United States

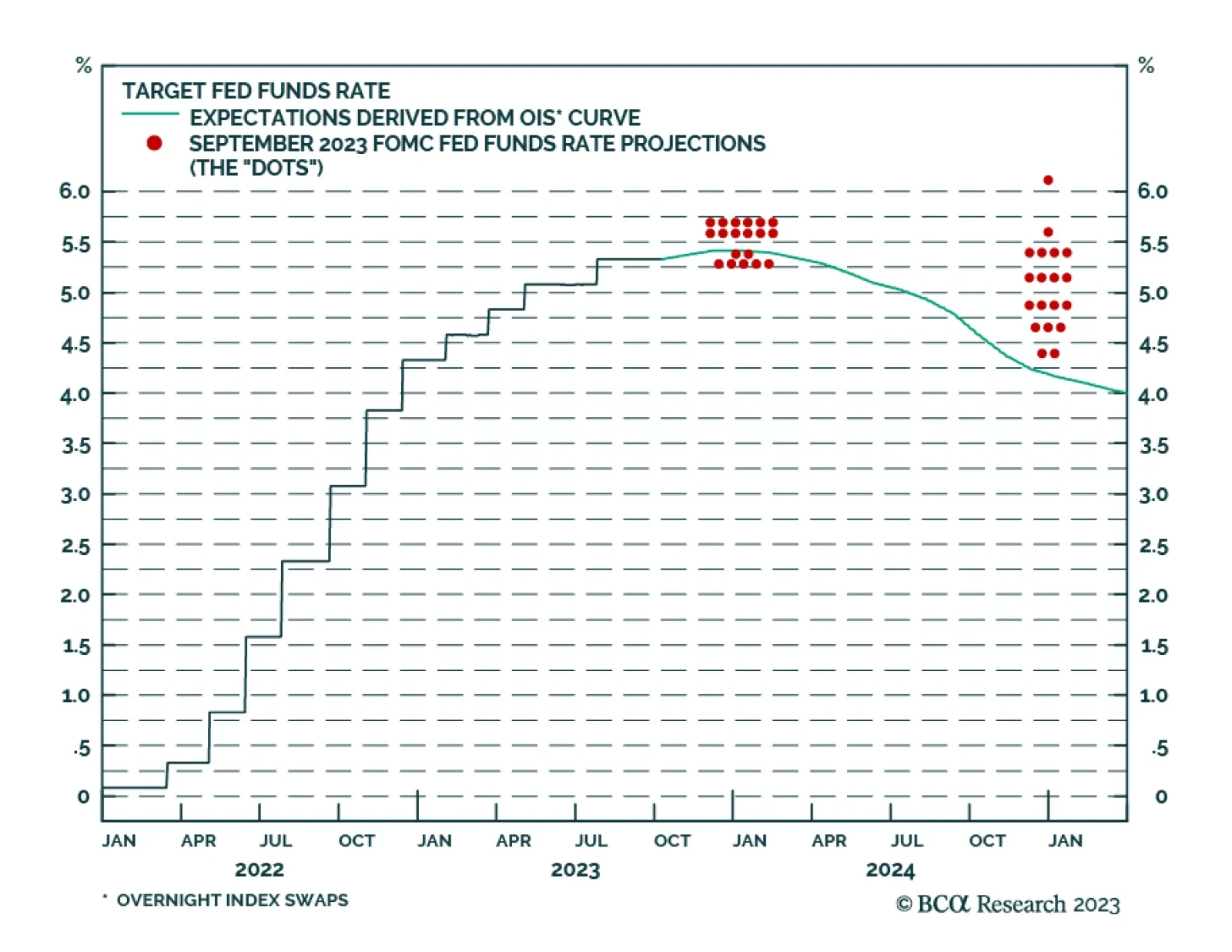

The sharp sell-off in long duration bonds (ticker TLT) has reached the collapsed 130-day complexity that implies a probable and playable rebound. More strategically, long-duration bonds yielding close to 5 percent are an excellent structural investment assuming central banks choose to slay inflation and the cost is a near-term recession. We discuss how to time and how to play the potential rebound.

Households’ excess pandemic savings will eventually run out, but we continue to disagree with the widespread view that they’re already gone or entirely in the hands of the wealthy. Consumers’ demise continues to be greatly exaggerated.

The market has been held hostage by surging rates. Zombie companies are “alive” and are multiplying – they are highly sensitive to surging borrowing costs. Underweight Utilities to reduce portfolio duration. Maintain neutral positioning of Basic Materials but take a granular approach to allocations within the sector.