United States

This week, we articulate what the actions of the three major central banks that met (Fed, ECB and BoE) mean for currency markets. This is within the context of our analysis of the latest data releases in the G10, that allows us to calibrate currency strategy.

Financial markets were taken on a wild ride between Wednesday and Friday of this week, with hugely important monetary policy meetings in the US, euro area and UK along with a rash of economic data. Despite all the news, noise and market volatility, the underlying message for monetary policy and bond yields in the US, euro area and UK is unchanged.

The US economy will experience a period of benign disinflation over the next few quarters. Beyond this goldilocks period, either the economy will slip into a mild recession in 2024, or more ominously, a second wave of inflation will prompt the Fed to slam on the brakes, leading to a deep recession.

This US Bond Strategy Insight discusses what we learned from yesterday’s FOMC meeting and press conference, and discusses the implications of the market’s reaction.

President Biden’s political capital has fallen as he enters a challenging year that will include a domestic faceoff with the House Republicans and foreign crises stemming from China, Russia, and Iran. Stay defensive and prefer bonds over equities.

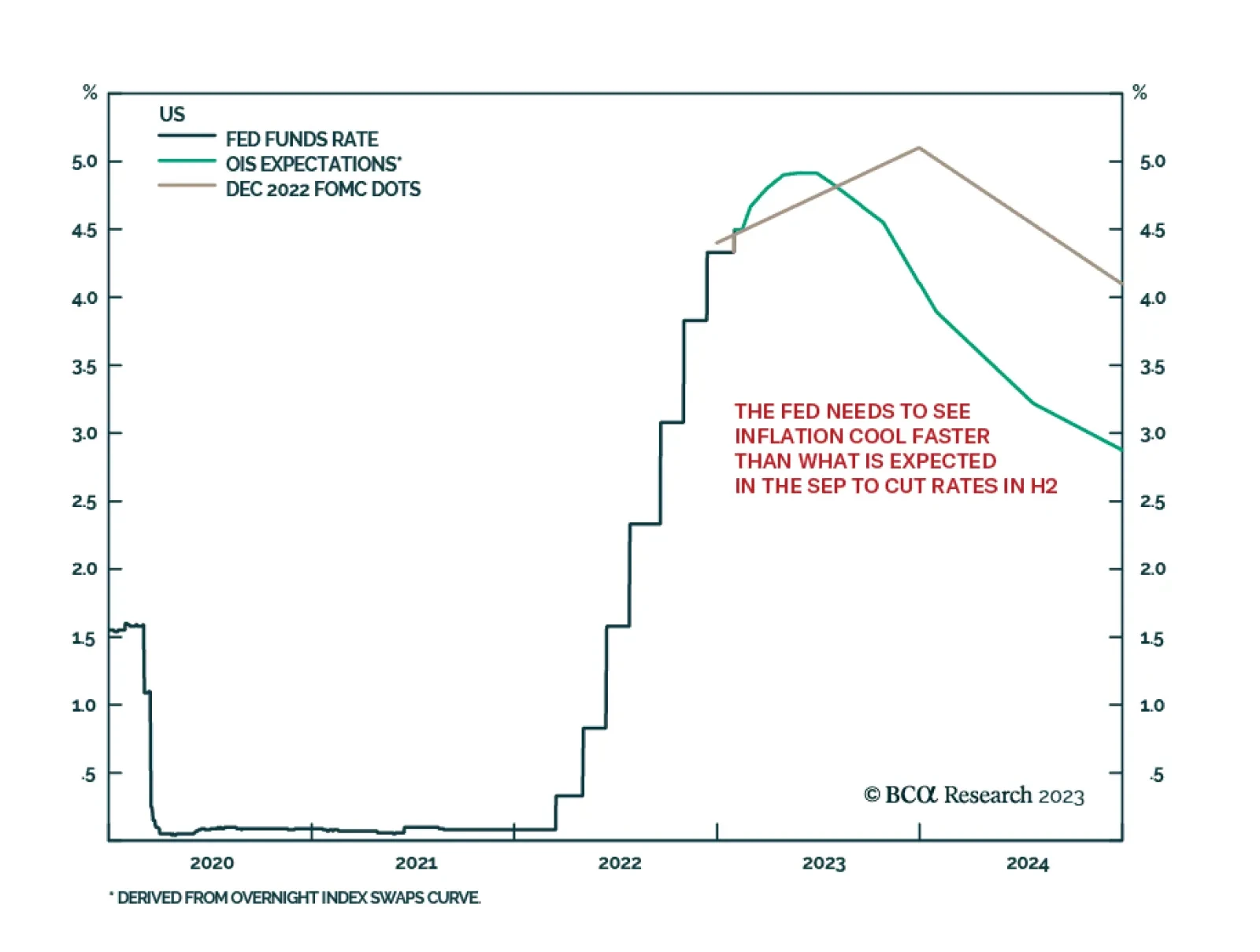

When does rising unemployment become a bigger problem than inflation? The Fed won't cut rates until that happens, probably thwarting market hopes of big cuts in 2H.

The Web 2.0 bubble is bursting, with far-reaching consequences for US stock market behaviour, sector allocation, and global asset allocation.