United States

The Conference Board’s US Leading Economic Indicator (LEI) fell by 0.3% m/m in January, marking the 10th straight monthly decline. The LEI is a leading indicator of recessions whereby it typically contracts on a year-on-year basis in the lead-up to a…

Stronger than anticipated economic data releases have caused market participants to revise their fed funds rate projections. Investors now expect the Fed will have to hike rates to a higher terminal rate and hold them there for longer than they were…

According to BCA Research’s Global Investment Strategy service, even if the US avoids a second inflation wave before the next recession, there is a good chance that it will experience another wave of inflation after the recession ends, similar to what…

The risk of a recession in 2023 is being supplanted by the risk of another inflation wave. We will turn more defensive on equities if it continues to look like inflation is making a comeback.

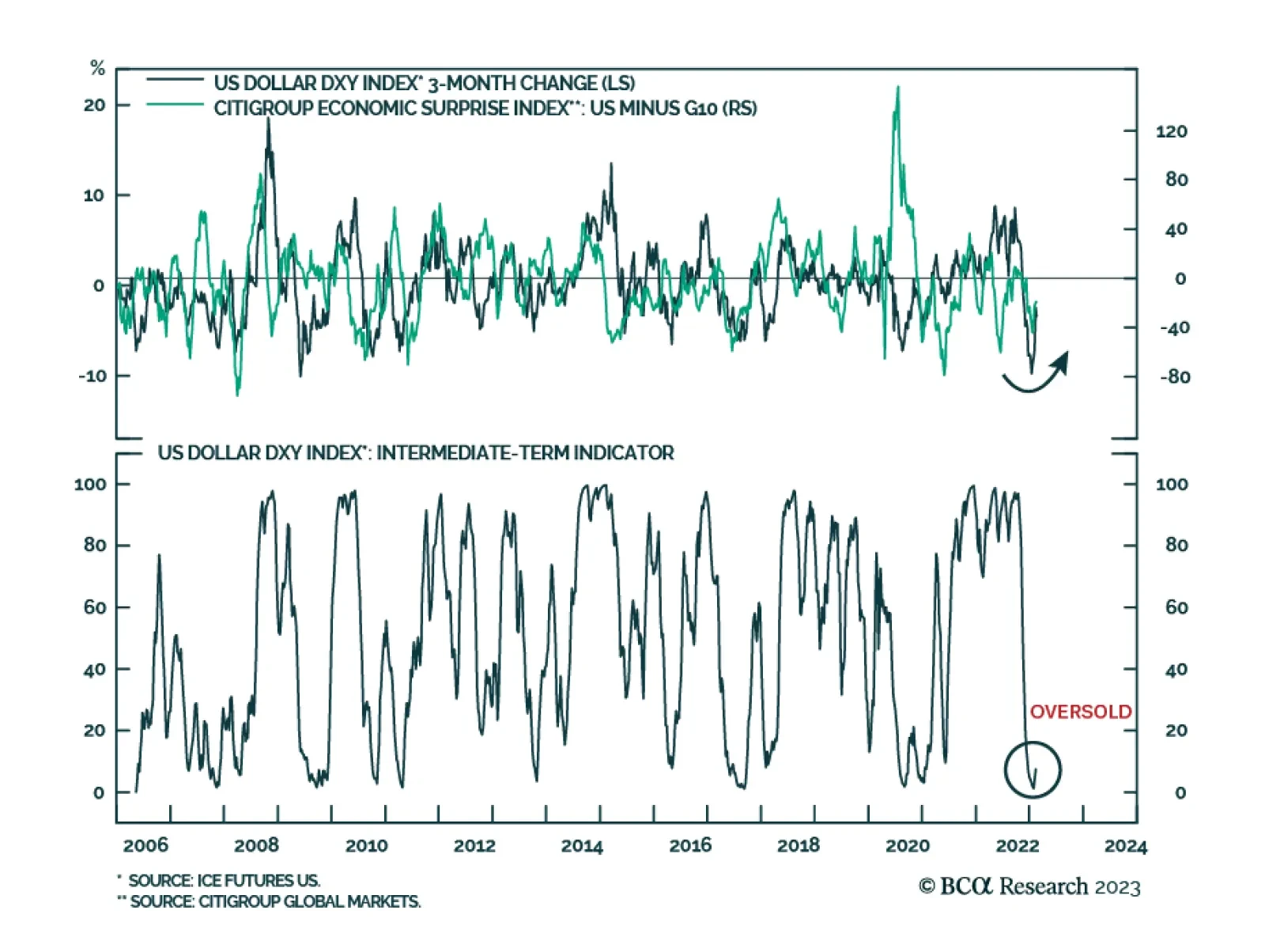

From a technical standpoint, the dollar is due for a bounce. In this report, we review various indicators to gauge the magnitude and duration of this rally. We also recommend two new trades: sell the gold/silver ratio at 90 and EUR/SEK at 11.30.

US data released on Thursday provide a mixed picture of economic conditions. On the one hand, results from the PPI report, New York Fed’s Business Leaders Survey and jobless claims corroborate the signal from the latest CPI, retail sales, JOLTS, and…

US retail sales delivered a positive signal about consumer demand in January. The 3.0% m/m increase – the largest since March 2021 – easily beat expectations of 2.0% m/m and marked a significant improvement from December’s 1.1% m/m decline. The retail…

US manufacturing sector indicators corroborate the positive signal about the US economy from the January retail sales report (see The Numbers). Although industrial output was flat in January, a 9.9% m/m drop in utilities – reflecting an unseasonably warm…

After declining by 11% between late-September and February 1, the DXY index has since gained 2%. Notably, this improvement in the dollar’s performance coincides with positive US economic data surprises over the past two weeks. In particular, nonfarm payroll…

Stocks have always underperformed bonds ahead of recessions, even during the inflationary 1970s. So, the current absence of underperformance of stocks versus bonds indicates that the markets are not yet priced for a recession. The main driver of stock…