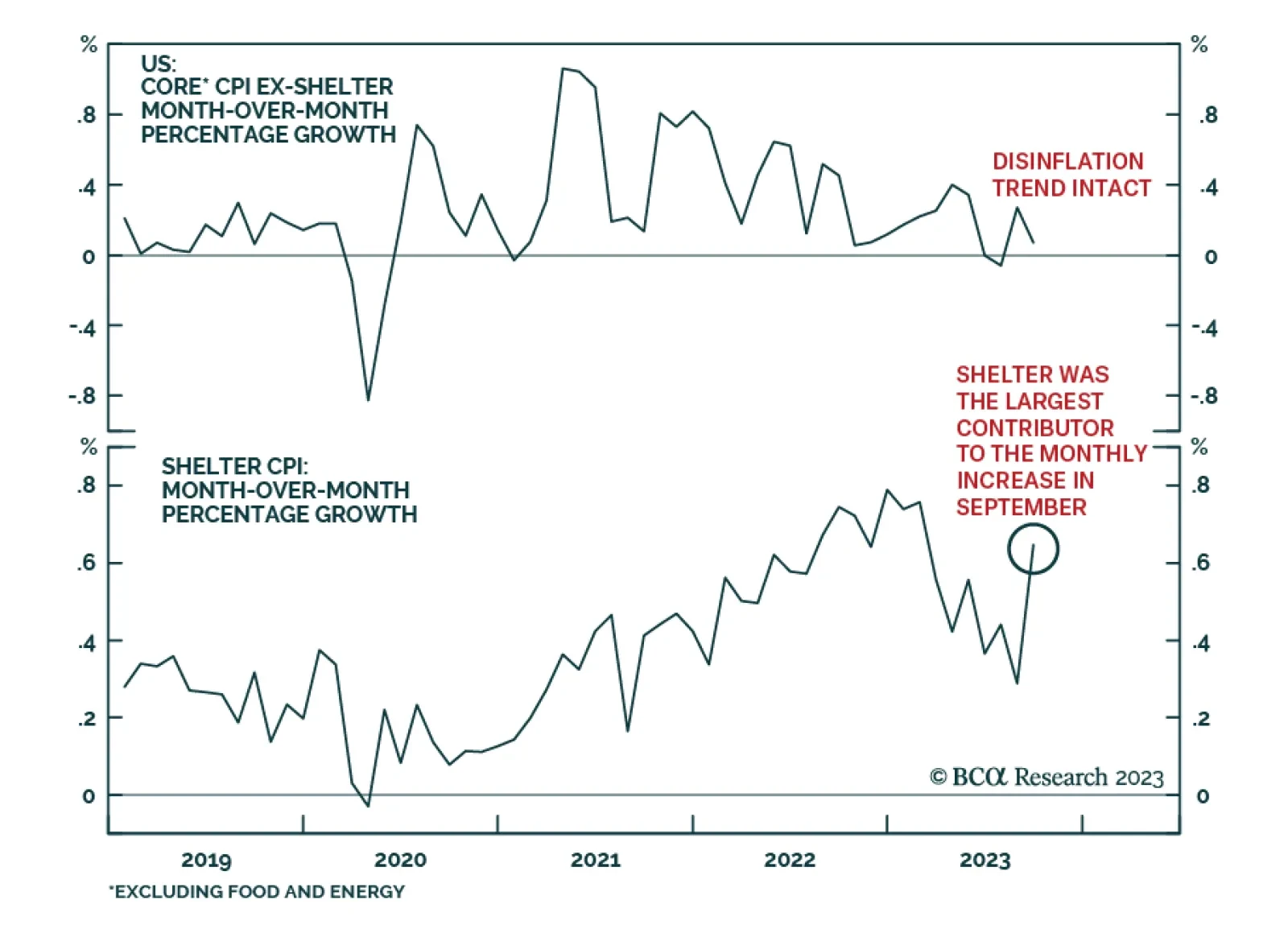

Comments on recent Fedspeak, bond market moves and this morning’s CPI report.