United States

We continue to expect Brent crude to trade just above $101/bbl in 4Q23, and to average $118/bbl in 2024. Higher volatility looms. We expect Russia will cut oil production next year as part of a concerted effort to undermine Biden’s re-election. Oil-demand volatility is set to rise in response to divergent policy imperatives. We continue to favor equity exposure to oil and gas via the XOP ETF; direct exposure via the COMT ETF, and long Dec23 $100/bbl Brent calls. We are getting long Jan-Feb-Mar 2024 Brent futures vs. short the same months in 2025 expecting steeper backwardation as inventories draw and markets tighten.

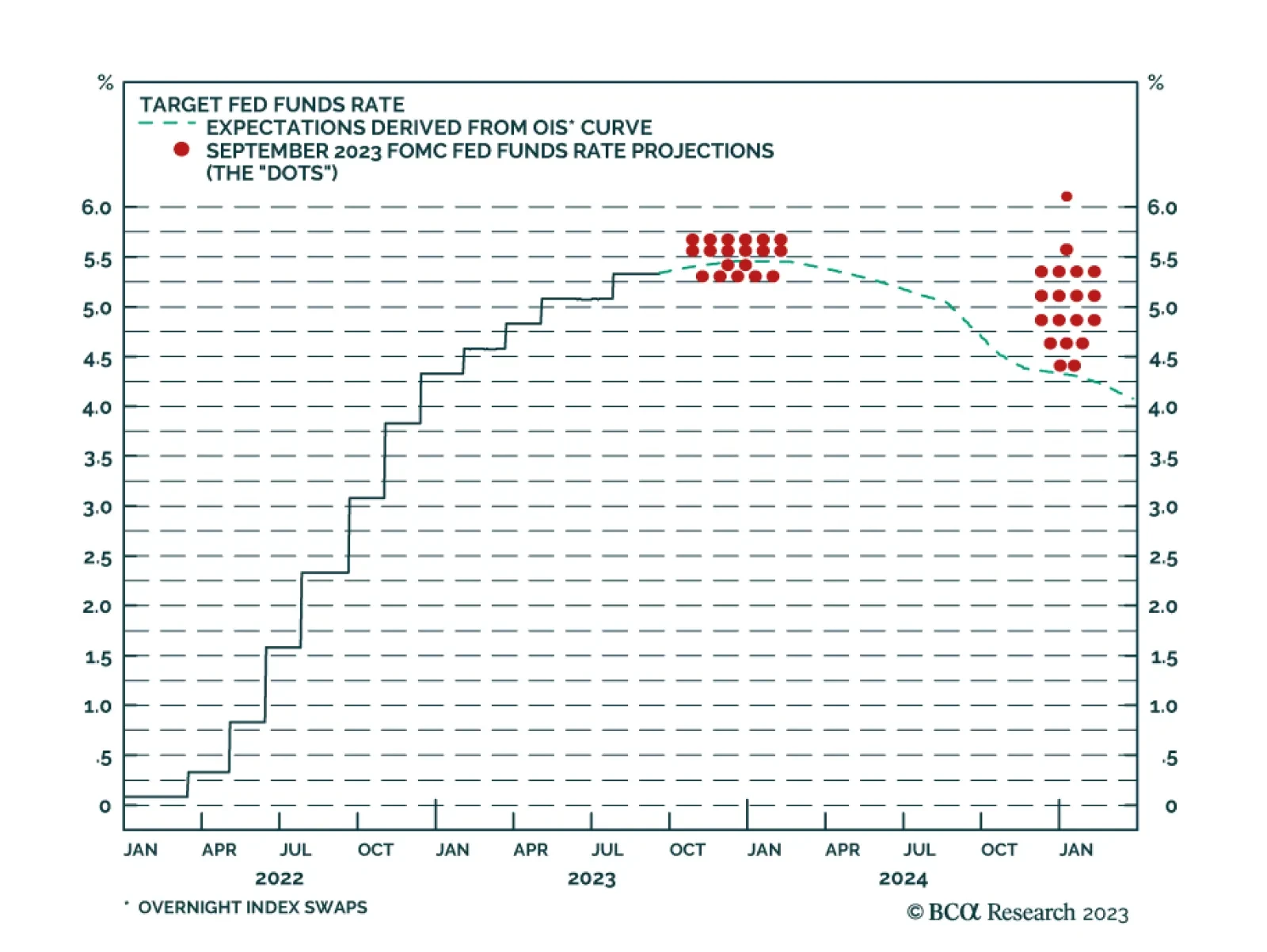

A discussion of today’s FOMC meeting and its investment implications.

The biggest misunderstanding in the markets right now is that to keep expected inflation well-anchored at 2 percent, inflation must <i>undershoot</i> 2 percent for some time. This implies that interest rate futures curves are mispriced, and that the probability of a ‘soft landing’ is lower than assumed. Plus: we show that the rally in oil has become fractally fragile, and recommend a tactical underweight.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.