United States

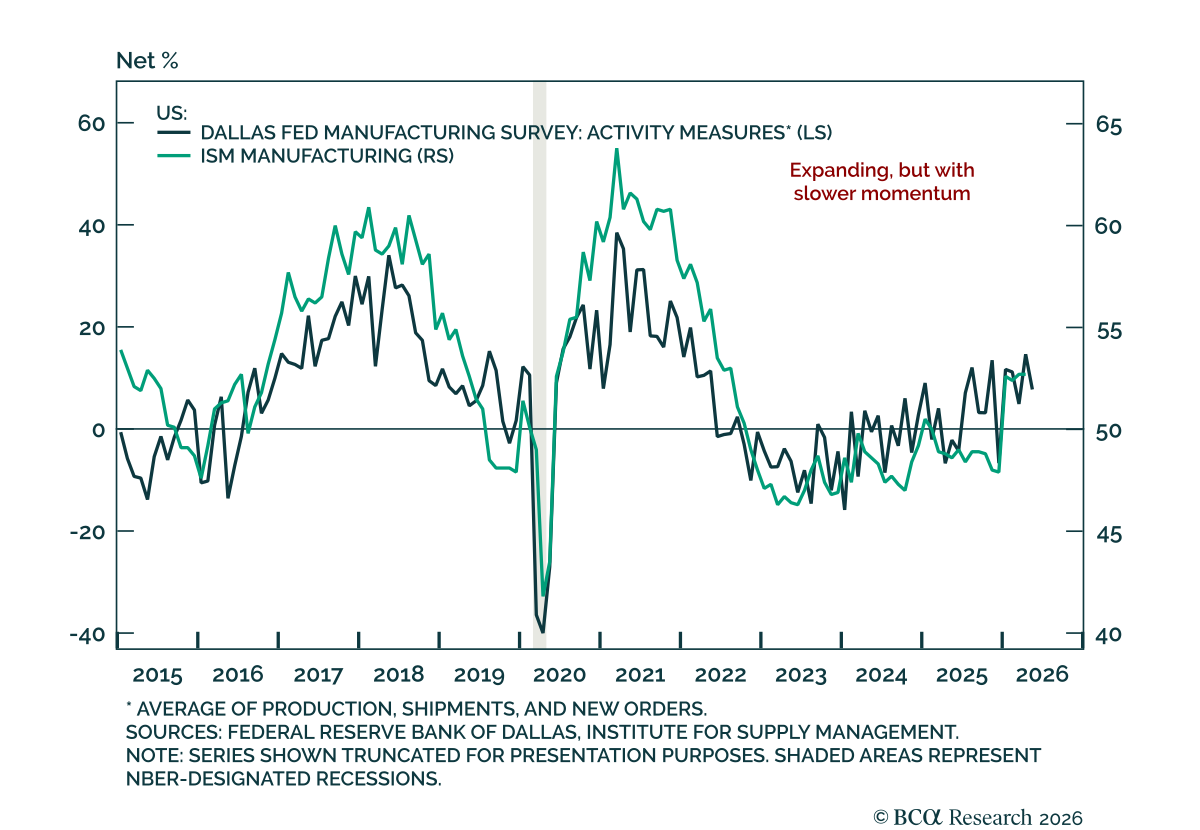

The Dallas Fed survey points to Texas manufacturing continuing to expand in May, but with slowing momentum. The production index fell 10 points to 9.4, signaling an average pace of output growth rather than a broad acceleration. The softer tone showed up…

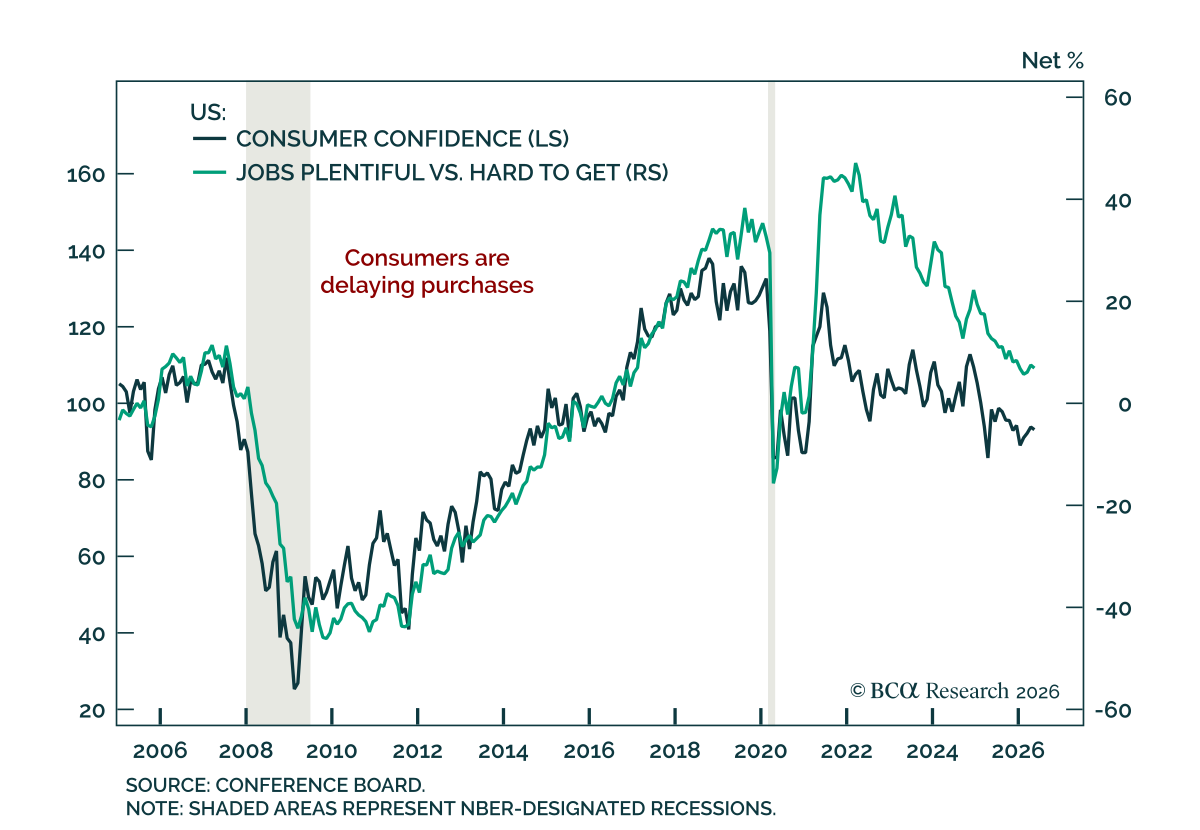

US consumer confidence softened marginally in May as high oil prices kept inflation pressure in focus. The Conference Board Consumer Confidence Index slipped to 93.1 from an upwardly revised 93.8 in April, but still came in slightly above…

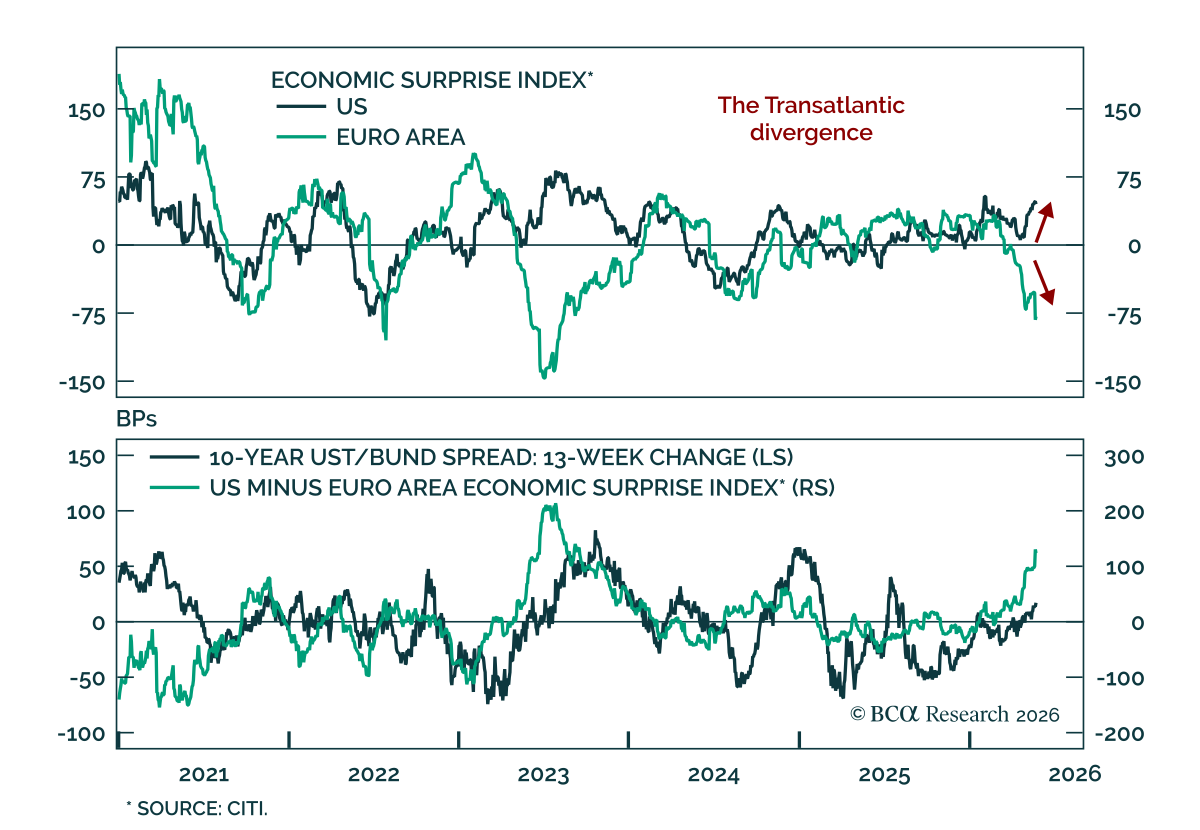

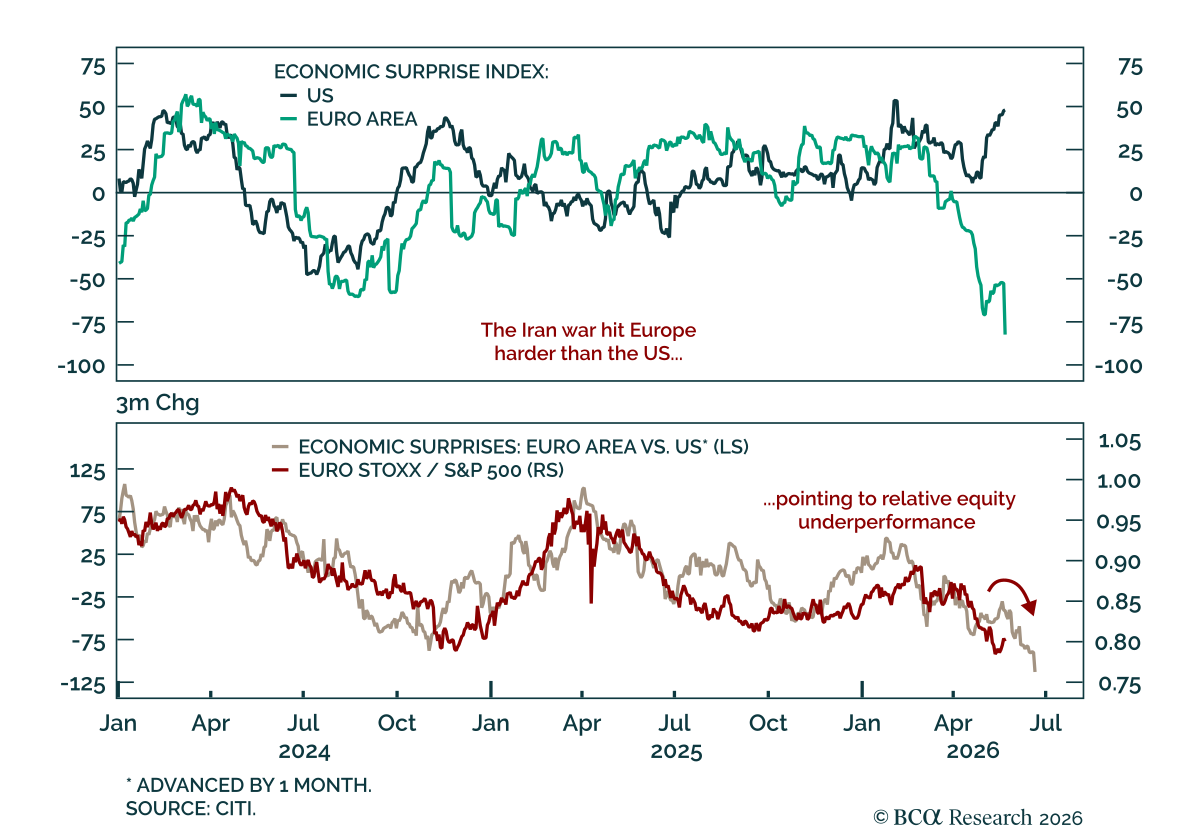

Go long German 10-year Bunds versus US 10-year Treasuries as US resilience diverges from euro area weakness. The trade is backed by a widening growth gap, with the US better insulated from rising oil prices and the euro area losing momentum. The US…

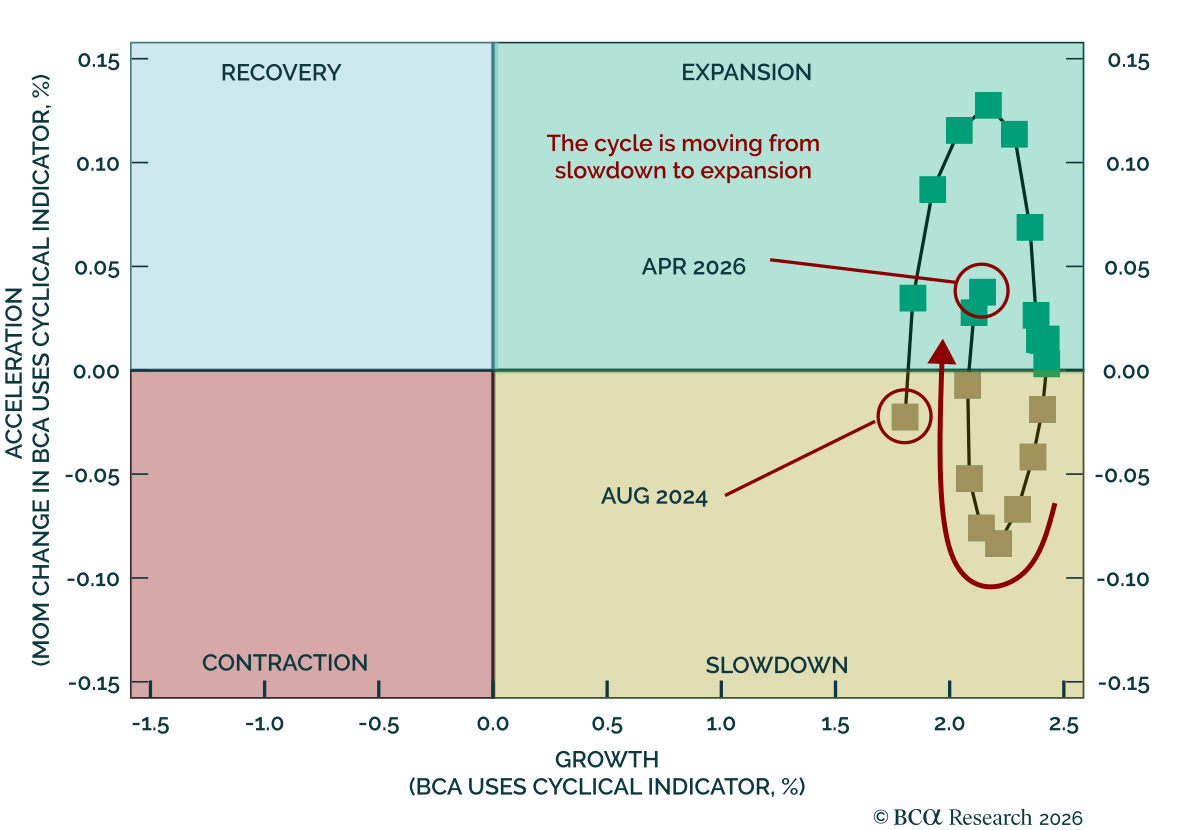

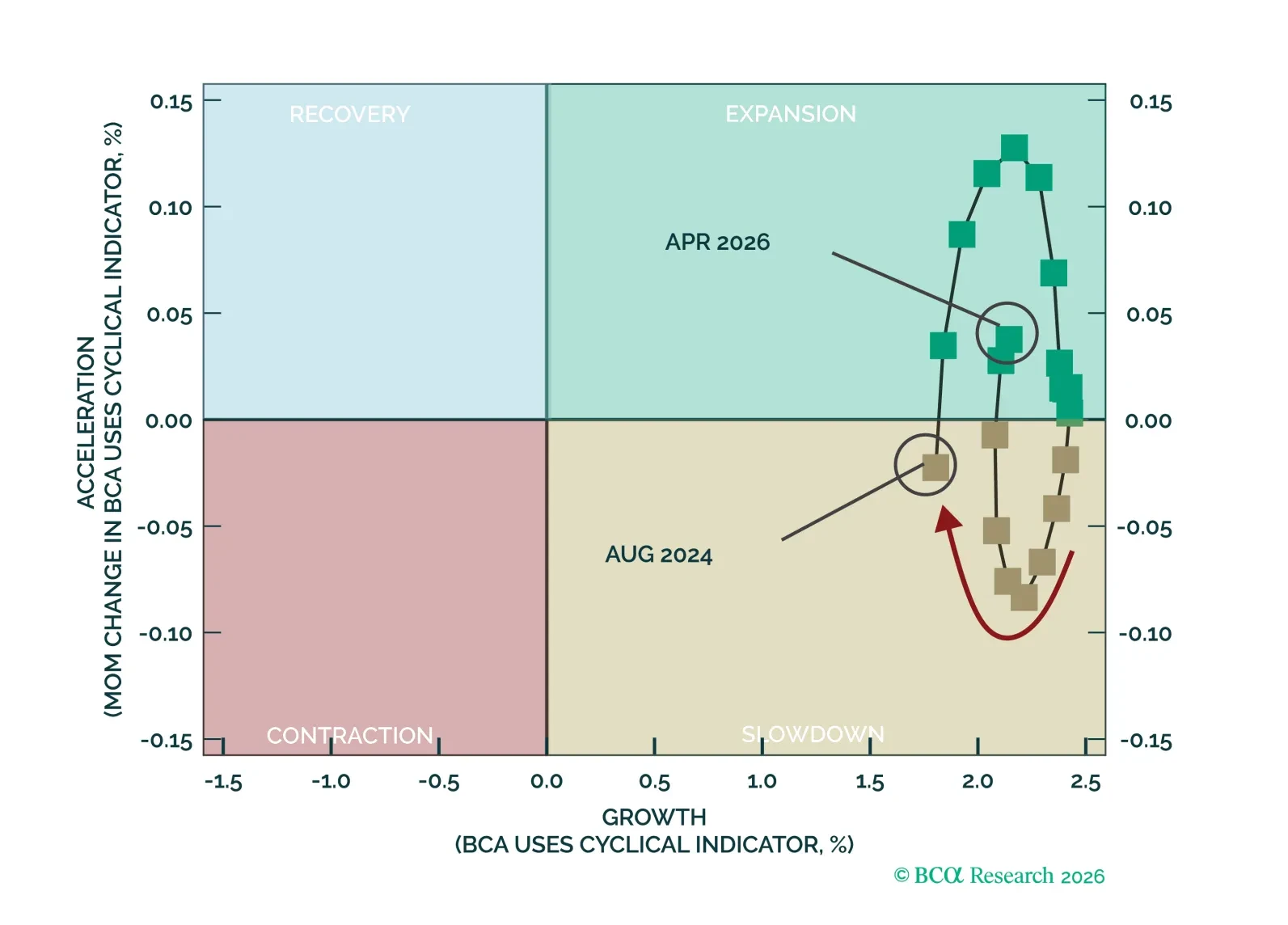

Our US Equity strategists remain bullish as their proprietary cyclical indicator shows US growth is modestly improving. The turn is being led by business-side indicators, while consumer and labor-market signals remain soft. Historically, expansion phases have…

Against the earnings-versus-everything-else market backdrop, stellar earnings are easily outweighing elevated oil prices, rising yields and the increased probability that the Fed may hike rates before the year is out. US allocators should remain invested in equities.

Relative macro momentum still favors the US over Europe. Our tactical framework rests on two ideas: the feedback loop between financial conditions and economic data surprises, and the impact of macro momentum on markets. In Europe, momentum had already…

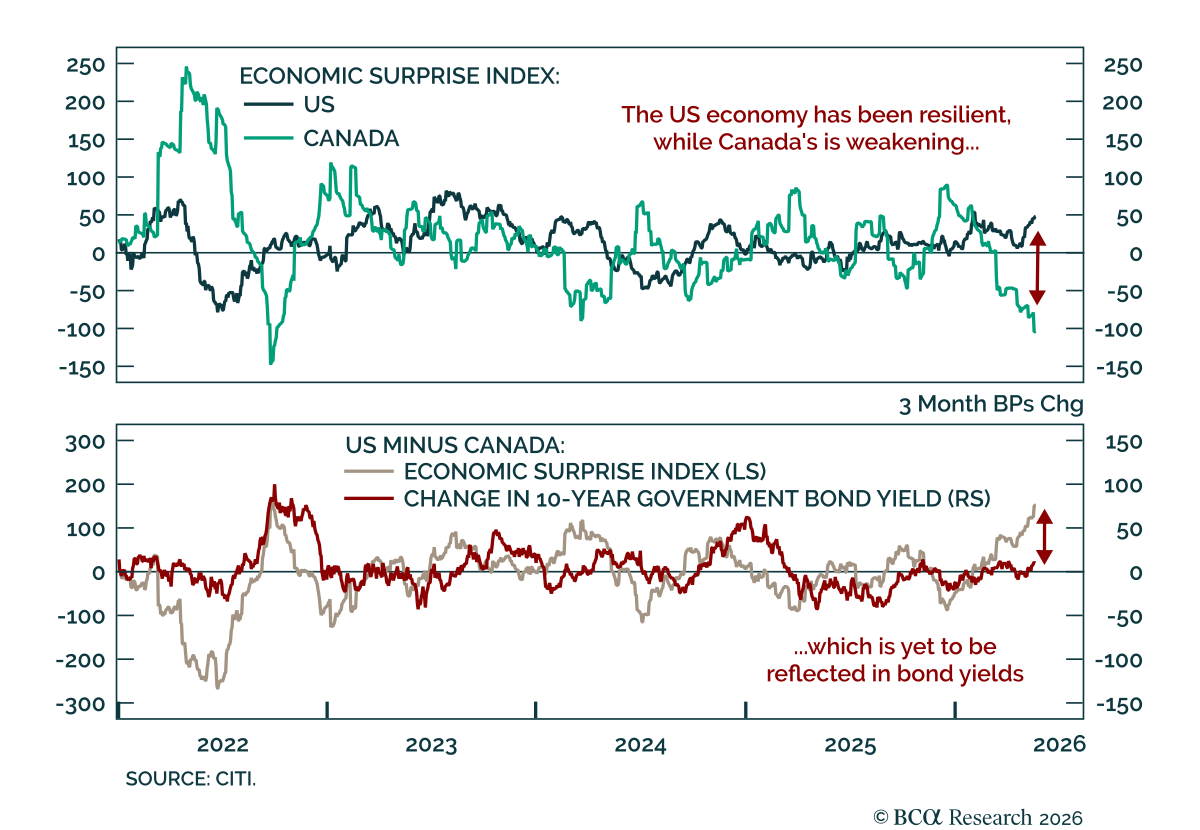

The US and Canada face increasingly different macro backdrops, and that divergence should support Canadian bonds versus Treasuries. US data has stayed resilient, surprising positively and showing growth momentum. Meanwhile, Canadian data has increasingly…

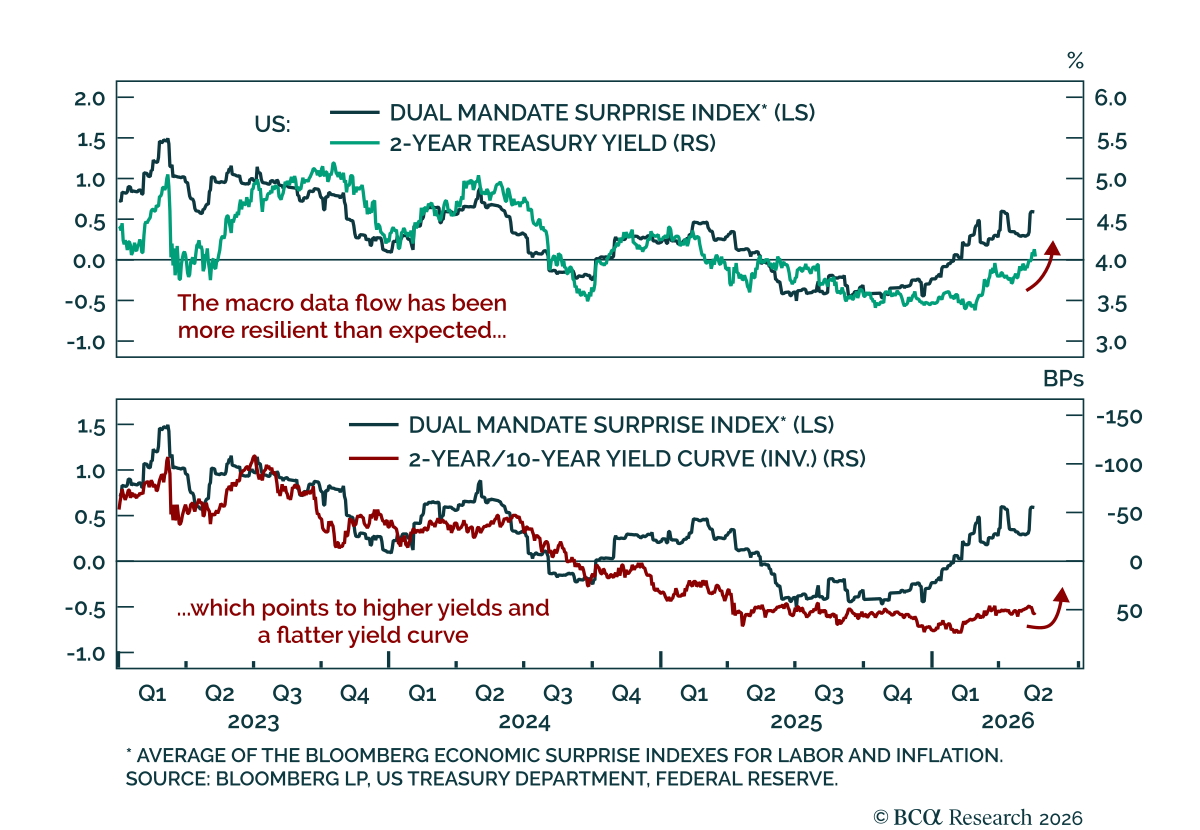

The April FOMC minutes clarified the hawkish shift that marked the meeting. The Fed held at its last meeting, but there were four dissents. While Governor Miran favored a 25 bps cut, regional presidents Hammack, Kashkari, and Logan supported a hold but voted…

US growth remains positive and is now improving, with the economy seemingly exiting Slowdown and proceeding into Expansion. Markets are reflecting the shift, rewarding revenue growth and capex growth, while earnings expectations continue to advance. The backdrop remains supportive, but expectations are rising and risks from financial conditions linger.

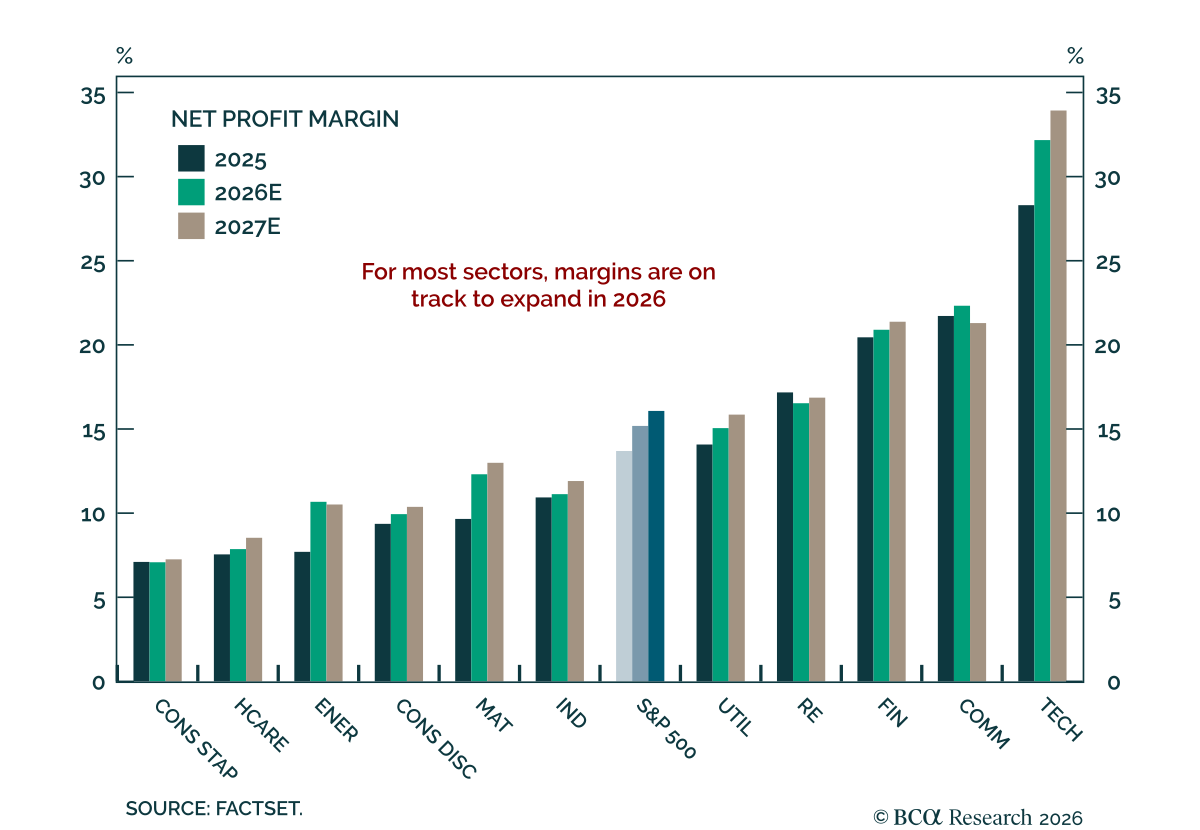

Strong and broad Q1 earnings are keeping the investment-led cyclical story intact despite rising geopolitical and supply-side risks. Our Chart Of The Week comes from Noah Weisberger, Chief US Equity Strategist. The Q1 earnings season has delivered strong…